Precision Machining Market Size, Share & Industry Analysis, By Control Type (Manual and CNC), By Process Type (Milling, Turning, Electrical Discharge Machining (EDM), Grinding, Drilling, and Others), By End User (Automotive, Aerospace and Defense, Medical, Industrial Machinery, Electronics, and Others), and Regional Forecast, 2026-2034

Precision Machining Market Size and Future Outlook

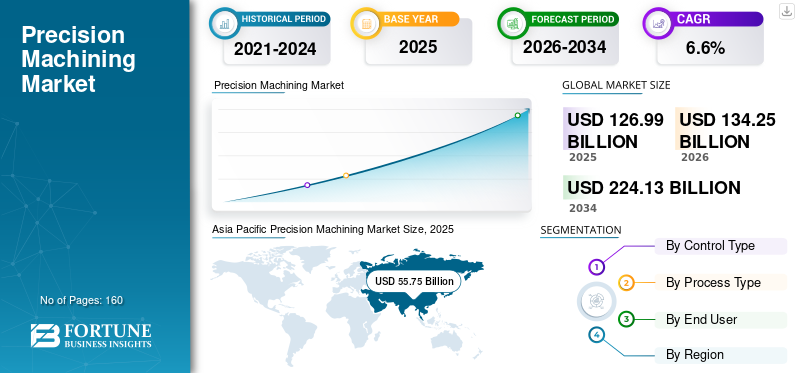

The global precision machining market size was valued at USD 126.99 billion in 2025. The market is projected to grow from USD 134.25 billion in 2026 to USD 224.13 billion by 2034, exhibiting a CAGR of 6.6% during the forecast period. Asia Pacific dominated the precision machining market with a market share of 43.9% in 2025.

The market plays a critical role in supporting modern manufacturing by delivering high-tolerance components required across multiple manufacturing sectors, including automotive, aerospace, medical, and electronics. The need for high accuracy, improved surface finishes, and complex part geometries in advanced industrial applications drives the growing demand for precision machining. As advanced manufacturers increasingly adopt automation, multi-axis CNC systems, and digital production technologies, precision machining continues to evolve toward smarter and more efficient production environments. In addition, the rise of additive manufacturing is complementing traditional subtractive machining processes, particularly in hybrid production models where printed components require high-precision finishing. The expansion of manufacturing activities in both developed and emerging market economies further supports the industry's sustained long-term growth.

Key players such as DMG MORI, Yamazaki Mazak, Okuma, and Makino continue to strengthen their positions by expanding multi-axis CNC platforms, automation-ready machining solutions, and digital monitoring capabilities to serve high-precision industrial requirements.

Download Free sample to learn more about this report.

PRECISION MACHINING MARKET TRENDS

Rising Multi-Axis CNC Adoption and Digital Machining Integration are Transforming Precision Manufacturing

The precision machining market is increasingly driven by the adoption of advanced multi-axis CNC machining centers and digital manufacturing technologies. According to industry data, CNC equipment accounts for the majority of new machine tool installations globally, reflecting the shift toward automated, high-accuracy production environments. The growing use of five-axis machining allows manufacturers to reduce setups, improve tolerance control, and increase productivity in aerospace and medical applications.

Major manufacturers such as DMG MORI and Mazak have expanded their multi-tasking and five-axis CNC platforms in recent years to meet demand for complex part machining. Additionally, integrating data analytics and machine monitoring software enables predictive maintenance and real-time performance optimization, supporting Industry 4.0 transformation across machining facilities.

Download Free sample to learn more about this report.

MARKET DRIVERS

Increasing Demand for High-Tolerance Components across EV, Aerospace, and Medical Sectors are Accelerating Market Growth

The shift toward electric vehicles, lightweight aerospace structures, and precision medical devices is significantly increasing demand for high-tolerance machined components. EV drivetrains, battery housings, and power electronics require advanced milling and turning processes with tight dimensional control. Aerospace manufacturers continue to expand production backlogs, driving demand for precision aluminum and titanium components.

The International Energy Agency has highlighted strong global EV production growth, which directly increases demand for precision-machined motor shafts, gear components, and structural housings. Similarly, the global recovery in aircraft production is reinforcing demand for machining of engine and structural components. These structural industry expansions continue to drive steady growth in the precision machining market.

MARKET RESTRAINTS

Skilled Workforce Shortages and Capital Intensity Pose Structural Challenges

Precision machining requires highly skilled operators, programmers, and engineers who can manage advanced CNC systems. Many industrial regions report shortages of skilled machinists, which can limit the expansion of production capacity. Additionally, high-end multi-axis machining centers and automation integration involve significant capital investment.

Industry reports from manufacturing associations frequently highlight the difficulty in recruiting trained machinists and CNC programmers. Small and mid-sized machine shops often face financial barriers when upgrading to advanced automation systems. These factors can moderate adoption rates, particularly in developing markets.

MARKET OPPORTUNITIES

Semiconductor Equipment Expansion and Reshoring Initiatives Create Long-Term Growth Potential

The growth in semiconductor fabrication facilities and the reshoring of advanced manufacturing to North America and Europe present strong opportunities for precision machining providers. Semiconductor equipment manufacturing requires ultra-precise components with extremely tight tolerances and advanced surface finishing.

Recent investments in semiconductor fabrication plants in the U.S. and Asia Pacific are expected to increase demand for precision-machined components used in lithography and processing equipment. Additionally, government-backed manufacturing incentives are encouraging expansion of local production capacity, creating sustained, long-term demand for advanced machining services.

Segmentation Analysis

By Process Type

Milling Segment Dominates Due to Versatility in Producing Complex Geometries

Based on the process type, the market is divided into milling, turning, Electrical Discharge Machining (EDM), grinding, drilling, and others.

In 2025, the milling segment accounted for the largest precision machining market share. Milling remains dominant due to its versatility in producing complex geometries, structural housings, engine components, and aerospace parts. The expansion of five-axis and multi-tasking machining centers has significantly increased milling efficiency and part complexity capability. Leading machine tool manufacturers such as DMG MORI and Mazak have introduced advanced milling platforms that support automation integration and real-time monitoring, reinforcing the segment's leading position.

The Electrical Discharge Machining (EDM) segment is anticipated to rise with a CAGR of 7.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Control Type

CNC Holds the Largest Share Due to Automation and Repeatability Advantages in the Machine

Based on the control type, the market is bifurcated into manual and CNC.

In 2025, the CNC segment held the largest market share. CNC machining provides superior precision, repeatability, and reduced human error compared to manual machining. The majority of new machine tool installations globally are CNC-based, reflecting the shift toward digital manufacturing. Automation integration, robotic loading systems, and AI-assisted machining optimization further strengthen CNC dominance. As manufacturers adopt smart factory initiatives, CNC systems continue to expand across both developed and emerging industrial regions.

The CNC segment is expected to grow at a CAGR of 6.7% over the forecast period.

By End User

Automotive Segment Leads the Market Due to High Production Volume and EV Expansion

Based on the end user, the market is segmented into automotive, aerospace and defense, medical, industrial machinery, electronics, and others.

In 2025, the automotive segment accounted for the largest share of the precision machining market. Automotive production requires large volumes of precision components, including engine parts, transmission systems, EV motor housings, and battery structural components. The rapid expansion of electric vehicle production has further increased demand for precision-machined lightweight components. Global EV sales growth, highlighted by international energy data agencies, continues to reinforce demand for machining across drivetrain and powertrain components.

The electronics segment is expected to grow at a CAGR of 7.7% over the forecast period.

Precision Machining Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

The North America market is projected to reach USD 27.76 billion in 2026. The region's precision machining market growth is supported by aerospace and defense manufacturing, electric vehicle production, and medical device fabrication. Ongoing reshoring initiatives and capital investments in advanced CNC machining centers are expected to strengthen domestic precision manufacturing capabilities.

U.S. Precision Machining Market

The U.S. market is projected to reach around USD 23.07 billion in 2026. Strong demand from aerospace manufacturers, defense contractors, and EV production facilities is driving continued investments in multi-axis CNC and automated machining systems.

Europe

The European market is projected to reach USD 32.69 billion in 2026. The region benefits from a strong automotive manufacturing base in Germany and Italy, as well as aerospace production and industrial machinery exports. Emphasis on high-quality engineering standards and precision-driven manufacturing processes is expected to sustain demand for advanced machining services.

U.K Precision Machining Market

The U.K. market is projected to reach USD 3.83 billion in 2026, equivalent to around 2.9% of global sales.

Germany Precision Machining Market

Germany's market is projected to reach USD 9.12 billion in 2026, equivalent to around 6.8% of global sales.

Asia Pacific

Asia Pacific held a dominant position in the market in 2024 and maintained its leading share in 2025, with a market valuation of USD 55.75 billion. The region is expected to maintain its market leadership due to its strong manufacturing ecosystem across China, Japan, South Korea, and India. Rapid expansion in automotive production, electronics manufacturing, and semiconductor equipment fabrication is supporting sustained demand for high-tolerance machined components. China remains the largest contributor, while India is anticipated to register the fastest growth within the region due to increasing industrialization and government manufacturing initiatives.

Asia Pacific Precision Machining Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Japan Precision Machining Market

Japan's market is projected to reach USD 12.06 billion in 2026, equivalent to around 9.0% of global sales.

China Precision Machining Market

China's market is estimated to reach USD 22.30 billion in 2026, equivalent to around 16.6% of global sales.

India Precision Machining Market

India's market is anticipated to reach USD 6.75 billion in 2026, equivalent to around 5.0% of global sales.

South America and the Middle East & Africa

The South America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. South America is projected to reach a market valuation of USD 7.87 billion in 2026. The growth is expected to be supported by automotive production in Brazil and gradual industrial modernization initiatives across the region. The Middle East & Africa market is expected to reach USD 6.64 billion in 2026. The growth is expected to be supported by automotive production in Brazil and gradual industrial modernization initiatives across the region.

GCC Precision Machining Market

GCC's market is set to reach USD 2.77 billion in 2026, equivalent to around 2.1% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Multi-Axis CNC Innovation and Digital Machining Ecosystems to Drive Competitive Positioning

Stronger competition exists in the global machine tool industry, especially from machine manufacturers and machining technology providers focused on advanced CNC systems, enabling automation integration into products such as aero engine component forming. DMG Mori's (DMM) and Alliant have also developed CNC systems for their own use. The combination of machine tool manufacturers' efforts to differentiate themselves with their respective multi-axis machining systems and their continued investment in developing digital CNC systems, along with the automation and integration of existing manufacturing processes, supports greater product productivity and improves production accuracy and precision.

For example, companies such as DMG Mori and Mazak continue to contribute positively to the industry by using machine tools to manufacture aerospace, automotive, and medical products. Many of the competing companies that comprise the machine tool industry use additional tooling or electrical discharge machining ("EDM") technologies in high-precision/high-tolerance applications, supporting a greater breadth of products manufactured by the machine tool industry. The primary focus of the entire industry remains on improving its manufacturing capabilities and systems through newer/different five-axis machining technologies, mill-turn center systems, and the ability to integrate automation. Continued innovation in the machine tool industry is critical to maintaining a competitive edge against other machine tool manufacturers and their respective industries.

LIST OF KEY PRECISION MACHINING COMPANIES PROFILED

- DMG MORI Co., Ltd. (Japan)

- Yamazaki Mazak Corporation (Japan)

- Okuma Corporation (Japan)

- Makino Milling Machine Co., Ltd. (Japan)

- FANUC Corporation (Japan)

- Sandvik AB (Sweden)

- Haas Automation, Inc. (U.S.)

- DN Solutions (South Korea)

- GF Machining Solutions (Switzerland)

- HERMLE AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- September 2024: Makino launches DA500 5-axis vertical machining center at AMB 2024. Makino emphasized combining milling and turning on a single platform to reduce setups and improve machining accuracy, which is relevant for aerospace engine and semiconductor manufacturing parts.

- May 2024: Mazak announces it will unveil new and expanded product lines at IMTS 2024. Mazak outlined additions across multiple machine series and highlighted automation and digital solutions, including monitoring features using real-time continuous data concepts.

- December 2023: Sandvik completes acquisition of Buffalo Tungsten. Sandvik confirmed completion of the transaction, reinforcing local supply capability for tungsten powder and carbide-related inputs used across machining applications.

- October 2023: Sandvik to acquire tungsten powder manufacturer Buffalo Tungsten. Sandvik announced an agreement to acquire Buffalo Tungsten to strengthen North American tungsten powder capabilities and support the machining value chain.

- September 2023: DMG MORI introduces INH 63 and INH 80 high-accuracy 5-axis horizontal machining centers. The company positioned the machines around higher static/dynamic/volumetric accuracy and automation-ready productivity for demanding precision applications.

REPORT COVERAGE

The global precision machining market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details strategic partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Control Type, Process Type, End User, and Region |

| By Control Type |

|

| By Process Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 126.99 billion in 2025 and is projected to reach USD 224.13 billion by 2034.

In 2026, the market value will stand at USD 27.76 billion.

The market is expected to exhibit a CAGR of 6.6% during the forecast period.

By control type, the CNC segment is expected to lead the market.

The rising demand for high-tolerance components in the EV, aerospace, and medical industries is driving steady market growth.

DMG MORI, Yamazaki Mazak, Okuma, and Makino are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us