Radiotherapy Market Size, Share & Industry Analysis By Product Type (Hardware [Instruments {Linear Accelerators (LINACs), Proton Therapy Systems, Carbon Ion Therapy Systems, and Others} and Accessories] and Software), By Type (External Beam Radiotherapy [Photon Based EBRT, Particle Therapy and Others], Internal Radiation Therapy (Brachytherapy) [High-dose rate brachytherapy, Low-dose rate brachytherapy, and Others) and Systemic Radiotherapy), By Application (Breast Cancer, Prostate Cancer, Lung Cancer, Gynecological Cancer, and Others), By End User, and Regional Forecast, 2026-2034

Radiotherapy Market Size and Future Outlook

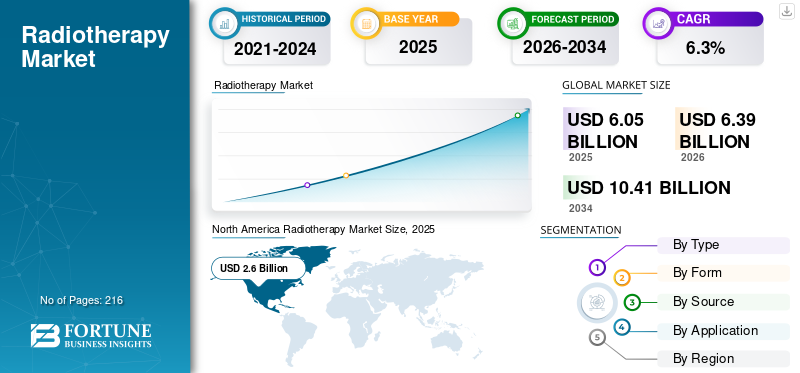

The global radiotherapy market size was valued at USD 6.05 billion in 2025 and is projected to grow from USD 6.39 billion in 2026 to USD 10.41 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period. North America dominated the global radiotherapy market with a market share of 42.98% in 2025.

Radiotherapy is a cancer treatment that uses high-energy radiation to destroy tumor cells and shrink tumors. The increasing prevalence of various types of cancer, including prostate cancer, lung cancer, and others, is resulting in a growing patient pool in healthcare settings. The increasing patient pool and advancements in radiation therapy systems are further boosting the demand for radiation therapy treatment, thereby contributing to the adoption rate of these radiotherapy devices in the market.

For instance, according to the 2025 statistics published by the American Cancer Society (ACS), approximately 226,650 new cases of lung cancer were reported in the U.S.

Additionally, the increasing preference toward non-invasive cancer treatment approaches is also a vital factor supporting the rising demand for these procedures in the market. This, along with the rising focus on acquisitions and mergers among other players, is driving the focus of major players, including Elekta, GE Healthcare, Siemens Healthineers AG, and others, and is anticipated to support the growth of the global radiotherapy market.

Download Free sample to learn more about this report.

Radiotherapy Market Key Takeaways

- 2025 Market Size: USD 6.05 Billion

- 2026 Market Size: USD 6.39 Billion

- 2034 Forecast Market Size: USD 10.41 Billion

- CAGR: 6.3% from 2026–2034

- North America dominated the radiotherapy market with a 42.98% share in 2025.

- The hardware segment held the largest market share in 2025.

- External beam radiotherapy (EBRT) is expected to account for 77.6% of the market in 2026.

North America

North America led the market with a valuation of USD 2.60 billion and a 42.98% market share in 2025.

Europe

Europe reached a market value of USD 1.74 billion in 2025 and is projected to grow at a CAGR of 6.2%.

Asia Pacific

Asia Pacific accounted for USD 1.27 billion in market value in 2025, making it the third-largest regional market.

U.S.

The U.S. radiotherapy market was estimated at USD 2.35 billion in 2025.

Japan

Japan is witnessing steady growth driven by advanced radiotherapy adoption and expanding cancer treatment infrastructure.

Read More

Market Dynamics:

Market Drivers

Increasing Prevalence of Various Types of Cancer to Support Growing Demand for Radiotherapy Procedures

The growing prevalence of various types of cancer, such as lung cancer, breast cancer, and others, is contributing to the growing demand for radiotherapy procedures among the patient population, subsequently driving the penetration rate of these products in the market.

For instance, according to data published by the World Cancer Research Fund, about 1.5 million new cases of prostate cancer were reported globally in 2022.

Moreover, the increasing focus on providing combination therapies to these patients is a vital factor supporting the rising adoption of these treatment options among patients, further boosting the demand for radiation therapy systems globally. Therefore, the factors above, along with the growing focus of major players on expanding R&D facilities to develop novel devices, are expected to drive the adoption rate, thereby contributing to the global radiotherapy market growth.

Other Prominent Drivers

A shift toward hypofractionation and ablative regimens can improve throughput and patient convenience, driving demand for precision delivery systems.

Market Restraints

High Cost Associated with Radiation Therapy Systems to Hinder the Market Growth

There is a growing demand for technologically advanced radiation therapy treatment modalities owing to their advantages, such as highly targeted treatment, among others. However, the high cost associated with these advanced products is expected to hamper the penetration rate for these systems, particularly in developing nations, including China, Mexico, and others.

The high upfront capital cost associated with installment and operation of radiation therapy systems represents a huge financial burden, particularly for small and mid-sized firms. Moreover, establishing a new radiation therapy facility is an expensive and complex process that demands substantial investment, infrastructure considerations, and others.

For instance, according to 2023 data published by the National Center for Biotechnology Information (NCBI), it was reported that the establishment of proton therapy facilities with three to four treatment rooms costs about USD 100.0 to USD 200.0 million.

Furthermore, the costs associated with regulatory compliance, continuous maintenance, software upgrades, and others add to the cost barrier, resulting in a limited penetration rate of these systems and facilities in emerging nations.

Market Opportunities

Increasing Emphasis on the Adoption of Proton Therapy Procedures to Boost Market Expansions

There is an increasing emphasis on the adoption of proton therapy procedures due to their distinct advantages, such as reduced toxicity profiles and superior dose distribution among the patient population. Healthcare facilities are prioritizing long-term survivorship outcomes, and precision oncology is leading to the growing adoption of proton therapy among patients.

Furthermore, the growing establishment of proton therapy units and favorable reimbursement policies is expanding the installation of radiation therapy systems in the market. This, along with the growing focus of prominent players on integrating artificial intelligence workflows into these products, is expected to drive the adoption rate for these systems in the market.

According to a 2025 article published by Springer Nature, there are about 125 active particle therapy centers worldwide.

Market Challenges

Limited Healthcare Expenditure in Developing Countries to Hinder the Market Growth

There is a growing focus on innovative radiation therapies for the treatment of cancer among the patient population. However, limited healthcare expenditure, shortage of technologically advanced LINAC devices, along with inadequate reimbursement frameworks, particularly in developing nations, are resulting in limited access to healthcare facilities among patients.

Additionally, a limited number of healthcare settings and limited trained radiation oncologists, among others, are some of the major factors resulting in the delayed detection of various types of cancer, resulting in the postponement of diagnostic and treatment procedures among patients, especially in emerging nations, including China, Brazil, among others.

For instance, according to 2024 data published by the International Atomic Energy Agency Directory of Radiotherapy Centres (DIRAC), it was reported that about 58 countries have no radiotherapy facilities at all in low- and low-middle-income countries.

Other Prominent Challenges

Regulatory approvals, interoperability of planning systems, and long equipment lifecycles complicate upgrade cycles and procurement decisions.

Radiotherapy Market Trends

Technological Advancements in these Devices to Create Market Opportunities

There is an increasing emphasis on the incorporation of technological advancements in these devices, which is driving a preferential shift toward precision, accuracy, and customized treatment. Technological advancements, such as proton therapy, adaptive radiotherapy, and magnetic resonance-guided therapy, among others, are enabling the delivery of accurate doses with reduced toxicity in patients.

The integration of automated devices, real-time tumor tracking, artificial intelligence, and other advanced features in these systems has accelerated workflow efficiency and improved clinical outcomes. This, along with the increasing focus of major players on R&D activities to launch technologically advanced devices such as LINACs, is expected to fuel the adoption rate for these systems in the market.

In September 2025, Accuray Incorporated launched the all-in-one radiotherapy solution Accuray Stellar Solution with an aim to strengthen its product offerings in the U.S.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Rising Demand in Advanced Radiation Therapy Devices Fuels Hardware Segment Growth

Based on product type, the market is classified into hardware and software. Hardware is further bifurcated into instruments and accessories. Additionally, instruments are further divided into linear accelerators (LINACs), proton therapy systems, carbon ion therapy systems, and others.

The hardware segment held the largest market share in 2025. The growth is due to the rising prevalence of cancer among patients, resulting in an increasing demand for advanced radiation therapy devices globally. This, along with the growing focus of key players toward R&D activities to launch innovative products, is further anticipated to support the segmental growth.

In May 2023, Brainlab, a digital medical technology company, launched ExacTrac Dynamic Surface, for radiotherapy patient positioning and monitoring that is dedicated to surface guided radiation therapy (SGRT).

The software segment is expected to grow at a CAGR of 6.9% over the forecast period.

By Type

Increasing Number of Installed Bases for EBRT Products Led to the Dominance of the Segment

Based on type, the market is segmented into external beam radiotherapy (EBRT), internal radiation therapy (brachytherapy), and systemic radiotherapy. External beam radiotherapy (EBRT) is further bifurcated into photon based EBRT, particle therapy, and others. Internal radiation therapy (brachytherapy) is divided into high-dose rate (HDR) brachytherapy, low-dose rate (LDR) brachytherapy, and others.

The external beam radiotherapy (EBRT) segment dominated the market in 2025. In 2026, the segment is anticipated to dominate with a 77.6% of the radiotherapy market share. The dominant share is due to its benefits, such as target a wide range of cancer types, efficient, improved safety, and others. This, along with the growing number of installed bases for EBRT radiation therapy products, such as LINACs, is expected to support segmental growth in the market.

According to 2021 statistics published by Elekta, there were approximately 14,000 installed bases for linear accelerators (LINACs) globally.

The systemic radiotherapy segment is expected to grow at a CAGR of 9.3% in the market during the forecast period.

By Application

Increasing Prevalence of Breast Cancer Led to the Dominance of the Segment

Based on application, the market is segmented into breast cancer, prostate cancer, lung cancer, gynecological cancer, and others.

The breast cancer segment dominated the global market in 2025 with a 25.9% market share. The growth is primarily owing to the growing prevalence of breast cancer is resulting in a rising number of radiotherapy treatment procedures among the patient population in the market.

For instance, according to the 2022 data published by the World Health Organization (WHO), it was reported that about 2.3 million women were diagnosed with breast cancer globally.

The segment of lung cancer is set to flourish with a growth rate of 7.2% across the forecast period.

By End-user

Increasing Prevalence of Various Types of Cancer Led to the Hospital and Clinics Segment’s Dominance

Based on end user, the market is segmented into hospitals & clinics, radiotherapy centers, and others.

The hospitals and clinics segment dominated the market in 2025. The increasing prevalence of various types of cancer, the growing number of healthcare facilities such as hospitals, and others are some of the crucial factors contributing to the growth of the segment in the market. Furthermore, the segment is set to hold a 71.9% share in 2025.

For instance, according to 2025 statistics published by the American Hospital Association (AHA), it was reported that there are about 6,093 hospitals in the U.S.

In addition, radiotherapy centers' end users are projected to grow at a CAGR of 7.0% during the study period.

Radiotherapy Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Radiotherapy Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America radiotherapy market held the dominant share in 2024, valued at USD 5.73 billion, and also took the leading share in 2025 with USD 6.05 billion. The dominance of the region is owing to certain factors, such as the growing prevalence of cancer, the largest revenue market with advanced technology adoption, innovative treatment plans, and strong reimbursement landscapes for various radiotherapy technologies, among others. In 2025, the U.S. market is estimated to reach USD 2.35 billion.

For instance, according to 2022 statistics published by the World Cancer Research Fund, it was reported that about 230,125 people were suffering from prostate cancer in the U.S.

Europe and the Asia Pacific

Other regions, such as Europe and the Asia Pacific, are expected to witness considerable growth in the forecast period. During the study period, the European region is projected to record a growth rate of 6.2% and reach the valuation of USD 1.74 billion in 2025. This is due to the high adoption of advanced external beam and brachytherapy technologies, centralized cancer centres, and cross‑border patient referrals influence demand in the region. Additionally, rising cancer incidence, expanding healthcare infrastructure in countries such as China, Japan, South Korea, India, and investments in particle therapy in several countries are also contributing factors to market growth. Backed by these factors, countries such as the U.K. are expected to record the valuation of USD 0.25 billion, Germany to record USD 0.42 billion, and France to record USD 0.32 billion in 2025. After Europe, the market in the Asia Pacific is estimated to reach USD 1.27 billion in 2025 and secure the position of the third-largest region in the market. In the region, India is estimated to reach USD 0.16 billion while China is estimated to reach USD 0.56 billion in 2025.

Rest of The World

Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market. The Latin America market in 2025 is set to record USD 0.25 billion as its valuation. The growing demand in urban centres, targeted expansion in larger markets, and others are anticipated to drive product adoption in these regions. In the Middle East & Africa, GCC is set to attain the value of USD 0.09 billion in 2025.

Competitive Landscape

Key Industry Players

Increasing Number of Product Launches Among the Prominent Companies to Support Their Dominance

A significant product portfolio of advanced devices, along with a strong global presence, is one of the key factors contributing to the market dominance of these players. GE Healthcare, Siemens Healthineers AG, and Elekta are crucial companies in the market in 2025. Moreover, the increasing focus of prominent players on product launches is likely to support the global radiotherapy market share.

For instance, in May 2023, GE Healthcare launched three new products for radiation therapy, such as Intelligent Radiation Therapy (iRT), Auto Segmentation, and an updated MR radiation therapy suite (AIR Open Coil Suite).

Other key players, including Accuray Incorporated, and others, are also growing in the market, primarily due to their increasing focus on R&D facility expansions among the other players to strengthen their presence in the market.

List of Key Radiotherapy Companies Profiled:

- GE Healthcare (U.S.)

- Accuray Incorporated (U.S.)

- Elekta (U.S.)

- Hitachi High-Tech Corporation (Japan)

- Koninklijke Philips N.V. (Netherlands)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Brainlab SE (Germany)

- Siemens Healthineers AG (Germany)

- IBA Worldwide (Belgium)

- Novartis AG (Switzerland)

KEY INDUSTRY DEVELOPMENTS:

- May 2025 – Standard Imaging introduced next-generation QA systems at the 2025 ESTRO Congress, including the highly anticipated MAX Elite Electrometer and a comprehensive expansion of its hardware and software portfolio. This helped the company in strengthening its presence.

- June 2024 – LEO Cancer Care collaborated with TibaRay to co-develop the next-generation upright linear accelerator (LINAC). This helped the company in strengthening its global presence.

- May 2024 – GE Healthcare launched Revolution RT, a new radiation therapy computed tomography (CT) solution with novel hardware and software solutions to help increase imaging accuracy.

- February 2024 – Siemens Healthineers AG received U.S.FDA approval for TrueBeam and Edge radiotherapy systems featuring HyperSight imaging solution with an aim to widen its product portfolio.

- June 2021 – Accuray Incorporated launched RayStation treatment planning support for the company's CyberKnife M6 and S7 Robotic Radiotherapy Systems, aiming to strengthen its product offerings.

REPORT COVERAGE

The market report provides a detailed global radiotherapy market analysis and focuses on key aspects such as leading companies, product type, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Global Radiotherapy Market Scope | |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Type, Application, End User, and Region |

| By Product Type |

|

| By Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 6.05 billion in 2025 and is projected to reach USD 10.41 billion by 2034.

In 2025, the North America regional market value stood at USD 2.60 billion.

Growing at a CAGR of 6.3%, the market will exhibit steady growth over the forecast period (2026-2034).

By product type, the hardware segment is the leading segment in this market.

The introduction of novel radiotherapy systems is one of the major factors driving the market's growth.

GE Healthcare and Elekta are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of cancer, the increasing number of system launches, among others, are some of the vital factors expected to boost the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 216

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us