SATCOM on the Move Market Size, Share & Industry Analysis, By Platform (Land, Airborne, and Maritime), By Frequency Band (Ku Band, Ka Band, X Band, L Band, C Band, and Others), By Component (Hardware, Software, and Services), By Application (Command & Control (C2), Intelligence, Surveillance & Reconnaissance (ISR), Situational Awareness & Navigation Support, Disaster Response, Remote Operations & Asset Monitoring, and Commercial Mobility & In-Transit Connectivity), By End User (Government & Defense, Commercial Enterprises, and Emergency Response Agencies), and Regional Forecast, 2026-2034

SATCOM on the Move Market Size and Future Outlook

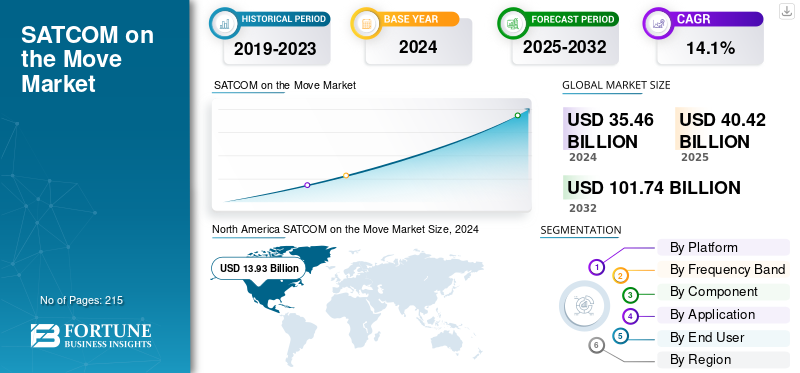

The global SATCOM on the Move market size was valued at USD 40.4 billion in 2025. The market is projected to grow from USD 46.1 billion in 2026 to USD 125.30 billion by 2034, exhibiting a CAGR of 13.30% during the forecast period. North America dominated the satcom on the move market with a market share of 39.20% in 2025.

SATCOM on the Move (SOTM) refers to satellite communication systems designed to provide continuous broadband connectivity to users and platforms in motion such as aircraft, naval vessels, ground vehicles, and unmanned systems. These systems integrate advanced antennas, modems, and tracking mechanisms that maintain stable links with satellites even during high-speed or dynamic movement across terrains and airspaces.

Government defense agencies and space regulators, including the U.S. Department of Defense (DoD), the European Space Agency (ESA), and the North Atlantic Treaty Organization (NATO), are driving the establishment of interoperability standards, frequency coordination policies, and cybersecurity frameworks for secure mobile satellite communications. These regulatory initiatives ensure resilience and operational reliability for defense and military, emergency response, and critical mission applications.

Leading industry players such as Viasat Inc., Thales Group, L3Harris Technologies, Collins Aerospace, and Honeywell Aerospace are spearheading the development of compact, high-throughput SOTM terminals and hybrid SATCOM architectures that integrate with next-generation constellations such as Starlink, OneWeb, and SES O3b mPOWER. In parallel, satellite operators including Intelsat, Eutelsat Group, and Iridium Communications are expanding mobile coverage and bandwidth capacity to support real-time command, control, and data transmission for both defense and commercial platforms. The convergence of high-capacity satellite networks with AI-driven network management and low-latency communication protocols is accelerating the evolution of SATCOM on the Move capabilities.

Download Free sample to learn more about this report.

SATCOM on the Move Market KEY TAKEAWAYS

- 2025 Market Size: USD 40.4 billion

- 2026 Market Size: USD 46.1 billion

- 2034 Forecast Market Size: USD 125.30 billion

- CAGR: 13.30% from 2026–2034

- North America dominated the SATCOM on the Move market with a 39.20% share in 2025.

- The Land segment is projected to dominate the market with a 50.08% share in 2026.

- The Hardware segment is projected to dominate the market with a 52.61% share in 2026.

North America

North America held a 39.20% market share in 2025, valued at USD 15.86 billion, and is projected to reach USD 18.06 billion in 2026.

Europe

Europe accounted for 19.80% of global revenue in 2025, reaching USD 8 billion and is projected to grow to USD 9.1 billion in 2026.

Asia Pacific

Asia Pacific contributed USD 10.3 billion in 2025, representing a 25.50% share, and is expected to reach USD 11.9 billion in 2026.

U.S.

U.S. Strong defense modernization programs and increasing adoption of mobile satellite communication systems continue to support market growth.

Japan

Japan Rising investments in advanced communication infrastructure and maritime connectivity are driving demand for SATCOM on the Move solutions.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Demand for Real-Time, Mission-Critical Connectivity to Drive Market Growth

The growing need for uninterrupted, high-speed communication across defense, emergency, and commercial mobility platforms is a major driver for SATCOM on the Move market. Armed forces, first responders, and logistics operators increasingly depend on real-time situational awareness and command capabilities that require continuous broadband connectivity even in remote or contested regions. The deployment of new low Earth orbit (LEO) constellations and high-throughput satellites (HTS) is further enabling resilient, low-latency communications, strengthening the value proposition of SOTM systems for modern operations. Moreover, there is a rise in the expansion of uninterrupted 5G connectivity for mobile platforms such as aircraft, ships, and vehicles through low-latency LEO links.

- In December 2024, ESA and Telesat achieved the world’s first direct 5G Non-Terrestrial Network (NTN) connection with a Low Earth Orbit satellite using Ka-band, demonstrating real-time mobile connectivity through space. This development enables standardized 5G access via satellites for applications such as telehealth, autonomous transport, and in-flight broadband.

MARKET RESTRAINTS:

High System Cost and Integration Complexity, Limit Widespread Adoption of SATCOM on the Move

Despite growing adoption, the high initial investment associated with SOTM terminals, advanced antennas, and satellite bandwidth remains a key restraint. The integration of these systems into diverse vehicle architectures ranging from armored ground vehicles to naval platforms and aircraft often involves extensive certification, customization, and maintenance requirements. This complexity increases total ownership costs and limits uptake, particularly among smaller defense forces and commercial fleet operators.

MARKET OPPORTUNITIES:

Expansion of Multi-Orbit and Hybrid Network Architectures to Create Growth Opportunities

The emergence of multi-orbit architectures combining LEO, MEO, and GEO satellite networks presents a major growth opportunity. These hybrid systems allow seamless switching between orbits to maintain optimal connectivity, enabling enhanced resilience and global coverage. Partnerships between satellite operators and equipment manufacturers are fostering the development of interoperable terminals capable of leveraging multiple frequency bands and network types. In addition, deployment of advanced, multi-orbit terminals that maintain robust, high-throughput communications for mobile military and defense platforms is expected to present significant opportunities.

- For instance, in October 2025, Kymeta’s Osprey u8 terminal leverages electronically steered flat-panel antennas to provide seamless multi-orbit connectivity across GEO, MEO, and LEO satellites, ensuring uninterrupted communications for mobile units. This multi-orbit approach addresses the U.S. Army’s need for flexible, resilient, and low-latency satellite links in dynamic, on-the-move environments.

SATCOM ON THE MOVE MARKET TRENDS:

Adoption of AI-Driven Network Optimization and Digital Twin Technologies is a Significant Market Trend

A key trend shaping the SATCOM on the Move landscape is the integration of artificial intelligence (AI) and digital twin technologies for autonomous network management and predictive maintenance. AI algorithms enable real-time traffic routing, adaptive beamforming, and link optimization to enhance reliability and bandwidth efficiency. Meanwhile, digital twin simulations are being used to model system performance across varying terrains and orbits, reducing downtime and improving deployment accuracy. This shift toward intelligent, self-managing communication networks marks a pivotal step in the modernization of global mobile satellite communication infrastructure.

MARKET CHALLENGES:

Cybersecurity and Signal Interference Risks to Hamper SATCOM on the Move Market Demand

As SOTM systems become more software-defined and networked, they face heightened exposure to cyberattacks and electronic warfare threats. Jamming, spoofing, and data interception can compromise mission-critical communications, making cybersecurity an operational priority. Ensuring end-to-end encryption, anti-jamming mechanisms, and secure authentication remains an ongoing challenge that requires continuous technological innovation and regulatory coordination.

Download Free sample to learn more about this report.

Segmentation Analysis

By Platform

Extensive Deployment of Land-Based Tactical Communication Systems Drives Segmental Dominance

On the basis of platform, the market is classified into land, airborne, and maritime.

The land segment accounted for the largest share of the market in 2024, driven by the extensive use of mobile satellite communication systems in defense ground vehicles, armored fleets, and command centers. Defense forces across major economies are integrating ruggedized SATCOM terminals and electronically steered antennas on vehicles to ensure uninterrupted command, control, and data exchange in dynamic operational environments. The Land segment is projecteed to dominate the market with a share of 50.08% in 2026.

- For instance, in June 2025, L3Harris Technologies secured a USD 487.3 million cost-plus-fixed contract from the U.S. Department of Defense for the modernization of enterprise terminals for mobile platforms including depot and engineering support over five years through 2030.

The maritime segment is anticipated to witness substantial growth, supported by the integration of SATCOM systems across naval fleets, commercial vessels, and offshore energy platforms. Expanding use of high-speed maritime broadband and secure naval communication networks is contributing to this growth.

- In August 2024, Orbit Communication Systems secured multiple contracts worth over USD 36 million, to supply advanced satellite communication systems for naval and airborne military platforms globally.

To know how our report can help streamline your business, Speak to Analyst

Ku-Band Holds Leading Position Owing to its Wide Coverage and Affordability

Based on frequency band, the market is segmented into L-band, C-band, Ku-band, Ka-band, X-band, and others.

The Ku-band segment captured the largest share in 2024, owing to its well-established ecosystem, wide coverage, and cost-effective bandwidth capabilities. It remains the preferred frequency for mobile connectivity across airborne, maritime, and land-based platforms.

- In March 2024, Intelsat announced the introduction of its FlexMove service portfolio to deliver enhanced Ku-band connectivity for government and enterprise mobility operations.

The Ka-band segment is expected to grow with fastest CAGR, driven by the deployment of high-throughput satellites (HTS) and low-latency multi-orbit networks. Ka-band offers higher data transfer rates and supports high bandwidth-intensive operations such as ISR and real-time C2 communication.

- In March 2025, Thales Group introduced a Ka-band multi-orbit terminal compatible with SES O3b mPOWER and Starlink, enabling seamless handover between satellite constellations and improving mobile network resilience.

By Component

Hardware Components Dominate as they Enable Connectivity across Dynamic Operational Environments

By component, the market is categorized into hardware, software, and services.

The hardware segment held the largest share in 2024, owing to the high demand for terminals, antennas, and modems that enable mobile connectivity across dynamic operational environments. The growing deployment of flat-panel, electronically steered antennas (ESA) and multi-band terminals for land, air, and maritime applications has reinforced hardware’s dominance in the SOTM ecosystem. The Hardware segment is projecteed to dominate the market with a share of 52.61% in 2026.

- In March 2025, Orbit Communication Systems Ltd. launched the MPT30Ka Deployable SATCOM System, a multi-purpose, man-portable satellite communication terminal designed for rapid field deployment, providing uninterrupted and secure connectivity for military forces in complex environments and mobile platforms.

Services is projected to be the fastest growing segment, supported by the rising preference for managed network models and satellite bandwidth leasing. Government and commercial operators are increasingly outsourcing maintenance and communication management to specialized SATCOM service providers for greater operational efficiency.

By Application

Command & Control (C2) Leads as Defense Organizations Require Secure-Real Time Communication

Based on application, the market is segmented into Command & Control (C2), Intelligence, Surveillance & Reconnaissance (ISR), situational awareness & navigation support, disaster response, remote operations & asset monitoring, and commercial mobility & in-transit connectivity. The Ku Band segment is expected to lead the market, contributing 37.15% globally in 2026.

The Command & Control (C2) segment accounted for the largest share in 2024, driven by continuous demand from defense organizations for secure, real-time communication links in mission-critical operations. SOTM systems enable high-speed data and video transfer between mobile command posts, ground vehicles, and airborne platforms.

- In December 2024, Kymeta launched a multi-band satellite antenna that simultaneously operates across both Ku- and Ka-band frequencies using a single, compact aperture, enabling four concurrent beams.

Commercial mobility & in-transit connectivity is projected to be the fastest-growing segment through 2032, supported by the expansion of satellite broadband services across aviation, logistics, and public transportation sectors. Growing passenger connectivity expectations and fleet telematics integration are fueling demand for mobile satellite broadband.

- In July 2025, Viasat announced a partnership with Maersk to equip cargo fleets with on-the-move broadband systems for real-time monitoring and global connectivity.

By End User

Defense Modernization and Expanding Commercial Mobility Services Drive End-User Adoption

On the basis of end user, the market is divided into government & defense, commercial enterprises, and emergency response agencies.

The government & defense segment dominated the market in 2024, accounting for the largest share due to ongoing military modernization programs, expansion of secure tactical networks, and adoption of multi-band terminals for field and naval operations. Defense agencies continue to invest heavily in SOTM hardware and systems for uninterrupted battlefield communication and situational awareness. The Antennas segment is projecteed to dominate the market with a share of 19.07% in 2026.

- For instance, in May 2025, U.S. Army selected Kymeta’s Osprey u8 terminal as its multi-orbit satellite communications system for the Next Generation Command and Control (NGC2) pilot program, aimed at modernizing command infrastructure to boost operational effectiveness.

The commercial enterprises segment is anticipated to witness the fastest growth over 2025–2032, propelled by rising adoption of mobile satellite connectivity for aviation, logistics, maritime transport, and energy operations. Increasing partnerships between satellite operators and mobility service providers are also expanding commercial SOTM applications.

- In August 2025, SES partnered with Hapag-Lloyd to deploy O3b mPOWER SOTM terminals across shipping fleets, enabling real-time route optimization and crew connectivity.

SATCOM on the Move Market Regional Outlook

North America

North America SATCOM on the Move Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America held 39.20% of the global market share, reaching a valuation of USD 15.86 Billion, and is projected to grow to USD 18.06 Billion in 2026. The region benefits from strong defense modernization programs, robust satellite communication infrastructure, and the presence of major industry players such as Viasat Inc., L3Harris Technologies, Collins Aerospace, and Honeywell Aerospace. The U.S. Department of Defense’s increasing investment in beyond-line-of-sight (BLOS) communication capabilities, mobile command systems, and next-generation network-centric warfare solutions continues to drive market demand.

- In February 2025, Viasat was awarded a task order to provide Ku-band low Earth orbit (LEO) satellite services for the U.S. Space Force under a USD 13 billion, 10-year IDIQ contract, supporting global government operations with managed services, network management, and technical support.

Furthermore, growing adoption of SATCOM on the move- (SOTM) systems in homeland security, disaster response, and commercial fleet connectivity applications reinforces the region’s leadership position.

Europe

The market in Europe reached USD 8 Billion in 2025, representing 19.80% of total market revenue, and is projected to reach USD 9.1 Billion in 2026. Europe is projected to witness substantial growth in the SATCOM on the Move industry, driven by defense communication modernization initiatives, transnational security cooperation, and investments in multi-orbit satellite constellations. The European Space Agency (ESA) and NATO are prioritizing resilient communication architectures capable of supporting mobile and hybrid operations across air, land, and sea domains. France, the U.K., and Germany are integrating SOTM terminals in military vehicles, naval fleets, and ISR aircraft to enhance situational awareness and coordination.

- In June 2025, Thales announced a contract with Airbus Defence & Space to supply its safety satellite communication (satcom) system, the AVIATOR 700S, for the A400M military transport aircraft.

This strong defense-driven demand, combined with growing commercial applications in maritime and logistics sectors, is expected to accelerate Europe’s market growth.

Asia Pacific

Asia Pacific contributed approximately USD 10.3 Billion to the global market in 2025, accounting for 25.50% share, and is expected to reach USD 11.9 Billion in 2026. Asia Pacific is anticipated to be the fastest-growing market during the forecast period. Rising defense budgets, cross-border security challenges, and the rapid digitalization of military and commercial communication networks are propelling adoption across China, India, Japan, South Korea, and Australia. Regional forces are increasingly investing in SOTM systems to ensure secure, real-time communication in dynamic combat and humanitarian operations. In addition, there is an increase in demand for continuous, reliable broadband connectivity in mobile environments in the transportation sector of the region.

- For instance, in 2023, Gilat Satellite Networks secured a multimillion-dollar contract to expand its SATCOM on the Move capabilities for rail networks in Asia Pacific. This contract specifically involves deploying Gilat's ER7000 electronically steered antennas to provide continuous high-speed satellite internet connectivity on trains.

In addition, the expansion of regional satellite networks and increasing collaborations with global operators are driving SATCOM on the Move market growth.

Latin America

In 2025, Latin America generated USD 4.19 Billion, contributing 5.10% to global market revenue, and is projected to grow to USD 4.66 Billion in 2026. Latin America is experiencing gradual but steady growth, supported by expanding defense modernization programs and improved satellite coverage. Brazil, Mexico, and Chile are deploying SOTM systems to strengthen border security, emergency services, and maritime communication networks. The growing role of satellite-enabled connectivity for disaster management and national security is expected to sustain demand across the region.

The Middle East & Africa

The Middle East & Africa region captured 10.40% of the global market in 2025, generating USD 2.08 Billion in revenue, and is projected to reach USD 2.33 Billion in 2026. The Middle East & Africa (MEA) region is poised for notable growth due to increasing investments in defense communication infrastructure, homeland security modernization, and smart mobility systems. The UAE, Saudi Arabia, Israel, and South Africa are actively integrating advanced SOTM systems for land and air platforms to enable real-time command and control. Ongoing defense cooperation programs, coupled with the expansion of commercial mobile satellite services for oil & gas and transport industries, are expected to drive sustained market growth in the MEA region.

COMPETITIVE LANDSCAPE

Key Industry Players:

Multi-Orbit Connectivity, Defense Modernization, and Strategic Industry Alliances Strengthen Market Leadership

The global market is driven by the rising demand for uninterrupted, high-speed connectivity for defense, commercial, and emergency response operations across land, air, and sea platforms. The increasing need for real-time situational awareness, command and control (C2) capabilities, and autonomous mission operations is accelerating the adoption of mobile satellite communication solutions. Market growth is further fueled by the integration of multi-orbit (LEO, MEO, and GEO) satellite networks, AI-enabled network management, and the expansion of 5G non-terrestrial network (NTN) capabilities that deliver resilient, low-latency communication links for users in motion.

Key players leading the global SOTM ecosystem include Viasat Inc., Thales Group, L3Harris Technologies, Collins Aerospace, Honeywell International, and Cobham Satcom. Prominent satellite operators such as SES S.A., Intelsat, Eutelsat Group, and Iridium Communications are expanding high-throughput and low-latency mobile coverage through hybrid constellations and interoperable satellite architectures. Meanwhile, emerging companies such as Kymeta, Hughes Network Systems, and Isotropic Systems are developing next-generation flat-panel antennas and software-defined terminals designed for dynamic beam steering, multi-network adaptability, and compact deployment across defense and commercial fleets.

Leading OEMs and defense integrators are investing in AI-driven resource allocation, predictive link optimization, and cyber-resilient communication frameworks to enhance operational continuity in contested or remote environments. Key players collaborate to develop secure, adaptive SOTM terminals supporting seamless transition between GEO and LEO satellites, improving tactical responsiveness and bandwidth utilization. Similarly, various companies such as L3 Harris are advancing modular SOTM solutions tailored for multi-domain operations enabling rapid integration across aircraft, ground vehicles, and naval vessels.

LIST OF KEY SATCOM ON THE MOVE COMPANIES PROFILED:

- Viasat Inc. (U.S.)

- Thales Group (France)

- L3Harris Technologies, Inc. (U.S.)

- Collins Aerospace – Raytheon Technologies (U.S.)

- Honeywell Aerospace (U.S.)

- Cobham Satcom (Denmark)

- SES S.A. (Luxembourg)

- Intelsat (U.S.)

- Eutelsat Group (France)

- Hughes Network Systems (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: OneWeb unveiled a lightweight, 9kg man-portable satellite antenna terminal designed as a backpack-sized solution to enhance the Indian Army’s tactical communications by providing high-speed, low-latency connectivity up to 195 Mbps download via its LEO satellite constellation.

- September 2025: Orbit Communication Systems unveiled the MPT30Ka Satcom On-the-Move terminal, its most compact and lightweight satellite communication system designed for military vehicles and maritime deployment, supporting multi-orbit connectivity across GEO, MEO, HEO, and LEO constellations.

- July 2025: Station Satcom partnered with Eutelsat to integrate OneWeb’s Low Earth Orbit (LEO) satellite services into its maritime connectivity portfolio, providing hybrid satellite connectivity across global oceans.

- July 2024: France defence procurement agency ordered 30 ground-based Syracuse IV SATCOM terminals from Thales for the French Army’s several armored vehicles under the Neptune contract awarded July 2024, expanding tactical communication nodes for battlefield connectivity.

- May 2024: Airbus demonstrated low-latency satellite communications using OneWeb’s LEO constellation on a moving vehicle in Finland, showing reliable connectivity for professional and government users in remote areas where traditional networks fall short.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.30% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Platform

By Frequency Band

By Component

By Application

By End User

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 40.4 billion in 2025 and is projected to reach USD 125.30 billion by 2034.

In 2025, the market value stood at USD 15.86 billion.

The market is growing at a CAGR of 13.30% during the forecast period of 2026-2034.

The land segment led the market by platform.

Factors such as rising demand for real-time, mission-critical connectivity are market drivers of the market.

Viasat Inc. (U.S.), Thales Group (France), L3Harris Technologies, Inc. (U.S.), and others are some of the prominent players in the market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 215

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us