Public Safety LTE Market Size, Share & Industry Analysis, By Infrastructure Type (Fixed LTE Sites, Tactical LTE, Indoor Systems, Border & Coastal Corridors, and Others), By Solution (Tactical LTE Kits, Base LTE Networks, Mission Software & Platforms, and LTE–SATCOM Integration Solutions), By Service (Network Design & Consulting, System Integration, Deployment & Optimization, Maintenance & Lifecycle Support, Training, and Others), By Application (Command, Control & Missions, ISR Backhaul, Situational Awareness, & Others), By End User, and Regional Forecast, 2026-2034

Public Safety LTE Market Size and Future Outlook

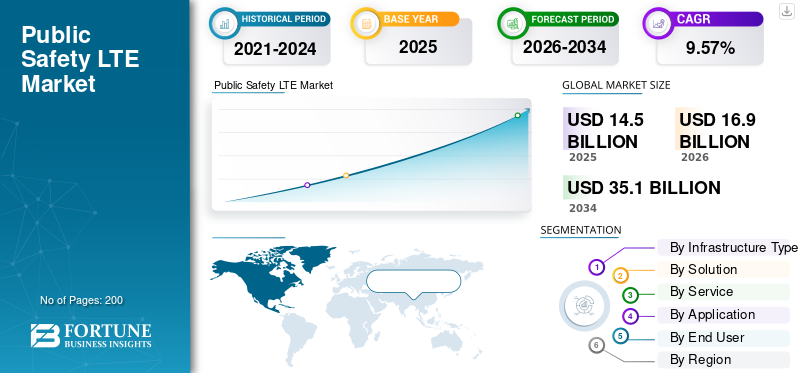

The global public safety LTE market size was valued at USD 14.5 billion in 2025. The market is projected to grow from USD 16.9 billion in 2026 to USD 35.1 billion by 2034, exhibiting a CAGR of 9.57% during the forecast period. North America dominated the public safety LTE market with a market share of 40.68% in 2025.

Public Safety LTE is a mission-critical broadband technology that provides secure audio, video, and data in real time across land, air, and maritime domains to first responders, manned aircraft, and drones. It consists of air-to-ground links, rugged devices, deployable, Long-Term Evolution Radio Access Network (LTE RAN), and dedicated spectrum, and mission-critical applications such as Mission-Critical Push-to-Talk (MCPTT), and situational awareness tools. Moreover, public safety aviation units, UAS teams, police, fire departments, emergency medical services, coast guard, airport and airline operations, and defense organizations are important end users.

Nokia, Samsung, Motorola Solutions, and AT&T/FirstNet are major providers that provide devices, infrastructure, and LTE networks across the country. These players are developing new products, forming alliances, and making acquisitions.

Download Free sample to learn more about this report.

PUBLIC SAFETY LTE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 14.5 billion

- 2026 Market Size: USD 16.9 billion

- 2034 Forecast Market Size: USD 35.1 billion

- CAGR: 9.57% from 2026–2034

- North America dominated the public safety LTE market with a 40.68% share in 2025.

- Fixed LTE sites held the largest infrastructure type segment share in 2025.

- Base LTE networks captured the largest solution segment share in 2025.

North America

North America remained the leading regional market, supported by strong government investments and nationwide public safety network initiatives such as FirstNet.

Europe

Europe is expected to reach USD 3.4 billion in 2026, driven by modernization programs replacing legacy public safety communication systems.

Asia Pacific

Asia Pacific is projected to register the fastest growth, expanding at a CAGR of 10.33% through the forecast period due to smart city investments and urbanization.

U.S.

The market is estimated to reach USD 4.2 billion in 2026, supported by growing demand for real-time data sharing and enhanced situational awareness across emergency services.

Japan

The market is projected to reach USD 1.0 billion in 2026, driven by continued investments in advanced public safety infrastructure and next-generation communication networks.

Read More

Russia-Ukraine War Impact:

The market has been greatly impacted by the Russia-Ukraine war. To combat Ukrainian drone assaults that depend on these networks for public safety, Russian authorities have enforced extensive LTE network shutdowns and internet blackouts in certain areas. Critical communications are impacted by these disruptions, which lead to operational difficulties and domestic economic effects. In the meantime, despite persistent cyber threats and infrastructure damage, the Ukrainian government is focused on developing network resilience through satellite integration and tactical LTE installations.

MARKET DYNAMICS

MARKET DRIVERS:

Increased Broadband Connectivity Across Various Platforms is a Market Driver

The expansion of broadband connectivity across various platforms significantly drives the public safety LTE market growth. Enhanced LTE and 5G networks provide first responders and aerospace users with reliable, high-speed data access, enabling real-time video streaming, high-resolution image sharing, and dynamic mapping critical for mission success. This interconnectedness improves situational awareness, coordination across land, air, and maritime units, and rapid decision-making in emergencies. Broadband connectivity communication offers greater security and supports advanced public safety applications such as AI-powered analytics and drone operations, thereby elevating safety capabilities and operational efficiency.

MARKET RESTRAINTS

Financial and Technical Challenges Restrain Market Growth

Market expansion is severely constrained by the high implementation and maintenance costs of sophisticated public safety LTE networks, particularly for aerospace users who require specialist equipment and extensive coverage. Moreover, the implementation is delayed by regulatory issues related to the restricted availability and distribution of licensed spectrum for public safety broadband. It is difficult to integrate LTE with current legacy communication systems, significant infrastructure modifications and interoperability solutions are needed. Rapid adoption across agencies is also hampered by technological issues such as maintaining dependable connectivity in challenging areas, controlling network congestion during emergencies, and protecting data privacy and cybersecurity.

MARKET OPPORTUNITIES

Expanding Integration and Advanced Technologies Offer Market Opportunity

The market presents significant growth opportunities through integration with emerging technologies such as Unmanned Aerial Vehicles (UAVs), AI, and Internet of Things (IoT). The transition from legacy radio systems to LTE networks for public safety enhances interoperability and real-time communication across agencies and platforms, boosting operational efficiency in aerospace and public safety missions. Increasing government investments in public safety network infrastructure and rising demand for secure broadband during emergencies further expand opportunities.

MARKET CHALLENGES:

Cybersecurity Threats Pose a Significant Challenge in Public Safety LTE Networks

Public safety LTE networks face growing challenges from sophisticated cybersecurity threats that can compromise mission-critical communications. Cyberattacks include spying, network jamming, data interception, communication disruption, and operational failures. The increasing interconnectivity of LTE with IoT devices expands the attack surface, necessitating advanced encryption, authentication, and real-time threat detection. Ensuring continuous network availability despite cyberattacks is crucial for emergency responders. Moreover, legacy systems integration complicates security management, demanding adaptive, AI-enabled cybersecurity strategies to protect sensitive data and maintain public trust in these vital communications networks.

PUBLIC SAFETY LTE MARKET TRENDS:

Integration of Artificial Intelligence and Machine Learning to Improve Decision Making is a Latest Market Trend

The integration of artificial intelligence (AI) and machine learning (ML) represents a key latest trend in the market. These technologies are increasingly embedded into public safety networks to enable advanced data analytics, predictive monitoring, automated incident detection, and resource optimization. AI and ML processes are vital to improve situational awareness and decision-making in real time. Furthermore, AI-powered tools assist law enforcement and emergency responders with facial recognition, video analysis, and natural language processing, significantly enhancing operational efficiency and response effectiveness in aerospace and broader public safety contexts.

Download Free sample to learn more about this report.

Segmentation Analysis

By Infrastructure Type

Network Modernization by Major Countries Boosted Fixed LTE Sites Segment Growth

On the basis of the market segmentation of infrastructure type, the market is classified into fixed LTE sites, tactical LTE, indoor systems, border & coastal corridors, and others.

The fixed LTE sites segment accounted for the largest market share in 2025. The growth in this segment is owing to the ongoing modernization of national public safety and defense communication networks, where governments are hardening and expanding LTE coverage across bases, cities, borders, and transport corridors.

The tactical LTE segment is expected to grow at the highest CAGR of 10.43% over the forecast period.

By Solution

Shift from Traditional Radio to Broadband Mission Networks Fostered Base LTE Networks Segment Growth

In terms of solution, the market is categorized into tactical LTE kits, base LTE networks, mission software & platforms, and LTE–SATCOM integration solutions.

The base LTE networks segment captured the largest public safety LTE market share in 2025. The growth in this segment is owing to the gradual shift from voice-centric traditional radio access network systems toward broadband-capable LTE/5G mission networks at bases, airfields, ports, and others.

The tactical LTE kits segment is expected to grow at the highest CAGR of 10.30% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Service

Expanding Installed Base Horizons Boosted Maintenance & Lifecycle Support Segment Growth

Based on service, the market is segmented into network design & consulting, system integration, deployment & optimization, maintenance & lifecycle support, training, and others.

The maintenance & lifecycle support segment held the dominating position in 2025. The growth in this segment is owing to the rapidly expanding installed base of LTE infrastructure and devices that demand continuous upgrades, security patches, and hardware refresh cycles.

The system integration segment is set to flourish at the highest CAGR of 10.47% over the forecast period.

By Application

Rise in Data Centric Command Systems Fueled Command, Control & Missions Segment Expansion

Based on application, the market is segmented into command, control & missions, ISR backhaul

situational awareness, critical infrastructure & base security (bases, borders, ports, airports, depots), emergency, natural disaster response, logistics & asset management (convoy tracking, supply chains, MRO data), training & exercises, and others.

The command, control & missions segment held the dominating position in 2025. The growth in this segment is owing to a shift from voice-only command models to data-centered mission environments.

The situational awareness segment will witness the highest growth rate of 10.48% over the forecast period.

By End User

Multi-Domain Operations and C4ISR Modernization Accelerate Armed Forces Segment Growth

Based on end user, the market is segmented into armed forces, special operations & rapid reaction forces, border security & coast guard agencies, homeland security force, civil defense & disaster management authorities, critical infrastructure operators, and others.

The armed forces segment held the dominating position in 2025. The growth in this segment is owing to defense modernization programs that prioritize resilient C4ISR, multi-domain operations, and high-bandwidth connectivity for soldiers, vehicles, UAVs, and command posts.

The special operations & rapid reaction forces segment will witness the highest growth rate of 10.31% over the forecast period.

Public Safety LTE Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America held the dominant share in 2024 valuing at USD 4.7 billion and also took the leading share in 2025, with USD 5.9 billion. The market in North America is expanding significantly, owing to the robust government support and programs such as the nationwide FirstNet network, which has stimulated significant investment in public safety LTE. The growth in the U.S. is driven by the need for improved situational awareness, the capacity to send high-speed data in real time across various emergency services. In 2026, the U.S. market is estimated to reach USD 4.2 billion.

Asia Pacific

The market in Asia Pacific is projected to record a 10.33% CAGR in the coming years, which is the highest amongst all the regions. Public safety LTE is rapidly expanding in Asia Pacific as a result of increased urbanization, a rise in investment in smart city initiatives, and others. A push for modernized public safety infrastructure in major countries such as China, India, and Japan further powers the demand. Backed by these factors, countries including China anticipates to record the valuation of USD 01 Billion, Japan to record USD 1.0 Billion, and India to record USD 0.9 Billion in 2026.

Europe

Europe is estimated to reach USD 3.4 billion in 2026. European governments are heavily investing in modernizing public safety networks to replace legacy systems, which drives the market growth in the region. The U.K. and Germany both are estimated to reach USD 1.1 billion and 1.0 billion, each, in 2026.

Rest of the World

In the Rest of the World, the Middle East & Africa and Latin America regions would witness a moderate growth over the projected period. The market in the Middle East & Africa 2026 is set to record USD 1.2 billion. Latin America is set to attain the value of USD 0.8 billion by 2026. The growth is driven by the high demand in major nations such as Turkey, Israel, and others for sophisticated communication infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Top Companies Focus on Mergers and Product Innovation to Redefine Market Landscape

The public safety LTE market is driven by major players such as Nokia, Motorola Solutions, AT&T, Samsung, and Ericsson, who focus on advanced network solutions and mission-critical devices. Recent partnerships and mergers, such as Nokia's collaborations with regional carriers, are focused on enhancing spectrum efficiency and coverage. Moreover, the expansion of dedicated public safety broadband networks such as FirstNet in the U.S. and comparable initiatives globally strengthens service reliability. Market leaders emphasize cybersecurity and hybrid LTE deployment models to meet diverse operational requirements, with notable growth in North America and Asia Pacific due to increased government investments and evolving regulatory support.

LIST OF KEY PUBLIC SAFETY LTE COMPANIES PROFILED:

- Motorola Solutions (U.S.)

- Nokia (Finland)

- Ericsson (Sweden)

- AT&T (U.S.)

- Verizon (U.S.)

- Samsung Electronics (South Korea)

- Airbus (France)

- L3Harris Technologies (U.S.)

- General Dynamics Mission Systems (U.S.)

- Sonim Technologies (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- November 2025: The U.K. Home Office has a critical communications contract with Etherstack. This contract is a part of its plan to shift U.K. public safety communications to next next-generation 5G network known as the ESN (Emergency Services Network).

- June 2025: Nokia and Leonardo, a global leader in aerospace, defense, and security, partnered to provide state of the art mission critical services that are integrated into Nokia's Core Enterprise Solutions.

- December 2024: The Georgia State Patrol, a leading public safety agency, transformed its emergency communication approach by implementing Southern Linc’s LTE system featuring mission-critical push-to-talk (MCPTT). This transition from the conventional VHF land mobile radio (LMR) technology is a step toward more dependable voice communications in emergencies.

- March 2024: Japan Radio Co., Ltd. (JRC) and Icom Incorporated announced their agreement to work together on the introduction of a cutting-edge private LTE network radio system. Since it aims to grow two crucial domains, the public safety and industrial sectors.

- March 2023: Honeywell announced phase one of the Bangalore Safe City project, which uses Honeywell's intelligent and linked safety and security technology to create a secure, effective, and empowering environment for women and girls, has been successfully executed.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.57% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Infrastructure Type, Solution, Service, Application, End User, and Region |

|

By Infrastructure Type |

|

|

By Solution |

|

|

By Service |

|

|

By Application |

|

|

By End User |

|

|

By Region |

North America (By Infrastructure Type, Solution, Service, Application, End User, and Country)

Europe (By Infrastructure Type, Solution, Service, Application, End User, and Country/Sub-region)

Asia Pacific (By Infrastructure Type, Solution, Service, Application, End User, and Country/Sub-region)

Rest of the World (By Infrastructure Type, Solution, Service, Application, End User, and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 14.5 Billion in 2025 and is projected to reach USD 35.1 Billion by 2034.

In 2025, the market value stood at USD 5.9 billion.

The market is expected to exhibit a CAGR of 9.57% during the forecast period of 2026-2034.

The base LTE networks segment dominated the market by solution.

Increased broadband connectivity across various platforms is a market driver.

Motorola Solutions (U.S.), Nokia (Finland), Ericsson (Sweden), AT&T (U.S.), Verizon (U.S.), and Samsung Electronics (South Korea) are some of the key players in the market.

North America dominated the market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us