Rocket Engine Market Size, Share & Industry Analysis, By Propulsion Type (Chemical, Electric, and Nuclear), By Chemical (Liquid, Solid, and Hybrid), By Stage (Single-stage and Multi-stage), By End-User (Commercial and Government & Military), and Regional Forecast, 2026-2034

Rocket Engine Market Size and Industry Overview

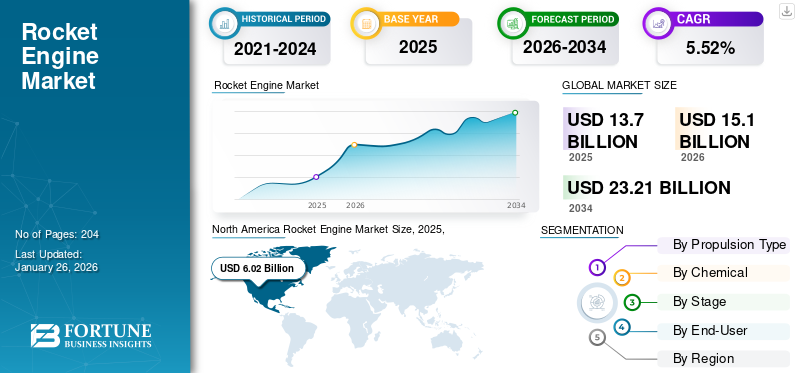

The global rocket engine market size was valued at USD 13.70 billion in 2025 and is projected to grow from USD 15.10 billion in 2026 to USD 23.21 billion by 2034, exhibiting a CAGR of 5.52% during the forecast period. North America dominated the rocket engine market with a market share of 44.44% in 2025.

A rocket engine is a reaction engine that generates thrust by expelling hot gases through its nozzle to propel the rocket forward. This expelled mass is typically a high-speed jet of high-temperature gas, which is produced by burning rocket propellants stored within the rocket. Solid rocket engines offer simplicity and reliability using a pre-mixed solid propellant, while liquid engines provide higher performance and control with separate liquid fuel and oxidizer. Hybrid engines blend solid fuel with a liquid or gas oxidizer, seeking a balance between simplicity and controllability for potential safety and cost advantages. Each type suits different mission needs based on performance, complexity, and operational requirements.

The market is growing rapidly due to increasing demand for satellite launches, military modernization, and space tourism, alongside innovations in 3D printing and AI-driven manufacturing. Companies such as SpaceX are developing reusable engine technology to lower costs, while Aerojet Rocketdyne develops high-performance propulsion systems for defense missions. Other companies in the market such as Ursa Major are focused on the development of advanced engines such as solid rocket motors for various space missions.

Download Free sample to learn more about this report.

ROCKET ENGINE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 13.70 billion

- 2026 Market Size: USD 15.10 billion

- 2034 Forecast Market Size: USD 23.21 billion

- CAGR: 5.52% from 2026–2034

- North America held a 44.44% market share in 2025.

- Chemical propulsion is projected to account for 92.82% of the market in 2026.

- Commercial end-users are expected to hold a 64.28% market share in 2026.

North America

North America held a 44.44% market share in 2025.

Asia Pacific

Asia Pacific accounted for 29.92% of the market in 2025.

Europe

Europe represented 20.73% of the market in 2025.

U.S.

U.S.: The market is projected to reach USD 5.99 billion in 2026.

Japan

Japan: The market is projected to reach USD 1.00 billion in 2026.

Read More

Market Dynamics

Market Drivers

Increase in Number of Satellite Launches Augment Market Growth

There is a surge in launch activities driven by government and commercial entities. Various commercial entities and government agencies around the globe have ambitious plans to deploy a significant number of satellites into low-Earth orbit constellations. These constellations will support various applications, from enhanced communication networks and internet services to advanced Earth observation and remote sensing capabilities. Therefore, there is a rise in demand for such engines to launch these satellites into desired orbits in space. The number of satellite launches reached 259 in the year 2024. SpaceX led launch trends with 152 launches, deploying nearly 2,000 Starlink satellites, while military spacecraft deployments rose by 86%. Senegal and Croatia deployed their first satellites, increasing the number of nations with active satellites to 92. Moreover, between 2023 and 2032, market intelligence firm Euroconsult forecasts an average of over 2,800 satellites will be launched each year, which is about 8 satellites per day, with a total mass of 4 tons. Therefore, this increase in launch frequency leads to a surge in demand for engines, which will be used to conduct these launch missions. Therefore, an increasing number of rocket launches is expected to drive the growth of the market during the forecast period.

Rise in Investment in Space Industry to Propel Market Growth

The surge in investment in the space industry is also a critical driver for the growth of the market. The investment is carried out for space exploration initiatives, satellite technology development, commercial space ventures, and various aerospace projects. In 2024, global government space spending reached a record USD 135 billion, a 10% increase from the previous year, driven mainly by defense spending, which now accounts for 54% of space budgets, totaling USD 73 billion.

Moreover, a World Economic Forum report, in collaboration with McKinsey & Company, projects the space economy will reach USD 1.8 trillion by 2035, up from USD 630 billion in 2023. This investment fuels research and development efforts focused on improving engine efficiency, reducing manufacturing costs, and exploring innovative propulsion concepts. These advancements are crucial for supporting the expansion of space exploration, the deployment of satellite constellations, and the growth of the commercial space sector. Therefore, a rise in investment remains a pivotal driver for sustained growth and innovation within the market.

Market Restraints

High Investment Hinder Entry of New Players in Rocket Engine Market

The high investment required for the production and procurement of the machines and equipment to manufacture the engines for rocket is expected to hinder the growth of the market. Engines used for rockets are complex systems reliant on advanced combustion technologies for efficient spacecraft propulsion, necessitating significant R&D investment and specialized, high-cost components.

Developing state-of-the-art engines demands advancements in materials science, thermodynamics, and combustion engineering. Funding is crucial for R&D programs, testing infrastructure, and attracting specialized personnel. Manufacturing processes entail intricate procedures and rigorous quality control, further increasing costs. The expenses associated with materials, precision manufacturing, and testing significantly contribute to the overall capital investment, which is expected to hamper the market growth.

Market Opportunities

Development of Advanced Propulsion System Act as Growth Opportunity

The market is evolving beyond traditional chemical propulsion systems. Two noteworthy trends gaining traction are the development of solar sailing technology and the advancement of hybrid propulsion systems, presenting both opportunities and potential disruptions to the established market.

Solar sailing, which harnesses solar radiation pressure for thrust, offers a propellant-less alternative for certain mission profiles. For instance, in April 2024, the National Aeronautics and Space Administration (NASA) Advanced Composite Solar Sail System (ACS3) successfully deployed its solar sail in space after its launch. The ACS3 mission is testing new lightweight composite booms that are more compact and efficient than previous designs, with the goal of using sunlight for propulsion. Such technological advancement in the material and structure of traditional engines is expected to bring opportunities for the expansion of the market.

Moreover, hybrid propulsion systems offer a balance between the simplicity of solid rockets and the controllability of liquid rockets. This combination results in increased safety, reduced environmental impact, and potential cost savings. Many manufacturers are involved in the development and testing of hybrid engine technology for rockets to expand access to space and promote environmental sustainability. For instance, in January 2025, SpaceForest, a Polish suborbital launch company, successfully test-fired an enhanced SF-1000 hybrid rocket engine, supported by approximately USD 2.5 million in co-funding from the European Space Agency. This project aims to advance SpaceForest's PERUN rocket, designed to carry 50-kilogram payloads to 150-kilometer altitudes and involves upgrades to the engine, manufacturing, and ground infrastructure. Such developments are expected to stimulate the sustained growth of the market.

Market Challenges

Regulatory Challenges to Hamper Market Growth

The industry faces significant regulatory hurdles that impact rocket engine market growth and innovation. Strict environmental standards, such as limits on toxic emissions from solid propellants, require costly upgrades to manufacturing processes and pollution control systems. These substances, including hazardous chemicals linked to health and environmental risks, demand specialized disposal methods, driving up operational expenses. Additionally, arms transfer regulations restrict the global exchange of propulsion technologies, limiting market access for defense-focused manufacturers.

Rocket Engine Market Trends

Advancement in Rocket Engine Design and Manufacturing is the Latest Trend

There is a rise in constant advancements in engine technologies for launching rockets. These innovations drive increased efficiency, reliability, and performance, which creates new opportunities for space exploration and consequently stimulates the growth of the rocket engine industry. There is continuous development in combustion technology to improve the performance and reusability of engines. Moreover, space agencies are increasingly focusing on improving various parameters of engines, such as thrust, impulse to enhance the overall performance of the engine. For instance, in 2024, ISRO (Indian Space Research Organization) developed a lightweight Carbon-Carbon (C-C) nozzle for engines, enhancing thrust, specific impulse, and thrust-to-weight ratios, which will boost launch vehicle payload capacity. The Vikram Sarabhai Space Centre (VSSC) created the nozzle using advanced materials and processes, including an anti-oxidation coating of silicon carbide to withstand extreme conditions.

In addition, the application of additive manufacturing techniques is transforming engine design and production. Additive manufacturing enables the creation of intricate engine parts with improved precision and effectiveness. For instance, in May 2024, Rocket Lab completed the development of the Archimedes engine using additive manufacturing to create a reusable, high-performance engine for its Neutron rocket. This aims to lower launch costs and increase payload capacity, driving growth in the engine and space launch markets.

Download Free sample to learn more about this report.

Segmentation Analysis

By Propulsion Type

Chemical Segment Held Largest Market Share Due to High Thrust-to-Weight Ratio

On the basis of propulsion type, the market is classified into chemical, electric, and nuclear.

The chemical segment is anticipated to hold the largest rocket engine market with a share of 92.82% in 2026. Chemical engines generate thrust by expelling hot gases produced from the chemical reaction of a fuel and an oxidizer, collectively known as the propellant. Chemical engines are the most commonly used type of rocket propulsion because they provide a high thrust-to-weight ratio, making them suitable for overcoming Earth's gravity and achieving escape velocity. They are essential for launching spacecraft into orbit and for the initial stages of interplanetary missions.

The electric segment is expected to grow fastest during the forecast period owing to higher efficiency compared to chemical propulsion. Electric propulsion is a spacecraft propulsion technique that utilizes electric and/or magnetic fields to accelerate mass to high speeds. It also includes systems powered by solar arrays (solar electric propulsion). However, electric thrusters produce much weaker thrust compared to chemical rockets due to limited electric power. However, their high efficiency makes them important for use in in-space operations and missions.

To know how our report can help streamline your business, Speak to Analyst

By Chemical

Liquid Engine Segment Held Largest Share Due to its High Efficiency and Controllability

On the basis of chemical, the market is classified into liquid, solid, and hybrid.

The liquid engine segment is projected to remain and dominant component in the market with a share of 62.75% in 2026. A liquid rocket engine is a propulsion system that generates thrust by burning liquid propellants. They are increasingly used and are common in space applications due to properties such as high efficiency and controllability. The flow rate of propellants can be easily adjusted, allowing precise control of the engine’s thrust.

The hybrid engine segment is estimated to grow at the highest CAGR during the forecast period. Hybrid engines use a combination of solid fuel and liquid or gaseous oxidizer to generate thrust. The development of hybrid engine is gaining traction as there is a rise in demand for increased safety, and high performance. Hybrid rockets have a high specific impulse, with performance between solid and liquid propulsion systems.

By Stage

Multi-Stage Segment Holds Largest Market Share Due to its Provision of Improved Efficiency and Payload Capacity

On the basis of stage, the market is classified into single-stage and multi-stage.

Multi-stage segment holds the highest share of the market contributing 76.55% globally in 2026, and is expected to grow with the highest CAGR. A multi-stage rocket is a launch vehicle that uses two or more rocket stages, each with its own engines and propellant. Multi-stage rockets are used more often than single-stage rockets to reach orbital speed because they enhance efficiency, boost payload capacity, and enable rockets to achieve greater altitudes and velocities. In launching missions, each stage can be optimized for specific operating conditions, such as decreased atmospheric pressure at higher altitudes.

The single-stage segment is estimated to grow at a significant rate in the market. A single-stage rocket uses only one engine and set of propellant tanks throughout its mission. Single-stage engines are easier to build and design as compared to multi-stage engines. Rise in use of single-stage rockets used for small payloads that require only a moderate amount of thrust drives the growth of the segment in the market.

By End-User

Commercial Stage Segment Holds Largest Market Share Due to Rise in Space Exploration and Satellite Deployment

On the basis of end-user, the market is classified into commercial and government & military.

Commercial segment is anticipated to hold the highest share of 64.28% in 2026. Commercial entities in the market manufacture and supply engines and related technologies for various space-related activities such as space exploration, satellite deployment, and others. Companies such as SpaceX utilize their engines for their Falcon rockets, which provide launch services for satellites and cargo missions to the International Space Station. Rise in investment in private space missions are expected to drive the market demand.

The government & military segment is estimated to be the fastest-growing segment owing to the rise in space exploration, and satellite launches by governments of various countries. Government entities are major end users of engines. They use them for various important missions and applications. Therefore, the use of engines by government and military entities for national security, scientific exploration, and technological advancement is fueling the growth of the market.

Rocket Engine Market Regional Outlook

The market is segmented on the basis of region into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Rocket Engine Market Size, 2025, (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America currently holds the largest rocket engine market share and is likely to remain dominant throughout the forecast period.North America contributed 44.44% to the global market in 2025, with a valuation of USD 6.02 billion, and is projected to reach USD 6.57 billion in 2026. The North American market is experiencing significant growth, driven by increasing demand for aerospace launch services for human spacecraft, satellites, and missions to the International Space Station, and testing probes. The established aerospace industry in the region and huge military expenditure contribute to its dominance in the market. The region is investing heavily in space tourism, exploration, and probe missions, further fueling the expansion of the market. Moreover, the presence of leading rocket engine manufacturers in the region such as SpaceX, Sierra Space, Ursa Major Technologies, is expected to stimulate further growth of the market in the region.

The market in the U.S. is expanding due to rising defense budgets, increased satellite launches, and advancements in propulsion technologies. Government initiatives, including military modernization and NASA collaborations, drive demand for high-thrust and cost-efficient engines. Moreover, the country requires advanced engines of rockets to meet surging needs for space missions and precision munitions. The U.S. market is valued at USD 5.99 billion by 2026.

Europe

Europe accounted for USD 2.86 billion in 2025, representing 20.73% of the global market share, and is projected to reach USD 3.17 billion in 2026. The European market is poised for significant growth, driven by increased military spending and the emergence of new industry players. The market is characterized by intense competition and continuous innovation, with companies developing advanced propulsion systems and reusable rockets. European space agencies and commercial entities are heavily investing in engine research and development and diverse launch systems. For instance, in September 2024, European Space Agency (ESA) awarded a contract to Pangea Aerospace, a Spanish company specializing in propulsion systems to design a Very High Thrust engine for future European launchers. Such contracts stimulate further investment and technological advancements in the Europe market. The UK market is valued at USD 0.49 billion by 2026, and the Germany market is valued at USD 0.54 billion by 2026.

Asia Pacific

The Asia Pacific market was valued at USD 4.15 billion in 2025, capturing 29.92% of global revenue, and is estimated to reach USD 4.63 billion in 2026. The Asia Pacific market is experiencing significant growth due to space programmes and rise in investment in the space industry. The rapid growth is driven by increasing research and development activities and expanding scientific capabilities in China, India, Japan, and South Korea. Moreover, increasing rocket launches are expected to drive innovation in engine manufacturing, thus driving the market. Countries in the region are investing in development and testing of engine technology for rockets. For instance, in January 2025, China's CASC tested five engines in a single day, including a new hydrogen-oxygen engine for an upper stage, to prepare for future aerospace projects. These tests, conducted in Beijing and Laiyuan, aimed to evaluate engine performance and gather data for refinement. Such development contribute to the market growth by driving innovation, validating new engine designs, and supporting future space missions. The Japan market is valued at USD 1.00 billion by 2026, the China market is projected to valued at USD 2.32 billion by 2026, and the India market is projected to valued at USD 0.80 billion by 2026.

The rest of the world

The Rest of the World region captured 4.91% of the global market in 2025, generating USD 0.67 billion in revenue, and is projected to reach USD 0.73 billion in 2026. In the rest of the world, Latin America and the Middle East is growing at a significant pace due to the emerging space programmes and rise in investment in space technologies. Many countries in these regions are developing or expanding their national space programs. This leads to increased demand for launch capabilities and, consequently, engines of rockets. Brazil is investing in space technologies for communication, Earth observation, and scientific research.

Competitive Landscape

Key Industry Players

Key Players Focus on Development of Technologically Advanced Products and Acquisition Strategies to Drive Growth

The prominent market players are prioritizing the advancement of their product offerings. The development of a diverse range of products and rise in investment in research and development of the propulsion technologies are key factors contributing to the market dominance of these players. The market is led by several players operating in this industry. Innovative technologies and streamlined production processes are crucial for reducing manufacturing costs in the market. Therefore, by investing in advanced materials and automation, manufacturers are focused on improving rocket engine price. Engine companies in the market are actively engaging in various strategies to enhance their market presence, increase their market share, and respond to the growing demand for engines of rockets.

LIST OF KEY ROCKET ENGINE COMPANIES PROFILED

- SpaceX (U.S.)

- Blue Origin (U.S.)

- Aerojet Rocketdyne (L3Harris Technologies Company) (U.S.)

- Sierra Space (U.S.)

- ABL Space Systems (U.S.)

- Ursa Major Technologies (U.S.)

- Northrop Grumman Innovation Systems (U.S.)

- Gilmour Space Technologies (Australia)

- Ariane Group (France)

- Masten Space Systems (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Blue Origin New Glenn rocket, powered by seven BE-4 engines, successfully reached orbit, after launching from Cape Canaveral35. The mission's second stage achieved its final orbit with two burns of its BE-3U engines, deploying the Blue Ring Pathfinder.

- September 2024: Ursa Major, a U.S. rocket engine maker, secured a USD 12.5 million contract from the Pentagon to enhance its production and testing capabilities for new solid fuel engines designed for rockets.

- July 2024: Aerojet Rocketdyne, an L3Harris Technologies company finished modernizing four RS-25 engines for NASA's SLS rocket, upgrading them with advanced flight computers to withstand higher temperatures. These enhanced engines will power the Artemis IV mission in 2028, marking the debut of the SLS Block 1B configuration.

- July 2023: Sierra Space received a USD 22.6 million contract by the U.S. Department of Defense to advance the development of its VR35K-A upper-stage engine, which recently completed a successful hot fire test campaign. The VR35K-A is a liquid oxygen and liquid hydrogen engine designed to produce 35,000 lbf of thrust, utilizing advanced VORTEX technology for improved efficiency and performance.

- April 2022: Aerojet Rocketdyne received a contract from United Launch Alliance (ULA), its largest RL10 contract to date, ordering 116 RL10C-X engines for the Vulcan Centaur rocket. These engines will support ULA's contract with Amazon to launch the Kuiper satellite constellation, a project aimed at increasing global broadband access.

REPORT COVERAGE

The report provides a detailed analysis of the sector and focuses on important aspects such as key players, propulsion types, stage, end-user, and applications depending on various regions. Moreover, it offers deep insights into the rocket engine market trends, competitive landscape, market competition, and market status and highlights key industry developments. Also, it encompasses several direct and indirect factors that have contributed to the sizing of the global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 5.52% from 2026 to 2034 |

|

Segmentation

|

By Propulsion Type

|

|

By Chemical

|

|

|

By Stage

|

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 15.10 billion in 2026 and is projected to record a valuation of USD 23.21 billion by 2034.

Registering a CAGR of 5.52%, the market will exhibit significant growth during the forecast period of 2026-2034.

By propulsion type, the chemical segment led the market.

SpaceX is the leading player in the market.

North America holds the highest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 204

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us