Reusable Launch Vehicle Market Size, Share & Industry Analysis, By Type (Partially Reusable and Fully Reusable), By Orbit Type (Low-Earth Orbit (LEO) and Geosynchronous Transfer Orbit (GTO)), By Vehicle Capacity (Up to 1000 Kg, 1000 Kg to 3000 Kg, and Above 3000 Kg), By Application (Commercial and Defense), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

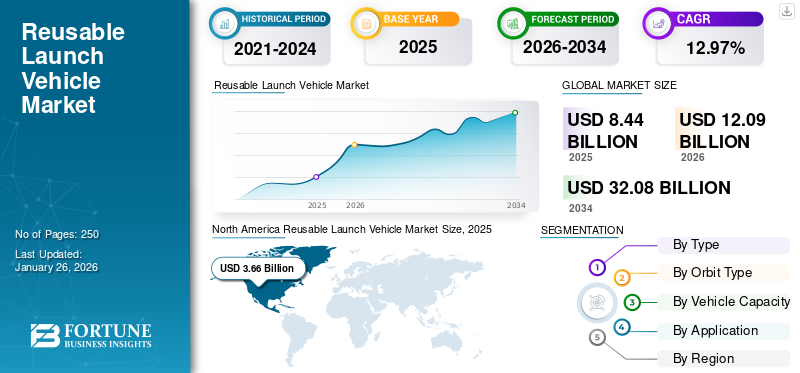

The global reusable launch vehicle market size was valued at USD 8.44 billion in 2025 and is projected to grow from USD 12.09 billion in 2026 to USD 32.08 billion by 2034, exhibiting a CAGR of 12.97% during the forecast period. North America dominated the reusable launch vehicle market with a market share of 43.41% in 2025.

Reusing launch vehicles allows the same parts to be utilized repeatedly, thereby significantly lowering the launch costs compared to those of conventional expendable rockets. This financial advantage increases accessibility to space for a wider array of customers, including commercial businesses and smaller countries, which will drive the global reusable launch vehicle market growth. For instance, in November 2024, the Falcon 9 successfully lifted off 24 Starlink satellites into Low-Earth Orbit (LEO) from Space Launch Complex 40 (SLC-40) located at Cape Canaveral Space Force Station in Florida.

The major players and emerging countries are heavily investing in reusable technology for cost saving. Companies, such as SpaceX and Blue Origin have illustrated the financial advantages of reusability through successful missions that showcase decreased operational expenses. For instance, SpaceX's Falcon 9 has proven that reusing rocket stages can lower launch costs by 30-40%.

A Reusable Launch Vehicle (RLV) is a space launch system designed to enable either complete or partial recovery of rocket stages after sending a satellite into orbit. The main objective of an RLV is to reduce the expenses associated with single-stage and multi-stage satellite launches by recapturing crucial systems and components that have been expended.

Download Free sample to learn more about this report.

Global Reusable Launch Vehicle Market Key Takeaways

Market Size & Forecast

- 2025 Market Size: USD 8.44 billion

- 2026 Market Size: USD 12.09 billion

- 2034 Forecast Market Size: USD 32.08 billion

- CAGR: 12.97% from 2026–2034

Market Share

- North America dominated the reusable launch vehicle market with a 43.41% share in 2025, driven by major players like SpaceX and Blue Origin, government initiatives through NASA and DoD, and rapid adoption of cost-saving reusable technologies.

- By orbit type, Low-Earth Orbit (LEO) accounted for the largest share in 2024 due to its suitability for small satellites, reduced launch costs, and increased demand for broadband networks like Starlink and OneWeb.

Key Country Highlights

- United States: Leads globally with significant R&D investments, successful Falcon 9 missions, and active government support for reusable technologies.

- China: Emerging as a key competitor, conducting vertical takeoff and landing tests for RLVs and investing heavily in indigenous launch programs.

- India: Advancing reusable and hybrid rockets through ISRO and private startups like Space Zone India, focusing on cost-efficient solutions for small satellites.

- Europe (France, Germany): ESA fosters public-private partnerships, supporting companies like ArianeGroup and Rocket Factory Augsburg to develop next-gen reusable systems.

Market Dynamics

Market Drivers

Demand for Satellite Launches to Significantly Contribute to Growth of Reusable Launch Vehicle Industry

Surge in the need for satellite networks, which encompass communications, Earth observation, and scientific research, has resulted in a higher frequency of satellite launches. This growing requirement for satellites is fueled by applications, such as military surveillance, navigation, and broadband services, which necessitate regular and dependable launch services.

For instance, in November 2024, scientists at Kyoto University initiated the launch of LignoSat, the world’s first wooden satellite, with the aim of creating sustainable habitats beyond Earth. Constructed from a type of magnolia that is customarily utilized in Japanese sword sheaths, this satellite intends to demonstrate wood as a viable alternative material for structures in space.

In addition, the launch of small satellites into Low Earth Orbit (LEO) is especially significant. The growing frequency of small satellite missions requires affordable launch options, which makes Reusable Launch Vehicles (RLVs) appealing as they can be used several times, thereby reducing the cost of each launch.

Market Restraints

High Development and Operational Costs and Cost Competitiveness to Hinder Market Growth

Promoting RLV technologies demands significant financial investment for research, development, and testing. The expenses related to cutting-edge materials, innovative propulsion systems, and complex manufacturing techniques can be overwhelming, particularly for smaller firms or new players in the industry.

The engineering involved in designing vehicles for multiple reuses is quite complex. This encompasses the restoration of rocket stages, verifying that heat shielding systems can endure re-entry conditions, and successfully executing vertical landings of boosters. These challenges result in higher development costs and operational expenses, which include refueling and retrofitting tasks between launches.

Reusable Launch Vehicles (RLVs) need to attain cost efficiency to compete with conventional expendable rockets. The upfront investment needed for RLVs usually leads to launch costs that are higher than those of expendable rockets, making them less appealing to prospective clients unless substantial cost effectiveness is realized through innovative approaches.

Market Opportunities

Market Poised for Growth Due Opportunities in Space Exploration Initiatives and Technological Advancements

International Market Expansion – Countries, such as China and India are actively pursuing indigenous space capabilities and investing in RLV technologies to enhance their space programs. This trend will open new markets for RLV manufacturers as these nations seek to establish robust space launch capabilities at lower costs.

Increased collaboration between governments, private companies, and international space agencies can lead to shared investments in the development of RLV technologies. Such partnerships can accelerate innovation and expand the market’s reach globally.

Growth of Space Tourism – The burgeoning interest in space tourism presents a significant opportunity for RLVs. As private companies look to offer suborbital and orbital experiences to paying customers, the demand for reliable and cost-effective launch solutions will increase. RLVs are well-suited to meet this need due to their reusability and associated cost savings.

Technological Advancements - Rapid advancements in materials science, propulsion systems, and manufacturing processes enhance the reliability and performance of RLVs. Technologies, such as 3D printing and improved heat shield materials contribute to the construction of more durable vehicles that are capable of withstanding multiple launches.

The development of autonomous landing systems and advanced navigation technologies is improving the efficiency of RLV operations. These innovations facilitate quicker turnaround times between launches, which is critical for commercial operators seeking to maximize their launch schedules.

Market Challenges

Operational Challenges, Market Competition, and Regulatory & Environmental Concerns to Hinder Market Growth

The engineering required for Reusable Launch Vehicles (RLVs) is intricate as it encompasses sophisticated recovery and refurbishment methods. Achieving the ability to reuse these vehicles multiple times without notable deterioration presents considerable technical hurdles that need to be tackled to guarantee safety and reliability.

Although RLVs are built with reusability in mind, the expenses related to maintenance, refurbishment, and recovery can be significant. To ensure that RLVs are economically competitive with traditional Expendable Launch Vehicles (ELVs), these ongoing costs need to be managed efficiently.

Currently, there are only a limited number of operational Reusable Launch Vehicle (RLV) systems, such as SpaceX's Falcon 9, which makes it difficult to reliably assess costs and performance using historical data. This scarcity of information results in uncertainties regarding RLV costs and may discourage investment in new initiatives.

The space sector is governed by stringent regulatory frameworks that may hinder the progress and implementation of emerging technologies. Maneuvering through these regulations can pose a considerable obstacle for firms aiming to innovate in the RLV domain. As the sector expands, there is heightened examination of the ecological effects of rocket launches. Businesses must tackle these issues while implementing sustainable methods that correspond with the global environmental objectives.

Reusable Launch Vehicle Market Latest Trends

Market Trends Are Driven by Advancements in Engineering and Increasing Demand for Satellite Services

Rising Need for Small Satellites – The increasing popularity of small and Nano-satellites has driven the creation of specialized Small Satellite Launch Vehicles (SSLVs). These launch systems are designed for speedy and effective launches, addressing the growing demand for small satellite placements.

For instance, in June 2024, NASA announced that it was preparing to launch multiple small satellites into space, which were developed with the assistance of students, educators, and researchers from around the nation. This was a part of the agency's CubeSat Launch Initiative.

In addition, smaller, modular launch vehicles are becoming more popular as they can be tailored for specific missions, thereby enhancing flexibility in satellite deployment and catalyzing the market’s growth.

- North America witnessed reusable launch vehicle market growth from USD 2.73 Billion in 2023 to USD 3.38 Billion in 2024.

Advanced Propulsion Technologies – In recent times, the approach to space exploration activities has moved toward sustainability, prompting the creation of environmentally friendly substitutes for conventional rocket fuels. A significant area experiencing groundbreaking advancements is the creation of green propellants for future launch vehicles and spacecraft.

A move is being made toward eco-friendly propellants that minimize the environmental effects of rocket launches. This development corresponds with the global sustainability objectives and regulatory demands. For instance, in January 2024, Bengaluru-based Bellatrix Aerospace achieved successful validation for its advanced Rudra and Arka propulsion systems for operation in the extreme environment of space. The Rudra green propulsion system signifies a groundbreaking transition from conventional toxic propellants, such as hydrazine to a high-performance, non-toxic substitute.

Integration of AI and Automation – The integration of artificial intelligence into launch systems is improving both their operational efficiency and reliability. AI can refine flight trajectories, oversee payload integration, and enhance mission planning.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Growing Investment in and Development of Fully Reusable Vehicles to Minimize Cost Drives Segment’s Growth

Based on type, the market is segmented into partially reusable and fully reusable.

The fully reusable segment is anticipated to hold a dominant market share of 69.69% in 2026. The segment is experiencing significant growth, driven by advancements in technology and increasing demand for cost-effective access to space. Moreover, fully reusable launch vehicles significantly reduce the costs associated with space launches by allowing the same components to be used multiple times. This capability makes space missions more affordable for various sectors, including government, commercial, and scientific research.

For instance, August 2024, EtherealX, a space startup from India, successfully secured USD 5 million in a seed funding round, intending to create fully reusable medium-lift launch vehicles that will make satellite launches both affordable and prompt.

By Orbit Type

Significant Advantages of Low Earth Orbit (LEO) for Several Applications Propel Segment’s Growth

Based on orbit type, the market is segmented into Low-Earth Orbit (LEO), and Geosynchronous Transfer Orbit (GTO).

The Low Earth Orbit (LEO) segment is poised to account for 78.22% of the market share in 2026. The benefits of reduced latency, affordability, flexibility, enhanced performance, reduced costs, wide-ranging coverage, continuous technological progress, and improved service delivery will increase satellite launches into the Low-Earth Orbit (LEO).

Moreover, major players, such as SpaceX and OneWeb are leading the way in low-Earth orbit satellite networks that are designed to deliver global internet services, thereby showcasing a significant level of market interest in the commercial sector. For instance, in December 2023, SpaceX launched 23 Starlink v2 mini satellites in the Low-Earth-Orbit.

By Vehicle Capacity

Rising Demand for Small Satellites and Cost Efficiency to Fuel Production of Vehicles Weighing Up to 1,000 Kg

Based on vehicle capacity, the market is divided into up to 1,000 kg, 1,000 kg to 3,000 kg, and above 3,000 kg.

The up to 1,000 kg segment is expected to lead the market, contributing 46.73% globally in 2026. The increasing deployment of small satellites for applications, such as Earth observation, telecommunications, and IoT is a primary driver of the segment’s growth. These low-capacity vehicles are well-suited for these missions as they can efficiently deliver multiple small satellites in a single launch. Moreover, the reduced expenses offer considerable advantages in terms of savings when compared to the conventional large rockets. By conducting multiple launches using the same parts, they lower the total cost per launch, which makes access to space more economical for both commercial organizations and governments.

- The 1,000 kg to 3,000 kg segment is expected to hold a 22.57% share in 2024.

To know how our report can help streamline your business, Speak to Analyst

By Application

Rising Deployment of Commercial Satellite Within Space Sector to Catalyze Segment’s Growth

Based on application, the market is categorized into commercial and defense.

The commercial segment is estimated to be the fastest-growing segment during the forecast period, accounting for a 77.19% market share in 2026. The increase in commercial satellite launches is fueled by the expansion of satellite constellations, technological advancements in launch vehicles, economic growth in the space sector, regulatory improvements that facilitate access to launch services, and rising interest in space tourism. These factors collectively create a robust environment for market’s growth in the commercial sector. For instance, in November 2024, SpaceX sent India’s GSAT-N2 satellite into orbit aboard a Falcon 9 rocket, taking off from Cape Canaveral. This mission marked SpaceX's second collaboration with a customer as it successfully deployed a communications satellite for NewSpace India Limited (NSIL), which is the commercial arm of the Indian Space Research Organization (ISRO) and is operated by the government. This launch represented the inaugural occasion of SpaceX carrying a payload for India. The Geosynchronous Satellite N2 (GSAT-N2) is the second demand-driven satellite for NSIL.

Reusable Launch Vehicle Market Regional Outlook

With respect to region, the market covers North America, Europe, Asia Pacific, and the rest of the world.

Europe

North America Reusable Launch Vehicle Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Europe generated USD 2.5 billion, contributing 29.66% to global market revenue, and is projected to grow to USD 3.62 billion in 2026. The ESA is actively investing in RLV technologies and fostering partnerships with commercial entities to enhance Europe’s capabilities in space. This support is crucial for the development of a robust RLV ecosystem. For instance, in October 2024, the European Space Agency chose Rocket Factory Augsburg, The Exploration Company, ArianeGroup, and Isar Aerospace to create advanced technologies for reusable rockets. Moreover, through government backing, collaboration with the private sector, and substantial funding programs, Europe seeks to enhance its Reusable Launch Vehicle (RLV) capabilities to satisfy the growing demand while prioritizing sustainability and cost-efficiency in space exploration. As these initiatives advance, Europe is poised to become an important participant in the global reusable launch vehicle market growth. The UK market is projected to reach USD 1.14 Billion by 2026, while the Germany market is projected to reach USD 0.45 Billion by 2026.

North America

North America maintained a strong presence in the global market, reaching USD 3.66 billion in 2025, accounting for 43.41% share, and is expected to reach USD 5.23 billion in 2026. The ability to refurbish and reuse rocket components makes space access more affordable for a wider range of customers, including small-scale commercial enterprises and smaller nations. In addition, the U.S. government, through agencies, such as NASA and the Department of Defense, actively supports RLV development with funding and favorable regulatory frameworks. This backing fosters a robust ecosystem of aerospace companies, startups, and research institutions focused on advancing reusable technologies. The U.S. market is projected to reach USD 4.71 Billion by 2026.

Asia Pacific

The Asia Pacific market accounted for USD 1.84 billion in 2025, representing 21.77% of the global industry, and is expected to reach USD 2.64 billion in 2026. Asia Pacific is emerging as a significant player in the Reusable Launch Vehicle (RLV) market, with various countries making substantial investments to enhance their space capabilities. This investment is driven by the increasing demand for satellite launches, advancements in technology, and a strategic focus on developing indigenous space programs. Moreover, the Chinese government is heavily investing in RLV technology as part of its broader space ambitions. For instance, in July 2024, China completed its inaugural 10-kilometer (6.2-mile) vertical takeoff and landing flight test of a reusable launch vehicle. Furthermore, India's growing private space sector is also contributing to the RLV’s developments, with startups focusing on creating cost-effective launch solutions for small satellites. For instance, in August 2024, India introduced its first reusable hybrid rocket, RHUMI-1, which was developed by the start-up Space Zone India, in collaboration with the Martin Group. The Japan market is projected to reach USD 0.51 Billion by 2026, the China market is projected to reach USD 1.16 Billion by 2026, and the India market is projected to reach USD 0.66 Billion by 2026.

Rest of the World

In the rest of the world, moderate growth is anticipated in the market in the Middle East and Africa throughout the study period. Rest of the World accounted for USD 0.44 billion in 2025, representing 5.16% of the global market share, and is projected to reach USD 0.61 billion in 2026. This growth is due to a heightened emphasis on the development of the space sector and the initiation of ambitious space programs by countries, such as Israel, Saudi Arabia, and the United Arab Emirates, among others. Meanwhile, in Latin America, countries primarily concentrate on space services and equipment linked to space activities. The market’s expansion in this region is projected to be fueled by an increase in contracts for space launches in Brazil, Argentina, and Colombia.

Competitive Landscape

Key Industry Players

Leading Market Players Are Focusing on Technological Advancements to Enhance Various Applications for Space Missions

The global market is experiencing rapid growth, driven by technological improvements, increasing demand for satellite launches, and significant investments from both private companies and government organizations. Key industry players are committing substantial resources to research and development to improve reusability and decrease expenses. As new competitors join the market and established firms continue to innovate, it is anticipated that the market will develop quickly, establishing RLVs as essential for future space exploration and commercialization initiatives. For instance, in November 2023, a manufacturer of launch vehicles in China announced that it was developing designs for a rocket that will be air-launched to place small satellites into orbit. The China Academy of Launch Vehicle Technology (CALT) is creating the system with the capacity to carry a payload weighing up to 300 kilograms to a Sun-Synchronous Orbit (SSO) at an altitude of 500 kilometers.

LIST OF KEY COMPANIES PROFILED

- Space Exploration Technologies Corp. (SpacX) (U.S.)

- Blue Origin Enterprises, L.P. (U.S.)

- ISRO (India)

- European Space Agency (France)

- Rocket Lab (U.S.)

- ArianeGroup (France)

- The National Aeronautics and Space Administration NASA (U.S.)

- Lockheed Martin Corporation (U.S.)

- United Launch Alliance, LLC (U.S.)

- The Boeing Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2024: - AVIC of China obtained a contract from the China Manned Space Agency to create a winged, reusable spacecraft known as Haolong. This reusable spacecraft is reportedly designed to transport cargo to China’s Tiangong space station.

- March 2024: - China's primary state-owned contractor announced that it intended to conduct test flights for two new large-diameter reusable rockets within the next few years, even with ongoing commercial reusability initiatives. The China Aerospace Science and Technology Corporation (CASC) aims to debut four-meter and five-meter-diameter reusable rockets in 2025 and 2026, respectively.

- May 2024: - Tokyo-based Innovative Space Carrier Inc. collaborated with a U.S.-based rocket engine manufacturer to create a reusable rocket for satellite launches, with plans for commercial deployment by approximately 2030.

- September 2024: - The Union Cabinet gave its approval for the creation of a partially-reusable Next Generation Launch Vehicle (NGLV), which will have three times the payload capacity of ISRO's Launch Vehicle Mark III, known as its workhorse. It set aside USD 824 Mn for the NGLV's development, three test flights, necessary facilities, program management, and the launch campaign.

- June 2024: - The Indian Space Research Organization (ISRO) successfully completed its third consecutive reusable launch vehicle landing experiment, showcasing the autonomous landing capability of the vehicle in more demanding conditions.

REPORT COVERAGE

The report provides an in-depth market analysis. It comprises all major aspects, such as R&D capabilities, supply chain management, competitive landscape, and optimization of manufacturing capabilities and operating services. Moreover, it offers insights into the global market trends, growth analysis, and size, and highlights key industry developments. In addition to the above-mentioned factors, the report mainly focuses on several factors that have contributed to the growth of the global market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.97% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Orbit Type

|

|

|

By Vehicle Capacity

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

As per a study by Fortune Business Insights, the market size was valued at USD 8.44 billion in 2025.

The market is likely to record a CAGR of 12.97% over the forecast period.

By orbit type, the LEO segment led the market.

North America dominated the reusable launch vehicle market with a market share of 43.41% in 2025.

The demand for satellite launches will significantly contribute to the growth of the market.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us