Rubber Processing Chemicals Market Size, Share & Industry Analysis, By Product Type (Antidegradants, Accelerators, Vulcanizing Agents, and Others), By End-use (Tires, Automotive Non-Tire, Industrial Rubber Goods, and Others), and Regional Forecast, 2026-2034

RUBBER PROCESSING CHEMICALS MARKET SIZE AND FUTURE OUTLOOK

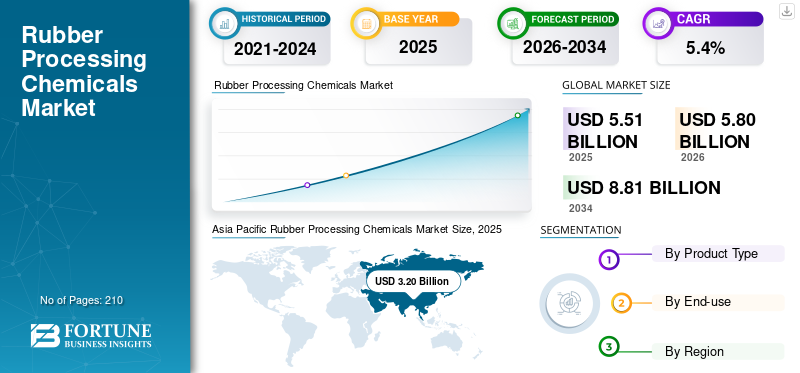

The global rubber processing chemicals market size was USD 5.51 billion in 2025. The market is projected to grow from USD 5.80 billion in 2026 to USD 8.81 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period. Asia Pacific dominated the rubber processing chemicals market with a market share of 58.07% in 2025.

Rubber processing chemicals (RPCs) are specialty additives incorporated during rubber compounding and vulcanization to enhance processability, durability, and performance characteristics of natural and synthetic rubber products. They include antidegradants, accelerators, vulcanizing agents, and processing aids that improve elasticity, aging resistance, heat stability, and curing efficiency. RPCs are essential in transforming raw rubber into high-performance materials used across tires, automotive components, and industrial rubber goods. The primary demand driver is global tire production, particularly the replacement tire market and increasing electric vehicle adoption, which require advanced rubber formulations with superior durability, lower rolling resistance, and enhanced environmental performance. LANXESS, BASF, NOCIL Limited, and Shandong Yanggu Huatai Chemical are the major players operating in the market.

Download Free sample to learn more about this report.

Rubber Processing Chemicals Market KEY TAKEAWAYS

- 2025 Market Size: USD 5.51 billion

- 2026 Market Size: USD 5.80 billion

- 2034 Forecast Market Size: USD 8.81 billion

- CAGR: 5.4% from 2026–2034

- Asia Pacific dominated the market with a 58.07% share in 2025.

- Antidegradants segment is anticipated to grow at a CAGR of 5.8%.

- Industrial rubber goods segment is anticipated to grow at a CAGR of 5.1%.

Asia Pacific

USD 3.03 billion in 2025. Strong tire manufacturing capacity across China, India, Japan, and South Korea drives regional demand.

North America

USD 1.11 billion in 2025. Replacement tire demand and a large vehicle parc support steady market growth.

Europe

20.04% market share in 2025. Premium tire manufacturing and stringent regulatory standards sustain demand.

U.S.

USD 0.73 billion in 2025. Replacement tire demand and automotive manufacturing support market growth.

Japan

USD 0.28 billion in 2025. Demand is driven by advanced tire manufacturing and automotive production.

Read More

RUBBER PROCESSING CHEMICALS MARKET TRENDS

Electric Vehicle Expansion Drives Reformulation of High-Performance Rubber Additives

The rapid rise of Electric Vehicles (EVs) is reshaping rubber compound requirements, driving demand for advanced RPC formulations. EV tires require lower rolling resistance, higher torque durability, reduced noise, and improved thermal stability, leading to increased use of high-performance antidegradants, optimized accelerators, and specialty processing aids. Additionally, sustainability pressures are accelerating the development of low-toxicity and environmentally compliant alternatives, particularly to conventional PPD-based antiozonants. Manufacturers are investing in reformulation, greener chemistry, and silica-compatible additive systems. This shift is gradually moving RPCs from commodity-driven procurement toward performance-differentiated, specification-driven demand, especially in Asia and Europe.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Global Active Vehicle Expansion Sustains Structural Tire Replacement Demand Driving Market Growth

The primary driver for rubber processing chemicals market growth is global tire production, particularly the replacement tire cycle. As the global vehicle use expands, especially in Asia Pacific, steady replacement demand ensures resilient baseline consumption of accelerators, antidegradants, and vulcanizing agents. Even during economic slowdowns, replacement tire demand provides structural stability. Growth in commercial vehicles, logistics activity, mining operations, and infrastructure spending further supports industrial tire and rubber goods production. Emerging markets such as Southeast Asia continue to add new vehicles to the road, sustaining long-term rubber chemicals consumption growth independent of short-term automotive production volatility.

MARKET RESTRAINTS

Environmental Scrutiny of 6PPD Derivatives Restrains Conventional Product Market Growth

Increasing regulatory and environmental scrutiny, particularly surrounding 6PPD and its transformation product 6PPD-quinone, poses a structural restraint on the industry. Scientific findings linking runoff from tire wear to aquatic toxicity have prompted regulatory evaluations in North America and Europe. This has introduced uncertainty around long-term demand for traditional PPD-based antiozonants, which represent a significant share of RPC volume. Reformulation costs, compliance requirements, and potential product substitution risks may pressure margins and increased R&D expenditures. While no large-scale ban exists globally, regulatory developments could disrupt established product portfolios in developed markets.

MARKET OPPORTUNITIES

Shift Toward Sustainable and Bio-Based Additives Creates Premium Growth Avenue

The transition toward sustainable materials present a meaningful opportunity for rubber processing chemicals manufacturers. Tire producers and OEMs are increasingly committing to lower carbon footprints and greener material sourcing, encouraging the development of bio-based processing oils, low-PAH additives, and environmentally safer antidegradants. Green tire technologies, silica-based tread systems, and energy-efficient curing systems require specialized additive packages. Companies investing in compliant, low-toxicity alternatives and circular-economy aligned products may capture premium pricing and long-term contracts. Emerging regulatory frameworks are also creating first-mover advantages for innovators capable of delivering performance without environmental compromise.

MARKET CHALLENGES

Feedstock Volatility and Commodity Exposure Challenge Margin Stability

Rubber processing chemicals production remains heavily dependent on petrochemical feedstocks such as benzene, aniline, sulfur, and aromatic derivatives. Volatility in crude oil, energy prices, and upstream chemical supply chains can significantly impact production costs and margins. The 2022 energy crisis highlighted the vulnerability of European producers to cost spikes, while Chinese scale advantages intensified pricing competition globally. As large portions of the market remain semi-commodity in nature, manufacturers often face limited pricing power during raw material inflation. Managing procurement risk, optimizing supply chains, and balancing regional production footprints remain ongoing strategic challenges.

SEGMENTATION ANALYSIS

By Product Type

Rising Tire Production and Cure Efficiency Optimization to Drive Accelerators Segment Growth

Based on the product type, the market is segmented into antidegradants, accelerators, vulcanizing agents, and others.

The accelerators segment is anticipated to hold the dominant market share during the forecast period. The primary driver for accelerators is the sustained growth in global tire production combined with manufacturers’ need to optimize curing efficiency. Accelerators directly influence vulcanization speed, crosslink density, and production throughput, making them essential for high-volume tire manufacturing. As tire plants pursue shorter cure cycles, improved scorch safety, and enhanced mechanical performance, particularly for radial and EV tires, demand for advanced sulfenamide and specialty accelerator systems increases. Additionally, expanding tire capacity in Asia Pacific further amplifies baseline accelerator consumption.

The key demand driver for antidegradants is the rising emphasis on durability, heat resistance, and long service life in modern tire formulations, especially for electric vehicles. EVs generate higher torque and heavier load stress, increasing the need for enhanced protection against ozone, oxidation, and thermal degradation. Antidegradants, particularly PPD-based chemistries, are critical to maintaining structural integrity under these conditions. As global vehicle use expands and performance standards tighten, tire manufacturers are increasing additive intensity, making antidegradants the fastest-growing segment.

The antidegradants segment is anticipated to rise with a CAGR of 5.8% over the forecast period.

By End-use

To know how our report can help streamline your business, Speak to Analyst

Rising Number of Vehicles on Road and Replacement Demand to Sustain Growth in Tires Segment

Based on the end-use segment, the global market includes tires, automotive non-tire, industrial rubber goods, and others.

The tires segment is anticipated to hold the dominant rubber processing chemicals market share during the forecast period. The primary driver for RPCs in the tire segment is the steady increase in the number of vehicles on the road, which supports recurring replacement tire demand. Unlike new vehicle production, replacement cycles provide stability as tires need periodic replacement regardless of economic conditions. In addition, rising electric vehicle adoption and stricter performance standards are increasing compound complexity, raising additive intensity per tire. Growth in commercial transport, logistics, and infrastructure further strengthens truck and off-the-road tire demand, reinforcing tires as the dominant RPC consumption segment globally.

Demand for RPCs in industrial rubber goods is primarily driven by infrastructure expansion, mining operations, and heavy industrial activity. Applications such as conveyor belts, industrial hoses, seals, and linings require durable rubber compounds capable of withstanding abrasion, heat, and chemical exposure. Emerging economies are increasing investments in construction and resource extraction, directly supporting industrial rubber output. As these sectors expand, consistent demand for accelerators, antidegradants, and vulcanizing agents follows, making industrial rubber goods the second-fastest growing end-use segment.

The industrial rubber goods segment is anticipated to rise with a CAGR of 5.1% over the forecast period.

RUBBER PROCESSING CHEMICALS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Rubber Processing Chemicals Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market was the largest in 2025. In Asia Pacific, demand for RPCs is primarily driven by tire manufacturing, supported by the region’s dominant position in global passenger and commercial tire production. Countries such as China, India, Japan, and South Korea continue expanding export-oriented and domestic tire capacity, sustaining strong consumption of antidegradants and accelerators. Industrial rubber goods provide secondary support, particularly in mining and infrastructure-intensive economies. Automotive non-tire components are growing alongside vehicle production, while other applications remain marginal contributors. The tire sector remains the structural anchor for market demand across the region.

Japan Rubber Processing Chemicals Market

Japan’s market reached approximately USD 0.28 billion in 2025, equivalent to around 5.1% of global sales.

China Rubber Processing Chemicals Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 1.82 billion, representing roughly 33.0% of global sales.

India Rubber Processing Chemicals Market

India’s market value reached approximately USD 0.39 billion in 2025, equivalent to around 7.1% of global sales.

North America

In North America, the replacement tire market is the dominant demand driver for RPCs. A large number of vehicles in operation ensures recurring tire replacement, supporting steady consumption of accelerators and antidegradants. Automotive non-tire components add incremental growth through OEM production and electrification-related applications. Industrial rubber goods linked to energy, logistics, and mining activity further contribute to demand. While overall growth is moderate, the resilience of replacement tire demand provides structural stability to the regional market.

U.S. Rubber Processing Chemicals Market

The U.S. market value was recorded approximately at around USD 0.73 billion in 2025, accounting for roughly 13.2% of global sales.

Europe

In Europe, tire manufacturing remains the principal driver of RPC demand, particularly in high-performance and EV-compatible tire segments. Strict durability, safety, and environmental standards increase additive intensity per tire. Automotive non-tire applications such as seals and hoses provide incremental demand, supported by advanced OEM manufacturing. Industrial rubber goods contribute modestly through construction and specialty manufacturing. While overall growth is moderate due to market maturity, premium tire production and regulatory-driven reformulation remain the core factors sustaining RPC demand in the region.

U.K. Rubber Processing Chemicals Market

U.K.’s market reached approximately USD 0.11 billion in 2025, equivalent to around 2.0% of global sales.

Germany Rubber Processing Chemicals Market

Germany’s market reached approximately USD 0.28 billion in 2025, equivalent to around 5.1% of global sales.

Latin America

In Latin America, tire production remains the primary driver of RPC demand. Mexico’s integration into North American automotive supply chains supports steady growth in tire and automotive non-tire components. Industrial rubber goods represent a meaningful secondary driver, supported by mining, agriculture, and infrastructure development across the region. While other applications remain limited in scale, expanding industrialization and transportation activity collectively reinforce long-term consumption growth.

Brazil Rubber Processing Chemicals Market

Brazil’s market size reached approximately USD 0.12 billion in 2025, equivalent to around 2.2% of global sales.

Middle East & Africa

In the Middle East & Africa, tire demand, particularly for commercial and off-the-road applications, serves as the primary driver of RPC consumption. Infrastructure development, construction, and mining activities increase demand for heavy-duty tires and industrial rubber goods such as conveyor belts and hoses. Automotive non-tire components contribute modestly where local assembly exists. While overall volumes remain smaller compared to other regions, industrial expansion and rising transportation needs are gradually strengthening regional RPC demand fundamentals.

Saudi Arabia Rubber Processing Chemicals Market

Saudi Arabia’s market value reached approximately USD 0.06 billion in 2025, equivalent to around 1.1% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Rising Capacity Expansion in Asia Intensifies Competition and Reinforce Leadership Through Scale and Integration

The global rubber processing chemicals industry is partially consolidated and highly cost-competitive, supported by strong manufacturing capabilities in Asia and integration across aniline and petrochemical value chains. Market competition is largely influenced by factors such as production scale, feedstock security, regulatory compliance, and long-term supply agreements with tire manufacturers. Chinese producers exert pricing pressure globally, while European and Japanese firms compete on specialty grades and performance differentiation. Environmental scrutiny around certain antidegradants is reshaping portfolios and increasing R&D intensity. The global key players include LANXESS, BASF, NOCIL Limited, and Shandong Yanggu Huatai Chemical, which collectively prompting global producers in supply dynamics and pricing benchmarks.

LIST OF KEY RUBBER PROCESSING CHEMICALS COMPANIES PROFILED

- BASF (Germany)

- Akrochem Corporation (U.S.)

- Arkema (France)

- BEHN MEYER (Germany)

- Finorchem (India)

- LANXESS (Germany)

- Nocil Ltd. (India)

- PMC Group, Inc. (U.S.)

- Sumitomo Chemical Co., Ltd. (Japan)

- Shandong Yanggu Huatai Chemical Co., Ltd. (China)

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading End-uses of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Historical Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Unit | Volume (Kiloton); Value (USD Billion) |

| Growth Rate | CAGR of 5.4% during 2026-2034 |

| Segmentation | By Product Type, End-use, and Region |

| By Product Type |

|

| By End-use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 5.51 billion in 2025 and is projected to record a valuation of USD 8.81 billion by 2034.

In 2025, the market value stood at USD 3.20 billion.

Registering a CAGR of 5.4%, the market will exhibit steady growth during the forecast period.

The tires end-use segment is expected to lead this market during the forecast period.

The global active vehicle growth sustains structural tire replacement demand, driving market growth in tandem.

LANXESS, BASF, NOCIL Limited, and Shandong Yanggu Huatai Chemical are the major players operating in the market.

Asia Pacific dominated the market in terms of share in 2025.

Shift toward sustainable and bio-based additives creates premium growth avenue and is expected to drive wider adoption.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us