Scaffolding Market Size, Share & Industry Analysis, By Type (Supported Scaffolding, Suspended Scaffolding, and Rolling Scaffolding), By Material (Steel, Aluminum, Wood, and Others), By End User (Construction Industry, Electrical Maintenance, Ship Building, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

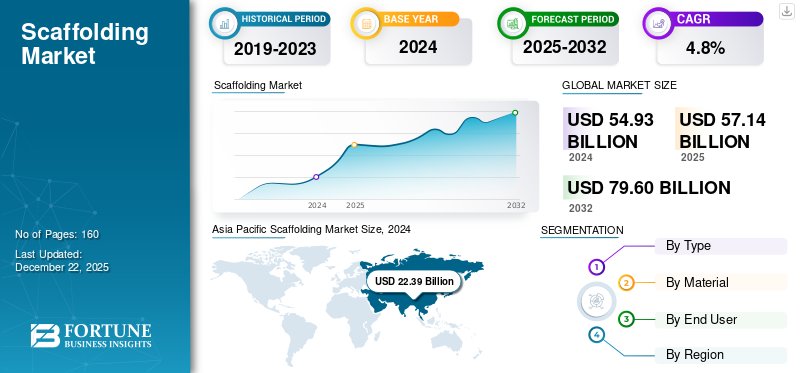

The global scaffolding market size was valued at USD 57.14 billion in 2025 and is projected to grow from USD 59.81 billion in 2026 to USD 79.6 billion by 2034, growing at a CAGR of 3.6% during the forecast period. Asia Pacific dominated the market with a share of 40.9% in 2025.

The global market includes temporary structures designed to provide critical support for workers and materials during construction, maintenance, and repair projects. In 2025, the scaffolding industry worldwide is changing due to innovation, sustainability, and safety precautions. The market is largely driven by changing construction market dynamics that rely on the implementation of smart scaffolding systems and the integration of Internet of Things (IoT) sensors and Building Information Modeling (BIM) or BIM technology for better structural monitoring of scaffolding structures and worker protection protocols. One of the main drivers in the growth of the market is the increased construction activities, particularly in developing countries, which is contributing to an increase in market share.

Major companies in the market such as Layher Holding GmbH & Co. KG, PERI, Brand Safway, and ULMA C y E, S.Coop are adapting to changing market demands by offering more intelligent temporary access solutions such as such as integrated elevated platforms and automated stair towers that enhance the capabilities of traditional scaffolding systems. For the scaffold and temporary access sector, technology is reinventing the wheel, with BIM in particular enabling clients to interact with impressive 3D models of intricate designs.

Download Free sample to learn more about this report.

Scaffolding Market Key Takeaways

- 2025 Market Size: USD 57.14 billion

- 2026 Market Size: USD 59.81 billion

- 2034 Forecast Market Size: USD 79.6 billion

- CAGR: 3.6% from 2026–2034

- Asia Pacific dominated the market with a share of 40.9% in 2025.

- Supported scaffolding is expected to hold the largest revenue market share of 59.79% in 2026.

- Steel is expected to account for a share of 52.5% in 2026.

Asia Pacific

Asia Pacific represented USD 23.38 billion, accounting for 40.90% of the worldwide market in 2025, and is projected to grow to USD 24.56 billion in 2026.

North America

North America accounted for USD 13.93 billion in 2025, representing 24.40% of the global industry, and is expected to reach USD 14.53 billion in 2026.

Europe

Europe recorded a market size of USD 11.7 billion in 2025, capturing 20.50% of the global market share, and is projected to reach USD 12.23 billion in 2026.

U.S.

The market is projected to reach USD 10.29 billion in 2026, driven by large-scale construction projects, infrastructure renewal programs, and commercial development.

Japan

The scaffolding market is expected to be valued at USD 2.58 billion in 2026, supported by ongoing infrastructure upgrades and industrial construction activities.

Read More

IMPACT OF GENERATIVE AI

AI Integration Eliminates Human Error and Enables Predictive Safety

Generative AI is transforming the market by assisting with the design process and improving safety with more structural assessments. AI-powered software can generate a number of different scaffold designs in minutes while accounting for weight distribution, material efficiency, and site conditions. This innovation is reshaping the scaffolding design sector by implementing structural modeling techniques. These automated approaches eliminate the need for extensive manual input from designers, thereby reducing concerns related to human error and accelerating design timelines. These intelligent systems integrate with Building Information Modeling technology to create detailed 3D visualizations that help identify potential structural issues before installation begins. This technology provides predictive maintenance capabilities and full safety analysis that allows engineers to model complex loading scenarios and avoid expensive failures.

IMPACT OF TARIFFS ON THE MARKET

Metals Import Duties Trigger Scaffolding Price Adjustments Across Market

Tariff policies have a measured impact on the global market, as the industry primarily serves local construction projects that remain relatively protected from international trade fluctuations. Market demand stems from regional activities, including residential construction and infrastructure development, which typically depend on established domestic supply networks. Nevertheless, tariffs imposed on essential raw materials such as steel and aluminum create moderate upward pressure on manufacturing expenses, which may influence final product pricing and operational expenditures for companies. The U.S. government's expanded tariffs on steel and aluminum imports, affecting approximately USD 150 billion worth of metal-derived products from basic hardware to heavy construction equipment, present viable cost increases that will impact both industry manufacturers and end consumers.

Scaffolding Market Trends

Surge in Digital Transformation and Smart Technologies Drive Market Evolution

Modern construction and infrastructure development have accelerated the integration of smart scaffolding systems and digitalized project management solutions. The adoption of Building Information Modeling (BIM) and advanced scaffold management software in contemporary construction projects has revolutionized site planning, real-time monitoring, and safety protocols, propelling innovation and driving widespread industry adoption. Construction companies are increasingly focusing on the importance of smart scaffolding technologies in reducing assembly time, minimizing material waste, and optimizing structural efficiency through precision design and automated planning systems. Digital scaffolding solutions with integrated sensors and IoT connectivity are being increasingly adopted in large-scale construction projects to enhance safety monitoring and operational efficiency, driving positive growth in the global scaffolding market share.

- For instance, in March 2025, Trimble launched Tekla Structures 2025 with enhanced AI capabilities and improved BIM collaboration features, revolutionizing structural design and scaffolding integration processes.

MARKET DYNAMICS

Market Drivers

Robust Construction Sector Expansion Fuels the Market Momentum

The continuous development in the construction industry and infrastructure investment have offered a huge demand for scaffolding systems in residential, commercial, and industrial construction works around the world. The initiation of large infrastructure programs at a government level, along with construction activities in the private sector, has greatly fast-tracked scaffolding deployment, making temporary structural support systems crucial for construction. Modern scaffolding systems with increased load-bearing capacities and modular designs are being extensively used in construction projects for supporting complex construction projects and safety compliance. Construction companies are realizing the need for advanced scaffolding solutions in programs involving multi-storey construction, facade rehabilitation, and development infrastructure towards attaining optimum project execution timelines and worker safety standards.

- For instance, in April 2025, The U.S. Department of Transportation stated that IIJA-funded infrastructure projects are addressing the national backlog of improvements for road and bridge repairs, improving safety and economic competitiveness. The IIJA provides nearly USD 500 billion for road and bridge activities in communities across the country.

Market Challenges

Raw Material Cost Volatility and Unskilled Labor Safety Risks Create Barriers to the Market Growth

The scaffolding industry confronts significant operational challenges from fluctuating raw material costs and workplace accidents caused by inadequately trained workers. Construction companies struggle with unpredictable steel and aluminum pricing that directly impacts project budgets and profit margins while simultaneously managing safety risks associated with workers who lack proper scaffolding assembly and maintenance skills. The market faces mounting pressure from tariff implementations and supply chain disruptions that create material cost uncertainties, coupled with persistent safety incidents resulting from insufficient training programs and rushed project timelines.

- For instance, in 2023, the U.S. Bureau of Labor Statistics (BLS) recorded 5,283 fatal work injuries, which translates to 3.5 fatalities per 100,000 full-time equivalent workers across all industries. In 2023, construction had the most deaths, 1,075, of any industry sector, and also had the highest number for the industry sector in 2011. Falls, slips, and trips were a factor in 39.2 percent, 421 of construction fatalities.

Market Opportunities

Green Energy Infrastructure and Smart City Development Drive Market Opportunities

The scaffolding sector is facing tremendous growth prospects with huge government investments in green energy projects and smart city infrastructure development. Construction companies are getting unprecedented access to high-paying contracts for services on wind turbine installations, solar panel mounting systems, and transmission grid upgradation projects, all of which need specialized scaffolding services. Government funding initiatives across the globe are directing billions of dollars into green energy and smart infrastructure initiatives, developing market demand for scaffolding manufacturers and service providers able to design for changing construction practices and safety standards.

- For instance, in October 2024, India's Smart Cities Mission encompasses 625 projects across various states worth USD 11.14 billion in total investment, as confirmed by the India Investment Grid government portal.

SEGMENTATION ANALYSIS

By Type

Supported Scaffolding Dominates the Market Owing to Versatility and Cost-Effectiveness

By type, the market is segmented into supported scaffolding, suspended scaffolding, and rolling scaffolding.

Supported scaffolding is expected to hold the largest revenue market share of 59.79% in 2026 and is projected to grow at the highest CAGR during the forecast period. It is versatile, cost-effective, and provides stable structural support across numerous construction applications. It is used primarily in residential construction, commercial building, and industrial infrastructure projects, in roles such as building exterior walls, interior finishing, and maintenance which require safe, reliable loading platform access capabilities.

Suspended scaffolding systems offer superior access to building facades and vertical surfaces without ground-level obstruction; they are becoming increasingly essential in urban renovation projects—their growing popularity across high-rise building maintenance, bridge inspection work, and exterior cleaning applications.

Rolling scaffolding maintains a significant market position due to its mobility advantages. Rolling scaffolding dominates applications requiring frequent repositioning due to its wheel-mounted design and operational flexibility. In warehouse operations and facility maintenance, rolling scaffolding is considered essential for accessing varying heights efficiently.

By Material

Steel Dominates the Market Owing to Durability and Superior Load Bearing Capacity

By material, the market is segmented into steel, aluminum, wood, and others. Others include fiberglass.

Steel is expected to be the dominant material in the market, accounting for a share of 52.5% in 2026 and is projected to command the highest share of revenue. This is because steel is stronger, more durable, and has superior load-bearing properties compared to any other material. Steel is also well-suited for large-scale construction, such as work on high-rise buildings, bridges, and industrial infrastructure. Steel scaffolding is capable of withstanding various environmental conditions and will be able to support heavier loads. It permits the use of larger section sizes, and the minimal risk of structural failure ensures not only worker safety but also continues supporting the structure without failure.

Aluminum accounts for the highest CAGR in the market because aluminum is lighter and resistant to corrosion and highly useful for maintenance or painting applications. Growing demand for sustainable, durable, and lightweight construction materials, particularly in developing economies, is prominently driven by stringent safety regulations. Wood, bamboo, in particular, offers a low-cost, environmentally-friendly option; it is also widely used in Asia Pacific for residential projects.

Other segments, including fiberglass, have niche applications for use, primarily due to their non-conductive properties.

By End User

To know how our report can help streamline your business, Speak to Analyst

Construction Industry Dominates the Market on account of Extensive Infrastructure Development and Safety Requirements

Based on the end user, the market is divided into the construction industry, electrical maintenance, ship building, and others. Others include event, film and television industries, etc.

The construction industry is expected to dominate the market, accounting for the highest revenue market share of 76.86% in 2026 and CAGR due to its wide use in residential, commercial, and industrial projects, such as multi-story buildings, bridges, and infrastructure development. Scaffolding provides construction workers with safe, stable work platforms at heights and allows them to effectively build exterior walls, complete interior finishing, or conduct building maintenance. It bears heavy loads, and its diverse environmental conditions make it indispensable with safety standards.

Electrical maintenance relies on non-conductive scaffolding, such as aluminum and fiberglass, for safe electrical system installation and repair. Ship building uses durable steel scaffolding to construct and repair vessels in demanding marine environments.

Others segment leverage scaffolding's versatility for temporary structures such as stages and sets in events and film production.

SCAFFOLDING MARKET REGIONAL OUTLOOK

By region, the market is divided into North America, Europe, Asia Pacific, South America, and the Middle East and Africa.

Asia Pacific dominates the market driven by rapid urbanization, extensive infrastructure development projects, and booming construction activities across emerging economies.

Asia Pacific

Asia Pacific Scaffolding Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific represented USD 23.38 billion, accounting for 40.90% of the worldwide market, and is projected to grow to USD 24.56 billion in 2026. The Asia Pacific market has the largest market share in terms of revenue and growth in the market due to factors such as rapid industrialization, massive infrastructure development projects, extensive urbanization, increasing construction activities across residential, commercial, and industrial sectors, and significant government investments in public works and transportation infrastructure. Additionally, in the Asia Pacific region, the presence of large-scale manufacturing facilities requiring industrial scaffolding solutions contributes to sustained demand and the scaffolding market growth. The Japan market is valued at USD 2.58 billion by 2026 and the India market is valued at USD 6.35 billion by 2026.

Download Free sample to learn more about this report.

China has the largest market share in the Asia Pacific in the market due to its extensive construction industry, ongoing urban development initiatives, massive infrastructure projects including railways and highways, significant industrial expansion, and government-backed construction programs such as the Belt and Road Initiative, which has generated substantial demand for scaffolding solutions across numerous mega-projects and infrastructure developments. The China market is valued at USD 11.27 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

North America

The North America market accounted for USD 13.93 billion in 2025, representing 24.40% of the global industry, and is expected to reach USD 14.53 billion in 2026. North America holds a significant share in the global market due to factors such as robust construction industry growth, extensive infrastructure modernization projects, and stringent safety regulations. These factors are driving demand for high-quality scaffolding systems and increasing renovation and maintenance activities across the aging infrastructure. The U.S. has the largest market share in North America due to its massive construction sector, ongoing infrastructure renewal programs, significant commercial and residential development projects, industrial facilities maintenance, and federal initiatives for infrastructure improvements, generating considerable demand for scaffolding solutions. The U.S. market is valued at USD 10.29 billion by 2026.

Europe

Europe recorded a market size of USD 11.7 billion in 2025, capturing 20.50% of the global market share, and is projected to reach USD 12.23 billion in 2026. The European region represents a substantial portion of the global market due to factors such as ongoing infrastructure rehabilitation projects, increasing focus on building renovations and heritage restoration, ship building activities, and significant industrial maintenance activities across manufacturing sectors. The commitment of the region to carbon neutrality by 2050 by the European Green Deal has spurred massive investments in green infrastructure, including renewable energy initiatives and building retrofitting programs, all demanding dedicated scaffolding solutions for construction sites and maintenance work. The UK market is valued at USD 2.67 billion by 2026, while the Germany market is valued at USD 2.95 billion by 2026.

Middle East and Africa

Middle East & Africa contributed 6.20% to the global market in 2025, with a valuation of USD 3.57 billion, and is projected to reach USD 3.74 billion in 2026. The Middle East and Africa market demonstrates exceptional growth potential in the global market due to factors such as massive infrastructure development initiatives, rapid urbanization across major cities, extensive oil and gas facility construction and maintenance, and significant government investments in mega-projects and economic diversification programs. The region's Vision 2030 initiatives across Gulf countries, focusing on smart cities, sustainable infrastructure, and tourism, and Africa's booming construction sector are driving the Middle East and Africa to generate substantial demand for scaffold systems.

South America

South America contributed approximately USD 4.57 billion to the global market in 2025, accounting for 8.00% share, and is expected to reach USD 4.75 billion in 2026. The South America market represents an emerging segment of the global market due to factors such as increasing infrastructure development projects, growing urbanization across major cities, and improving transportation networks and industrial facilities. South America's scaffolding market is supported by significant infrastructure projects, including Brazil's transportation network expansions and Colombia's 4G highway development program.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Strategic Investment and Product Innovation Strengthened the Key Players Market Positions

Global market key players are mainly comprised of several market participants, including scaffolding manufacturers, rental companies, and construction companies. The market is expected to witness steady growth, with key players increasing their investment in research and development to diversify their products as the market is moderately fragmented. Major players are innovating their products such as increasing load-bearing capacities and forming strategic partnerships to cater to the growing demand in developing economies.

Long List of Key Scaffolding Companies Studied (including but not limited to)

- Altrad Group (France)

- ADTO Group Xiang (China)

- Layher Holding GmbH & Co. KG (Germany)

- MJ Gerust GmbH (Germany)

- Brand Safway (U.S.)

- Peri Group (Germany)

- WACO Scaffolding and Equipment Co. (U.S.)

- Changli Xingminweiye Architecture Equipment Limited Corporation (China)

- Atlantic Pacific Equipment LLC (U.S.)

- ULMA C y E, S.Coop. (Spain)

- Wellmade Scaffold Co. Ltd. (China)

- BSL Scaffolding Ltd. (U.K.)

- Cangzhou Weisitai Scaffolding Co. Ltd. (China)

- United Rentals (U.S.)

- Uni-Span Group (Australia)

- Doka GmbH (Austria)

- Sunbelt Rentals (U.S.)

- Tianjin Gowe Industrial Co. Ltd. (China)

- Instant Upright (U.K.)

- Stepup Scaffold, LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2022: A major developer and provider of formwork and scaffolding systems, PERI Formwork Systems, Inc., has developed what would become a new industry standard for bridge construction. VPS ensures a safety and efficiency gap through a highly versatile system that is adjustable, rentable, and productive in forming bridge columns and caps.

- July 2022: Doka, a key player in formwork solutions and services to the construction industry has taken its collaboration with the well-known American scaffolding company AT-PAC to the next level by making a significant investment in the US-based firm. The two companies first teamed up in 2020 to offer comprehensive solutions for building sites, and their partnership has only grown stronger since then.

- July 2022: A Glasgow subsidiary named StepUp Scaffold UK from StepUp Scaffold Group in Memphis has completed the purchase of MP House ApS located near Copenhagen during July 2022. The company MP House stands as the dominant supplier of tools and equipment along with accessories to scaffolding operators based in Denmark.

- April 2022: Layher Holding GmbH Co KG has introduced the Allround Scaffold, a name that reflects the company and perhaps represents the pinnacle of modular scaffolding solutions. The Modular Scaffolding System is essentially the Layher Allround Scaffolding. This system is comparable to Allround Performance, as it serves multiple purposes within a single framework. No matter how complex the designs, architectural styles, or strict safety standards may be, Allround Scaffolding consistently proves to be the quicker, safer, and more economical choice.

- December 2021: Hindalco Industries Ltd., the metals arm of the Birla Group, has officially struck a deal to acquire Hydro's aluminum extrusions business in India for Rs 247 crore. The Kuppam plant operated by Hydro boasts a capacity of 15,000 tons for aluminum extrusions, along with impressive value-added features for surface treatment and fabrication. This acquisition opens up even more growth opportunities for the scaffolding industry.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, Type, Material, and End User of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.6% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Material

By End User

By Region

|

|

Companies Profiled in the Report |

Altrad Group (France), Layher Holding GmbH & Co. KG (Germany), United Rentals (U.S.), Brand Safway (U.S.), Peri Group (Germany), Atlantic Pacific Equipment LLC (U.S.), ULMA C y E, S.Coop. (Spain), Wellmade Scaffold Co. Ltd. (China), Doka GmbH (Austria), Sunbelt Rentals (U.S.), etc. |

Frequently Asked Questions

The market is projected to reach USD 79.6 billion by 2034.

In 2025, the market was valued at USD 57.14 billion.

The market is projected to grow at a CAGR of 3.6% during the forecast period.

The supported scaffolding segment leads the market.

Robust construction sector expansion fuels the market momentum are the key factor driving market growth.

Altrad Investment Authority, Brand Safway, Peri Group, ULMA C y E, S.Coop. are the top players in the market.

Asia Pacific is expected to hold the highest market share.

By end use, construction industry is expected to grow with a highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us