Premium Bottled Water Market Size, Share & Industry Analysis, By Product Type (Sparkling, Flavored, Functional, Mineral/Spring, and Purified), By Packaging Type (Premium PET Bottles, Glass Bottles, Metal Cans, and Others), By Price Tier (Premium, Super Premium, and Luxury/Ultra-premium), By Distribution Channel (Off-trade, On-trade, Online Channels, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

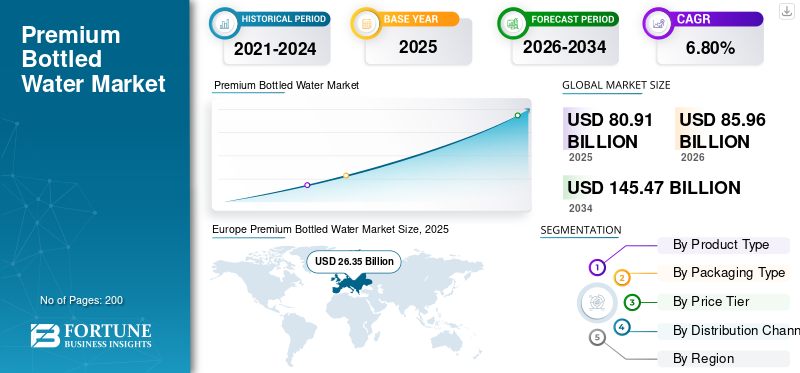

Premium Bottled Water Market Size and Future Outlook

The global premium bottled water market size was valued at USD 80.91 billion in 2025. The market is projected to grow from USD 85.96 billion in 2026 to USD 145.47 billion by 2034, exhibiting a CAGR of 6.80% during the forecast period. Europe dominated the premium bottled water market with a market share of 32.56% in 2025.

Premium bottled water includes high-quality natural mineral water, spring water, sparkling water, and value-added hydration products positioned at higher price points due to their source quality, mineral composition, health benefits, brand image, and sustainability packaging differentiation. Demand is being supported by rising consumer preference for healthier beverages, premium lifestyle products, and functional hydration offerings across retail and foodservice channels. The market is also benefiting from innovation in flavored, electrolyte-enhanced, and sustainably packaged water formats.

The global market demand is led by key companies, including Nestlé S.A., Danone S.A., PepsiCo, Inc., The Coca-Cola Company, San Pellegrino, and FIJI Water Company LLC. These companies are primarily competing through premium brand building, functional and flavored water innovation, source-led product positioning, and sustainable packaging strategies.

Download Free sample to learn more about this report.

Premium Bottled Water Market Key Takeaways

- 2025 Market Size: USD 80.91 billion

- 2026 Market Size: USD 85.96 billion

- 2034 Forecast Market Size: USD 145.47 billion

- CAGR: 6.80% from 2026–2034

- Europe dominated the premium bottled water market with a 32.56% share in 2025.

- The mineral/spring segment led the market and was valued at USD 30.64 billion in 2025.

- The premium PET bottles segment held the largest market share, reaching USD 46.71 billion in 2025.

Europe

Europe reached USD 26.35 billion in 2025 and is projected to reach USD 39.40 billion by 2034 at a CAGR of 5.76%.

North America

North America was valued at USD 18.99 billion in 2025 and is expected to reach USD 31.28 billion by 2034 at a CAGR of 6.80%.

Asia Pacific

Asia Pacific reached USD 25.99 billion in 2025 and is projected to grow to USD 54.77 billion by 2034 at the fastest CAGR of 8.68%.

U.S

The market was valued at USD 12.29 billion in 2025, supported by strong demand for premium and functional bottled water.

Japan

The market showed steady growth driven by rising demand for premium hydration and packaged drinking water products.

Read More

Premium Bottled Water Market Trends

Increasing Consumer Shift Toward Healthier Hydration and Premium Beverage Choices to Shape Industry Trends

Consumers globally are shifting away from carbonated and sugary beverages toward healthier hydration, driving increased demand for the product. This shift is driven by increasing awareness of lifestyle-related health conditions and the growing adoption of wellness-oriented consumption habits. Brands are capitalizing on this trend by introducing functional variants such as electrolyte-enhanced, alkaline, and vitamin-infused water, along with innovative packaging and branding strategies targeting affluent and urban conscious consumers.

- For instance, in March 2026, Ghodawat Consumer Limited (GCL), part of the Sanjay Ghodawat Group, recently launched TBH Coconut Water under its "To Be Honest" (TBH) brand to enter India's growing natural hydration market. This marks an expansion of TBH's clean-label portfolio from healthy snacks into functional beverages, emphasizing 100% natural coconut water with no added sugar, concentrates, or artificial flavors.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Global Consumption of Packaged and Health-Oriented Beverages to Support Market Growth

The increasing global consumption of packaged beverages, particularly healthier alternatives, is a key driver for the market. As consumers become more health-conscious, demand for beverages free of sugar, artificial additives, and preservatives has significantly increased. Urbanization, rising disposable incomes, and changing dietary habits are further contributing to the global premium bottled water growth, especially in emerging economies, where consumers are trading up from standard tap water to premium offerings.

- According to the Food and Agriculture Organization (FAO), global trade in processed and packaged food and beverage products exceeded USD 1.5 trillion in 2023, reflecting strong demand for packaged consumption products.

Market Restraints

Regulatory Compliance and Labeling Standards Across Regions to Restrict Market Expansion

The market is subject to complex and highly fragmented regulatory frameworks across regions, creating significant compliance challenges for manufacturers. Regulations govern multiple aspects, including water source classification (mineral, spring, purified), permissible treatment processes, mineral content disclosure, labeling requirements, and packaging standards. Companies operating across multiple geographies must adapt to region-specific regulatory definitions and certification processes, increasing operational complexity, compliance costs, and time-to-market for new product launches.

- According to the European Commission, natural mineral water must comply with Directive 2009/54/EC, which mandates strict source protection, microbiological purity, and detailed mineral composition labeling, limiting processing flexibility. Another instance, the U.S. FDA requires bottled water to meet standards under 21 CFR Part 165, including identity, quality, and labeling regulations, with mandatory disclosure of treatment methods such as reverse osmosis or distillation.

These regulatory variations and compliance requirements increase costs, delay product approvals, limit formulation flexibility, and create barriers for small and mid-sized players entering new markets, thereby restraining overall market expansion.

Market Opportunities

Expansion of Sustainable Packaging and Premiumization Strategies to Create Growth Opportunities

The shift toward sustainability presents a major opportunity for brands. Companies are investing in eco-friendly packaging formats, carbon-neutral production processes, and ethically sourced water to align with evolving consumer expectations. Additionally, premiumization strategies such as luxury branding, limited-edition packaging, and functional water innovations (alkaline, electrolyte-enhanced, vitamin-infused) are creating new revenue streams and differentiation in a competitive market. These efforts drive premium bottled water market growth.

- For instance, in October 2024, Perfect Hydration Alkaline Water launched a rebrand, focusing on refreshed packaging that emphasizes its sustainable credentials and performance-oriented branding. The update retains the signature blue color while introducing a sporty "pH" logo, crisper fonts, and prominent highlights for eco-friendly materials.

SEGMENTATION ANALYSIS

By Product Type

Mineral/Spring Segment Dominated Due to Strong Consumer Preference for Naturally Sourced and Mineral-Rich Water

Based on product type, the market is segmented into sparkling, flavored, functional, mineral/spring, and purified.

The mineral/spring segment dominated the global market, valued at USD 30.64 billion in 2025, supported by rising consumer preference for naturally sourced water products perceived as pure, healthy, and premium. These products benefit from strong brand positioning, source authenticity, and broad acceptance across retail and foodservice channels.

The functional segment is projected to grow at the fastest CAGR of 9.93% during the forecast period, driven by increasing demand for electrolyte-enhanced, vitamin-infused, and wellness-oriented hydration products.

To know how our report can help streamline your business, Speak to Analyst

By Packaging Type

Premium PET Bottles Segment Dominated Due to Convenience, Cost Efficiency, and Widespread Retail Availability

By packaging type, the market is segmented into premium PET bottles, glass bottles, metal cans, and others.

The premium PET bottles segment held the leading position in the global market, valued at USD 46.71 billion in 2025, owing to its lightweight nature, cost-effectiveness, durability, and extensive use across supermarkets, hypermarkets, and convenience stores. PET packaging remains the preferred format for large-volume sales as it supports product portability and shelf visibility while maintaining competitive pricing.

The metal cans segment is anticipated to record the fastest CAGR of 10.87% during the forecast period, driven by growing consumer preference for recyclable and environmentally friendly packaging options.

By Price Tier

Premium Segment Dominated Due to Its Broad Consumer Base and High Sales Through Mainstream Retail Channels

By price tier, the market is segmented into premium, super premium, and luxury/ultra-premium.

The premium segment dominated the global market, reaching USD 44.39 billion in 2025, supported by strong consumer demand for better quality and brand value than standard bottled water at relatively accessible prices. This segment benefits from its wide availability across modern retail outlets and its suitability for both regular consumption and impulse purchases.

The luxury/ultra-premium segment is expected to witness the fastest CAGR of 8.28% during the forecast period, driven by rising demand for exclusive, source-specific, and lifestyle-oriented bottled water products.

By Distribution Channel

Off-trade Segment Dominated the Market Due to Strong Penetration Across Supermarkets, Hypermarkets, and Convenience Stores

By distribution channel, the market is segmented into off-trade, on-trade, online channels, and others.

The off-trade segment dominated with the largest premium bottled water market share, valued at USD 52.61 billion in 2025, due to its extensive retail reach and ability to support high-volume consumer purchases. Supermarkets, hypermarkets, specialty stores, and convenience stores continue to serve as the primary sales channels for premium bottled water, particularly for take-home and everyday consumption.

The online channels segment is projected to grow at the fastest CAGR of 10.87% during the forecast period, supported by increasing e-commerce penetration, subscription-based delivery models, and direct-to-consumer expansion by branded players.

Premium Bottled Water Market Regional Outlook

Regionally, the market is studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe Premium Bottled Water Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe accounted for the largest share in the global market, valued at USD 26.35 billion in 2025 and is projected to reach USD 39.40 billion by 2034, registering a CAGR of 5.76% over the forecast period. The region benefits from established consumption of mineral and spring water and strong regulatory support for quality standards.

Germany Premium Bottled Water Market

Germany is expected to achieve moderate growth in the European market, valued at USD 4.40 billion in 2025, supported by high consumption of sparkling water and strong domestic brands.

U.K. Premium Bottled Water Market

The U.K. market was valued at approximately USD 3.00 billion in 2025, driven by demand for flavored and functional premium water products.

North America

North America was valued at USD 18.99 billion in 2025 and is projected to reach USD 31.28 billion by 2034, growing at a CAGR of 6.80% (2026–2034). Growth is driven by high consumption of bottled water, increasing health awareness, and declining soft drink consumption.

U.S. Premium Bottled Water Market

The U.S. dominates the region, valued at approximately USD 12.29 billion in 2025, supported by strong demand for functional water, premium hydration products, and sustainable packaging innovations.

Asia Pacific

Asia Pacific was valued at USD 25.99 billion in 2025, and is projected to reach USD 54.77 billion by 2034, growing at a CAGR of 8.68% over the forecast period. Growth is supported by rapid urbanization, rising disposable incomes, and an expanding middle-class population.

China Premium Bottled Water Market

China represents the largest market in the region, valued at approximately USD 9.77 billion in 2025, supported by strong domestic demand and increasing penetration of premium brands.

South America and the Middle East & Africa

South America reached USD 6.09 billion in 2025 and is projected to grow to USD 11.94 billion by 2034, registering a CAGR of 7.82% over the forecast period. Growth is supported by expanding urban populations and retail distribution networks.

The Middle East & Africa market was valued at USD 3.82 billion in 2025 and is projected to reach USD 38.06 billion by 2034, expanding at a CAGR of 9.78% during the forecast period, driven by water scarcity and increasing reliance on packaged drinking water.

UAE Premium Bottled Water Market

The UAE market was valued at approximately USD 1.02 billion in 2025. Growth is primarily driven by high per capita bottled water consumption due to extreme climatic conditions, limited natural freshwater availability, and strong dependence on packaged drinking water.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Premiumization, Brand Positioning, and Sustainable Packaging Innovation to Gain Market Advantage

The global premium bottled water market is moderately consolidated, with multinational beverage companies and premium water brands competing through product differentiation, branding, and sustainability initiatives. Leading players focus on expanding premium portfolios, introducing functional water variants, and investing in eco-friendly packaging to strengthen market positioning.

Key Players in the Premium Bottled Water Market

|

Rank |

Company Name |

|

1 |

Nestlé S.A. |

|

2 |

Danone S.A. |

|

3 |

PepsiCo, Inc. |

|

4 |

The Coca-Cola Company |

|

5 |

FIJI Water Company LLC |

List of Key Premium Bottled Water Companies Profiled

- Nestlé S.A. (Switzerland)

- Danone S.A. (France)

- PepsiCo, Inc. (U.S.)

- The Coca-Cola Company (U.S.)

- FIJI Water Company LLC (U.S.)

- Voss Water (Norway)

- Suntory Holdings Limited (Japan)

- Nongfu Spring Co., Ltd. (China)

- Gerolsteiner Brunnen GmbH & Co. KG (Germany)

- CG Roxane LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Maison Perrier's French Kiss marked a strategic entry into the functional sparkling water category, combining prebiotic fiber (6g per can from soluble corn fiber), real fruit juice (10%+), natural flavors, and under 1g added sugar in four flavors: Blackberry & Lemon, Peach & Cherry, Mango & Coconut, and Raspberry & Lime.

- January 2026: Cawston Press launched a flavored sparkling water range to enter the growing “lower‑sugar hydration” segment, positioning itself between plain sparkling water and traditional carbonated soft drinks. The range is called Cawston Press Sparkling Water and initially comprises two variants: Squeezed Lime and Pressed Watermelon.

- August 2024: Flow Beverage Corp. introduced a new product line called Flow Sparkling Mineral Spring Water, expanding its portfolio of premium, sustainably sourced water offerings. Flow Sparkling Mineral Spring Water is a premium carbonated mineral spring water with zero sugar and zero calories, positioned as a health‑conscious, clean‑label beverage.

- May 2024: Marvelle Healthcare launched Rhythm, a premium natural mineral water brand. Sourced from the Himalayas after extensive research by founder Rajathi Kalimuthan, a certified Water Sommelier, it emphasizes purity from a 20-year natural filtration process.

- December 2023: Clear Premium Water acquired a majority stake, variously reported as 51% or simply “majority”, in Kelzai Volcanic Water, a brand that markets natural mineral water sourced from volcanic springs. Kelzai Volcanic Water will be exclusively distributed and marketed by Energy Beverages, Clear’s parent, leveraging its nationwide network and presence in India.

REPORT COVERAGE

The global premium bottled water market industry report analyzes the market in depth and highlights crucial aspects such as global market trends, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.80% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Packaging Type

|

|

|

By Price Tier

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 80.91 billion in 2025 and is anticipated to reach USD 145.47 billion by 2034.

At a CAGR of 6.80%, the global market will exhibit steady growth over the forecast period.

By price tier, the premium segment led the market in 2025.

Europe held the largest market share in 2025.

Rising global consumption of packaged and health-oriented beverages is the crucial factor driving the global market.

Nestle S.A., Danone S.A., PepsiCo, Inc., The Coca-Cola Company, and FIJI Water Company LLC are the leading players in the market.

Increasing consumer shift toward healthier hydration and premium beverage choices is the key market trend.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us