Responsive Space Launch Market Size, Share & Industry Analysis, By Launch Platform (Fixed ground launch, Mobile ground launch, Air-launch, and Sea-launch), By Payload Type (Earth Observation, Communications, SIGINT/ELINT/COMINT, Space Domain Awareness (SDA)/ tracking, PNT Augmentation/Timing Payloads, Technology demonstration/experimental, Scientific/Civil Missions), By Vehicle Type, By Service Type, By End User (Defense Ministries/Armed Forces, National space organizations, Intelligence/SIGINT Authorities, Commercial Launch Providers, and Others) and Regional Forecast, 2026-2034

Responsive Space Launch Market Size and Future Outlook

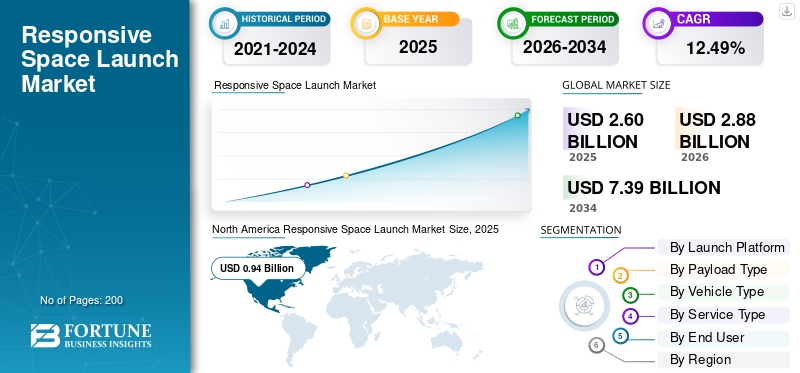

The global responsive space launch market size was valued at USD 2.60 billion in 2025. The market is projected to grow from USD 2.88 billion in 2026 to USD 7.39 billion by 2034, exhibiting a CAGR of 12.49% during the forecast period. North America dominated the responsive space launch market with a market share of 36.15% in 2025.

Responsive space launch involves launching small satellites (up to 500 kg) on demand into low Earth orbit (LEO), with operations starting within days. It encompasses small launch vehicles such as Electron, rapid payload integration (e.g., 24 hours), and responsive satellites for quick assembly. It is primarily used in defense for reconstituting lost capabilities, augmenting assets, ISR missions, and constellation replenishment amid threats. Driving factors include advancing reusable tech, miniaturization, and AI automation.

Key players include Rocket Lab, Firefly Aerospace, SpaceX, and ULA. They offer Electron for 24-hour call-up launches and standby satellites, provides OSP-4 launches.

Download Free sample to learn more about this report.

Responsive Space Launch Market Takeaways

- 2025 Market Size: USD 2.60 billion

- 2026 Market Size: USD 2.88 billion

- 2034 Forecast Market Size: USD 7.39 billion

- CAGR: 12.49% from 2026–2034

- North America dominated the responsive space launch market with a 36.15% share in 2025.

- The Reusable Launch Vehicles segment is projected to maintain strong growth, supported by the market's 12.49% CAGR during 2026–2034.

- The Mobile Ground Launch segment is expected to witness significant growth, registering an 8.62% CAGR over the forecast period.

North America

North America maintained its leading position with a market value of USD 0.94 billion in 2025, driven by strong government investments and commercial launch capabilities.

Europe

Europe is projected to reach USD 0.82 billion by 2026, expanding at a 12.19% CAGR, supported by increasing investments in defense and space infrastructure.

Asia Pacific

Asia Pacific is expected to reach USD 0.82 billion by 2026, emerging as the fastest-growing regional market due to expanding national space programs and launch capabilities.

U.S.

The market is estimated at approximately USD 0.57 billion in 2026, supported by robust defense funding and leadership in responsive launch technologies.

Japan

The market is estimated at approximately USD 0.16 billion in 2026, benefiting from growing investments in satellite deployment and responsive launch capabilities, with an estimated 13.18% CAGR during the forecast period.

Read More

RESPONSIVE SPACE LAUNCH MARKET TRENDS

AI Automation is a Key Trend in the Market

AI automation emerges as a pivotal trend in responsive launches, automating inspection, testing, and decision-making to enable hour-level timelines from checkout to launch. Combined with reusable vehicles, it supports re-launches within hours post-recovery, with multi-day cycles. Moreover, in flight, AI drives real-time fault diagnosis, mission flexibility and replanning, and fault control within seconds, boosting reliability by 1-2 orders of magnitude.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Advances in SmallSat Miniaturization to Drive Market Growth

Advances in smallsat miniaturization drive the responsive space launch market growth by enabling compact, high-performance payloads under 500 kg for rapid LEO satellite deployment. Leveraging HDI PCBs, micro vias, and repurposed processors, CubeSats and 16U variants now deliver GEO-level optical resolution and full subsystems at physical limits set by solar efficiency. This slashes development cycles to under two years, cuts launch costs via rideshares, and reduces SWaP-C for multiple satellites per vehicle. U.S. Space Force Tactically Responsive Space, miniaturized ISR sats support on-demand reconstitution against threats, with propulsion and comms shrinking to fit hour-level timelines.

MARKET RESTRAINTS

Stringent Regulations to Restrict Market Expansion

Stringent Federal Aviation Administration (FAA) licensing and International Traffic in Arms Regulations (ITAR) export controls restrain responsive space launch by imposing multi-week approvals incompatible with hour/day timelines. Operators must submit detailed payload, site, and hazard analyses under 14 CFR Part 450, including quantitative risk assessments and airspace coordination with the Air Traffic Organization (ATO), delaying TacRS demos. ITAR deems launches as "exports," requiring State Department munitions licenses for foreign components, even domestically.

MARKET OPPORTUNITIES

Proliferated LEO Constellations to Create New Market Opportunities

Proliferated LEO constellations create significant market opportunities in responsive space launch by demanding frequent launches in satellite replenishment to maintain resilient architectures against threats. USSF TacRS missions such as Victus Sol prioritize rapid deployment of ISR smallsats to fill gaps in large constellations vulnerable to ASAT attacks. With thousands of satellites in mega-constellations facing annual attrition from failures and maneuvers, dedicated small launchers enable on-demand top-ups without rideshare delays.

MARKET CHALLENGES

Supply Chain-Volatility to Present a Major Market Challenge

Supply chain volatility hampers responsive space launch as sole-source dependencies on specialized components such as radiation-hardened electronics and propulsion systems cause production delays. ITAR restrictions limit global sourcing, exacerbating shortages of focal plane arrays and amplifiers with high scrap rates. In the U.S., the surging Department of Defense (DoD) demand competes with commercial aerospace for capacity, extending lead times for smallsat and launcher builds.

Segmentation Analysis

By Launch Platform

Infrastructure Reliability to Boost the Fixed Ground Launch Segmental Growth

Based on launch platform, the market is segmented into fixed ground launch, mobile ground launch, air-launch, and sea-launch.

The fixed ground launch segment is anticipated to account for the largest market share. The segmental share is driven by the need for reliable, cost-effective launch infrastructure that can rapidly deploy small satellites such as those at Cape Canaveral, Vandenberg, and Rocket Lab’s Complex 1.

The mobile ground launch segment is anticipated to rise with the highest CAGR of 8.62% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Payload Type

Rapid Need for Near-Real-Time Data for Surveillance Boosted Earth Observation Segment Growth

Based on payload type, the market is segmented into earth observation, communications, SIGINT/ELINT/COMINT, Space Domain Awareness (SDA)/tracking, PNT augmentation/timing payloads, technology demonstration/experimental and Scientific/civil missions.

In 2025, the earth observation segment dominated the global market. The segmental growth is due to the need for near-real-time data for surveillance, disaster monitoring, and environmental tracking.

The Space Domain Awareness (SDA)/tracking segment is projected to grow at a highest CAGR of 8.73% over the forecast period.

By Vehicle Type

Surge in Demand for Small Satellites & Constellations to Boost the Small Launch Vehicles Segment Growth

Based on vehicle type, the market is segmented into small launch vehicles, medium launch vehicles (configured for rapid call-up/rapid integration), solid-based quick-reaction launch vehicles, reusable launch vehicles (partial or full reuse), and air-launched rockets.

The small launch vehicles segment is anticipated to witness a dominating responsive space launch market share over the forecast period. The segmental dominance is owing increase in demand for satellite constellations for remote sensing, ISR, and earth observation which requires dedicated launches.

The reusable launch vehicles segment is projected to grow at a highest CAGR of 8.68% over the forecast period.

By Service Type

Rapid Response & High Cadence to Boost On-demand dedicated launch Segment Growth

Based on service type, the market is segmented into On-demand dedicated launch, responsive rideshare, capacity reservation/slot booking, Standby/alert launch service (launch-on-order), launch campaign & ground operations services (multi-spaceport/expeditionary), mission design, range, safety & licensing services, and sustainment/refurbishment/turnaround services.

The on-demand dedicated launch segment is anticipated to witness a dominating market share over the forecast period. The segmental dominance is owing to dedicated launch providers prioritizing high-frequency, "on-demand" scheduling, which enables satellites to be launched within days or weeks of readiness.

The standby/alert launch service (launch-on-order) segment is projected to grow at a highest CAGR of 8.68% over the forecast period.

By End User

Increasing Demand for Space Surveillance Boosted the Defense Ministries/Armed Forces Segment

Based on end user, the market is segmented into Defense ministries/armed forces, National space organizations, intelligence/SIGINT authorities, commercial launch providers, and others.

The defense ministries/armed forces segment dominated the segmental market share. The segmental dominance is due to the fact that defense forces require direct, all-weather, and real-time 24/7 monitoring capabilities for ISR to track adversary movements.

Intelligence/SIGINT authorities are projected to grow at a high CAGR of 8.54% during the study period.

Responsive Space Launch Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America held the dominant share in 2024, valued at USD 0.85 billion, and also maintained its leading position in 2025, with USD 0.94 billion. North America dominates responsive space launch due to the U.S. Space Force's (USSF) aggressive TacRS program, featuring Victus Nox's 27-hour satellite-to-launch demo and 2026 OSP-4 missions for rapid ISR reconstitution amid contested orbits.

North America Responsive Space Launch Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

U.S. Responsive Space Launch Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.57 billion in 2026, accounting for roughly 12.90% CAGR. The U.S. leads via USSF's Space Systems Command, advancing TacRS prototypes, prioritizing hour/day timelines for satellite processing, launch, and on-orbit ops to deter orbital disruptions.

Europe

Europe is projected to record a steady growth rate of 12.19%, during the forecast period, which is the second-highest among all regions, and reach a valuation of USD 0.82 billion by 2026. Europe pursues responsive capabilities through ESA's orbital transfer vehicles and national programs.

U.K. Responsive Space Launch Market

The U.K. market in 2026 is estimated at around USD 0.25 billion, representing roughly 12.56% CAGR during the study period. The U.K. advances responsive launch via Skyrora's Spectrum vehicle, aiming for frequent smallsat missions from Sutherland to support defense constellations.

Germany Responsive Space Launch Market

Germany’s market is projected to reach approximately USD 0.21 billion in 2026. Germany funds Isar Aerospace's Spectrum rocket for responsive LEO operations, integrating with USSF TacRS-such as demos for European sovereignty in contested space.

Asia Pacific

The Asia Pacific region is estimated to reach USD 0.82 billion in 2026 and secure the position of the third-largest region in the market and fastest-growing during the study period. The region grows via sovereign programs, with Japan, China, and India building small launcher fleets for resilient LEO architectures against regional threats.

Japan Responsive Space Launch Market

The Japanese market in 2026 is estimated at around USD 0.16 billion, accounting for roughly 13.18% of the compound annual growth rate (CAGR) during the forecast period. JAXA and Mitsubishi Heavy Industries develop small launchers for TacRS-equivalent ops, enhancing US alliance deterrence in Indo-Pacific.

China Responsive Space Launch Market

China’s market is projected to be one of the largest in the Asia Pacific, with 2026 revenues estimated at around USD 0.25 billion. China rapidly scales responsive launch through CASIC's small rockets, enabling proliferated ISR constellations for South China Sea monitoring and anti-access denial.

India Responsive Space Launch Market

The Indian market in 2026 is estimated at around USD 0.21 billion. ISRO's SSLV supports responsive smallsat deployment, with DRDO investments for military rapid replenishment amid border tensions.

Rest of the World

The rest of the world include Middle East & Africa and Latin America. Latin America witnesses nascent efforts via Brazil's ALCOM Saturn VLS for regional LEO access. The Middle East advances with the UAE's Yah Satellite Services exploring responsive ISR. The Middle East & Africa and Latin America market is set to reach a valuation of USD 0.13 billion and USD 0.08 billion, respectively, in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships Fuel Responsive Space Launch Market Expansion

The responsive space launch market exhibits moderate consolidation dominated by agile smallsat launch specialists such as Rocket Lab, Firefly Aerospace, SpaceX, and ULA, leveraging NSSL contracts and TacRS demonstrations for DoD primacy.

Partnerships accelerate growth as Rocket Lab collaborates with USSF on 24-hour Electron call-ups for Victus missions, Firefly secures OSP-4 with Space Systems Command for rapid ISR, and SpaceX/ULA integrate responsive tiers within Phase 3 NSSL. These alliances fortify supply resilience amid proliferated LEO constellations and geopolitical orbital threats.

LIST OF KEY RESPONSIVE SPACE LAUNCH COMPANIES PROFILED

- Rocket Lab (U.S.)

- Firefly Aerospace (U.S.)

- SpaceX (U.S.)

- United Launch Alliance (ULA) (U.S.)

- Relativity Space (U.S.)

- Blue Origin (U.S.)

- Isar Aerospace (Germany)

- Skyrora (U.K.)

- PLD Space (Spain)

- Skyroot Aerospace (India)

- China aerospace science and technology corporation (China)

KEY INDUSTRY DEVELOPMENTS

- December 2025: The STP-S30 mission will be deployed by Rocket Lab Corporation, a world leader in launch services and space systems, on its upcoming Electron launch for the Space Systems Command (SSC) of the U.S. Space Force (USSF).

- September 2025: Space Systems Command officials hosted a National Security Space Launch (NSSL) Industry Day with representatives from 17 commercial space businesses to help commercial launch service and space capability providers prepare for NSSL Phase 3 Lane 1 on-ramp opportunities.

- April 2025: The U.S. Department of Defense's (DoD) Defense Innovation Unit (DIU) Sinequone Project granted Firefly Aerospace, a leader in end-to-end responsive space services, a contract to use its Elytra spacecraft to conduct a responsive on-orbit mission.

- February 2025: Firefly Aerospace received a USD 21.81 million contract from Space Systems Command for "Victus Sol," the fifth of a series of tests intended to force contractors and USSF to create, transport, and launch satellites at record speed.

- October 2024: The Space Force awarded Impulse Space a USD 34.5 million contract for two missions involving ultra-mobile spacecraft. The two missions would show how highly maneuverable spacecraft can assist the military in quickly responding to threats in space as part of the Space Force’s Tactically Responsive Space (TacRS) program.

REPORT COVERAGE

The global responsive space launch industry analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, Porter’s five forces analysis, company profiles, and the retrofitting program. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.49% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Launch Platform, Payload Type, Vehicle Type, Service Type, End User, and Region |

| By Launch Platform |

|

| By Payload Type |

|

| By Vehicle Type |

|

| By Service Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.60 billion in 2025 and is projected to reach USD 7.39 billion by 2034

In 2025, the market value stood at USD 0.94 billion.

The market is expected to exhibit a CAGR of 12.49% during the forecast period (2026-2034).

By launch platform, the fixed ground launch segment is expected to dominate the market.

Advances in SmallSat Miniaturization is the key factor driving market growth.

Rocket Lab, Firefly Aerospace, SpaceX, United Launch Alliance (ULA), Relativity Space, Blue Origin are few key players in the global market.

North America dominated the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us