Radiofrequency Ablation Devices Market Size, Share & Industry Analysis, By Product (Capital Equipment, Reusable Accessories, and Disposable Consumables), By Application (Cardiac Arrhythmia Ablation, Pain Management and Neuromodulation, Oncology, Dermatology and Aesthetic Applications, General Surgery Application, and Others), By End-user (Hospitals and ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Radiofrequency Ablation Devices Market Size and Future Outlook

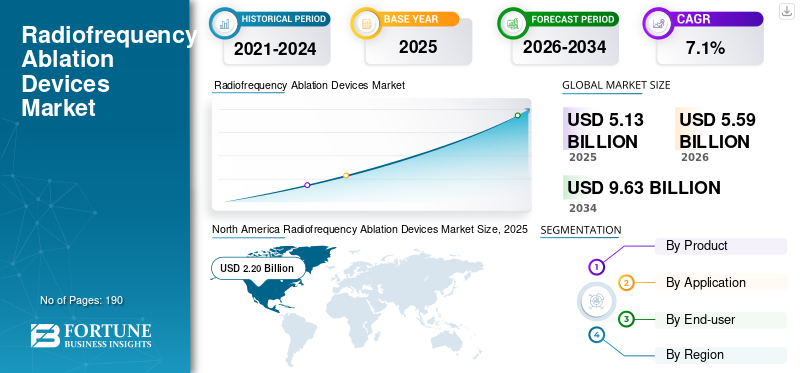

The global radiofrequency ablation devices market size was valued at USD 5.13 billion in 2025. The market is projected to grow from USD 5.59 billion in 2026 to USD 9.63 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period. North America dominated the radiofrequency ablation devices market with a market share of 42.88% in 2025.

Radiofrequency ablation devices are medical systems that use high-frequency electrical energy to generate controlled heat and destroy targeted tissue with minimal damage to surrounding structures. They are used across a broad range of indications, especially cardiac arrhythmia treatment, pain management, oncology, and selected surgical applications. The market is growing as hospitals and specialists increasingly favor minimally invasive therapies that can shorten recovery time, reduce hospital stay, and improve procedural precision. Growth is also supported by the large and persistent burden of cardiovascular disease, rising use of image-guided and catheter-based procedures, and continuous device innovation in mapping, sensing, and energy delivery.

Furthermore, Johnson & Johnson, Boston Scientific Corporation, Abbott, and Medtronic plc International held the largest market share, driven by increasing investments and planned initiatives, such as new product launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

RADIOFREQUENCY ABLATION DEVICES MARKET TRENDS

Technology Refinements Propel Adoption of Smarter Ablation Platforms Driving Market Growth

A clear market trend is the move from stand-alone ablation tools toward integrated procedural ecosystems. Buyers increasingly want devices that work seamlessly with mapping systems, sensing technologies, imaging support, and workflow software rather than isolated generators or single-function catheters. In electrophysiology, this means demand is shifting toward platforms that combine navigation, real-time feedback, and more precise lesion creation. Recent FDA approvals illustrate this direction, with newer systems positioned not just as energy sources but as components of a broader procedural environment. This trend matters as it changes how value is measured. Providers are seeking beyond the device itself and asking whether a platform improves efficiency, reproducibility, and procedural confidence.

Another visible trend is the continued strength of disposable revenue streams. As utilization rises, recurring sales from single-use catheters, probes, electrodes, and related accessories become increasingly important to vendor economics. This is encouraging companies to sharpen their consumables strategy alongside capital placements. Over time, the market is anticipated to reward suppliers that can combine clinical performance, training support, and recurring product pull-through within a tightly connected ecosystem.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Burden of Cardiac Rhythm Disorders and Preference for Minimally Invasive Therapy Driving Product Adoption

One of the strongest radiofrequency ablation devices market growth drivers is the steady increase in demand for minimally invasive treatment of cardiac arrhythmias, especially atrial fibrillation and atrial flutter. RF ablation has become deeply embedded in electrophysiology practice as it allows clinicians to target abnormal electrical pathways with precision while avoiding the morbidity associated with more invasive surgical approaches. As cardiovascular disease continues to place pressure on health systems worldwide, providers are investing more heavily in advanced ablation platforms that improve workflow, mapping accuracy, and lesion control.

The market is also benefiting from the growing installed base of electrophysiology labs, stronger physician familiarity with catheter-based ablation, and a broader willingness among patients to opt for interventional solutions earlier in the treatment pathway. Regulatory progress is reinforcing this trend. Recent FDA approvals for newer ablation and mapping systems show that manufacturers are actively improving catheter design, energy delivery, and procedural integration. Beyond cardiology, the same minimally invasive appeal supports continued adoption in tumor ablation and pain interventions, giving the market a strong multi-specialty demand base.

MARKET RESTRAINTS

Competition from Alternative Ablation Technologies to Limit Market Growth

A major restraint for this market is that radiofrequency ablation does not operate in isolation. In several clinical areas, it competes with alternative energy modalities, such as cryoablation, microwave ablation, pulsed-field ablation, laser-based systems, and other targeted thermal or non-thermal approaches. This can slow purchasing decisions, especially in hospitals that prefer multi-technology flexibility or are evaluating which platform is most appropriate for a specific specialty. In oncology, for example, radiofrequency ablation is established. Still, it is one among several local treatment options, and physicians may choose another technology depending on tumor size, location, and clinical objective. In cardiac care, the emergence of newer energy approaches is also reshaping the competitive landscape, potentially limiting the pace of expansion for conventional RF systems in some centers.

Another restraint is the capital-intensive nature of advanced ablation platforms. Hospitals must weigh the cost of generators, mapping systems, accessories, and training against expected procedural throughput. In cost-sensitive markets, these budget considerations can delay adoption, particularly outside large tertiary centers. As a result, even where clinical demand is real, commercial conversion can be slower than the underlying disease burden might suggest.

MARKET OPPORTUNITIES

Broader Use in Oncology, Pain Care, and Outpatient Settings Creates Significant Growth Opportunities

The market still offers significant opportunities, as radiofrequency ablation is no longer confined to a single specialty. While cardiac electrophysiology remains the most visible revenue engine, oncology and pain management offer meaningful headroom, particularly as clinicians seek targeted interventions that reduce recovery time and align with outpatient or short-stay care models. In cancer care, radiofrequency ablation is already recognized as a treatment approach for selected tumors, and ongoing work around combination therapy and image-guided intervention could strengthen its role in carefully chosen patient populations. In pain management, demand is supported by the need for non-opioid, procedure-based solutions for chronic nerve and joint-related pain.

There is also an opportunity in emerging markets, where specialist infrastructure is improving, and tertiary hospitals are gradually expanding interventional capabilities. As healthcare systems invest in catheter labs, imaging support, and procedural training, RF ablation devices stand to benefit from broader access. Manufacturers that offer user-friendly systems, robust clinical education, and specialty-specific product lines are particularly well-positioned to unlock this next phase of growth across both mature and developing regions.

MARKET CHALLENGES

High Procedural Complexity, Training Demands, and Uneven Access Remain Practical Barriers

Despite its clinical value, radiofrequency ablation still faces real-world challenges that can limit adoption and scale-up. Procedural success often depends on specialist expertise, careful patient selection, and access to well-equipped centers, which means outcomes can vary widely between high-volume institutions and less experienced facilities. In advanced cardiac applications, providers need trained electrophysiologists, mapping capability, catheter lab infrastructure, and support staff who understand complex workflows. That creates a steep entry barrier for smaller hospitals. Similar issues exist in oncology and pain management, where successful use often depends on imaging guidance, multidisciplinary coordination, and strong post-procedure follow-up. There is also the challenge of reimbursement and budget justification. Even when the clinical case is sound, administrators may hesitate if the capital outlay is high or if procedure volumes are still developing.

Finally, the market must navigate a fast-moving competitive environment in which clinicians are constantly comparing RF against alternative ablation options. For manufacturers, that means growth is not just about launching better devices; it also requires investment in evidence generation, physician training, and long-term support to build durable adoption.

Segmentation Analysis

By Product

Dependence on Single-use Components to Drive Disposable Consumables Segment Growth

Based on product, the market is segmented into capital equipment, reusable accessories, and disposable consumables.

By product, disposable consumables account for the highest market share as radiofrequency ablation is fundamentally a procedure-driven market. Every intervention requires single-use or limited-use components such as catheters, electrodes, probes, grounding accessories, or procedure-specific kits, which creates a recurring revenue stream that scales directly with volume.

Additionally, the reusable accessories segment is projected to grow at a CAGR of 5.6% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Strong Electrophysiology Demand makes Cardiac Arrhythmia Ablation the Leading Application

By application, the market is classified into cardiac arrhythmia ablation, pain management and neuromodulation, oncology, dermatology and aesthetic applications, general surgery application, and others.

By application, cardiac arrhythmia ablation holds the largest radiofrequency ablation devices market share as it combines high clinical need, strong physician adoption, and ongoing technology investment. RF ablation is widely used in treating abnormal heart rhythms, and the burden of cardiovascular disease continues to push more patients into diagnostic and interventional care pathways. Moreover, the segment is projected to hold a 46.7% share in 2026.

Additionally, the oncology segment is estimated to grow at a CAGR of 9.5% during the forecast period.

By End-user

Hospitals and ASCs Leads due to Advanced Infrastructure and Case Complexity

On the basis of end-user, the market is classified into hospitals and ASCs, specialty clinics, and others.

By end user, hospitals and ambulatory surgical centers account for the highest share as most radiofrequency ablation procedures still require specialized infrastructure, trained staff, and access to imaging or mapping support. This is especially true in cardiac electrophysiology and many oncology procedures, where the clinical environment needs to support patient monitoring, procedural precision, and complication management. Hospitals also tend to be the earliest adopters of new ablation platforms, giving them an advantage in both volume and technology uptake. Furthermore, the segment is set to hold a 75.0% share in 2026.

In addition, the specialty clinics segment is projected to grow at a CAGR of 8.8% during the forecast period.

Radiofrequency Ablation Devices Market Regional Outlook

Based on region, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Radiofrequency Ablation Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 2.03 billion, and reached USD 2.20 billion in 2025. North America is expected to remain the largest regional market as the U.S. and Canada combine a high burden of cardiovascular disease with strong procedural capacity, broad access to electrophysiology labs, and faster adoption of minimally invasive device-based therapies. On the supply side, leading medtech companies such as Boston Scientific and Abbott have continued to highlight electrophysiology as an important growth area, which supports demand for RF ablation systems, mapping platforms, and recurring consumables in the region.

U.S. Radiofrequency Ablation Devices Market

In 2026, the U.S. market is forecasted to represent USD 2.11 billion, capturing 37.9% of total global revenue.

Europe

Europe is expected to achieve a 6.7% growth rate in the coming years, the second-highest globally, reaching USD 1.74 billion by 2026. A well-established cardiology ecosystem, rising electrophysiology procedure intensity, and continued adoption of catheter-based therapies across major markets such as Germany, the U.K., France, Italy, and Spain are supporting Europe’s growth. Growth is also supported by ageing populations, rising chronic disease burden, and the gradual expansion of advanced interventional care into a wider set of hospitals beyond the largest tertiary centers.

U.K. Radiofrequency Ablation Devices Market

The U.K. market is projected to reach USD 0.31 billion by 2026, accounting for 5.6% of the global market revenue.

Germany Radiofrequency Ablation Devices Market

Germany's market is forecasted to reach about USD 0.38 billion by 2026, representing roughly 6.8% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 1.04 billion, ranking as the third-largest globally. Asia Pacific is projected to be the fastest-growing region, driven by a very large patient pool, improving healthcare infrastructure, expanding specialist capacity, and a rapid rise in the ageing-related disease burden.

Japan Radiofrequency Ablation Devices Market

Japan is projected to generate approximately USD 0.25 billion in revenue by 2026, contributing nearly 4.4% to the global market.

China Radiofrequency Ablation Devices Market

China’s market is forecast to reach approximately USD 0.34 billion by 2026, contributing about 6.0% to global revenues.

India Radiofrequency Ablation Devices Market

India is forecast to contribute approximately USD 0.14 billion to the market by 2026, corresponding to about 2.5% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate market growth, with Latin America expected to reach around USD 0.24 billion by 2026. Latin America is growing from a smaller base, but the outlook remains positive due to the region’s sizable cardiovascular burden, improving diagnostic rates, and the gradual expansion of interventional treatment capacity in countries such as Brazil and Mexico. The Middle East and Africa region is expected to expand steadily as tertiary hospitals, especially in the GCC and South Africa, continue to strengthen their capabilities in cardiovascular and oncology care.

GCC Radiofrequency Ablation Devices Market

By 2026, the GCC is expected to generate approximately USD 0.07 billion in the market, accounting for nearly 1.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Continuous Product Innovation Drives Stronger Market Positioning of Leading Players

The market structure shows a moderate level of consolidation among top players, while remaining fragmented at the lower levels. Leadership sits with large diversified medtech companies that have strong positions in cardiac electrophysiology, especially players such as Johnson & Johnson, Boston Scientific Corporation, Abbott, and Medtronic plc, where scale, installed base, physician relationships, and integrated mapping-plus-ablation ecosystems create a meaningful competitive advantage.

Additionally, other major companies such as AtriCure, Inc., Avanos Medical, Inc., Hologic, Inc., and Stryker Corporation maintain competitiveness through ongoing advancements in technologies. Further, other improvements include growing demand for improved healthcare infrastructure and efforts to improve therapy outcomes.

LIST OF KEY RADIOFREQUENCY ABLATION DEVICES COMPANIES PROFILED

- Johnson & Johnson (U.S.)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- Medtronic plc (Ireland)

- AtriCure, Inc. (U.S.)

- Avanos Medical, Inc. (U.S.)

- Hologic, Inc. (U.S.)

- Stryker Corporation (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- Olympus Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Boston Scientific Corporation has received U.S. Food and Drug Administration (FDA) approval to expand the instructions for use (IFU) labeling for the FARAPULSE Pulsed Field Ablation (PFA) System.

- July 2025: Johnson & Johnson announced U.S. Food and Drug Administration (FDA) approval of an update to the VARIPULSE Platform’s irrigation flow rate, reflecting the company’s commitment to the evolution of PFA innovation following real-world clinical practice.

- January 2025: Johnson & Johnson announced European CE mark approval of the Dual Energy THERMOCOOL SMARTTOUCH SF Catheter for the treatment of cardiac arrhythmias.

- October 2024: Medtronic plc announced U.S. Food and Drug Administration (FDA) approval of the Affera Mapping and Ablation System with Sphere-9 Catheter, an all-in-one, High-Density (HD) mapping, Pulsed Field (PF), and Radiofrequency (RF) ablation catheter for treatment of persistent atrial fibrillation (AFib) and for RF ablation of Cavotricuspid Isthmus (CTI) dependent atrial flutter.

- October 2024: Boston Scientific Corporation announced it has received U.S. Food and Drug Administration (FDA) approval for the navigation-enabled FARAWAVE NAV Ablation Catheter for the treatment of paroxysmal Atrial Fibrillation (AF) and FDA 510(k) clearance for the new FARAVIEW Software, which will combine to provide visualization for cardiac ablation procedures with the FARAPULSE PFA System.

- May 2024: Johnson & Johnson announces the launch of the CARTO 3 System Version 8, the latest version of the company’s leading three-dimensional (3D) heart mapping system used in cardiac ablation procedures.

- February 2024: Johnson & Johnson announced European CE mark approval of the VARIPULSE Platform for the treatment of symptomatic drug-refractory recurrent paroxysmal AF using PFA.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Application, End-user, and Region |

| By Product |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.13 billion in 2025 and is projected to reach USD 9.63 billion by 2034.

In 2025, the market value stood at USD 2.20 billion.

The market is expected to exhibit a CAGR of 7.1% during the forecast period.

The disposable consumables segment led the market by product.

The key factors driving the market are the rising burden of cardiac rhythm disorders and preference for minimally invasive therapy.

Johnson & Johnson, Boston Scientific Corporation, Abbott, and Medtronic plc are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us