Project Logistics Market Size, Share & Industry Analysis, By Service (Transportation & Haulage, Freight Forwarding & Multimodal Management, Warehousing, Storage & Laydown Management, Customs and Regulatory Compliance, and Others), By Mode of Transport (Road, Rail, Air, and Sea), By End-User (Oil and Gas, Mining and Quarrying, Energy Generation and Transmission, Construction and Infrastructure, Manufacturing and Industrial Plants, and Aerospace and Defense), and Regional Forecast, 2026-2034

Project Logistics Market Size and Future Outlook

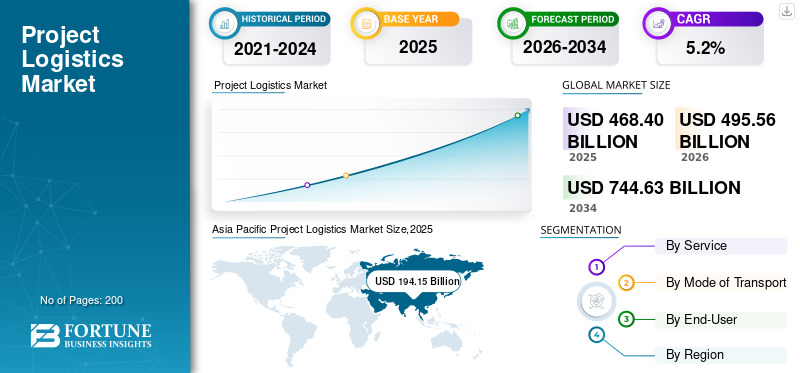

The global project logistics market size was valued at USD 468.40 billion in 2025. The market is projected to grow from USD 495.56 billion in 2026 to USD 744.63 billion by 2034, exhibiting a CAGR of 5.2% during the forecast period. Asia Pacific dominated the global project logistics market with a market share of 41.4% in 2025.

Project logistics refers to the specialized planning, coordination, and execution of transport and handling operations for oversized, overweight, high-value, or mission-critical cargo used in large industrial, infrastructure, and energy projects. It involves multimodal transportation services, route engineering, heavy-lift operations, customs compliance, risk assessment, and on-site delivery synchronization. Project logistics ensure the safe and timely movement of components, such as turbines, reactors, modules, and construction equipment, essential for EPC megaprojects. Its complexity demands engineering expertise, rigorous safety standards, and coordination among contractors, suppliers, ports, and regulatory authorities.

The global market growth supports large-scale industrial, energy, mining, and infrastructure developments by managing specialized movement of heavy and oversized equipment across road, sea, air, and rail networks. Demand is driven by investments in renewable energy, cross-border infrastructure corridors, expansion of petrochemical complexes, and growth in manufacturing and mining projects across both developed and emerging economies. Logistics operations require heavy-lift engineering, multimodal integration, advanced route planning, and strict regulatory compliance. Key players shaping the global competitive landscape include DHL Industrial Projects, DB Schenker, Kuehne+Nagel, DSV, GEODIS, deugro, Mammoet, Sarens, Bolloré Logistics, CEVA Logistics, and Maersk Project Logistics.

U.S. tariffs significantly influence global project logistics industry by altering sourcing strategies, shipment routes, and cost structures for industrial equipment and components integrated into large engineering projects. Tariff policies on steel, machinery, renewable energy components, and technology goods often prompt companies to redesign their supply chains, shift production locations, or diversify their suppliers. This creates fluctuations in inbound and outbound project cargo volumes for ports and carriers. Higher duties increase project costs, delay procurement cycles, and encourage rerouting through alternative gateways, directly reshaping logistics demand patterns across international project corridors.

Download Free sample to learn more about this report.

PROJECT LOGISTICS MARKET Key Takeaways

- 2025 Market Size: USD 468.40 Billion

- 2026 Market Size: USD 495.56 Billion

- 2034 Forecast Market Size: USD 744.63 Billion

- CAGR: 5.2% from 2026–2034

- Asia Pacific dominated the project logistics market with a 41.4% share in 2025.

- The transportation & haulage segment held the largest market share in 2025.

- The oil & gas, mining & quarrying segment accounted for the leading share of the global market in 2025.

Asia Pacific

Asia Pacific led in 2025, driven by infrastructure projects, urbanization, and energy transition.

North America

North America maintained strong growth, driven by LNG, petrochemical, and power investments.

Europe

Europe is experiencing steady growth due to offshore wind expansion, grid modernization, industrial decarbonization, and infrastructure upgrades.

U.S.

LNG, renewable energy, and semiconductor projects are driving logistics demand.

Japan

Renewable energy and industrial infrastructure investments are driving logistics demand.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Acceleration of Energy Transition and Infrastructure Investment Drives Project Logistics Demand

Surging investment in renewables and grid infrastructure is expanding the volume and complexity of project cargo globally, especially for wind turbines, solar equipment, transformers, and high-voltage components. Governments are pushing record additions of renewable capacity, requiring heavy-lift vessels, SPMTs, and engineered logistics to move nacelles, blades, and substations to remote or offshore sites. The IEA reports renewable capacity additions jumped nearly 50% to around 510 GW in 2023, marking the fastest growth in two decades. In June 2024, Maersk secured a global heavy-lift and multimodal logistics contract with Vestas for giant offshore wind turbine components, illustrating the surge in demand. This is expected to boost the project logistics market growth over the forecast period.

MARKET RESTRAINTS

Physical Corridor Constraints and Climate-Related Disruptions Restrain Efficient Project Cargo Flows

Route bottlenecks and climate impacts on key maritime passages are constraining the capacity and reliability of project logistics. Restrictions in narrow canals, draft limits, lock closures, and drought-affected waterways necessitate the re-routing of heavy-lift ships and energy cargo, thereby adding time, cost, and schedule risk to large EPC projects. These constraints are particularly acute for outsized modules that have few viable routes. The Panama Canal drought significantly reduced daily transits, created lengthy queues, and increased shipping costs, disrupting the flow of LPG and other energy commodities. In August 2023, U.S. authorities reported record LPG shipping rates through the Panama Canal due to these canal restrictions, directly impacting project shipping economics.

MARKET OPPORTUNITIES

Industrial Policy and Reshoring of Advanced Manufacturing Create New Project Logistics Opportunities

Large-scale industrial policies are triggering a surge in megaprojects for semiconductor fabs, battery plants, and advanced manufacturing hubs, creating a demand for project logistics providers. The construction of wafer fabs, gigafactories, and high-tech industrial parks requires the movement of ultra-sensitive process tools, cleanroom modules, and specialized heavy-duty utility equipment under tight timelines. The U.S. CHIPS and Science Act, as well as similar incentives in Europe and Asia, are catalyzing the development of dozens of such facilities. In January 2023, McKinsey estimated that U.S. semiconductor players alone had announced around USD 130 billion in domestic fab construction projects, underscoring the forthcoming demand for specialized logistics, complex logistics, and installation solutions.

MARKET CHALLENGES

Escalating Technical Complexity and Execution Risk Challenges Safe Delivery of Mega Components

Rapid upscaling of turbines, reactors, modules, and industrial systems is increasing technical risk and operational complexity in project logistics. Longer blades, heavier nacelles, taller reactors, and modularized process units push the limits of cranes, transport equipment, ports, and roads, thereby increasing the likelihood of damage, delays, or redesigns. Logistics plans must account for dynamic loads, structural clearances, and safety margins across multiple modes. Failures or design issues can ripple through supply chains and project schedules. In January 2023, Siemens Gamesa cancelled a planned offshore wind blade factory at Virginia’s Portsmouth Marine Terminal amid turbine quality and financial pressures, highlighting how technical challenges can unsettle project flows and associated logistics plans.

PROJECT LOGISTICS MARKET TRENDS

Shift Toward Integrated, Low-Carbon, Digitally Orchestrated Project Logistics Shapes Market Evolution

The market is steadily moving from transactional, mode-specific services toward integrated, end-to-end project logistics solutions that bundle engineering, heavy-lift, customs, and multimodal management under one provider, while also reducing emissions. Major players are investing in digital control towers, routing optimization, emissions reporting, and greener assets to align with customer ESG goals and new maritime decarbonization rules. The IMO’s 2023 GHG strategy sets ambitious emissions-reduction targets for international shipping, accelerating this shift. In July 2023, DHL Industrial Projects emphasized its tailored project cargo solutions for renewables, including vessel chartering and engineering support, while Maersk continued to promote integrated project logistics for oversized cargo, illustrating this integrated, sustainability-oriented trend.

Download Free sample to learn more about this report.

Segmentation Analysis

By Service

High Capital Intensity and Direct Cargo Movement Anchor Transportation & Haulage Dominance

By service, the market is divided into transportation & haulage, freight forwarding & multimodal management, warehousing, storage & laydown management, customs and regulatory compliance, and others.

Transportation & Haulage remains the largest service segment in project logistics as every megaproject ultimately monetizes around physically moving outsized cargo between ports, fabrication yards, and project sites. Heavy trailers, SPMTs, barges, and heavy-lift ships capture the bulk of project budgets, especially in the oil and gas, petrochemical, and large infrastructure sectors, where modules can weigh hundreds of tonnes. Integrated providers are increasingly bundling haulage with engineering, but revenue attribution still focuses on transport moves. In June 2024, Maersk’s project division secured a global heavy-lift contract with Vestas to move 260-ton turbine powertrains across Europe, underlining haulage’s centrality.

Freight forwarding & multimodal management for engineered heavy-lift, rigging, and project management services are expanding at the highest CAGR during the forecast period, as turbines, reactors, and industrial modules become larger and more complex. Engineering-intensive heavy-lift and project management services are experiencing the fastest growth in other services. Providers win value by designing lifts, route engineering, and on-site execution, not just transport. In June 2024, Maersk’s Vestas contract combined heavy-lift, customs, intermodal, and warehousing in one engineered solution, reflecting the rapid growth of this higher-value service layer.

To know how our report can help streamline your business, Speak to Analyst

By Mode of Transport

Deep-Sea Breakbulk Capacity and Global Reach Anchor Sea Mode Dominance

By mode of transport, the market is divided into road, rail, air, and sea.

Sea transport dominates the project logistics market share by carrying the heaviest and longest hauls between continents on breakbulk, heavy-lift, and Ro-Ro vessels. Most large equipment, such as refinery modules, offshore platforms, wind towers, and transformers, must be transported by ocean due to weight, geometry, and cost considerations. Growth in offshore wind, LNG trains, and cross-border energy projects further reinforces the role of specialized project vessels and barges. Shipowners and brokers are adding custom tonnage for foundations, blades, and cable carousels. In May 2023, deugro and Siemens Gamesa unveiled the Rotra Futura and Rotra Horizon vessels, which are purpose-built for offshore turbine components, illustrating the structural dominance of sea mode.

Road is the fastest-growing mode as every project shipment ultimately relies on heavy-haul or SPMTs for last-mile delivery and in-country moves between ports, yards, and sites. Investments in modular trailers, SPMT fleets, and specialized heavy-haul corridors are rising, especially in North America, the Middle East, and Asia. In a recent case, Mammoet utilized a large SPMT fleet to transport some of the industry’s largest onshore modules along a dedicated eight-kilometer route for the Gulf Coast Growth Ventures plastics complex in Texas, underscoring the rapid pace of road-based project activity.

By End-User

Massive Hydrocarbon Megaproject Pipelines Anchor Oil & Gas, Mining & Quarrying Dominance

By end-user, the market is divided into oil and gas, mining and quarrying, energy generation and transmission, construction and infrastructure, manufacturing and industrial plants, and aerospace and defense.

Oil and gas, mining and quarrying remain the dominant end-user segment as LNG, petrochemical complexes, and large mines need enormous process modules, compressors, reactors, and mining equipment moved to remote, often greenfield locations. These projects generate sustained waves of project cargo from module yards and OEMs to export terminals, processing plants, and pits. National oil companies and majors continue approving multi-billion-dollar expansions that lock in multi-year logistics scopes. In May 2023, QatarEnergy awarded a USD 10 billion EPC contract for the North Field South LNG expansion, part of a plan to lift Qatar’s LNG capacity from 77 to 126 mtpa, driving intensive project logistics demand.

Energy Generation & Transmission, especially renewables and high-voltage grid projects, is the fastest-growing segment as countries add record solar and wind capacity and reinforce networks. Offshore and onshore wind, utility-scale solar, and new transmission corridors require heavy-lift vessels, specialized trailers, and complex multimodal coordination. In April 2024, the Global Wind Energy Council reported a record 117 GW of new wind installations in 2023, 50% higher than 2022, highlighting surging logistics needs for turbine components and grid assets worldwide.

PROJECT LOGISTICS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific is the dominant and fastest-growing regional market for project logistics, backed by massive infrastructure programs, rapid urbanization, and energy-transition megaprojects. China, India, Southeast Asia, Japan, and South Korea collectively anchor demand for power plants, LNG terminals, petrochemicals, offshore wind, and industrial parks. Asia Pacific already leads global wind and solar additions and is expected to account for the majority of new renewable capacity and related supply-chain investments this decade, spurring high volumes of heavy-lift sea, road, and barge movements. In June 2024, IEEFA estimated that solar and offshore wind supply chains in seven Asian markets alone could attract more than USD 1.1 trillion in investment through 2050, highlighting huge long-term potential for project cargo flows.

Asia Pacific Project Logistics Market Size,2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America’s market is underpinned by large LNG, petrochemical, power, and industrial investments, especially along the U.S. Gulf Coast and Western Canada. Heavy-lift road and barge corridors support multi-module refinery, chemicals, and plastics complexes, while onshore wind, solar, and grid upgrades add diverse oversized cargo flows. The region is mature but still expanding steadily as new LNG trains and export terminals move into construction, driving sustained demand for specialized haulage, marine heavy-lift, and rigging services. In September 2024, the U.S. EIA reported that North American LNG export capacity is expected to more than double between 2023 and 2028, reflecting a major pipeline of megaprojects requiring intensive project logistics.

The U.S. market trends by large-scale LNG, petrochemical, renewable-energy, and semiconductor manufacturing projects, supported by strong federal incentives and industrial policy. Gulf Coast refinery expansions, offshore wind developments, and CHIPS Act–driven fab construction generate steady demand for heavy-haul transport, engineered lifting, and multimodal moves. Growing grid-modernization projects further elevate requirements for transformers, substations, and oversized power-equipment logistics.

Europe

Europe’s market is driven by decarbonization, offshore wind build-out, grid reinforcement, and industrial retrofits rather than greenfield hydrocarbons. Northern Europe and the North Sea remain focal points for offshore wind, submarine cables, and large transformers, stimulating demand for heavy-lift vessels, jack-ups, port laydown space, and engineered road transport. EU energy-efficiency regulations and industrial decarbonization programs are prompting modernization of steel, chemicals, and manufacturing facilities, generating recurring project cargo. In September 2025, TotalEnergies and RWE secured around USD 4.7 billion to build a 1.5 GW offshore wind farm off Normandy, underlining long-term demand for European offshore project logistics services.

Rest of the World

Rest of the World, encompassing the Middle East, Africa, and Latin America, is the second fastest growing project logistics region, expanding from a smaller base. Growth is propelled by large oil and gas developments, petrochemicals, mining projects, and port and corridor upgrades, especially in the Gulf, West Africa, and Brazil. Governments and developers are investing in offshore structures, terminals, and heavy industry, requiring advanced lifting assets and specialized marine logistics. In September 2024, Dubai’s Drydocks World agreed to acquire a new 5,000-tonne floating sheerleg crane, the largest of its kind in the Middle East and Africa, specifically to meet rising offshore heavy-lift demand, underscoring accelerating project logistics requirements in the wider region.

COMPETITIVE LANDSCAPE

Key Industry Players

Integrated Heavy-Lift Capabilities and Global Engineering Expertise Strengthen Competitive Advantage in Project Logistics

Global project logistics leaders distinguish themselves via vast asset pools, multimodal capabilities (sea, road, air, heavy-lift), and integrated services engineering, chartering, customs, and storage, enabling them to handle mega-projects end-to-end. Firms such as Maersk Project Logistics seamlessly move 260-ton turbine powertrains from factory to port to site, combining sea freight, custom heavy-lift, intermodal, customs clearance, and warehousing under one contract. Similarly, DHL Industrial Projects offers global forwarding, vessel chartering, lifting & marine operations, reinforcing its competitive advantage through scale and full-service reach.

LIST OF KEY PROJECT LOGISTICS COMPANIES PROFILED

- DHL Industrial Projects (Germany)

- DB Schenker Projects (Germany)

- Kuehne + Nagel Project Logistics (Switzerland)

- DSV Project Logistics (Denmark)

- Maersk Project Logistics (Denmark)

- GEODIS Project Logistics (France)

- Bolloré Logistics – Projects (France)

- CEVA Logistics – Projects (France)

- Nippon Express Project Logistics (Japan)

- Kerry Logistics – Projects (Hong Kong SAR)

- Mammoet (Netherlands)

- Sarens (Belgium)

- Deugro Group (Germany)

- Fracht Group (Switzerland)

- Savino Del Bene (Italy)

KEY INDUSTRY DEVELOPMENTS

- In October 2025, the Uttar Pradesh government approved 38 private logistics and warehousing projects valued at USD 28 million to strengthen the state’s freight ecosystem and support industrial expansion. These projects are part of the state’s ongoing logistics policy push aimed at enhancing multimodal connectivity and storage capacity. The initiatives include new warehouses, distribution hubs, and integrated logistics facilities to improve supply-chain efficiency for manufacturers and exporters. The state expects these developments to accelerate job creation and improve cargo flow across key industrial corridors.

- In February 2025, AR Africa Launch announced a new multimodal logistics initiative designed to strengthen trade routes between India, Africa, and the Middle East. The initiative focuses on enhancing port capacity, transit corridors, and integrated freight solutions to support growing bilateral commerce, energy shipments, and industrial cargo movement. By connecting major maritime hubs with inland logistics centers, it aims to reduce transit times, improve reliability, and expand market access for exporters. The program positions the region as a more efficient gateway for south-south trade and project-cargo flows.

- In January 2025, Transport Logistic partnered with Heavy Lift & Project Forwarding International (HLPFI) to launch a dedicated global Project Cargo Platform supporting heavy-lift, breakbulk, and project logistics communities. The platform will serve as a knowledge-exchange hub connecting shippers, EPC contractors, and logistics providers through market insights, business matchmaking, and technical content. It aims to strengthen collaboration in specialized cargo transport, spotlight innovations in lifting and multimodal routing, and enhance visibility for project-cargo professionals across Europe, Asia, the Middle East, and the Americas.

- In October 2024, WR Group Holding announced a strategic investment in RETEMS to expand WR Logistics’ operational footprint into Azerbaijan. The partnership enhances WR Group’s capabilities in cross-border road freight, industrial logistics, and warehousing across the Middle Corridor connecting Central Asia, the Caucasus, Türkiye, and Europe. The move strengthens access to growing trans-Eurasian trade lanes and supports regional infrastructure development. The company aims to leverage Azerbaijan’s strategic geographic position to build an integrated logistics network for energy, project, and manufacturing sectors.

- In October 2023, Ascela Advisory was awarded the mandate to support the development of a major logistics zone at the Port of Cotonou in Benin. The scope includes master planning, regulatory structuring, and operational design to transform the port into a regional logistics gateway for West Africa. The project aims to strengthen maritime-land connectivity, expand storage and processing capabilities, and position Cotonou as a competitive trade hub. Ascela’s role supports Benin’s broader strategy to modernize port infrastructure and attract private-sector logistics investment.

REPORT COVERAGE

The global project logistics market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market forecast offers a comprehensive competitive landscape, encompassing the largest market share, emerging opportunities, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service, By Mode of Transport, By End-User, and By Region |

| By Service |

|

| By Mode of Transport |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 468.40 Billion in 2025 and is projected to reach USD 744.63 Billion by 2034.

In 2025, the market value stood at USD 194.15 billion.

The market is expected to grow at a CAGR of 5.2% during the forecast period of 2026-2034.

By mode of transport, the sea segment leads the market.

Acceleration of energy transition and infrastructure investment drives project logistics demand.

Top players in the market include DHL Industrial Projects, DB Schenker, Kuehne Nagel, DSV, GEODIS, CEVA Logistics, and Maersk Project Logistics.

Asia Pacific accounted for the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us