School Bus Market Size, Share & Industry Analysis, By Type (Type A, Type B, Type C, and Type D), By Propulsion (Diesel, Gasoline, CNG/LPG, Electric, and Hybrid), By Application (Public School, Private School, and Fleet Contractor), By Seating Capacity (Less than 30 Seats, 30–50 Seats, and Above 50 Seats), By Sales Channel (OEM and Retrofitted), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

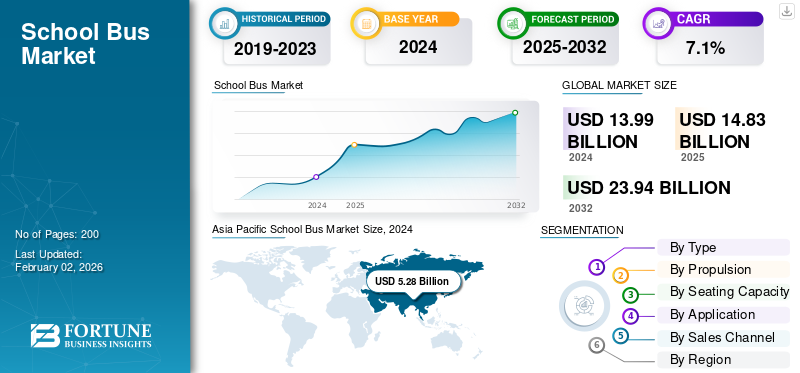

The global school bus market size was valued at USD 14.83 billion in 2025. The market is projected to grow from USD 15.77 billion in 2026 to USD 27.33 billion by 2034, exhibiting a CAGR of 7.11% during the forecast period. Asia Pacific dominated the school bus market with a market share of 38.1% in 2025.

The global market encompasses vehicles designed for safe student transportation, equipped with advanced safety, comfort, and connectivity features. Growth is driven by rising school enrollments, increasing focus on student safety, and government investments in modernizing school transportation fleets. The shift toward electric and alternative fuel buses, coupled with stricter emission norms, is accelerating fleet electrification. The integration of telematics, GPS tracking, and driver assistance systems enhances operational efficiency and improves safety monitoring. Additionally, the expansion of private education infrastructure, demand for fleet replacement, and supportive funding programs position school buses as a vital component of sustainable and smart mobility ecosystems.

Key players in the global market include Blue Bird Corporation, Thomas Built Buses, IC Bus, Tata Motors, and Yutong Bus Co., Ltd. These companies focus on developing electric and low-emission buses, integrating advanced safety systems, and adopting telematics and fleet management solutions. Strategic partnerships with governments and technology providers, along with investments in autonomous driving, energy efficiency, and smart connectivity, strengthen their presence in the evolving school transportation ecosystem.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Government Investments in Safe and Sustainable Student Transportation Drive Market Growth

Authorities across major economies are implementing policies promoting the transition from diesel to electric and CNG-powered buses for schools. These initiatives aim to reduce air pollution and protect children’s health while supporting sustainability goals. In May 2024, the U.S. Environmental Protection Agency (EPA) announced funding to support approximately 3,100 additional electric buses for students nationwide, backed by nearly USD 900 million in rebate funds under the Clean School Bus Program. These funds were aimed at aiding around 530 school districts in replacing diesel-burning buses. The programme emphasized equity, with about 67% of funding directed to underserved, low-income, rural, and tribal communities.

MARKET RESTRAINTS

High Initial Cost of Electric School Buses Restrains Market Expansion

Despite environmental and operational benefits, the high upfront cost of electric buses for schools significantly restrains market growth. Expenses related to vehicle acquisition, charging infrastructure, and battery maintenance create financial challenges, particularly for smaller districts with limited budgets. While subsidies exist, they often fail to cover the full transition cost, delaying widespread adoption.

- In November 2023, a report from the Canadian Electric School Bus Alliance (CESBA) noted that electric school buses cost up to 2.5 times as much as their diesel counterparts in Canada, presenting a major adoption barrier.

MARKET OPPORTUNITIES

Electrification and Digital Integration Offer Lucrative Market Opportunities

The global shift toward electric mobility and connected fleet technologies in electric school buses offer significant opportunities for student transport vehicle manufacturers and operators. Integrating electric propulsion systems with telematics, AI-driven diagnostics, and remote monitoring improves efficiency, safety, and sustainability. These innovations reduce the total cost of ownership while enabling predictive maintenance and real time performance tracking.

- In January 2024, the Los Angeles Unified School District placed a record order of 180 battery-electric student buses from Blue Bird Corporation, 150 of the All American model and 30 of the Vision model, marking the largest EV-school-bus contract in the company’s history.

School Bus Market Trends

Adoption of Telematics and ADAS Technologies Emerging as a Key Trend

The integration of telematics, advanced driver-assistance systems (ADAS), and GPS tracking has become a defining feature of market trends. These technologies enhance students safety, enable predictive maintenance, and improve operational efficiency by offering real-time fleet visibility. Operators can monitor driver behavior, optimize routes, and respond swiftly to emergencies.

- In July 2023, IC Bus introduced its latest CE Series school bus featuring factory-installed collision mitigation, lane departure warning, and remote telematics diagnostics, demonstrating the growing emphasis on intelligent, connected, and safety-focused school transportation solutions across developed and emerging markets.

MARKET CHALLENGES

Limited Charging Infrastructure Challenges Electric Fleet Deployment

Many regions, particularly suburban and rural districts, lack the electrical grid capacity and public charging networks necessary to support daily operations of electric buses. This restricts route planning and increases operational downtime. In April 2024, the California Energy Commission highlighted multiple cases of delayed electric buses for school deployments due to limited charging facilities and grid capacity constraints, emphasizing that infrastructure development remains a critical bottleneck in achieving widespread zero-emission school bus adoption.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Operational Flexibility and Safety Advancements Strengthen Type C School Bus Leadership

The type segment covers type A, type B, type C, and type D.

Type C academic transit buses hold the dominant share of the global market due to their balanced seating capacity, strong advanced safety features, and suitability for both urban and rural routes. They are widely adopted by school districts for daily operations, offering optimal cost-efficiency and flexibility in fleet deployment. The type C segment will account for 68.04% market share in 2026.

Type D school bus types are witnessing the fastest school bus market growth due to their high-capacity, electric-powered configurations ideal for large districts and urban fleets. In October 2024, Thomas Built Buses showcased its customer-driven approach to developing its Type D electric school bus, designed for high-capacity routes and superior performance. The new model integrates advanced battery technology, enhanced driver ergonomics, and customizable configurations based on district feedback, reflecting Thomas Built’s commitment to innovation, reliability, and zero-emission student transportation solutions.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion

Established Infrastructure and Reliability Uphold Diesel School Bus Supremacy

In terms of propulsion, the market is categorized into diesel, gasoline, CNG/LPG, electric, and hybrid.

The Diesel segment is expected to lead the market, contributing 43.69% globally in 2026. Diesel student transport vehicles currently dominate the global market due to their established infrastructure, proven reliability, and lower upfront costs compared to electric and alternative fuel models. Despite growing environmental sustainability concerns, many school districts, especially in developing regions, continue to rely on diesel fleets for affordability and maintenance simplicity. In January 2025, Ashok Leyland introduced the upgraded Sunshine school bus, powered by a 1.5-liter i-Gen6 diesel engine delivering improved fuel efficiency and lower emissions. The model also features enhanced safety systems, including fire detection, anti-roll bars, and child check alerts, alongside telematics integration, reflecting the company’s focus on performance, safety, and compliance with updated Indian emission norms.

Electric school buses are the fastest-growing segment in propulsion, driven by emission reduction goals, government incentives, and declining battery costs.

By Seating Capacity

Versatile Design and Route Efficiency Reinforce 30–50 Seat Bus Market Lead

By seating capacity, the market is bifurcated into Less than 30 seats, 30–50 seats, and above 50 seats.

The 30–50 seats segment dominate the market owing to their versatility, optimal size for both urban and suburban routes, and balanced operating economics. The 30–50 seats segment will account for 51.88% market share in 2026. These mid-sized buses are widely preferred by public and private schools as they provide efficient student transport while maintaining manageable fuel and maintenance costs. This drives the segmental growth in the school bus market forecast period.

Large-capacity buses above 50 seats are the fastest-growing segment, driven by rising student populations and fleet electrification in densely populated areas. In January 2024, Blue Bird received a record order for 180 high-capacity electric buses from the Los Angeles Unified School District, underscoring this growth trend.

By Application

Government Funding and Centralized Operations Cement Public School Bus Preeminence

On the basis of application, the market is segmented into public school, private school, and fleet contractors.

The public school segment will account for 50.55% market share in 2026. Public school buses dominate the global market due to extensive government-funded education systems and centralized transportation programs ensuring safe, regulated student travel. These fleets benefit from consistent budget allocations, standardization policies, and national-level safety mandates. Public institutions in countries such as the U.S., Canada, India, and U.K. maintain large bus fleets for daily commutes. In March 2024, the U.S. EPA’s Clean School Bus Program prioritized funding for public school districts, reinforcing their dominant role in fleet modernization and electrification.

Fleet contractor school bus operators are growing rapidly as schools increasingly outsource transportation for cost efficiency and operational flexibility. In April 2024, Student Transportation of America expanded contracts with multiple U.S. districts for electric bus fleet management, reflecting rising outsourcing trends.

By Sales Channel

Regulatory Compliance and Technological Innovation Fortify OEM School Bus Stronghold

Based on the sales channel the market is divided into OEM and retrofitted.

The OEM segment dominates the global school bus market revenue as most school districts and institutions prefer purchasing new vehicles that comply with the latest safety, emission, and efficiency standards. OEMs continuously innovate with electric, hybrid, and connected bus technologies to meet evolving regulatory and operational needs. In May 2023, Blue Bird Corporation expanded its manufacturing capacity in Georgia to meet rising global school bus market demand for new electric and low-emission buses, reaffirming OEMs’ central role in market growth.

Retrofitted educational transport vehicles represent the fastest-growing sales channel, driven by sustainability goals and cost-effective fleet modernization.

School Bus Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific School Bus Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific maintained a strong presence in the global market, reaching USD 5.65 Billion in 2025, accounting for 38.10% share, and is expected to reach USD 6.06 Billion in 2026. Asia Pacific dominates and grows fastest due to expanding student populations, rapid urbanization, and government-backed education transport programs. Countries such as China and India are investing heavily in electric and CNG-powered buses to improve safety and reduce emissions. In August 2024, India’s government announced plans to implement an RFID-based national modern school buses tracking system to enhance student safety and real-time monitoring. The initiative aims to create a centralized database for tracking school transport nationwide, though data privacy and security concerns have been raised by experts. The system will integrate GPS, RFID tags, and cloud analytics.

North America

In 2025, the North America market stood at USD 5.55 Billion, representing 37.46% of global demand, and is projected to grow to USD 5.89 Billion in 2026. North America holds the second-largest school bus market share, driven by strict safety regulations, modernization of existing fleets, and growing adoption of electric school buses. The region benefits from strong government funding and established manufacturers such as Blue Bird and IC Bus.

The U.S. dominates the North American market due to extensive public-school infrastructure, stringent safety standards, and large-scale electrification programs. Federal initiatives and local funding support ongoing fleet renewal. In May 2024, First Student launched six new electric school transport vehicles in Pennsylvania, funded through the EPA’s Clean School Bus Program Round One grants. The initiative supports local districts in reducing emissions, improving air quality, and promoting sustainable student transportation while advancing the company’s goal of electrifying its extensive North American fleet.

Europe

The Europe region captured 15.06% of the global market in 2025, generating USD 2.23 Billion in revenue, and is projected to reach USD 2.34 Billion in 2026. Europe is witnessing steady growth fueled by EU-wide emission reduction targets, urban sustainability goals, and increasing replacement of aging diesel fleets. Nations such as France, Germany, and the U.K. are piloting zero-emission school transport projects to meet carbon-neutral commitments. In January 2023, Forsee Power announced that it will supply the battery systems for the first public school-bus retrofit order in France, converting 49 diesel coaches for Métropole Rouen Normandie into electric vehicles with the help of the retrofit kit by Greenmot.

Rest of the World

The Rest of the World market generated USD 1.39 Billion in 2025, representing 9.39% of the global market landscape, and is expected to reach USD 1.48 Billion in 2026. The Rest of the World region, including South America, the Middle East, and Africa, is experiencing gradual market growth driven by expanding educational access and public transport investments. Governments are adopting safety regulations, pilot electric mobility projects, and technologically advanced buses. In August 2023, Dubai Taxi Corporation announced deployment of hi-tech student mobility fleets for the 2023-2024 academic year. The new fleet will feature real-time GPS tracking, CCTV monitoring, and parent-notification systems, enhancing safety and transparency in student transport across the emirate.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements and OEM Collaborations Define Competitive Landscape

The global market is moderately consolidated, with key players’ increased focus on electrification, safety innovation, and strategic partnerships to strengthen market presence. Key players in the market include Blue Bird Corporation, Thomas Built Buses, IC Bus, Tata Motors, and Yutong Bus Co., Ltd, playing a crucial role in the market growth. Manufacturers are investing in advanced telematics, ADAS, and zero-emission technologies to meet global sustainability mandates. In March 2024, Thomas Built Buses partnered with Proterra to expand its electric drivetrain production, enhancing performance and range efficiency. In July 2024, Tata Motors introduced its new electric bus for schools lineup in India, underscoring increasing regional competitiveness and global emphasis on sustainable student transportation solutions.

LIST OF KEY SCHOOL BUS COMPANIES PROFILED

- Blue Bird Corporation (U.S.)

- Thomas Built Buses, Inc. (U.S.)

- IC Bus (Navistar, Inc.) (U.S.)

- Collins Bus Corporation (U.S.)

- Lion Electric Company (Canada)

- Tata Motors Limited (India)

- Ashok Leyland Limited (India)

- Yutong Bus Co., Ltd. (China)

- Zhengzhou Zhongtong Bus Holding Co., Ltd. (Zhongtong Bus) (China)

- BYD Company Limited (China)

- Anhui Ankai Automobile Co., Ltd. (Ankai Bus) (China)

- Higer Bus Company Limited (China)

- Scania AB (Sweden)

- MAN Truck & Bus SE (Germany)

- Isuzu Motors Limited (Japan)

- Mitsubishi Fuso Truck and Bus Corporation (Japan)

- Alexander Dennis Limited (ADL) (U.K.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Thomas Built Buses unveiled “Wattson,” its first electric Type D bus, extending the Jouley lineage into a high-capacity, flat-front format. The move broadens OEM product coverage across Type C and Type D EVs, giving districts more options for long, dense routes.

- April 2025: Blue Bird Corporation welcomed a new authorized dealership in Alabama, strengthening its dealer network in the Southeastern U.S. This expansion supports faster delivery, local servicing, and greater support for both conventional and electric bus fleets for schools in the region.

- April 2025: A-Z Bus Sales celebrated delivery of its 1,000th all-electric Blue Bird school bus, marking a California milestone and signaling maturing dealer ecosystems for large-scale zero-emission deployments. The delivery at Orange Unified School District reflects cumulative learning on charging, training, and service that’s unlocking faster repeat orders.

- April 2025: Dearborn Public Schools rolled out 18 Blue Bird All American Type D electric buses with support from Michigan’s EGLE, cutting local emissions and noise while expanding high-capacity, zero-emission pupil transport. The deployment shows midwestern districts moving from pilots to multi-dozen fleet waves.

- February 2025: Guilford County Schools in North Carolina introduced 10 Blue Bird Vision propane-powered buses for schools, marking its first deployment of low-emission propane models. The initiative reduces fuel costs and harmful emissions while improving fleet reliability, reflecting the district’s shift toward sustainable student transportation and Blue Bird’s leadership in alternative-fuel school bus innovation.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.11% from 2026-2034 |

|

Unit |

Value (USD Billion) and Volume (Hundred Units) |

|

Segmentation |

By Type, Propulsion, Seating Capacity, Application, Sales Channel, and Region |

|

By Type |

|

|

By Propulsion |

|

|

By Seating Capacity |

|

|

By Application |

|

|

By Sales Channel |

|

|

By Region |

North America (By Type, By Propulsion, By Seating Capacity, By Application, By Sales Channel, and Country)

Europe (By Type, By Propulsion, By Seating Capacity, By Application, By Sales Channel, and Country)

Asia Pacific (By Type, By Propulsion, By Seating Capacity, By Application, By Sales Channel, and Country)

Rest of the World (By Type, By Propulsion, By Seating Capacity, By Application, By Sales Channel, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 14.83 billion in 2025 and is projected to reach USD 27.33 billion by 2034.

In 2025, the market value stood at USD 5.65 billion.

The market is expected to exhibit a CAGR of 7.11% during the forecast period.

The type C segment led the market by type.

Increasing government investments in safe and sustainable student transportation drive market growth.

Key players in the global market include Blue Bird Corporation, Thomas Built Buses, IC Bus, Tata Motors, and Yutong Bus Co., Ltd.

Asia Pacific held the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us