Precious Metals Market Size, Share & Industry Analysis, By Type (Silver, Gold, and Platinum Group Metals), By Application (Industrial, Jewelry, Investment, and Others), and Regional Forecast, 2026-2034

Precious Metals Market – Global Outlook 2026

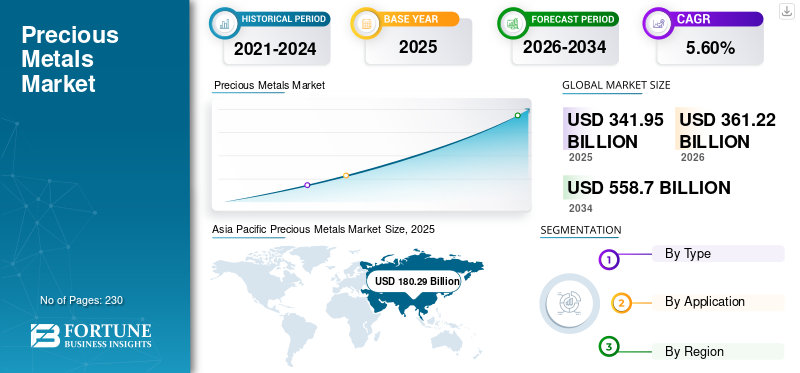

The global precious metals market size was USD 341.95 billion in 2025 and is projected to grow from USD 361.22 billion in 2026 to USD 558.70 billion by 2034 at a CAGR of 5.60% during the forecast period. Industry growth is driven by industrial demand expansion, inflation hedging behavior, energy transition requirements, jewelry consumption, and evolving investment allocation strategies. Asia Pacific dominated the market with a market share of 52.70% in 2025.

Increasing disposable incomes and changing lifestyle choices are a few of the factors driving the market. The demand for these metals is estimated to increase globally for jewelry and investment applications, as gold and silver are of prime importance in wedding ceremonies of Southeast Asian countries. Therefore, the rising population and increasing spending capacity of consumers in the region will contribute to the market growth.

The onset of the pandemic in January 2020 caused significant damage to the market. To mitigate the spread of the virus, manufacturing facilities and mining activities were temporarily shut down. The production of electronic products reduced as the demand from consumers declined. Key players functioning in the electrical & electronics industry were unable to acquire silver to produce printed circuit boards and composite boards.

For instance, according to the Silver Institute, the demand for silver for industrial applications declined by 5% in 2020. However, increasing investments in precious metals and in Gold Exchange-Traded Fund (ETFs) slowed the damage caused by the pandemic on the market. According to a study by the World Gold Council, global investment demand for gold increased by 40% in 2020, compared to 2019. Thus, this market is expected to thrive during the forecast period.

The global precious metals market continues functioning as both an industrial value chain and a strategic store-of-value ecosystem, shaped by macroeconomic uncertainty, industrial manufacturing demand, investment allocation behavior, and supply-side concentration. Gold, silver, and platinum group metals increasingly demonstrate differentiated demand profiles, reflecting varied exposure to jewelry consumption, industrial applications, technology manufacturing, and institutional investment strategies. Market behavior increasingly reflects cross-sector interdependence rather than commodity-specific demand in isolation.

The precious metals market remains strongly influenced by inflation expectations, monetary policy direction, and geopolitical instability. Gold continues to maintain importance within portfolio diversification strategies, particularly during periods of currency volatility, elevated sovereign risk, and financial market uncertainty. Silver demonstrates a dual-demand profile, balancing investment demand with expanding industrial consumption linked to solar technologies, electronics, and electrical conductivity requirements. Platinum group metals continue benefiting from automotive emissions systems, hydrogen-related technologies, and advanced industrial manufacturing applications.

Download Free sample to learn more about this report.

PRECIOUS METALS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 341.95 Billion

- 2026 Market Size: USD 558.70 Billion

- 2034 Forecast Market Size: USD 558.70 Billion

- CAGR: 5.60% from 2026–2034

- Asia Pacific dominated the precious metals market with a 52.70% share in 2025.

- The gold segment is projected to hold a dominant 55.65% market share in 2026.

- The industrial segment is projected to account for 48.89% of the market in 2026.

Asia Pacific

Asia Pacific led the global market with USD 180.29 billion in revenue in 2025 and is projected to reach USD 191.16 billion in 2026.

North America

North America accounted for 26.40% of the global market in 2025 and is expected to reach USD 95.40 billion in 2026.

Europe

Europe contributed 17.30% of global revenue in 2025 and is projected to reach USD 61.70 billion in 2026.

U.S.

The precious metals market is projected to reach USD 83.50 billion by 2026.

Japan

The precious metals market is projected to reach USD 17.22 billion by 2026.

Read More

Key Market Dynamics

Market Trends

Consistent Growth of the Industrial Sector Globally to Offer Lucrative Opportunities

The growth of end-use industries such as automotive and electrical & electronics is increasing the demand for these metals. The automotive industry is the major consumer of platinum and palladium, with the primary application in the catalytic converter. Additionally, the growing awareness about environmental pollution and changing regulations regarding carbon emissions from vehicles will substantially boost the demand for metals of the platinum group for application in catalytic converters.

Furthermore, the rapid expansion of the electrical & electronics industry, due to rising demand for consumer electronic products, will increase the consumption of silver. The rising demand for silver by solar panel manufacturers is aiding the demand for these metals, as silver has the ability to conduct electricity with the highest efficiency. As stated by the Silver Institute, photovoltaics accounted for 10.2% of the total silver market’s demand in 2020.

Precious metals market trends increasingly reflect the intersection of industrial technology demand and macroeconomic uncertainty. Gold continues functioning as a financial hedge during inflationary periods and geopolitical disruptions, while silver increasingly demonstrates stronger industrial relevance due to accelerating adoption in renewable energy systems and electronics manufacturing. This divergence continues to reshape demand composition across the precious metals industry.

Energy transition investment remains an important structural trend. Silver demand continues to expand within photovoltaic manufacturing because of its conductivity properties, while platinum group metals increasingly attract attention in hydrogen fuel cell development and electrolyzer technologies. Industrial applications are therefore becoming more important contributors to long-term demand visibility beyond traditional jewelry and investment consumption.

Recycling activity continues expanding across precious metals supply chains. Recovery of gold, silver, platinum, and palladium from electronics, automotive catalysts, and industrial waste streams increasingly supplements mined production. Recycling also supports supply diversification amid growing environmental scrutiny surrounding extraction activities and resource availability.

Download Free sample to learn more about this report.

Market Drivers

Increasing Disposable Income and Changing Lifestyle to Drive Growth

Inflating disposable income and changing lifestyle choices are the important factors driving the market growth. Additionally, the extensive importance of jewelry in wedding ceremonies of China, India, and other South Asian countries is projected to increase the consumption of precious metals. Furthermore, the perception of gold as a status symbol and safe haven for investment has significantly contributed to the growth of the market.

To avoid the risk of negative interest return rates from equities, bonds, or real estate, investors regularly flock towards gold as an asset that will maintain its value. For instance, as per the study by the World Gold Council, ETFs and other investments accounted for 23% of the total gold demand in 2020. Therefore, the aforementioned factors are expected to contribute to the precious metals market growth.

Rising Product Demand from Industrial Applications to Drive Market Growth

The rising demand for precious metals in industrial applications propels market growth due to their unique properties. Metals, such as gold, silver, and platinum, are prized for their higher conductivity, corrosion resistance, and catalytic capabilities, making them indispensable in the electrical & electronics, automotive, and healthcare sectors. For instance, gold is used in electronics for its conductivity and in healthcare for its biocompatibility.

Silver finds applications in solar panels and antimicrobial coatings. Platinum is essential in catalytic converters for vehicles, reducing emissions. The growing adoption of green technologies, such as electric vehicles and renewable energy systems, further boosts demand for these metals. As industries increasingly prioritize sustainability and innovation, the product demand for cutting-edge technologies continues to surge, driving their market growth.

The precious metals market continues benefiting from diversified demand drivers spanning investment allocation, industrial manufacturing, jewelry consumption, and strategic technology applications. Inflation concerns, monetary tightening cycles, currency depreciation, and geopolitical uncertainty continue supporting investment demand for gold and, to a lesser extent, silver. Institutional investors and central banks frequently increase precious metal allocations during periods of financial instability, strengthening long-term market resilience.

Industrial demand remains a significant growth contributor, particularly for silver and platinum group metals. Silver continues witnessing stronger consumption in photovoltaic systems, semiconductors, medical technologies, and electronics manufacturing due to its high electrical conductivity and corrosion resistance. Platinum and palladium remain essential within catalytic converters and emissions control technologies, while emerging hydrogen-related applications increasingly strengthen industrial relevance.

Jewelry consumption also continues supporting precious metals market growth, especially across Asia-Pacific and Middle Eastern economies, where cultural purchasing behavior influences gold and silver demand patterns. Seasonal buying cycles, wedding-related consumption, and rising disposable incomes continue shaping regional demand stability.

Market Restraints

Inconsistent Prices of Precious Metals to Impede Growth

The precious metals prices are heavily influenced by several factors such as inflation, currency fluctuations, government reserves, and geopolitical uncertainties. Owing to such instabilities in pricing, the demand and supply of these metals are severely affected, thereby impacting the industrial production activities. Additionally, the mining of precious minerals is a tedious task involving large capital in machinery, long working hours, and uncertainty of output, which is anticipated to hamper the growth. Furthermore, the inefficient polishing to preserve the luster and color of these metals will also hamper the market.

Price volatility continues to represent one of the most significant restraints within the precious metals market. Commodity pricing remains sensitive to interest rate movements, currency fluctuations, geopolitical developments, and investor sentiment shifts. Gold and silver frequently experience short-term price corrections when monetary tightening strengthens fixed-income attractiveness or reduces safe-haven investment activity.

Mining cost inflation also continues to affect supply economics. Rising labor costs, stricter environmental compliance requirements, energy price volatility, and declining ore quality increasingly pressure mining profitability. Exploration and permitting timelines often extend project development cycles, limiting near-term supply responsiveness and increasing capital expenditure requirements across extraction activities.

Substitution risk remains relevant across select industrial applications. Manufacturers occasionally reduce dependence on higher-cost precious metals by adopting alternative materials where performance requirements permit. Automotive manufacturers, for example, continue evaluating catalyst optimization strategies to reduce platinum group metal dependency amid pricing volatility and supply concentration concerns.

Market Opportunities

Industrial electrification and clean energy deployment continue to create substantial opportunities within the precious metals market. Silver demand increasingly benefits from photovoltaic installations, grid modernization, and advanced electronics manufacturing. Platinum group metals also continue expanding into hydrogen-related technologies, fuel cells, and industrial decarbonization systems, strengthening long-term industrial demand visibility.

Recycling infrastructure represents another important opportunity area. Recovery technologies for gold, silver, and platinum group metals continue improving as electronic waste volumes increase globally. Urban mining and advanced refining capabilities increasingly support material recovery, reduce supply concentration risk, and strengthen sustainability objectives across industrial value chains.

Investment diversification trends continue supporting market expansion. Institutional investors, sovereign wealth funds, and central banks increasingly evaluate precious metals as portfolio stabilizers during inflationary periods, currency volatility, and geopolitical uncertainty. Financial innovation, including exchange-traded products and digital trading access, continues to broaden participation across investment channels.

Precious Metals Market Segmentation Analysis

By Type Analysis

Gold Segment Held the Dominant Position in 2023, Driven by High Demand for Jewelry

Based on type, the precious metals market is segmented into silver, gold, and platinum group metals.

Gold

The Gold occupied segment is anticipated to hold a dominant market share of 55.65% in 2026. The growth of the segment is associated with increasing disposable income and growing knowledge about investments amongst consumers. Gold is extensively used for jewelry and investments due to its visual appeal and aesthetics. Developing countries in the Asia Pacific, such as India and China, are the major consumers of gold due to the rising spending capacity of individuals.

Gold continues accounting for a substantial share of the precious metals market due to its unique role across investment, jewelry, reserve holdings, and technology-related applications. Market demand remains strongly influenced by macroeconomic conditions, monetary policy expectations, inflation concerns, and geopolitical uncertainty. Central banks, institutional investors, and private wealth managers frequently view gold as a portfolio stabilizer during periods of financial volatility.

Investment demand remains one of the strongest pillars of gold consumption. Exchange-traded investment vehicles, bullion holdings, sovereign reserves, and wealth preservation strategies continue supporting market resilience. Gold typically demonstrates lower industrial dependence than silver or platinum group metals, making its demand profile more closely linked to financial market sentiment and currency stability. Monetary tightening, interest rate shifts, and inflation expectations continue to materially influence investment activity.

Jewelry consumption remains another important contributor to the precious metals market size, particularly across Asia-Pacific and Middle Eastern economies, where gold purchasing carries cultural and financial significance. Seasonal demand patterns, weddings, and gifting traditions continue supporting consumption stability. However, jewelry demand often demonstrates price sensitivity, particularly during periods of elevated gold valuation.

Silver

The silver segment will exhibit significant growth during the forecast period. The growth is characterized by rising demand for electrical & electronics applications. In addition, the low cost of silver compared to its counterparts poses an advantage for consumers for investments and jewelry.

Silver represents one of the most commercially diverse segments within the precious metals market due to its dual role as both an industrial input and an investment asset. Unlike gold, silver demand demonstrates stronger sensitivity to industrial production cycles because of widespread use across electronics, semiconductors, electrical systems, medical devices, and photovoltaic technologies. Conductivity, thermal efficiency, and corrosion resistance continue to support its relevance across advanced manufacturing environments.

Industrial demand continues to reshape silver consumption patterns. Solar photovoltaic expansion remains particularly important because silver paste is widely used in photovoltaic cells. Accelerating renewable energy deployment, electrification initiatives, and electronics miniaturization continue to support industrial silver demand. Semiconductor manufacturing and telecommunications infrastructure also contribute to sustained consumption growth, particularly as data processing and connectivity requirements expand globally.

Jewelry and silverware consumption continue supporting baseline demand, especially across emerging economies where affordability advantages improve accessibility relative to gold. Consumer purchasing remains influenced by pricing trends, disposable income, and cultural preferences. At the same time, recycling activity increasingly contributes to secondary supply as industrial recovery technologies improve. Silver, therefore, occupies a strategically important position within the precious metals market growth due to balanced exposure across industrial, investment, and consumer applications.

Platinum Group Metals

Platinum group metals are witnessing increasing demand for the auto-catalyst application. Owing to their highly efficient ability to capture carbon and other harmful emissions, industries are increasingly using platinum group metals to curb pollution and meet the environmental standards set by the government.

Platinum group metals (PGMs), including platinum, palladium, and rhodium, represent a strategically important segment within the precious metals market due to concentrated supply dynamics and strong industrial dependency. Unlike gold, which primarily reflects financial sentiment, platinum group metals demonstrate greater exposure to automotive production, industrial manufacturing, emissions control technologies, and emerging clean energy applications. Supply concentration remains a defining feature, with mining activity heavily centered in South Africa and Russia, increasing exposure to geopolitical and operational disruptions.

To know how our report can help streamline your business, Speak to Analyst

By Application Analysis

Industrial Segment to Occupy the Largest Market Share due to the Rising Product Demand from Photovoltaic Manufacturers

Based on the application, the precious metals market is segmented into industrial, jewelry, investments, and others.

Industrial

The industrial segment is projected to dominate the market with a share of 48.89% in 2026. The segment’s growth is driven by fueling demand for silver from photovoltaic manufacturers. Depleting fossil fuels has propelled the demand for solar panels, thereby boosting the segment growth.

Industrial applications account for a significant share of the precious metals market due to widespread use in electronics, semiconductors, medical technologies, renewable energy systems, automotive manufacturing, and chemical processing. Silver remains particularly important because of conductivity requirements across electronics and photovoltaic manufacturing, while platinum group metals continue to support emissions reduction systems and industrial catalysts. Gold also retains specialized industrial importance in aerospace systems, advanced electronics, and precision components, where corrosion resistance and conductivity remain essential.

Energy transition investment increasingly strengthens industrial demand visibility. Renewable power systems, battery technologies, hydrogen-related applications, and electrification infrastructure continue increasing industrial reliance on silver and platinum group metals. Semiconductor manufacturing and advanced communication systems also remain important consumption channels. Industrial demand, therefore, increasingly reflects structural technology shifts rather than short-term manufacturing cycles alone.

Jewelry

The jewelry segment is estimated to grow at a significant CAGR during the forecast period. The primary factor for the segment’s growth is the rising disposable income of consumers, hence driving the demand for jewelry. Gold and silver are the most preferred metals to produce jewelry due to their luster and malleability. The increasing demand for jewelry from consumers in Southeast Asia, owing to the importance of gold in wedding ceremonies, is fueling the segment's growth.

Jewelry remains one of the most established applications within the precious metals market, particularly for gold and silver. Consumer demand continues to reflect cultural purchasing traditions, discretionary income levels, gifting behavior, and ceremonial buying patterns. Asia-Pacific and Middle Eastern markets remain especially important because jewelry purchases frequently serve both ornamental and wealth preservation purposes.

Gold jewelry continues to account for a substantial share of global consumption due to cultural significance and long-term value retention characteristics. Silver jewelry demonstrates broader affordability, supporting stronger accessibility across price-sensitive consumer groups. Platinum jewelry also maintains relevance within premium categories where exclusivity and durability influence purchasing behavior.

Investment

The investment application is calculated to be the fastest-growing segment during the forecast period. The increasing investments in a commodity such as gold due to its low-risk factor compared to other investments are augmenting the segment growth. Additionally, the drop in gold prices amidst the COVID-19 pandemic provided investors a new opportunity to increase their wealth, thereby resulting in the segment’s growth.

Investment applications continue representing a core demand pillar within the precious metals market, particularly for gold and silver. Precious metals frequently function as portfolio diversification tools during inflationary periods, financial market instability, and currency depreciation concerns. Institutional investors, sovereign wealth funds, central banks, and private wealth managers continue allocating precious metals within broader risk management strategies.

Gold remains the dominant investment metal because of its reserve asset status and lower relative volatility. Silver investment demand often demonstrates stronger cyclical movement because industrial exposure influences pricing dynamics. Exchange-traded products, bullion holdings, coins, and digital trading platforms continue improving market accessibility across investor categories.

Regional Insights

Asia-Pacific Precious Metals Market Analysis

Asia Pacific Precious Metals Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for USD 180.29 billion in 2025, representing 52.70% of the global market share, and is projected to reach USD 191.16 billion in 2026. The region held a dominant share of the market in 2023 and is expected to retain the leading position throughout the forecast period. The domination is attributed to the presence of the largest electrical & electronics industry in the region.

China and India have the widest influence on the market, owing to the countries being major consumers of gold. These countries are rapidly expanding their industrial sector by partnering with foreign investors and international companies, which are expected to boost the demand. The Japan market is projected to reach USD 17.22 billion by 2026, the China market is projected to reach USD 146.68 billion by 2026, and the India market is projected to reach USD 18.73 billion by 2026.

Asia-Pacific accounts for a substantial precious metals market share due to strong jewelry consumption, industrial manufacturing, and investment activity. China, India, and Japan continue driving regional demand across gold, silver, and platinum group metals. Renewable energy investment, electronics manufacturing, and rising household wealth continue supporting long-term precious metals market growth throughout the region.

Japan Precious Metals Market

Japan continues to support the precious metals market demand through advanced manufacturing, electronics production, and automotive technologies. Platinum group metals remain important across industrial and automotive applications, while gold investment demand reflects portfolio diversification preferences. Recycling infrastructure and technological innovation continue supporting material recovery and efficient resource utilization across precious metals value chains.

China Precious Metals Market

China represents one of the largest precious metals market participants due to strong industrial demand, jewelry consumption, and gold investment activity. Silver demand continues benefiting from solar photovoltaic manufacturing and electronics production. Industrial expansion, renewable energy investment, and rising household income continue to strengthen the precious metals market size across multiple application segments.

To know how our report can help streamline your business, Speak to Analyst

North America Precious Metals Market Analysis

The North American market generated USD 90.2 billion in 2025, representing 26.40% of the global market landscape, and is expected to reach USD 95.4 billion in 2026. The presence of major precious minerals mines in the vicinity of the region, combined with the strong manufacturing capabilities of the U.S., is likely to fuel the market growth.

The U.S. market is projected to reach USD 83.5 billion by 2026. Moreover, the precious metals market in the U.S. is projected to grow significantly, reaching an estimated value of USD 117.78 billion by 2032, driven by increasing demand for gold and silver as safe-haven assets amid economic uncertainty.

North America remains an important precious metals market due to established mining infrastructure, investment demand, refining capabilities, and industrial consumption. Gold and silver production continue to support regional supply, while investment activity remains sensitive to inflation expectations and monetary policy direction. Industrial demand for silver and platinum group metals continues to benefit from renewable energy and technology manufacturing.

United States Precious Metals Market

The United States accounts for a substantial share of the precious metals market through investment activity, industrial consumption, and refining operations. Gold investment demand remains influenced by inflation concerns, monetary policy expectations, and portfolio diversification behavior. Industrial silver demand continues to expand across electronics, solar manufacturing, and advanced technologies, supporting broader precious metals market growth.

Europe Precious Metals Market Analysis

Europe contributed 17.30% to the global market in 2025, with a valuation of USD 59.2 billion, and is projected to reach USD 61.7 billion in 2026. Europe will witness a significant rise in demand for precious metals from industrial applications. The major automotive countries in the region are substantially contributing to the rise in demand.

Furthermore, the rise in the consumption of jewelry owing to the expansion of the fashion industry in the region will support the growth. The UK market is projected to reach USD 10.58 billion by 2026, while the German market is projected to reach USD 15.15 billion by 2026.

Europe represents a mature precious metals market supported by industrial manufacturing, automotive demand, jewelry consumption, and investment activity. Platinum group metals remain important due to automotive catalyst requirements and industrial processing applications. Sustainability requirements, recycling infrastructure, and renewable energy expansion continue to strengthen regional silver demand across photovoltaic and electronics manufacturing sectors.

Germany Precious Metals Market

Germany continues to contribute significantly to the precious metals market through automotive manufacturing, industrial processing, and advanced engineering sectors. Platinum group metals remain relevant for automotive emissions technologies, while silver demand benefits from electronics and renewable energy systems. Industrial recycling activity and advanced refining capabilities continue to strengthen material recovery and supply resilience.

United Kingdom Precious Metals Market

The United Kingdom's precious metals market remains supported by investment demand, refining activities, and financial market participation. Gold continues to maintain importance within wealth preservation strategies and institutional portfolio diversification. Jewelry demand and industrial consumption remain comparatively stable, while London’s global trading role continues to influence broader precious metals market liquidity and pricing activity.

Middle East & Africa Precious Metals Market Analysis

In 2025, the Middle East & Africa held 2.20% of the global market, reaching a valuation of USD 7.66 billion, and is projected to grow to USD 8.06 billion in 2026. The growth of the precious metals market in the Middle East & Africa is characterized by high demand from Gulf countries. High demand from jewelry and industrial applications will drive the market in the region. Latin America will witness significant growth in the market owing to the high demand for industrial applications.

The Middle East & Africa continue to support precious metals market activity through gold mining, jewelry demand, and investment consumption. Gold purchasing remains culturally significant across several regional economies. Mining development, refining investment, and changing regulatory frameworks continue influencing supply capacity, while industrial demand remains comparatively concentrated in selected sectors.

Latin America Precious Metals Market Analysis

Latin America contributed approximately USD 4.62 billion to the global market in 2025, accounting for 1.40% share, and is expected to reach USD 4.85 billion in 2026. Latin America remains an important contributor to the precious metals market due to substantial mining activity and growing refining capabilities.

Gold and silver production continue to support global supply chains, while investment and jewelry demand remain comparatively moderate. Regulatory developments, environmental requirements, and mining investment continue shaping regional market dynamics and supply stability.

Precious Metals Industry Competitive Landscape

Joint Ventures and Acquisition of Mines Will Increase the Presence of Key Companies

Key players are implementing approaches such as joint ventures to investigate and mine precious minerals. The major companies are likely to focus on large reserves in the African region, which are unexplored. New precious mineral mining projects sanctioned to private companies and regulated by the governments are likely to support the rising demand. To expand its presence and to fulfill the demand for gold in the future, Newmont Corporation is focused on acquiring mining sites and forming partnerships.

The precious metals market demonstrates a moderately concentrated competitive structure shaped by diversified mining companies, specialized producers, refiners, recycling firms, commodity traders, and downstream industrial processors. Competitive positioning depends heavily on reserve quality, geographic diversification, refining capabilities, production cost efficiency, environmental compliance, and access to stable extraction jurisdictions. Companies increasingly compete not only through mining scale but also through supply resilience and downstream integration.

Major global vendors continue focusing on operational efficiency, reserve replacement strategies, and geographic diversification to reduce exposure to political and supply concentration risks. Large mining firms with diversified exposure across gold, silver, and platinum group metals generally maintain stronger resilience during commodity price fluctuations because revenue streams remain distributed across multiple metals and jurisdictions. Exploration investment, acquisition activity, and long-term production planning continue shaping competitive positioning within the precious metals industry.

Gold-focused producers increasingly prioritize low-cost production assets, operational stability, and disciplined capital allocation. Silver producers continue strengthening exposure to industrial demand growth associated with electronics, renewable energy systems, and electrification infrastructure. Platinum group metal producers remain highly influenced by automotive demand cycles and hydrogen-related technology development, encouraging investment in long-term industrial partnerships and recycling capabilities.

LIST OF KEY COMPANIES PROFILED:

- Newmont Corporation (U.S.)

- Barrick Gold Corporation (Canada)

- AngloGold Ashanti Limited (South Africa)

- Kinross Gold Corporation (Canada)

- Newcrest Mining Limited (Australia)

- Gold Fields Limited (South Africa)

- Freeport-McMoRan (U.S.)

- Wheaton Precious Metals (Canada)

- Anglo American Platinum Limited (South Africa)

- Impala Platinum Holdings Limited (South Africa)

KEY INDUSTRY DEVELOPMENTS:

- March 2025: Anglo American Platinum announced continued investment in platinum group metal processing optimization and operational restructuring to improve production efficiency and cost discipline amid evolving automotive catalyst demand. The initiative focused on refining capabilities, smelter optimization, and operational resilience measures to strengthen platinum group metal supply stability and long-term competitiveness.

- February 2025: Newmont Corporation expanded investment in digital mining technologies and ore processing optimization to improve operational productivity and asset efficiency across precious metals extraction sites. The initiative aimed to strengthen production visibility, reduce operational variability, and enhance mine planning capabilities through advanced analytics, automation systems, and predictive maintenance technologies.

- October 2024: Barrick Gold Corporation advanced exploration and mine-life extension programs across selected gold assets to strengthen reserve replacement and long-term production continuity. The strategy emphasized geological modeling, resource expansion, and operational optimization capabilities to improve extraction efficiency while supporting long-term precious metals supply resilience.

- September 2024: Sibanye-Stillwater expanded precious metal recycling activities to strengthen secondary platinum group metal supply and reduce exposure to mining concentration risks. The initiative focused on catalytic converter recycling, metallurgical recovery technologies, and refining efficiency improvements to support circular supply chain capabilities within industrial precious metals applications.

- June 2024: Wheaton Precious Metals strengthened long-term streaming agreements to improve supply access and production visibility across gold and silver assets. The strategy emphasized diversified sourcing exposure, capital discipline, and portfolio optimization capabilities to improve operational resilience and long-term market positioning within the precious metals industry

- November 2023: Wheaton Precious Metals announced that it has agreed with Orion Mine Finance to acquire the Kudz Ze Kayah and Platreef projects. It also announced the purchase of a gold stream for Dalradian Gold's Curraghinalt Project. The move is anticipated to strengthen the company’s market position significantly.

- May 2021: Newmont Corporation completed the acquisition of GT Gold by acquiring the remaining 85.1% shares of the company. With the acquisition, the company strengthened its portfolio. The acquisition includes the Tatogga project, which will contribute to the production of copper and gold in the future.

- April 2021: Barrick Gold Corporation’s Loulo-Gounkoto’s third underground mine to start delivering gold. The mine is estimated to produce an output of 19.8 tons of gold by the end of 2021.

REPORT COVERAGE

The market research report provides a detailed industry analysis and focuses on key aspects, such as profiles of leading companies, types of precious metals, and leading applications of these metals. Besides this, it offers insights into the current precious metals market trends, dynamics, and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the advanced precious metals industry over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.60% during 2026-2034 |

|

Unit |

Volume (Kiloton); Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Application

|

|

|

By Geography

|

Frequently Asked Questions

According to Fortune Business Insights, the global precious metals market was valued at USD 341.95 billion in 2025 and is projected to grow to USD 558.70 billion by 2034, exhibiting a CAGR of 5.60% during the forecast period.

Key growth drivers include rising disposable incomes, increased investment in gold and silver as safe-haven assets, and expanding industrial use in automotive, electronics, and solar energy sectors.

Registering a CAGR of 5.60%, the market will exhibit decent growth over the forecast period (2026-2034).

Asia Pacific dominated the precious metals market with a market share of 52.70% in 2025.

Precious metals are widely used in industrial applications (e.g., solar panels, electronics), jewelry manufacturing, and investment instruments like gold ETFs and bullion.

Gold leads the market in terms of demand and revenue, primarily due to its extensive use in jewelry and investment portfolios, especially in emerging economies.

Leading players include Newmont Corporation, Barrick Gold, AngloGold Ashanti, Kinross Gold, and Wheaton Precious Metals, all of which are expanding through acquisitions and joint ventures.

- 2021-2034

- 2025

- 2021-2024

- 230

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us