Satellite Attitude and Orbit Control System Market Size, Share & Industry Analysis, By Satellite Type (Small Satellite and Medium & Heavy Satellite), By Solution (Hardware and Software), By Hardware (Sensors, Actuators, GPS Receiver, Star Tracker Assembly, and Others), By Orbit Type (LEO, GEO, and MEO), By Application (Commercial, Government & Civil, and Defense), and Regional Forecast, 2026-2034

Satellite Attitude and Orbit Control System Market Size

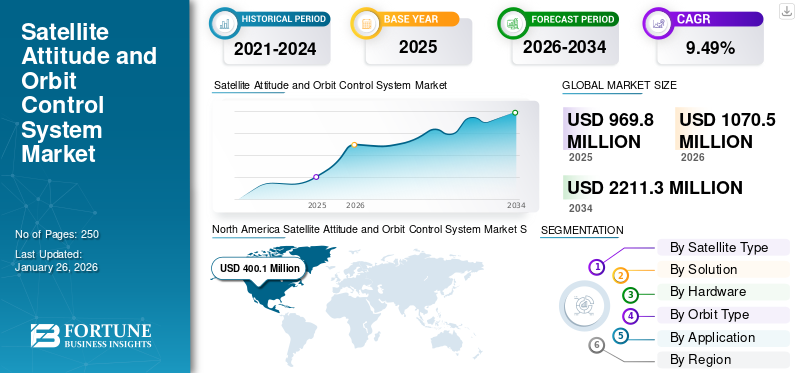

The global satellite attitude and orbit control system market size was valued at USD 969.8 million in 2025 and is projected to grow from USD 1070.5 million in 2026 to USD 2211.3 million by 2034, exhibiting a CAGR of 9.49% during the forecast period. North America dominated the satellite attitude and orbit control system market with a market share of 41.25% in 2025.

Satellite Attitude and Orbit Control Systems (AOCS) are critical components that ensure satellites maintain their desired orientation (attitude) and trajectory (orbit) in space. These systems are essential for various applications, including Earth observation, communication, and scientific exploration. A typical AOCS comprises several key components such as sensors, actuators, control algorithms, algorithms, software, and computers. Attitude control refers to the orientation of the satellite to a reference frame, which is crucial for tasks such as accurately pointing antennas or cameras toward Earth or other celestial bodies. Orbit control involves managing the satellite's path around Earth, ensuring it remains in its designated orbit despite gravitational perturbations from celestial bodies.

The global satellite attitude and orbit control systems (AOCS) market is rapidly evolving, driven by advancements in technology and increasing demand for satellite-based services. AOCS market is characterized by strong competition among key players who are continuously innovating to meet the demands of an expanding satellite industry. Recent developments indicate a robust pipeline of projects aimed at enhancing satellite capabilities through advanced attitude and orbit control technologies. For instance, in April 2023, Space logistics and orbital transportation company D-Orbit has launched Guardian, the 10th commercial mission of its proprietary orbital transport vehicle (OTV), the ION Satellite Carrier (ION). The satellite will test the onboard attitude and orbit control system and the Visiona onboard data handling software (OBDH), which are critical to managing satellite operations.

Download Free sample to learn more about this report.

Global Satellite Attitude and Orbit Control System Market Overview

Market Size & Forecast

- 2025 Market Size: USD 969.8 million

- 2026 Market Size: USD 1070.5 million

- 2034 Forecast Market Size: USD 2211.3 million

- CAGR: 9.49% from 2026–2034

Market Share

- North America led the market with 41.25% share in 2025. Growth is driven by advanced satellite manufacturing infrastructure, high government spending by NASA and the U.S. Department of Defense, and significant private sector activity from companies like SpaceX and Northrop Grumman.

- Hardware segment held the largest market share, supported by the integration of AI-driven sensors, actuators, and star tracker assemblies that enhance satellite autonomy and mission success rates.

Key Country Highlights

- United States: Major driver due to NASA’s Artemis and Commercial Lunar Payload Services (CLPS) programs, alongside Department of Defense investments in next-generation satellite navigation and surveillance systems.

- France: Home to the European Space Agency (ESA) and Thales Group, focusing on sustainable satellite missions and electric propulsion technology development.

- China: Rapid growth fueled by large-scale LEO constellation projects and government-backed programs like BeiDou Navigation Satellite System, boosting demand for advanced AOCS hardware.

- India: ISRO’s continuous launches under programs like Gaganyaan and PSLV missions, focusing on cost-efficient satellites and indigenous AOCS solutions aligned with Make in India initiatives.

Market Drivers

Adoption of AI for Autonomous Operations to Catalyze Global Satellite Attitude and Orbit Control System Market Growth

Satellite AOCS enables precise control of a satellite's orientation in space, which is essential for a variety of applications including communications, Earth observation, and scientific research. This precision allows equipment such as cameras and antennas to be accurately aligned with targets, optimizing data collection and communication efficiency. Additionally, the system ensures the satellite's attitude stability despite external disturbances such as gravity and solar radiation pressure, which is essential for long-duration missions that require consistent performance over long periods of time.

Moreover, satellite attitude and orbit control system significantly improves the quality of data collected from space by ensuring accurate pointing of sensors and instruments. This is particularly important for Earth observation satellites, which on high-resolution imagery for environmental monitoring and disaster management. Modern AOCS systems often include artificial intelligence-based algorithms that enable autonomous decision-making and adjustments. This reduces the need for constant ground control intervention, allowing for more efficient operations and faster responses to changing on-orbit conditions.

Satellite attitude and orbit control system play a vital role in improving satellite performance for a variety of applications. Their ability to provide precise control, stability, and autonomous operation has made them essential in modern satellite technology. As the demand for satellite services continues to grow, improvements to AOCS will further improve operational efficiency and mission success, driving the global satellite attitude and orbit control system market growth during the forecast period.

Market Restraints

Huge Investment and Complexity of Satellite Launch Mission Could Hamper the Market Growth

Developing advanced AOCS technology requires significant investment in research, development, and testing. The high costs associated with creating reliable and accurate systems can deter small and medium-sized companies from entering the market, limiting competition and innovation.

Additionally, the increasing complexity of satellite missions requires advanced AOCS solutions integrating various technologies including sensors, actuators, and control algorithms. This complexity can prolong development timelines and increase the risk of failure during operation, discouraging investment in the sector.

The space industry is subject to strict government regulations regarding safety, environmental impact, and operational standards. Compliance with these regulations is time-consuming and costly, which can delay projects and increase overall expenses for AOCS developers.

Furthermore, growing awareness of environmental issues has led to increased attention to space activities, including the potential creation of space debris resulting from satellite operations. Companies are addressing these issues through sustainable practices, which may require additional investment in research and development. The aerospace sector faces a demand for highly skilled engineers and technicians, but this demand often outstrips supply. The resulting talent shortage can stifle innovation, delay project timelines, and hamper market growth.

Market Opportunities

Real-Time Data Analysis and Autonomous capabilities to Amplify Product Demand

AI algorithms can analyze huge amounts of sensor data in real time, enabling more precise calculations for attitude adjustments and orbital maneuvers. This precision is critical for tasks such as precisely pointing cameras and antennas, allowing satellites to collect high-quality data and maintain efficient communications links. AI-based control systems operate autonomously, making real-time decisions based on the satellite’s current condition and mission objectives. This reduces the need for continuous human intervention from ground control and allows faster responses to changing conditions in space. Autonomous operations also improve the satellite's ability to handle unexpected situations, such as system failures or environmental anomalies.

AI algorithms can predict future actions and conditions by analyzing historical data, allowing potential problems can be predicted before they occur. For instance, predictive analysts can help identify risks of structural failures or fragmentations in space, enhancing safety and sustainability of the mission. AI-based systems continuously monitor the health of various subsystems and can identify anomalies or malfunctions more rapidly than traditional methods. If a fault is detected, the AI autonomously initiates recovery protocols to ensure the satellite continues to operate without waiting for instructions from ground control.

For instance, in November 2024, AI-based technologies are poised to unlock true autonomy in orbit, potentially allowing spacecraft to operate independently and send more personalized, intelligently controlled data back to Earth. In October 2024, Canadian software startup Mission Control recently announced plans to test long-term autonomy for spacecraft in partnership with Spire, which would provide small satellites for missions lasting at least one year to evaluate machine learning (ML) capabilities.

SATELLITE ATTITUDE AND ORBIT CONTROL SYSTEM MARKET TRENDS

Integration of Electric Propulsion Systems in Satellite Attitude and Orbit Control System to Enhance Operational Efficiency and Effectiveness

Electric propulsion systems provide high specific impulse, enabling more efficient fuel usage. This efficiency translates into greater satellite maneuverability, allowing precise attitude adjustments and orbital maneuvers with reduced fuel consumption. As a result, satellites can maintain an optimal position for a long time, thereby enhancing mission capabilities and lifespan.

Moreover, electric propulsion systems often require less fuel than traditional chemical propulsion systems due to their higher efficiency. This reduction in required propellant mass allows lighter satellite designs, leading to reduced launch costs and increased payload capacity. By optimizing satellite attitude and orbit control system with electric propulsion, satellites can achieve their operational objectives without the excessive weight of fuel systems.

Furthermore, the efficiency of electric propulsion systems allows satellites to operate for extended periods without rapidly depleting their fuel supplies. This capability is particularly useful for long-duration missions where maintaining attitude and orbit for extended periods is important, such as missions in geostationary orbit or deep space exploration. Electric propulsion systems can be integrated with on-board power systems (such as solar panels) to optimize energy consumption.

By managing energy more efficiently, these systems ensure sufficient power for propulsion and satellite attitude and orbit control system functions, improving overall system performance. For example, during high demand for maneuvers, the system can effectively balance the distribution of energy between propulsion and other satellite operations.

- North America witnessed satellite attitude and orbit control system market growth from USD 311.9 Million in 2023 to USD 368.8 Million in 2024.

For instance, in September 2021, Satellite propulsion provider Aliena PTE Ltd (Aliena) signed an agreement with Orbital Astronautics Ltd (OrbAstro), a satellite and on-orbit services provider, to launch the AOCS AA multi-module all-electric propulsion system onboard the OrbAstro ORB-12 (a 12U class satellite). Aliena developed the multi-module Attitude and Orbital Control System (AOCS) in collaboration with Finnish partner Aurora Propulsion Technologies. The distribution of the general internal architecture for fuel, electronic control and fluids, the movements segment will include a compact and efficient motor designed by Aurora, enhancing the propulsion and control capabilities of the satellite.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Satellite Type

Increasing Launches of Small Satellites Due to Cost Advantages to Catalyze Segmental Growth

By satellite type, the market is divided into small satellite and medium & heavy satellite.

The small satellite is estimated to be the fastest-growing segment during the forecast period from 2025-2032. The segment is experiencing significant growth, driven by the cost advantages small satellites offer, including lower manufacturing, launch, and operational costs. These benefits make them accessible for a wider range of applications, from commercial to scientific research. This cost efficiency is particularly appealing to startups and smaller organizations looking to enter the space market without significant financial burdens.

In addition, there is an increasing demand for real-time Earth observation data across various sectors such as agriculture, disaster management, urban planning, and climate monitoring. Small satellites are well-suited for these applications due to their ability to deploy in constellations that provide frequent, high-resolution imaging capabilities.

The medium & heavy satellite segment will capture 54.76% of the market share in 2026.

By Solution

Hardware Segment to Display Fastest CAGR due to Integration of Artificial Intelligence for Enhanced Autonomy

By solution, the market is divided into hardware and software.

The hardware segment is estimated to expand at the fastest CAGR during the forecast period from 2025-2032 and held the largest market share in 2024. Recent developments in AOCS hardware reflect significant advancements aimed at enhancing performance, reliability, and efficiency. In addition, the integration of artificial intelligence (AI) into AOCS is revolutionizing the way these systems operate. AI-driven algorithms enhance autonomous decision-making capabilities, allowing satellites to perform complex maneuvers without ground intervention. This segment is expected to dominate the market with a share of 77.03% in 2026.

Furthermore, there is a rising focus on improving sensor accuracy, enhancing onboard computing capabilities, utilizing COTS components, developing electric propulsion systems, and employing digital twin technologies for better design validation. These innovations collectively contribute to more efficient, reliable, and cost-effective satellite operations across various applications in the expanding space industry.

The software segment is anticipated to grow with a CAGR of 9.11% during the forecast period (2025-2032).

By Hardware

Significant Innovations and Adoption of Technological Advance Sensors Catalyze the Segmental Growth

By hardware, the market is divided into sensors, actuators, GPS receiver, star tracker assembly, and others.

The sensor segment is estimated to expand at the fastest CAGR during the forecast period. Recent advancements in AOCS hardware, particularly in sensor technologies, have significantly contributed to the growth of this segment. Sensor technologies such as sun sensors, gyroscopes, magnetometers, and others, are pivotal to the growth of the satellite industry. Innovations in sensors enhance the precision, reliability, and efficiency of satellite operations while reducing costs through the use of COTS components. In 2026, the GPS receiversegment is projected to lead the market with a 25.7% share.

By Orbit Type

LEO Segment Held the Dominant Share due to Expansion of Satellite Networks

By orbit type, the market is divided into LEO, GEO, and MEO.

The Low Earth Orbit (LEO) segment is estimated to expand at the fastest CAGR during the forecast period and is expected to account for the largest market share of 73.98% in 2026. The benefits of reduced latency, availability, flexibility, increased productivity, reduced costs, wide coverage, continued technological advancements, and improved service delivery are driving the growth of low Earth orbit satellite launches. In addition, major players such as SpaceX and OneWeb are leading the development of low Earth orbit satellite networks designed to provide internet services worldwide, demonstrating the significant market interest in the commercial sector. For instance, in December 2023, SpaceX launched 23 Starlink v2 mini-satellites into low Earth orbit. The segment is expected to gain 76% of the market share in 2025.

The GEO segment is poised to attain 10.41% of the market share in 2025.

To know how our report can help streamline your business, Speak to Analyst

By Application

Deployment of Commercial Satellite Are Growing within the Commercial Space Sector to Aid the Segmental Growth

By application, the market is divided into commercial, government & civil, and defense.

The commercial segment is estimated to be the fastest growing during the forecast period of 2025-2032. The market has grown significantly due to the growth of small satellites, including CubeSats and nanosatellites. These small platforms are increasingly being used in commercial applications such as communications, remote sensing, and data collection. The demand for high-precision control systems in these small satellites is driving the need for advanced AOCS solutions. Commercial applications of AOCS span multiple sectors such as telecommunications, earth observation, scientific research, and navigation, driving an increasing demand for satellite services and significant investments from both public and private sectors. This segment is expected to hold the largest share of 72% in 2025.

The defense segment is anticipated to record a substantial CAGR of 10.13% during the forecast period (2025-2032).

SMALL ATTITUDE AND ORBIT CONTROL SYSTEM MARKET REGIONAL OUTLOOK

Based on region, the market is analyzed across North America, Europe, Asia Pacific, and the Rest of the world.

Europe

In 2025, Europe held 27.77% of the global market, reaching a valuation of USD 269.3 million, and is projected to grow to USD 300.9 million in 2026. The Europe region is estimated to be the fastest-growing during the forecast period. ESA is actively investing in space technologies and forming partnerships with commercial organizations to enhance European capabilities in space. This support is crucial for the development of a reliable space ecosystem. The U.K. market is foreseen to grow with a value of USD 76 million in 2026. Additionally, through government support, private sector collaboration, and large funding programs, Europe is prioritizing sustainability and cost-effectiveness, and investment in space exploration. Europe is also working to expand its satellite manufacturing capabilities to meet the growing demand for the product. As these efforts progress, Europe is poised to become a significant participant in the global growth of the market. Germany is estimated to be valued at USD 33 million in 2026, while France is poised to stand at USD 0.14 million in 2025.

North America

North America Satellite Attitude and Orbit Control System Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 400.1 million in 2025, capturing 41.25% of global revenue, and is estimated to reach USD 440.3 million in 2026. The growth is driven by advancements in satellite technology and increasing demand for satellite services across various sectors. In addition, significant investments from government agencies, including NASA and the Department of Defense, are fostering innovation within the AOCS sector. These investments promote research and development of new technologies that can meet the evolving need of satellite operations. The U.S. market is poised to reach a market value of USD 351.2 million in 2026.

Asia Pacific

The market in Asia Pacific reached USD 213.5 million in 2025, representing 22.01% of total market revenue, and is projected to reach USD 236.3 million in 2026. The Asia Pacific region is witnessing significant growth as various countries are investing heavily in expanding their space capabilities and emerging as key players in the market. The Chinese market is forecasted to grow with a valuation of USD 77.1 million in 2026. These investments are driven by increasing demand for satellite launches, technological advancements, and strategic focus on developing regional space programs, which are expected to grow significantly during the forecast period. In addition, countries like China, India, and Japan are heavily invested in space technologies as part of their wider space ambitions. India is expected to reach USD 59.3 million in 2026, while Japan is projected to be worth USD 47 million in 2025.

Rest Of The World

In 2025, Rest of the World generated USD 87 million, contributing 8.97% to global market revenue, and is projected to grow to USD 93 million in 2026. Rest of the world is expected to experience moderate growth throughout the study period due to the increased attention on developments in the space sector and the launch of ambitious space programs by countries such as Israel, Saudi Arabia, and the United Arab Emirates. Latin America is mainly focused on space services and equipment related to space activities. It is expected that the market expansion of the area will be caused by an increase in satellite contracts in Brazil, Argentina, and Colombia.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Key Players are Striving to Technology Advance Led to Significant Opportunities within the Market

The global satellite attitude and orbit control system (AOCS) market is experiencing rapid growth, driven by significant activity among key players striving to innovate and capture market share. As demand for satellite services continues to grow, particularly in commercial applications, companies that focus on product differentiation, cost-effectiveness, strategic partnerships, and technological advancements are likely to lead the way in this dynamic market. Companies such as OHB System AG, Thales Group, SENER Group, and Bradford Engineering B.V. are focusing on enhancing their product portfolio and expanding their business globally. Moreover, these companies specialize in high-precision sensors and systems for space applications.

LIST OF KEY COMPANIES PROFILED:

- AAC Clyde Space (Sweden)

- European Space Agency (France)

- Airbus (Netherlands)

- Honeywell International Inc. (U.S.)

- Leonardo S.p.A. (Italy)

- Northrop Grumman (U.S.)

- Thales (France)

- Sener Group (Spain)

- OHB System AG (Germany)

- NewSpace Systems (Pty) Ltd (South Africa)

KEY INDUSTRY DEVELOPMENTS

- November 2024: - Kratos Defense & Security Solutions Inc. announced that it has received an order worth USD 12 million to supply satellite and communications systems, facilities, and equipment. The award recognizes mission performance, maneuver planning, telemetry processing, command, orbit and attitude control, resource management, spacecraft and ground systems modeling, safety, support planning, execution, and training.

- October 2024: - Italian space logistics company D-Orbit signed a USD 131 million contract with the European Space Agency for the maintenance of spacecraft. Under the contract, D-Orbit would develop, launch, and demonstrate a vehicle capable of performing rendezvous, docking, and orientation and orbit control functions for satellites in geostationary orbit.

- September 2024: - BlackSky Technology announced a contract with HEO, an Australian startup that provides space imagery for defense, intelligence, and commercial uses. HEO's customers will request images of extraterrestrial objects through its HEO Inspect automated tasking and delivery platform. The HEO software would then determine imaging capabilities and assign tasks to BlackSky satellites via an API. Customers would receive advanced analytics reports, which include satellite orientation and location, subsystem identification, and life’s analysis.

- September 2024: - The Union Cabinet approved the creation of a partially-reusable Next Generation Launch Vehicle (NGLV), which will have three times the payload capacity of ISRO's Launch Vehicle Mark III, known as the workhorse of India’s space program. The cabinet allocated USD 824 Mn for the NGLV's development, including three test flights, necessary facilities, program management, and the launch campaign.

- March 2024: - OHB Sweden and N3O signed a partnership agreement during the IAC (International Astronautical Congress) in Milan. The agreement covers the development, assembly, validation and testing of two Atlantic Constellation VHR satellites. N3O is responsible for the development and implementation of the entire Atlantic Constellation space segment, while OHB Sweden is responsible for the basic design of the two VHR satellite platforms, the attitude and orbit control subsystems, and the provision of propulsion and support services for the N3O team.

REPORT COVERAGE

The report provides an in-depth market analysis. It comprises all major aspects, such as R&D capabilities, supply chain management, competitive landscape, market segments and optimization of the manufacturing capabilities and operating services. Moreover, the report offers insights into the global satellite attitude and orbit control system market trends, growth analysis, and size and highlights key industry developments. In addition to the above-mentioned factors, it mainly focuses on several factors that have contributed to the growth of the global market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.49% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Satellite Type

By Hardware

By Orbit Type · LEO · GEO · MEO By Application · Commercial · Government & Civil · Defense By Region North America (By Satellite Type, By Solution, By Hardware, By Orbit Type, By Application, and By Country) o U.S. (By Application) o Canada (By Application) · Europe (By Satellite Type, By Solution, By Hardware, By Orbit Type, By Application, and By Country) o U.K. (By Application) o Germany (By Application) o France (By Application) o Luxemburg (By Application) o Russia (By Application) o Rest of Europe (By Application) · Asia Pacific (By Satellite Type, By Solution, By Hardware, By Orbit Type, By Application, and By Country) o China (By Application) o India (By Application) o Japan (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Rest of the World (By Satellite Type, By Solution, By Hardware, By Orbit Type, By Application, and By Country) o Middle East & Africa (By Application) o Latin America (By Application) |

Frequently Asked Questions

As per a study by Fortune Business Insights, the market size was valued at USD 969.8 Million in 2025.

The market is likely to grow at a CAGR of 9.49% over the forecast period.

As per orbit type, the LEO segment lead the market in 2025.

The market size in North America stood at USD 400.1 million in 2025.

Ensuring primary operations of satellite for the mission successful rates to catalyze the market growth.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us