Secure Access Service Edge Market Size, Share & Industry Analysis, By Service Type (Network Services, Security Services, and Managed & Platform Services), By Deployment (Cloud-Native SASE, Hybrid SASE, and On-premises), By Enterprise Type (Large Enterprises and Small & Medium-sized Enterprises (SMEs)), By Industry (IT & Telecom, BFSI, Manufacturing, Retail & E-commerce, Healthcare, Government, Energy & Utilities, and Others), and Regional Forecast, 2026 – 2034

Secure Access Service Edge Market Overview

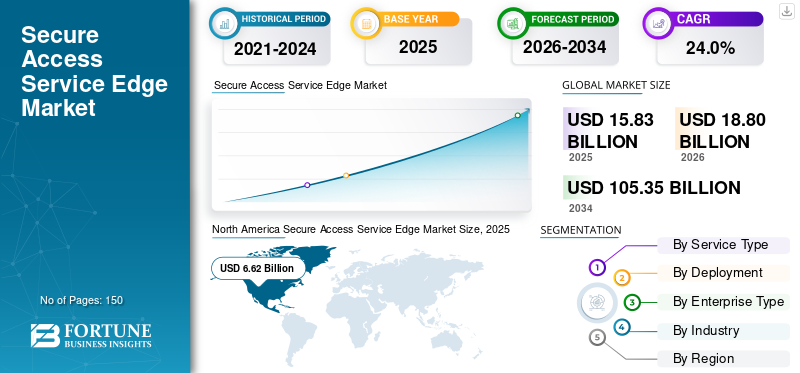

The global secure access service edge market size was valued at USD 15.83 billion in 2025. The market is projected to grow from USD 18.80 billion in 2026 to USD 105.35 billion by 2034, exhibiting a CAGR of 24.0% during the forecast period. North America dominated the secure access service edge market with a market share of 41.81% in 2025.

Secure Access Service Edge (SASE) solutions are advanced platforms that integrate networking and security to provide enterprises with secure, scalable, and cloud-native access across distributed environments. Unlike traditional VPN or point-based security solutions, SASE platforms offer centralized policy enforcement, Zero Trust access, SD-WAN, and AI-driven threat detection, enabling organizations to efficiently manage complex hybrid and multi-cloud infrastructures.

The growing adoption of hybrid workforces, cloud-based applications, and distributed enterprise networks is increasing the demand for high-performance, reliable, and flexible secure access solutions. Enterprises are investing in SASE to streamline connectivity, consistently enforce security policies, reduce latency, and protect against evolving cyber threats.

Key players such as Cisco Systems, Palo Alto Networks, Zscaler, and Fortinet are expanding their SASE portfolios through platform integration, AI-enabled threat prevention, and strategic partnerships with cloud providers and managed service operators. These vendors focus on delivering secure, high-performance, and scalable platforms that support hybrid work, multi-cloud deployments, and real-time threat analytics.

Download Free sample to learn more about this report.

IMPACT OF AI

AI-Driven Threat Detection and Policy Automation Strengthening Security Posture Strengthen Market Growth

The adoption of AI within SASE platforms is significantly enhancing enterprise security and network management by enabling automated threat detection, intelligent policy enforcement, and optimized traffic routing. AI analyzes network behavior, user activity, and cloud workloads to identify anomalies, generate dynamic access policies, and anticipate potential risks, reducing manual intervention and operational errors. It supports proactive security capabilities across multi-cloud and hybrid environments, ensures compliance, and improves performance for distributed and remote users through real-time traffic optimization. For instance,

- In March 2026, Cato Networks launched its first GPU‑powered SASE platform with native AI security, embedding NVIDIA GPUs into its global backbone to enable real‑time AI/ML threat inspection. The enhancement improves performance and consistent policy enforcement across cloud and hybrid environments.

By integrating AI capabilities, SASE platforms evolve from reactive tools into self-optimizing, intelligent solutions that improve operational efficiency, enhance the user experience, and provide vendors with a competitive advantage in the rapidly growing secure access market.

SECURE ACCESS SERVICE EDGE MARKET TRENDS

Shift to Cloud-Native SASE Architectures Across Enterprise Services to Strengthen Market Expansion

Enterprises globally are accelerating the migration of critical workloads to public, private, and multi-cloud environments to achieve greater operational flexibility, scalability, and cost efficiency. For instance,

- According to the European Commission, in 2025, cloud computing adoption among medium-sized enterprises rose significantly, with 66.78% using purchased cloud services, up from 59.09% in 2023.

Traditional network infrastructures such as VPNs and MPLS are increasingly inadequate for delivering secure, high-performance access across distributed cloud applications. SASE platforms address this gap by providing centralized security policies, optimized cloud routing, and threat protection across all cloud workloads, enabling seamless connectivity for remote and hybrid teams.

Moreover, the rapid adoption of SaaS applications and microservices architectures amplifies the need for secure cloud access, as sensitive data traverses multiple environments beyond the traditional corporate perimeter. SASE solutions reduce the risk of data leakage, enhance compliance with regional and industry-specific regulations, and allow IT teams to enforce consistent security controls across hybrid and multi-cloud deployments.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Adoption of Hybrid and Remote Work Driving Secure Access Needs Drives Market Growth

The ongoing shift toward hybrid and remote work models has transformed the way enterprises approach network and security infrastructure. Organizations now require secure, seamless access to enterprise applications, data, and collaboration tools from any location, often across multiple cloud environments. For instance,

- According to CXOToday, India is expected to have between 60 million and 90 million remote workers by 2025, accounting for nearly 10% to 15% of the country’s workforce, based on the World Bank’s estimate of a 593 million labor force.

SASE platforms address this need by providing centralized security enforcement, optimized connectivity, and secure cloud access, ensuring consistent policy application regardless of user location.

In addition, the hybrid work trend is driving the adoption of Zero Trust Network Access (ZTNA) frameworks within SASE, enabling organizations to verify user identity and device posture before granting access to sensitive resources. Enterprises are also leveraging SASE to simplify IT operations, reduce dependency on legacy VPNs, and maintain high performance for distributed teams. As hybrid work becomes a standard operational model, SASE adoption is increasingly viewed as a strategic enabler for secure, scalable, and resilient enterprise connectivity.

MARKET RESTRAINTS

Rapidly Evolving Cyber Threats Increase Operational Complexity to Restraint Market Growth

The dynamic nature of cyber threats presents a significant challenge to secure access service edge market growth. Enterprises may hesitate to deploy new SASE platforms if they perceive the security features as immature or insufficient to handle emerging attack vectors, such as AI-driven malware, sophisticated phishing campaigns, and zero-day exploits. Organizations operating in sectors such as BFSI, healthcare, and government that manage sensitive data are particularly cautious and often delay adoption until the platform demonstrates robust, real-world protection capabilities.

Moreover, the constantly evolving threat landscape necessitates frequent product upgrades and patches, which increases operational complexity for IT and security teams. Enterprises must continuously monitor for new vulnerabilities, update configurations, and retrain staff to leverage newly introduced SASE capabilities effectively.

MARKET OPPORTUNITIES

Industry-Specific Solutions Tailored to BFSI, Healthcare, Retail, and Government to Create Growth Opportunities for Market

The SASE market presents a significant growth opportunity through the development of industry-tailored solutions. Sectors such as BFSI, healthcare, retail, and government have distinct security, regulatory, and operational requirements that generic SASE offerings may not fully address. For instance, financial institutions require payment security, fraud detection, and regulatory compliance; healthcare organizations need secure access for telehealth platforms and electronic health records; retail enterprises demand protection of point-of-sale systems, cloud-based inventory management, and e-commerce platforms; and government entities prioritize secure data exchange and protection of critical infrastructure.

By creating customized SASE solutions for these verticals, vendors can differentiate themselves and address specific pain points. Tailored offerings can include predefined security policies, compliance frameworks, threat intelligence integrations, and workflow optimizations designed for the operational context of each industry.

Segmentation Analysis

By Industry

IT & Telecom Vertical Commanded Market Fueled by High Cloud Adoption and Distributed Networks

Based on industry, the market is classified into IT & telecom, BFSI, manufacturing, retail & e-commerce, healthcare, government, energy & utilities, and others.

IT & telecom segment held the majority share of the industry market in 2024. In 2025, the segment dominated with a 25.5% share, as companies are early adopters of cloud, SD-WAN, and advanced networking technologies. They operate distributed networks across global offices and cloud infrastructures, requiring robust, integrated security, and access solutions. Additionally, IT & Telecom companies often provide managed secure services and enterprise networking solutions themselves, making SASE both a critical internal tool and a client-facing service.

Retail & e-commerce segment is expected to witness the highest CAGR of 28.9% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Service Type

Security Services Led Market Driven by Growing Threat Landscape and Compliance Requirements

Based on service type, the market is divided into network services, security services, and managed & platform services.

Security services segment held the majority share by service type in 2024. In 2025, the segment also dominated with 45.7% share as enterprises prioritize protecting data, applications, and network traffic in increasingly complex hybrid and multi-cloud environments. With rising cyber threats, regulatory compliance requirements, and the shift to remote work, organizations are investing heavily in threat detection, Zero Trust enforcement, and continuous monitoring. Security services provide the essential backbone for all SASE deployments, ensuring safe connectivity and mitigating risks, which drives their larger share compared to network or managed/platform services.

Managed & platform services segment is expected to witness the highest CAGR of 26.8% during the forecast period.

By Deployment

Cloud-Native SASE Dominated Deployment Segment Enabled by Scalable and Flexible Architecture

Based on deployment, the market is segmented into cloud-native SASE, hybrid SASE, and on premise.

Cloud-native SASE segment held the majority share by deployment in 2024. In 2025, the segment dominated with a 57.9% share as most enterprises are rapidly migrating workloads to the cloud, and cloud-native architectures provide scalable, centralized security and networking without the limitations of on-premises infrastructure. Cloud SASE allows organizations to enforce consistent policies across distributed users, remote offices, and multiple cloud applications, making it the preferred deployment model for large-scale enterprise adoption.

Hybrid SASE segment is expected to witness the highest CAGR of 21.3% during the forecast period.

By Enterprise Type

Large Enterprises Hold Majority Share Due to Extensive IT Infrastructure and Complex Networking Needs

Based on enterprise type, the market is categorized into large enterprises and small & medium-sized enterprises (SMES).

Large enterprises segment held the majority share of the enterprise type in 2024. In 2025, the segment held a major share as they have extensive IT infrastructure, distributed offices, and complex networking requirements that demand robust, scalable, and secure access solutions. They face higher exposure to cyber threats and stricter regulatory and compliance requirements, motivating substantial investment in integrated SASE platforms. Additionally, their larger budgets and dedicated IT/security teams enable faster adoption of advanced features such as Zero Trust, SD-WAN, and cloud security, giving them a majority share compared to SMEs, which often rely on simpler or managed solutions.

Small & Medium-sized Enterprises (SMEs) segment is expected to witness the highest CAGR of 27.4% during the forecast period.

Secure Access Service Edge Market Regional Outlook

By region, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America Secure Access Service Edge Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the majority of secure access service edge market share and was valued at USD 6.62 billion in 2025 due to its high concentration of large enterprises, advanced IT infrastructure, and early adoption of cloud and security technologies. The region hosts leading technology vendors, cloud service providers, and managed service operators, which accelerates enterprise adoption of SASE solutions. A strong regulatory focus on data protection, combined with high cybersecurity awareness, is driving organizations across the BFSI, healthcare, and government sectors to invest heavily in integrated, secure access platforms.

Additionally, the prevalence of hybrid workforces, multi-cloud deployments, and distributed enterprise networks in the U.S. and Canada creates significant demand for centralized, cloud-native SASE solutions, giving North America the largest revenue share compared to other regions.

U.S. Secure Access Service Edge Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market was valued at around USD 5.42 billion in 2025, accounting for roughly 34.2% of sales.

Europe

Europe is projected to grow at 22.6% over the coming years and reached a valuation of USD 3.15 billion in 2025, driven by regulatory pressure, digital transformation, and cloud adoption. The enforcement of the GDPR, NIS2, and eIDAS directives compels enterprises to adopt centralized, cloud-native security architectures, thereby increasing demand for SASE. Germany, the U.K., and France are modernizing government IT infrastructure and enabling hybrid work, which is driving enterprise investment in Zero Trust and SD-WAN-integrated solutions.

U.K. Secure Access Service Edge Market

The U.K. market was valued at around USD 0.66 billion in 2025, representing roughly 4.2% of global revenues.

Germany Secure Access Service Edge Market

Germany’s market reached approximately USD 0.61 billion in 2025, equivalent to around 3.9% of global sales.

Asia Pacific

Asia Pacific is expected to grow at the highest CAGR and reached a valuation of USD 4.69 billion in 2025, driven by massive cloud adoption, aggressive digital transformation initiatives, and rapidly expanding enterprise IT infrastructure across both mature and emerging markets. China and India, for instance, are witnessing exponential growth in cloud-based enterprise applications and e-commerce platforms, driving demand for secure access solutions that integrate networking and security. The proliferation of hybrid work models in Japan, South Korea, and Singapore is creating urgent requirements for low-latency, cloud-native SASE deployments to ensure secure connections for distributed employees.

Japan Secure Access Service Edge Market

The Japanese market was valued at around USD 0.85 billion in 2025, accounting for roughly 5.4% of global revenues.

China Secure Access Service Edge Market

China’s market is projected to be one of the largest globally, with 2025 revenues valued at around USD 1.54 billion, representing roughly 9.7% of global sales.

India Secure Access Service Edge Market

The India market was valued at around USD 0.97 billion in 2025, accounting for roughly 6.1% of global market share.

South America and Middle East & Africa

The Middle East & Africa region is expected to grow at the second-highest CAGR during the forecast period in the market. It is due to rapid digital transformation initiatives, increased cloud adoption, and growing cybersecurity awareness across enterprises and government sectors. Countries in the GCC (Saudi Arabia, UAE, and Qatar) are investing heavily in smart city projects, cloud-based public services, and advanced IT infrastructure, which requires secure, centralized access solutions. Additionally, large enterprises and telecom providers in the region are adopting cloud-native SASE platforms to support hybrid workforce models, remote branch connectivity, and multi-cloud deployments.

South America is expected to grow at a stable CAGR during the forecast period, due to a combination of gradual digital transformation, cautious enterprise IT spending, and emerging cloud adoption. Brazil, Argentina, and Chile are increasingly migrating workloads to cloud environments. Still, adoption is slower compared to regions including Asia Pacific or North America due to limited infrastructure in certain areas and budget constraints among SMEs.

GCC Secure Access Service Edge Market

The GCC market reached around USD 0.30 billion in 2025, representing roughly 1.9% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Industry Players Driving Innovation and Strategic Expansion in SASE Market

Key players in the SASE market are enhancing their platforms to meet the growing demand for scalable, secure, and AI-enabled secure access solutions. Leading vendors are pursuing strategic initiatives such as partnerships, acquisitions, and joint technology development to expand their global footprint, strengthen cloud-native offerings, and integrate advanced features such as Zero Trust, SD-WAN, and AI-driven threat detection. These efforts aim to provide enterprises with high-performance, resilient, and flexible SASE platforms that support hybrid workforces, multi-cloud environments, and increasingly complex security and networking requirements.

LIST OF KEY SECURE ACCESS SERVICE EDGE COMPANIES PROFILED IN REPORT

- Cisco Systems, Inc. (U.S.)

- Palo Alto Networks (U.S.)

- Zscaler, Inc. (U.S.)

- Fortinet, Inc. (U.S.)

- Netskope (U.S.)

- Cloudflare, Inc. (U.S.)

- Cato Networks (Israel)

- Check Point Software Technologies Ltd (Israel)

- Forcepoint (U.S.)

- Barracuda Networks, Inc. (U.S.)

- Versa Networks, Inc. (U.S.)

- VMware (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2026: Altair released Altair HPCWorks 2026, enhancing its HPC and cloud platform to support cloud-based EDA workloads. The update improves GPU integration, AI-driven resource optimization, Kubernetes connectivity, and advanced reporting, enabling semiconductor and electronic design teams to run large-scale EDA jobs more efficiently in cloud environments.

- February 2026: Cloudflare announced that its Cloudflare One SASE platform now supports modern Post‑Quantum (PQ) encryption standards, making it the first SASE solution to protect against future quantum computing threats natively. This upgrade enhances security for enterprise connections across its global network at no extra cost.

- February 2026: Cisco announced AI‑aware security advancements for its Secure Access Service Edge (SASE) offering, introducing industry‑first capabilities, including AI-driven traffic detection and optimization to secure and accelerate agentic workflows. These enhancements aim to improve threat detection, AI supply chain governance, and runtime protection for distributed enterprise environments.

- January 2026: TPx launched TPx Managed SASE, a fully managed SASE service designed to help businesses adopt a modern secure access architecture without internal operational burden. The offering merges networking and security with Zero Trust policies and is optimized for cloud‑centric enterprise environments.

- September 2025: Forrester updated its SASE evaluation, highlighting significant market transformation as vendors embed stronger Zero Trust capabilities and improved integration across networking + security functions. This signals maturity and broader adoption of advanced features.

- August 2025: AT&T and Cisco launched the AT&T Secure Access Service Edge (SASE) solution, combining AT&T’s network expertise with Cisco’s cloud‑delivered security technologies. The solution offers multilayer defense with SD‑WAN, zero trust, and centralized policy management designed for enterprises modernizing legacy infrastructure.

REPORT COVERAGE

The secure access service edge market report provides a comprehensive analysis of the industry, focusing on key market participants, service types, and major deployment areas. It offers valuable insights into current market trends, emerging technologies, and significant industry developments shaping the competitive landscape. The report also examines key growth drivers, challenges, opportunities, and strategic initiatives that have contributed to the expansion of the SASE market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 24.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service Type, Deployment, Enterprise Type, Industry, and Region |

| By Service Type |

|

| By Deployment |

|

| By Enterprise Type |

|

| By Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 15.83 billion in 2025 and is projected to reach USD 105.35 billion by 2034.

In 2025, the North America’s market value stood at USD 6.62 billion.

The market is expected to grow at a CAGR of 24.0% during the forecast period.

By industry, the IT & telecom segment is expected to lead the market.

Rising adoption of hybrid and remote work driving secure access needs drives market growth.

Cisco Systems, Palo Alto Networks, Zscaler, and Fortinet are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us