The Japan market is projected to reach USD 0.12 billion by 2026, the China market is projected to reach USD 0.24 billion by 2026, and the India market is projected to reach USD 0.10 billion by 2026.

Satellite IoT Market Size, Share & Industry Analysis, By Connectivity Mode (Direct-to-Device and Satellite Backhaul), By Orbit (LEO, MEO, & GEO), By Frequency Band (L-Band, S-Band, Ku-Band/Ka-Band, & Others), By Application (Transportation & Logistics, Maritime & Fisheries, Energy & Utilities, Agriculture, Government & Public Safety), By Organization Size (Small Enterprises, Medium Enterprises, & Large Enterprises), By System (Hardware (Terminals & Trackers, Modules & Chipsets, Gateways & Backhaul Units, and Antennas & Other Accessories), Software, & Services)), & Regional Forecast, 2026-2034

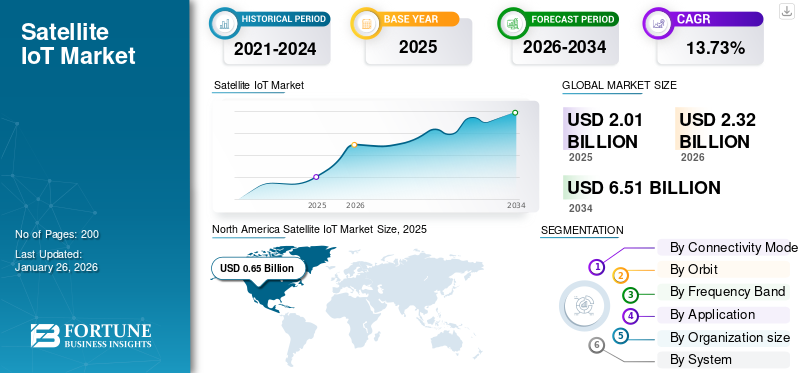

Satellite IoT Market Size

The global satellite IoT market size was valued at USD 2.01 billion in 2025 and is projected to grow from USD 2.32 billion in 2026 to USD 6.51 billion by 2034, exhibiting a CAGR of 13.73% during the forecast period. North America dominated the satellite IoT market with a market share of 32.21% in 2025.

Satellite IoT refers to the ecosystem of devices, connectivity services, platforms, and applications that enable machine-to-machine (M2M) and sensor communications via satellite networks. It uses non-terrestrial networks (NTN) operating through Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Geostationary Orbit (GEO) satellites to provide global and continuous coverage. Such types of solutions are deployed in remote, rural, offshore, or mobile environments where terrestrial connectivity is unavailable, unreliable, or cost-prohibitive.

The major government and regulatory bodies such as the Federal Communications Commission (FCC), the European Space Agency (ESA), and the International Telecommunication Union (ITU) are responsible for spectrum allocation, satellite licensing, and operational frameworks in the market. Moreover, key players in the market such as Iridium Communications, Inmarsat, ORBCOMM, and Globalstar provide satellite-based IoT connectivity solutions. The companies offer such solutions to various industries, including transportation, logistics, agriculture, and energy, and others. In addition, emerging operators such as Astrocast, OQ Technology, and Hiber are expanding the ecosystem with the launch of dedicated nanosatellite constellations for making cost-effective and low-power IoT applications on a global scale.

Download Free sample to learn more about this report.

SATELLITE IOT MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 2.01 billion

- 2026 Market Size: USD 2.32 billion

- 2034 Forecast Market Size: USD 6.51 billion

- CAGR: 13.73% from 2026–2034

- North America dominated the satellite IoT market with a 32.21% share in 2025.

- The direct-to-device segment is expected to lead the market with a 68.84% share in 2026.

- The LEO segment is projected to account for 58.22% of the global market in 2026.

North America

North America: Generated USD 0.65 billion in 2025, accounting for 32.21% of global revenue, and is projected to reach USD 0.75 billion in 2026

Europe

Europe: Accounted for USD 0.58 billion in 2025 with a 28.79% market share and is expected to reach USD 0.67 billion in 2026

Asia Pacific

Asia Pacific: Reached USD 0.52 billion in 2025, representing 25.76% of the global market, and is projected to grow to USD 0.61 billion in 2026

U.S.

The market is projected to reach USD 0.62 billion by 2026

Japan

The satellite IoT market is expected to reach USD 0.12 billion by 2026

Read More

Impact of War & Geopolitical Conflict

War & geopolitical conflict has emphasized the importance of satellite and role of its IoT connectivity for global connectivity and data transmission during the compromise of terrestrial infrastructure. During war situations, fiber networks, cell towers, and microwave backhaul are often destroyed or disabled. Such destruction increases the demand for satellite-based communication.

For instance, in 2022, terrestrial networks were repeatedly disrupted by missile strikes in Mariupol and Kharkiv. Therefore, the Ukrainian government deployed Starlink terminals provided by SpaceX to restore internet and critical IoT-type services. Thus, military forces and humanitarian organizations are increasingly relying on satellite IoT-enabled sensors and trackers for logistics, fleet coordination, and battlefield situational awareness.

On the other hand, there are negative effects to the growth of the market due to the chip shortage issue created by the Russia-Ukraine war. Ukraine supplies approximately 70% of global neon gas, which is used in semiconductor lithography machines. The Russian invasion of Ukraine disrupted neon production plants in Mariupol and Odessa, which were shut down or destroyed in 2022. IoT terminals and satellite IoT modules rely on low-cost chipsets. Therefore, this has slowed down the production, increased cost, and delay in the deployment of low-cost IoT devices.

Impact of U.S. Tariff

The current U.S. tariff regime has introduced additional cost pressures and supply chain challenges for the market. Satellite IoT devices, terminals, and communication modules rely heavily on imported components such as semiconductors, RF modules, antennas, and integrated chipsets. Such components are sourced from Asian manufacturing hubs, including China, Taiwan, and Southeast Asia. The imposition of tariffs on Chinese-origin electronics and communication equipment has increased the landed cost of IoT hardware for U.S. operators and manufacturers. This has a direct impact on the economics of satellite-enabled IoT deployments. Since these terminals are generally low-ARPU devices, even modest increases in component costs can delay adoption, reduce margins, and hamper the growth of the market.

MARKET DYNAMICS

MARKET DRIVERS:

Remote Asset Monitoring in Areas Beyond Terrestrial Coverage to Propel Market Growth

A major driver which is responsible for significant growth of the satellite IoT industry is the rise in the need for remote asset monitoring in industries that operate in geographically dispersed and hard-to-reach regions. Traditional cellular and fiber networks are unable to provide coverage across deserts, oceans, forests, and remote industrial sites. Thus, there is demand for satellite based IoT for the continuous data transmission for critical assets. The IoT solutions help to improve the operational efficiency, safety, and predictive maintenance in such environments.

For instance, in July 2025, Viasat announced the launch of IoT Nano, a new low-power satellite IoT service built on ORBCOMM’s OGx technology. This service is specifically positioned to support remote industries such as agriculture, transport, utilities, mining, and environmental monitoring. Similarly, agricultural enterprises are deploying satellite based sensors to track soil conditions and irrigation where there is lack of terrestrial connectivity.

MARKET RESTRAINTS:

High Cost of Satellite IoT Hardware and Services to Restrict Market Expansion

A significant restraint for the market is the relatively high cost of hardware (terminals, sensors, and modules) and ongoing service subscriptions compared to terrestrial IoT solutions. The small and medium enterprises, especially in developing regions are unable to invest heavily for satellite terminals and the recurring connectivity fees. This limitation is expected to stop the large-scale adoption of satellite based IoT service. While costs are gradually decreasing with new LEO constellations and mass production of IoT modules, affordability remains a significant barrier to scaling.

MARKET OPPORTUNITIES:

Direct-to-Device (DtD) / Direct-to-Smartphone Connectivity to Create Lucrative Growth Opportunities

As satellite constellations mature, especially LEO satellites, there is an opportunity to bypass traditional ground infrastructure and provide direct connectivity to consumer devices without relying on intermediate terrestrial networks. This opens up new business models in underserved regions, enabling voice, SMS, and IoT data services directly via satellite.

- For instance, in March 2025, MTN (South Africa) and Lynk Global conducted Africa’s first satellite voice call using a standard smartphone via a LEO satellite link in Vryburg, South Africa.

Therefore, this threshold of commercial readiness, and that mobile operators are actively experimenting with hybrid terrestrial & non terrestrial services.

SATELLITE IOT MARKET TRENDS:

Shift toward Hybrid & Multi-Orbit Network Architectures is a Significant Market Trends

Satellite IoT providers increasingly adopt hybrid models blending LEO, MEO, and GEO systems or integrate with terrestrial networks to improve coverage, reduce latency, and enhance reliability. Instead of relying on a single orbit regime, operators are leveraging the strengths of each layer: LEO for low-latency and frequent revisit, GEO/MEO for backbone throughput or regional fill-in, and terrestrial networks for local continuity. LEO for low-latency and frequent revisit, GEO/MEO for backbone throughput or regional fill-in, and terrestrial networks for local continuity.

- For instance, in March 2025, SES announced a partnership with Lynk Global to bridge direct-to-device (D2D) satellite connectivity using its multi-orbit infrastructure

Download Free sample to learn more about this report.

MARKET CHALLENGES:

Spectrum Allocation and Regulatory Fragmentation to Hamper Market Demand

Satellite IoT operators face a major challenge in accessing and harmonizing spectrum across countries. Non-terrestrial networks (NTN) need clear spectrum rules to interoperate with terrestrial 5G/IoT systems, but national regulators often apply inconsistent licensing regimes. This slows service rollout, raises compliance costs, and deters large-scale investment, especially in emerging regions where rules are still evolving. As a result, satellite IoT operators face a patchwork of requirements that complicates compliance, increases costs, and slows the rollout of services.

Segmentation Analysis

By Connectivity Mode

Wide Establishment of Satellite Backhaul for Extending Terrestrial Network to Segmental Growth

On the basis of the segmentation of connectivity mode, the market is classified into direct-to-device, and satellite backhaul.

A connectivity mode comprises standard devices such as smartphones, wearables, or IoT sensors that connect directly to satellites without the need for dedicated ground terminals. While, the satellite backhaul is a mode where satellites provide aggregated network links to backhaul IoT and broadband traffic.

The direct-to-device segment is expected to account for the largest share of 68.84% of the satellite IoT market in 2026. The segment holds the largest share as this type of connectivity is widely used to connect remote towers, oil rigs, mining sites, and rural communities where fiber/microwave is uneconomical.

- For instance, in February 2025, SES partnered with Quvia to integrate AI-driven orchestration tools with its multi-orbit network, enabling dynamic allocation of satellite capacity to enhance customer quality of experience. This advancement strengthens the satellite backhaul segment by allowing SES to intelligently shift bandwidth to enterprise, mobility, and cloud gateways.

The direct-to-device segment will grow at a fastest rate due to its ability to enable smartphones, wearables, and IoT devices to connect directly to satellites without requiring specialized terminals. Moreover, companies investing in direct-to-device connectivity for applications such as emergency messaging, asset tracking, agriculture, and others are expected to provide growth opportunities for the segment.

- For instance, in November 2024, Viasat successfully demonstrated direct-to-device (D2D) satellite connectivity in Saudi Arabia, enabling two-way and SOS messaging on commercial Android smartphones during the “Connecting the World from the Skies” event in Riyadh.

By Orbit

Low Latency and Global Coverage Fuels Growth of LEO Segment

In terms of orbit, the market is categorized into LEO, MEO, and GEO. LEO provides low latency and low cost connectivity to large-scale IoT deployments such as asset tracking, agriculture, and direct-to-device services. GEO delivers wide-area coverage and reliable backhaul for maritime, aviation, utilities, and remote community IoT services.

The LEO segment is expected to hold the largest share of 58.22% of the market in 2026, owing to rapid deployments of large-scale constellations such as Iridium, Globalstar, Orbcomm, and Swarm (SpaceX). These constellations are optimized for small data packets and low cost connectivity. Moreover, LEO satellites provide low-latency and global coverage which has led to adoption of these satellites for applications such as logistics tracking, smart agriculture, and consumer IoT devices.

- For instance, in March 2025, GeeSpace launched 11 new LEO satellites aboard a Smart Dragon-3 rocket from Shandong. This deployment supports the company’s goal of accelerating global IoT connectivity by scaling low-cost, small satellite.

To know how our report can help streamline your business, Speak to Analyst

By Frequency Band

Resilience to Interference and Strong Adoption across Mission-Critical Applications Fuels Growth of L-Band Segment

In terms of frequency band, the market is categorized into L-band, S-band, Ku-band/Ka-band, and others. Others include X-band, UHF bands, and other specialized or niche spectrums.

In 2026, the L-band segment is expected to hold the largest share of 46.51% of the market due as it is optimized for low-data-rate, mission-critical IoT services such as vessel tracking, aircraft safety communications, remote asset monitoring, and defense applications. Moreover, the band is resilient to rain fade and atmospheric interference, making it dependable in maritime, aviation, and harsh terrain. In addition, its widespread adoption by operators such as Viasat, Inmarsat, and other key players is expected to propel the growth of the segment during the forecast period.

- For instance, in July 2025, Viasat introduced IoT Nano, a low-power satellite IoT service built on Orbcomm’s OGx technology to support faster, larger two-way messaging for remote industries including agriculture, transport, utilities, and mining. The service runs on Viasat’s L-band satellite constellation.

The S-band is expected to be the fastest growing segment due to rising demand for direct-to-device services. There is a surge in allocation of S-band by regulators for supporting mobile satellite services for connectivity between smartphones and IoT devices. In addition, companies are exploring the potential of data transmission through S-band beyond sensor readings from remote and hard-to-reach locations.

- For instance, in July 2025, OQ Technology successfully transmitted an image via its LEO satellite using the 5G NTN IoT protocol over S-band spectrum, marking the first visual data transfer of its kind. The demonstration highlights the extension of visual IoT for connectivity for sectors such as oil & gas, utilities.

By Application

High Demand for Fleet Tracking and Supply Chain Visibility Stimulate Growth of Transportation & Logistics Segment

In terms of application, the market is categorized into transportation & logistics, maritime & fisheries, energy & utilities, agriculture, government & public safety, and others.

In 2026, the transportation & logistics segment is expected hold the largest share of 37.8% of the market due to increased use of satellite enabled IoT solutions for cross-border fleet tracking, container monitoring, and supply chain visibility. Long-haul trucking routes, cross-ocean shipping containers, and rail networks require seamless global coverage to ensure compliance, safety, and operational efficiency. Moreover, logistics companies collaborate with IoT operators for IoT connectivity, particularly for asset tracking, and logistics.

- For instance, in September 2025, Europorte, Kerlink, and Kinéis partnered to launch Track Value, a new IoT tracking solution for the freight industry that combines terrestrial LoRaWAN with satellite IoT connectivity for logistics applications.

Agriculture is emerging as the fastest growing segment driven by the need for precision farming, livestock tracking, and irrigation management in remote rural areas where connectivity gaps limit digital adoption.

By Organization Size

Widespread Deployment across Shipping, Energy, and Defense Supplemented Large Enterprises Segment Growth

Based on organization size, the market is segmented into large enterprises, medium enterprises, and small enterprises.

The large enterprises segment held the dominating position in 2024. The segment is growing due to the increased IoT adoption in sectors such as shipping fleets, aviation, utilities, energy, and defense. Global shipping companies and oil & gas majors are deploying IoT terminals for fleet management, safety, and monitoring which is expected to drive segment growth.

The small enterprises segment is anticipated to be the fastest growing segment during the forecast period. With the advent of low-cost satellite IoT modules and direct-to-device (D2D) connectivity, small businesses such as farmers, fisheries, and independent transport operators are also expected to invest in satellite based IoT during the forecast period.

By System

Widespread Deployment across Shipping, Energy, and Defense Supplemented Large Enterprises Segment Growth

Based on system, the market is segmented into hardware, software, and services. The hardware segment is further classified into terminals & trackers, modules & chipsets, gateways & backhaul units, and antennas & other accessories.

The hardware segment acquired the largest market share in 2024. The factors that contribute to the segment growth are widespread deployment of terminals, asset trackers, modules, and antennas. There is a surge in development and deployment of units in sectors such as transportation & logistics, maritime, aviation, and utilities, driving demand for rugged, reliable, and low-power devices.

- For instance, in March 2024, Myriota FlexSense hardware platform was launched as a deploy-ready satellite IoT device, designed for fast installation in remote environments and enabled by Myriota’s low-power satellite connectivity.

The services segment is anticipated to be the fastest growing segment during the forecast period. Managed connectivity and analytics services are expanding rapidly as customers increasingly seek end-to-end solutions along with hardware units. Moreover, operators such as Viasat, OQ Technology, and Iridium offer bundled IoT connectivity plus analytics and cloud integration, creating recurring revenue streams.

- For instance, in July 2025, Viasat launched IoT Nano, a managed service built on ORBCOMM’s OGx technology, combining L-band connectivity with enterprise-ready management features.

Satellite IoT Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Satellite IoT Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America maintained a strong presence in the global market, reaching USD 0.65 billion in 2025, accounting for 32.21% share, and is expected to reach USD 0.75 billion in 2026. The North America region holds the largest share of the market and is projected to expand at a significant pace during the forecast period. Growth is driven by the presence of leading satellite operators and service providers (Iridium, ORBCOMM, Globalstar, and Viasat), along with well-established ground infrastructure and integration with terrestrial networks.

- For instance, in February 2025, Globalstar, a U.S.-based satellite communication company introduced a new two-way satellite IoT solution using its LEO constellation. The solution is expected to allow low-power, low-latency, and globally reliable communications for applications such as fleet tracking, asset monitoring, pipelines, vessels, disaster response, and precision farming.

The U.S. is expected to witness a strong adoption of satellite IoT across logistics, agriculture, energy, and defense, supported by favorable spectrum regulations and government contracts. Moreover, there is an increase in demand for real-time asset tracking, remote monitoring, and resilient connectivity further supports market expansion in the region. The U.S. market is projected to reach USD 0.62 billion by 2026.

Europe

In 2025, Europe generated USD 0.58 billion, contributing 28.79% to global market revenue, and is projected to grow to USD 0.67 billion in 2026. Europe is anticipated to witness significant growth in the market during the forecast period, supported by strong regulatory support, space initiatives conducted at regional level, and presence of satellite IoT operators. Countries in the region such as France, Germany, and U.K. are witnessing increased adoption of IoT via satellite, with applications across maritime, logistics, agriculture, and utilities. In addition, major operators in the region are focusing on active expansion or modernization of the satellite constellation used for IoT applications driving market growth in Europe. The UK market is projected to reach USD 0.21 billion by 2026, and the Germany market is projected to reach USD 0.13 billion by 2026.

- For instance, in June 2025, Kinéis successfully completed the deployment of its 25-satellite IoT constellation.

Such developments are expected to strengthen the region’s position in the market by enabling large-scale, low-power connectivity for remote areas across the globe.

Asia Pacific

The Asia Pacific market accounted for USD 0.52 billion in 2025, representing 25.76% of the global industry, and is expected to reach USD 0.61 billion in 2026. Asia Pacific is projected to be the fastest growing region in the industry, and the market is growing significantly due to increase in demand for connectivity through satellite IoT in various industries such as agriculture, mining, and smart city construction. These solutions are widely being adopted in these applications across countries such as China, India, Japan, and Australia. Vast rural populations and connectivity gaps make satellite IoT critical for precision farming, resource monitoring, and logistics. The region is also witnessing rapid deployment of LEO constellations and direct-to-device IoT pilots, fueling long-term growth.

- For instance, in September 2025, Geespace, a Chinese satellite firm completed the first phase of its IoT constellation with 64 satellites. This is supposed to help build near-global real-time communications for industries and vehicles, with plans to expand to 72 satellites in coming years.

Latin America

Latin America contributed 6.65% to the global market in 2025, with a valuation of USD 0.13 billion, and is projected to reach USD 0.15 billion in 2026. During the forecast period, the market in the Latin America region is growing due to its heavy reliance on agribusiness, mining, and oil & gas operations in remote areas. Countries such as Brazil, Mexico, and Argentina are key adopters, using satellite IoT for cattle tracking, crop monitoring, and energy infrastructure management. Moreover, companies form strategic collaboration for providing low-power satellite networks and IoT services for agriculture and other industries.

- For instance, in July 2025, Myriota entered into a strategic partnership with Wyld Networks to expand affordable satellite IoT connectivity across South America. This development aims to increase IoT services adoption for supporting diverse sensor integrations, starting with soil monitoring applications in Brazil, and other countries in North & South America.

Middle East & Africa

In 2025, Middle East & Africa represented USD 0.13 billion, accounting for 6.59% of the worldwide market, and is projected to grow to USD 0.15 billion in 2026. Furthermore, the Middle East & Africa region is anticipated to experience growing adoption of IoT via satellite, driven by its oil & gas, mining, and public safety sectors. These sectors especially where remote operations require constant monitoring and communication are increasingly relying on IoT solutions over satellite technology. Countries such as Saudi Arabia, UAE, South Africa, and Nigeria are investing in IoT for energy infrastructure, utilities, and disaster resilience.

COMPETITIVE LANDSCAPE

Key Industry Players:

Product Diversification, Sustainable Technologies, and Strategic Partnerships Supports Market Expansion of Key Players

The global market is driven by rising demand for real-time connectivity, asset tracking, and resilient communications in sectors such as transportation & logistics, agriculture, energy, maritime, and government. The satellite IoT market growth is further supported by the development of direct-to-device (D2D) services, 5G NTN integration, and cost-efficient low-power IoT modules, which are expanding adoption beyond traditional enterprise use cases.

Key players in this market include Iridium Communications, Globalstar, ORBCOMM, Inmarsat (Viasat), Eutelsat, Kinéis, OQ Technology, Swarm (SpaceX), and emerging operators such as AST SpaceMobile and Lynk Global. These companies contribute by offering a broad range of IoT solutions across LEO, MEO, and GEO orbits, serving applications in logistics, agriculture, utilities, defense, and environmental monitoring.

Companies are focusing on expanding satellite constellations, enhancing frequency band utilization (L-band, S-band, Ku/Ka-band), and integrating AI-driven orchestration tools to improve performance and coverage. Moreover, leading operators are investing in D2D satellite connectivity, 5G NTN standards, and hybrid satellite terrestrial solutions to align with evolving customer needs and enable seamless global IoT services.

LIST OF KEY SATELLITE IOT COMPANIES PROFILED:

- Iridium Communications (U.S.)

- Globalstar (U.S.)

- ORBCOMM (U.S.)

- Viasat (U.S.)

- Eutelsat Group (France)

- Kinéis (France)

- OQ Technology (Luxembourg)

- Swarm Technologies – SpaceX (U.S.)

- AST SpaceMobile (U.S.)

- Lynk Global (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- September 2025: Iridium partnered with Mavenir to deploy a cloud-native Converged Packet Core on AWS, enabling 3GPP-based Non-Terrestrial Network (NTN) capabilities and preparing its satellite connected for direct-to-device (D2D) services.

- September 2025, OQ Technology and Dutch telecom operator KPN signed a roaming agreement to integrate OQ’s LEO satellite network with KPN’s terrestrial and GEO infrastructure, enabling seamless global 5G IoT connectivity.

- September 2025, Blues introduced Starnote for Iridium, an accessory that integrates with its Cellular or WiFi Notecard to provide satellite IoT fallback connectivity via the Iridium network when terrestrial connections are unavailable.

- July 2025: Viasat launched IoT Nano, its next-generation satellite IoT service designed to provide low-power, two-way messaging connectivity for industries such as agriculture, transport, utilities, mining, and environmental monitoring in remote areas.

- June 2025: OQ Technology partnered with Dutch telecom operator KPN to enable roaming onto its LEO satellite constellation, extending 5G IoT connectivity to remote and hard-to-reach areas such as polar regions and maritime routes.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics, and market trends expected to drive the market in the forecast period. The market report includes porter’s five forces analysis which illustrates the potency of buyers-suppliers in the market. Satellite IoT market forecast offers information on the technological advancements, new product launches, key trends, major industry developments, and details on partnerships, mergers & acquisitions. The satellite IoT market analysis also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ARRTIBUTES | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.73% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Connectivity Mode, Orbit, Frequency Band, Application, Organization size, System, and Region |

| By Connectivity Mode |

|

| By Orbit |

|

| By Frequency Band |

|

| By Application |

|

| By Organization size |

|

| By System |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.01 billion in 2025 and is projected to reach USD 6.51 billion by 2034.

In 2025, the market value stood at USD 0.65 billion.

The market is growing at a CAGR of 13.73% during the forecast period.

The LEO segment led the market by orbit.

The key factors driving the market are growth of market are rising adoption of business jets for flexible travel & surge in demand for emergency medical services.

Iridium Communications (U.S.), Globalstar (U.S.), ORBCOMM (U.S.), and Viasat (U.S.), among others are some of the prominent players in the market.

North America dominated the market in 2025.

Seeking Comprehensive Intelligence on Different Markets?Get in Touch with Our Experts

Speak to an Expert

- 2021-2034

- 2025

- 2021-2024

- 200

Download Free Sample

Jump to Content

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Aerospace & Defense

Clients

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us