Secondary Battery Market Size, Share & Industry Analysis, By Battery Type (Lithium-ion Battery, {Lithium Iron Phosphate, Lithium Nickel Manganese Cobalt, Lithium Nickel Cobalt Aluminium, Lithium Titanate, and Others), Lead Acid Battery {Flooded Lead Acid Battery, Valve Regulated Lead Acid Battery (VRLA)}, Nickel-Based Battery, Sodium-Ion Battery, and Others), By End-User (Electric Vehicles {Passenger EVs, Commercial EVs, and Others}, Consumer Electronics {Smart Phones, Laptops and Tablets, Wearables, and Others}, Energy Storage System, Industrial, and Others), and Regional Forecast, 2026-2034

Secondary Battery Market Overview

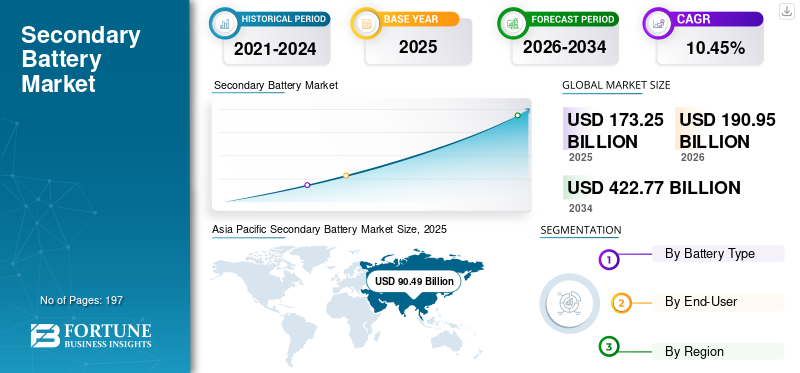

The secondary battery market size was valued at USD 173.25 billion in 2025. The market is projected to grow from USD 190.95 billion in 2026 to USD 422.77 billion by 2034, exhibiting a CAGR of 10.45% during the forecast period. Asia Pacific dominated the secondary battery market with a market share of 52.23% in 2025.

A secondary battery is an electrochemical energy storage device that can be recharged and reused multiple times through reversible chemical reactions. The market has become a critical component of the global energy and electrification ecosystem, driven by the increasing adoption of rechargeable energy storage technologies across multiple industries. Secondary batteries offer high energy density, longer lifespans, and improved efficiency, making them suitable for modern applications that require reliable, sustainable power sources.

The demand for secondary batteries is growing rapidly due to several structural shifts in global energy consumption and technology adoption. One of the primary drivers is the accelerating adoption of electric vehicles, as governments and automotive manufacturers worldwide push to reduce carbon emissions and phase out internal combustion engine vehicles. In addition, the increasing penetration of renewable energy sources, such as solar and wind, has created a strong need for efficient energy storage solutions to manage intermittency and maintain grid stability.

The market is moderately fragmented, with several large global manufacturers alongside numerous regional and specialized battery producers. Major players such as Contemporary Amperex Technology Co., Limited (CATL), LG Energy Solution, Panasonic Energy, Samsung SDI, SK On, BYD Company Ltd., and Tesla account for a significant share of global production capacity, particularly for lithium-ion batteries used in electric vehicles and energy storage systems. To strengthen their market position, leading companies are focusing on capacity expansion, strategic partnerships with automotive OEMs, vertical integration of raw materials, and development of next-generation battery chemistries.

For instance, in June 2025, CATL announced plans to expand its battery-swapping and recycling technology into Europe, aiming to build large networks of battery-swap stations and collaborate with European automakers to reduce EV costs and improve battery lifecycle management.

Download Free sample to learn more about this report.

Secondary Battery Market Trends

Increasing Adoption of Electric Vehicles is Emerging Market Trend

The increasing adoption of electric vehicles is driving significant secondary battery market growth, as EVs rely heavily on rechargeable batteries as their primary power source. Secondary batteries, particularly lithium-ion batteries, provide high energy density, longer lifecycle, and efficient energy storage, making them suitable for electric mobility applications. As governments worldwide implement strict emission regulations and provide incentives for EV adoption, automotive manufacturers are rapidly expanding their production. Additionally, EVs rely on rechargeable batteries, particularly lithium-ion batteries, as their primary power source, thus reshaping the market growth.

- In March 2026, BYD, a Chinese manufacturer of electric vehicles, announced its new Blade Battery 2.0 technology. Blade Battery 2.0 will allow an EV to be charged from 10% to 70% in just five minutes with a power-up charger. This improvement in charging speed and energy density also enhances the safety of these types of batteries and demonstrates the many innovations underway in rechargeable batteries for EVs.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Consumer Electronics to Drive Market Growth

The increasing demand for consumer electronics such as smartphones, laptops, tablets, smartwatches, wireless earbuds, and other portable devices is driving market growth. These devices rely heavily on rechargeable batteries, particularly lithium-ion and lithium-polymer batteries, due to their high energy density, lightweight design, and long cycle life.

In October 2025, Toshiba introduced advanced SCiB lithium-ion battery technologies that are increasingly being adopted in portable electronic devices and compact power systems due to their fast charging, long lifecycle, and enhanced safety. These rechargeable batteries support applications in consumer electronics, such as portable devices, smart equipment, and compact energy storage units, offering higher efficiency and longer operational life than conventional battery technologies.

MARKET RESTRAINTS

High Cost of Advanced Battery Technologies Hampers Market Expansion

The higher cost of advanced battery technologies, particularly lithium-ion, solid-state, and other next-generation rechargeable batteries, restrains the market growth. These batteries require expensive raw materials such as lithium, cobalt, nickel, and rare earth elements, along with complex manufacturing processes and advanced battery management systems. Additionally, significant investments in research and development, safety systems, and production facilities further increase the overall cost of battery production.

MARKET OPPORTUNITIES

Technological Advancements in Battery Technology to Provide Lucrative Market Opportunities

Advancements in battery technology are offering market opportunities by improving performance, efficiency, and safety. Innovations such as high-energy-density lithium-ion batteries, solid-state batteries, and sodium-ion batteries are enabling longer battery life, faster charging, and enhanced reliability. These improvements make secondary batteries more suitable for a wide range of applications, including electric vehicles, renewable energy storage systems, consumer electronics, and industrial equipment.

In April 2024, CATL unveiled the world’s first-ever LFP battery capable of exceeding 1,000km in range and charging at 4C: the Shenxing PLUS. Less than eight months after introducing the Shenxing super-fast-charging battery model (in August 2023), CATL has continued to expand the boundaries of LFP battery technology, marking a new era of industry change toward more efficient, rapid-charge LFP batteries.

MARKET CHALLENGES

High Cost of Raw Materials to Challenge Market Growth

The high cost of raw materials is a major factor restraining the growth of the market. Rechargeable batteries, particularly lithium-ion batteries, require critical materials such as lithium, cobalt, nickel, and graphite, which are often expensive and subject to price fluctuations. The limited availability of these materials and increasing global demand from industries such as electric vehicles, consumer electronics, and energy storage systems can further drive up costs.

Segmentation Analysis

By Battery Type

Lithium-ion Batteries Dominates Market Due to Their High Energy Density and Longer Cycle Life

Based on battery type, the market is segmented into Lithium-ion (Li-ion) battery, lead-acid battery, Nickel-based battery (NiMH and Ni-Cd), sodium-ion battery, and others.

Lithium-ion batteries represent the largest segment globally, driven by their high energy density, longer cycle life, lightweight design, and superior charge-discharge efficiency compared to conventional rechargeable batteries. The widespread adoption of lithium-ion batteries in electric vehicles, consumer electronics, energy storage systems, and portable devices has significantly strengthened their market position. Rapid electrification of the transportation sector and large-scale deployments of renewable energy storage are further accelerating lithium-ion battery demand.

Sodium-ion batteries are projected to grow at a CAGR of 22.39% during the forecast period. Emerging technologies such as sodium-ion batteries are attracting attention as cost-effective and resource-efficient alternatives to lithium-ion batteries, particularly for grid-scale energy storage and entry-level electric vehicles. Sodium-ion batteries offer advantages such as abundant raw material availability, improved thermal stability, and lower production costs, which could help address supply constraints for lithium, cobalt, and nickel.

By End-User

To know how our report can help streamline your business, Speak to Analyst

Surging Demand for Rechargeable Batteries Drives Consumer Electronics Segment Dominance

Based on end-user, the market is segmented into Electric Vehicles (EVs), consumer electronics, Energy Storage Systems (ESS), industrial applications, and others.

Consumer electronics currently represent the largest end-user segment, primarily due to the widespread adoption of rechargeable batteries in devices such as smartphones, laptops, tablets, wearable devices, cameras, and other portable electronics. The high global penetration of smart devices, combined with frequent product replacement cycles and continuous technological upgrades, sustains strong demand for secondary batteries in this segment. Lithium-ion batteries dominate consumer electronics applications due to their high energy density, lightweight design, and long life cycle, making them ideal for compact electronic devices that require reliable, long-lasting power.

Electric vehicles represent the fastest-growing segment, with a CAGR of 13.64% during the forecast period. This is driven by the global shift toward vehicle electrification and decarbonization of the transportation sector. Governments worldwide are implementing stricter emission regulations, as well as incentives and subsidies, to promote EV adoption, while automotive manufacturers are significantly expanding their electric vehicle portfolios.

Secondary Battery Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Secondary Battery Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region dominated the global market, accounting for USD 90.49 billion in 2025 and is expected to reach USD 101.07 billion in 2026. The region’s growth is primarily supported by its position as the global manufacturing hub for batteries and electronic components, along with the presence of well-established supply chains for lithium, nickel, and other key materials. Additionally, the region benefits from high production of consumer electronics, expanding industrial base, and strong policy support for domestic battery manufacturing and energy storage deployment. Countries such as China, Japan, and South Korea continue to lead in technological innovation and large-scale battery production capacity.

China Secondary Battery Market

In 2025, the China market reached USD 50.31 billion. China’s market is driven by its dominance in battery manufacturing capacity, strong domestic demand for electronic devices, and large-scale deployment of energy storage systems. The country also benefits from integrated supply chains and government-backed industrial policies supporting battery innovation and production.

- In March 2026, BYD launched the new second-generation Blade Battery with its FLASH Charging Technology. This marks BYD's second-generation battery and second-generation fast-charging solution, which, according to BYD, provides the fastest electric vehicle charging in the world. It represents BYD's most significant battery development since the original Blade Battery launched in 2020. The announcement was made at BYD's headquarters in Shenzhen, China.

India Secondary Battery Market

The Indian market in 2025 was at USD 12.72 billion, accounting for roughly 7.34% of the global market. The market is expanding due to the growing demand for consumer electronics, rapid digitalization, and increasing investments in renewable energy infrastructure. Government initiatives such as the Production Linked Incentive (PLI) scheme are encouraging local battery manufacturing, while the expansion of telecommunications and data infrastructure is further supporting demand for reliable energy storage solutions.

North America

North America was valued at USD 31.45 billion in 2025 and is expected to reach USD 34.21 billion in 2026. North America is witnessing steady growth, supported by rising investments in domestic battery manufacturing, expansion of grid-scale energy storage projects, and increasing focus on energy security. The region is also benefiting from policy measures aimed at strengthening local supply chains and reducing reliance on imports, along with growing demand from data centers, industrial automation, and backup power applications.

U.S. Secondary Battery Market

The U.S. market was valued at USD 28.24 billion in 2025. The U.S. market is growing due to increasing adoption of electric vehicles, expansion of battery manufacturing facilities, rising demand for energy storage systems for renewable energy and government initiatives supporting clean energy and domestic battery production.

Europe

The Europe region accounted for USD 37.52 billion in 2025 and is predicted to reach USD 40.87 billion in 2026. The market is driven by strict environmental regulations, strong emphasis on sustainability, and increasing investments in renewable energy integration. The region is focusing on building a localized battery value chain, supported by funding programs and regulatory frameworks aimed at reducing dependency on imports. Additionally, the growth of stationary energy storage systems and industrial electrification is contributing to rising battery demand.

U.K. Secondary Battery Market

The U.K. market in 2025 was at USD 6.76 billion, representing 3.9% of the global market. The U.K. market is growing due to the expansion of renewable energy capacity, increasing deployment of residential and commercial energy storage systems, and government initiatives supporting low-carbon technologies. Investments in battery innovation and grid modernization.

Germany Secondary Battery Market

The German market in 2025 was at USD 8.24 billion. The market is growing due to the strong expansion of the electric vehicle industry, rising investments in battery manufacturing, and supportive government policies that promote clean energy and electrification. Germany is home to major automotive manufacturers such as Volkswagen, BMW, and Mercedes-Benz, which are rapidly increasing electric vehicle production, thereby boosting demand for rechargeable batteries.

Latin America & Middle East Africa

Latin America and the Middle East & Africa accounted for USD 8.40 billion and USD 5.39 billion in 2025. The Latin American market is developing steadily, driven by the growing deployment of renewable energy projects, increasing need for grid reliability, and rising investments in mining and resource-based industries. Countries such as Chile, Argentina, and Brazil are also important due to their abundance of lithium resources, which supports the regional battery ecosystem. Additionally, the expansion of off-grid and rural electrification projects is contributing to increased demand for battery storage solutions.

The Middle East & Africa market is growing due to the increasing adoption of renewable energy projects, rising demand for energy storage systems, and expanding telecommunications infrastructure.

GCC Secondary Battery Market

The GCC market in 2025 was at USD 2.53 billion. The GCC region is a key contributor, supported by large-scale investments in renewable energy projects, smart city developments, and growing demand for uninterrupted power supply across commercial and industrial sectors. Countries such as Saudi Arabia and the UAE are focusing on energy transition initiatives and grid modernization, which is driving adoption of advanced battery technologies .

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players are Investing in Advanced Secondary Battery Technologies and Expanding Production Capacity to Sustain Competition

Secondary battery vendors are undertaking various developments to support market growth by focusing on technological innovation, production expansion, and strategic partnerships. Major battery manufacturers such as CATL, LG Energy Solution, Panasonic, and Samsung SDI are investing heavily in advanced battery technologies, including solid-state, sodium-ion, and high-energy-density lithium-ion batteries, to improve performance, safety, and charging speed.

In December 2025, the IFC (International Finance Corporation) invested about USD 50 million of its funds to help build India's First Integrated Battery Materials Plant (GFCL EV Products) in Gujarat. This facility will produce essential battery materials commonly used in EV and energy storage solutions, thereby supporting the global secondary battery supply chain.

LIST OF SECONDARY BATTERY COMPANIES PROFILED

- CATL (China)

- LG Energy Solution Ltd. (South Korea)

- Panasonic Holdings Corporation (Japan)

- Samsung SDI Co., Ltd. (South Korea)

- BYD Company Ltd. (China)

- SK On Co., Ltd. (South Korea)

- Saft Groupe S.A. (TotalEnergies) (France)

- GS Yuasa Corporation (Japan)

- Exide Industries Ltd. (India)

- Toshiba Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- December 2025: SAMSUNG SDI announced that it had signed a Memorandum of Understanding (MOU) with leading Korean automaker KG Mobility (KGM) to jointly develop next-generation battery pack technologies for electric vehicles. SAMSUNG SDI today announced that it has signed a Memorandum of Understanding (MOU) with leading Korean automaker KG Mobility (KGM) to develop next-generation battery pack technologies for electric vehicles jointly.

- August 2025: Toshiba Corporation and battery-tech startup Naturenix Inc. are advancing their secondary battery subscription demonstration project for electric motorcycle taxis in Bangkok, Thailand. The companies are expanding the program's scale and transitioning to a paid subscription model for battery usage. As part of the next phase, production of secondary battery packs and related components has already begun to support the initiative. The new demonstration phase is scheduled to run from December 2025 through March 2026, aiming to promote the adoption of rechargeable battery solutions for electric mobility in the region.

- July 2025: Panasonic Energy Co., Ltd., part of the Panasonic Group, announced the official opening of its new EV cylindrical lithium-ion secondary battery production facility in De Soto, near Kansas City, Missouri. This is one of the largest automotive secondary battery manufacturing facilities in North America. At this time, the company has begun mass manufacturing 2170 cylindrical lithium-ion secondary battery cells at its second North American facility, the Kansas Factory. This factory will be designed to have an annual production capacity of about 32 GWh to meet increased demand for EV secondary batteries.

- June 2025: Safran Electrical & Power, a world leader in electric aircraft systems, and Saft, a subsidiary of TotalEnergies that develops advanced secondary batteries for a wide range of industrial sectors, including aerospace, signed an exclusive partnership to develop a high-voltage secondary battery system for aviation, paving the way for the next generation of aircraft.

- May 2023: Honda Motor Co., Ltd., and GS Yuasa are collaborating to develop the next generation of lithium-ion batteries for electric vehicles. This partnership aims to improve battery performance, safety, and energy density as we transition to electric mobility. The collaboration focuses on improving battery performance, safety, and energy density, thereby advancing secondary battery technologies and accelerating the transition toward electric mobility.

REPORT COVERAGE

The global secondary battery market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.45% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Battery Type, By End-User, and Region |

| By Battery Type |

|

| By End-User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 173.25 billion in 2025 and is projected to reach USD 422.77 billion by 2034.

The market is expected to exhibit a CAGR of 10.45% during the forecast period (2026-2034).

The consumer electronics segment led the market in terms of end-user.

Rising demand for consumer electronics to drive the market growth.

CATL, LG Energy Solution Ltd., BYD Company Ltd., and other companies are among the prominent players in the market.

Asia Pacific region held the largest share of the market.

Technological advancements in battery favors the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 197

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us