Semaglutide Market Size, Share & Industry Analysis, By Product (Ozempic, Rybelsus, Wegovy, and Others), By Disease Indication (Type 2 Diabetes Mellitus, Chronic Weight Management/Obesity, Cardiometabolic Risk Management, and Others), By Route of Administration (Subcutaneous {Prefilled Multi-dose Pens and Prefilled Single-dose Pens} and Oral), By Type (Branded and Generic/Non-originator), By Age (Pediatric and Adults), By Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies, Specialty Pharmacies, and Others), and Regional Forecast, 2026-2034

Semaglutide Market Size and Future Outlook

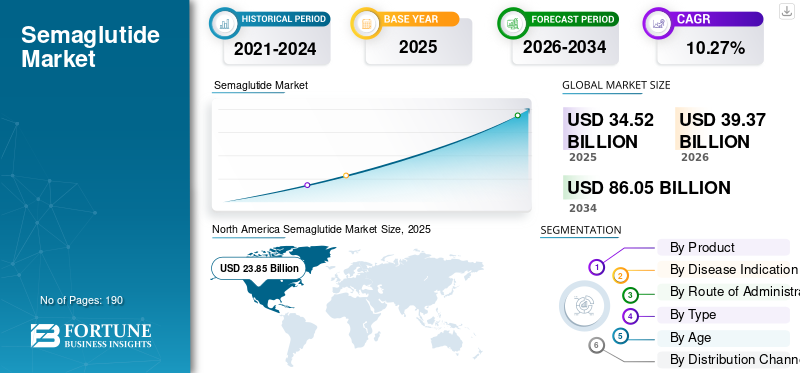

The global semaglutide market size was valued at USD 34.52 billion in 2025 and is projected to grow from USD 39.37 billion in 2026 to USD 86.05 billion by 2034, exhibiting a CAGR of 10.27% during the forecast period. North America dominated the semaglutide market with a market share of 69.09% in 2025. The glbal semaglutide industry growth is driven by rising obesity prevalence, GLP-1 therapies adoption, and expanding regulatory approvals.

Semaglutide-based therapies are gaining wider acceptance as they help improve glycemic control, support weight reduction, and are being used across broader patient groups. As clinical confidence increases and companies expand access, supply, and product formats, the market is expected to witness sustained growth across major regions.

The global market is projected to grow strongly in the coming years, driven by the rising burden of obesity, prevalence of type 2 diabetes, and the increasing demand for effective long-term metabolic disease management. Furthermore, continued investments in and lifecycle expansion of semaglutide products, along with strategic collaborations among key companies, are supporting overall market expansion.

- For instance, in March 2026, Novo Nordisk collaborated with Hims, Inc. as part of a new strategy for weight-loss care treatments involving GLP-1s, evolving its U.S. offering to align with the company's approach globally. In the U.S., the company plans to provide GLP-1 customers with access to a broad assortment of U.S. FDA-approved medications and offer compounded semaglutide through the platform on a limited scale.

Key players in the semaglutide industry, such as Novo Nordisk A/S., Eli Lilly and Company, AstraZeneca PLC, and Sanofi, are focusing on expanding their offerings and strengthening their market positions. Novo Nordisk remains the dominant player in the global semaglutide market, supported by a strong portfolio including injectable and oral formulation options.

Products such as Ozempic, Rybelsus, and Wegovy have achieved substantial market penetration, supported by multiple FDA approvals and expanding regulatory approvals across global markets. This has reinforced the company’s leading semaglutide market share and established a high barrier to entry for competitors.

The global semaglutide market is driven by the increasing prevalence of type 2 diabetes and the growing demand for effective obesity treatments. The semaglutide market size is expanding significantly as GLP-1 receptor agonist therapies gain widespread clinical adoption. These therapies demonstrate strong efficacy in glycemic control and weight loss, positioning semaglutide-based therapies as a cornerstone in chronic weight management.

Download Free sample to learn more about this report.

Semaglutide Market KEY TAKEAWAYS

- 2025 Market Size: USD 34.52 billion

- 2026 Market Size: USD 39.37 billion

- 2034 Forecast Market Size: USD 86.05 billion

- CAGR: 10.27% from 2026–2034

- North America dominated the semaglutide market with a 69.09% share in 2025.

- The Ozempic segment held the largest market share due to strong commercial adoption.

- The Type 2 Diabetes Mellitus segment accounted for the largest market share.

North America

The market reached USD 23.85 billion in 2025 and continues to lead globally.

Europe

The market is projected to reach USD 6.61 billion in 2026, growing at a 12.96% CAGR.

Asia Pacific

The market is expected to reach USD 4.67 billion in 2026, driven by rising diabetes and obesity prevalence.

U.S.

The market is estimated at USD 24.10 billion in 2026, accounting for 61.20% of global revenues.

Japan

The market is estimated at USD 1.11 billion in 2026, accounting for 2.81% of global revenues.

Read More

Semaglutide Market Trends

Increasing Demand for Long-Term Prescription Weight Management Solutions is Emerging as a Key Market Trend

The global market is witnessing a shift toward long-term prescription-based weight management, as obesity is increasingly being treated as a chronic condition. Patients, physicians, and healthcare platforms are showing interest in therapies that can support sustained weight reduction over a longer treatment period. This is improving the commercial outlook for semaglutide, as its clinical profile and growing use in obesity care are making it a more accepted option in routine metabolic disease management. Additionally, broader availability, self-pay access models, and new product formats are further strengthening this trend across the market.

- For instance, in January 2026, Novo Nordisk announced that the Wegovy pill, described as an oral GLP-1 for weight loss in adults, was available across the U.S. through more than 70,000 pharmacies and multiple care channels. This development is expected to facilitate easier patient access to long-term prescription obesity treatment, further accelerating the adoption of semaglutide-based therapies in the market.

A key trend is the broadening use of semaglutide-based therapies beyond type 2 diabetes into chronic weight management and cardiometabolic risk reduction. This expansion reflects increasing recognition of obesity as a primary disease, driving sustained demand for GLP-1 therapies.

Download Free sample to learn more about this report.

The shift toward oral formulation represents a significant advancement. Oral semaglutide is improving patient adherence by offering a non-invasive alternative to injectable treatments. This trend is expanding accessibility and supporting wider adoption across diverse patient populations, particularly those reluctant to initiate injectable therapy.

Another notable trend is the integration of semaglutide into comprehensive treatment pathways. Healthcare providers are combining pharmacotherapy with lifestyle interventions to enhance long-term outcomes. This approach is reinforcing the role of semaglutide within broader metabolic disease management strategies.

Key Market Dynamics

Market Drivers

The rising global burden of Obesity and Type 2 Diabetes is Driving Market Growth.

A key factor driving the global semaglutide market growth is the rising burden of Type 2 diabetes and obesity globally. As these conditions increase, healthcare systems and physicians are placing greater focus on treatments that can improve blood sugar control while also supporting meaningful weight reduction. This is increasing demand for semaglutide-based therapies, as they address two major metabolic health needs through a single treatment approach. In addition, growing awareness of obesity as a chronic disease and the expanding diabetes patient pool are expected to support long-term market growth.

- For instance, in February 2026, Novo Nordisk announced a significant reduction in the U.S. list price for Wegovy, Ozempic, and Rybelsus, while continuing efforts to expand access to its semaglutide medicines. This is expected to support wider patient adoption of obesity and diabetes treatments, further strengthening demand in the overall market.

The rising prevalence of metabolic disorders is creating sustained demand for effective GLP-1 receptor agonist therapies. Semaglutide-based therapies have demonstrated strong clinical outcomes in glycemic control and weight loss, supporting their rapid adoption across healthcare systems.

Expanding use of semaglutide in chronic weight management is a significant growth catalyst. Physicians are increasingly prescribing these therapies beyond diabetes treatment, addressing obesity as a primary condition. This shift is supported by growing awareness of obesity-related complications, including cardiovascular risks, which further reinforces demand for advanced obesity treatments.

Regulatory approvals are also accelerating market expansion. Multiple FDA approvals and global regulatory approvals for semaglutide products have expanded access across key markets. These approvals enable broader clinical use and support integration into standard treatment guidelines.

Market Restraints

Gastrointestinal Side Effects and Tolerability Issues Hinder Market Growth

The global market faces a critical restraint as gastrointestinal side effects, such as nausea, vomiting, diarrhea, constipation, and abdominal discomfort, can reduce patient comfort during treatment initiation and dose escalation. When patients experience these side effects, some may delay dose titration, discontinue therapy early, or become less willing to continue long-term treatment, which can limit prescription persistence and overall market expansion. This becomes more important in obesity management, where treatment is often continued for a longer duration, and patient adherence plays a major role in commercial success. As a result, tolerability concerns remain an important factor that can slow broader adoption of semaglutide across some patient groups.

- For example, the FDA-approved Wegovy label states that in adult weight-reduction trials, 73% of Wegovy-treated patients reported gastrointestinal adverse reactions versus 47% on placebo, with severe reactions reported more frequently with Wegovy (4.1%) than placebo (0.9%). The label also notes that severe gastrointestinal adverse reactions have been associated with Wegovy and that it is not recommended in patients with severe gastroparesis.

The semaglutide market faces several constraints related to cost, safety considerations, and supply chain limitations. High treatment costs remain a significant barrier, particularly in emerging markets. Semaglutide-based therapies are priced at a premium, limiting accessibility for uninsured populations and restricting broader semaglutide market growth.

Side effects associated with GLP-1 therapies also present challenges. Common adverse effects, including gastrointestinal discomfort, may affect patient adherence and physician prescribing behavior. Concerns regarding long-term safety and tolerability require ongoing clinical evaluation, influencing adoption rates.

Market Opportunities

Rising Demand for Oral Semaglutide Formulations Presents a Major Market Growth Opportunity

The global market is expected to offer strong growth opportunities for oral formulations, as they can improve treatment convenience and expand the patient base beyond those comfortable with injectable therapies. As more patients and physicians look for easier long-term treatment options for obesity and metabolic disorders, oral semaglutide can support better acceptance, earlier treatment uptake, and wider commercial reach. This is creating a meaningful opportunity for companies to strengthen access across retail, primary care, and broader chronic disease management settings. In addition, oral formulations can help semaglutide penetrate new patient segments where convenience and familiarity of tablet-based treatment play an important role in therapy choice.

- For instance, in January 2026, Novo Nordisk highlighted the FDA approval and launch of the Wegovy pill in the U.S., describing it as the first and only approved once-daily oral GLP-1 medicine for weight management. The company stated that this advancement opens new possibilities for the more than 100 million people in the U.S. living with obesity, indicating strong commercial potential for oral semaglutide and supporting future market expansion.

The semaglutide market presents significant opportunities driven by expanding therapeutic indications and increasing global demand for obesity treatments. The rising prevalence of metabolic disorders is creating a large addressable patient population, supporting long-term semaglutide market growth. Opportunities are particularly strong in chronic weight management, where unmet medical needs remain substantial.

Geographic expansion offers considerable potential. Asia Pacific and Latin America are emerging as high-growth regions due to increasing healthcare access and rising awareness of obesity-related conditions. Regulatory approvals in these regions are enabling broader market entry and expanding the global semaglutide market size.

Development of next-generation formulations represents another key opportunity. Innovations aimed at improving dosing frequency, reducing side effects, and enhancing efficacy are expected to strengthen competitive positioning. Long-acting and combination therapies are under development, offering potential for improved patient outcomes.

Market Challenges

Restricted Access in Lower-Income and Price-Sensitive Markets is Emerging as a Key Challenge for Market

The global market faces a major challenge as high product prices, limited reimbursement support, and uneven market availability are restricting access in lower-income and price-sensitive markets. When affordability remains low, a large share of eligible patients cannot start or continue treatment, reducing prescription volumes and slowing broader market penetration. This challenge is more significant in emerging countries, where healthcare budgets are tighter, and obesity medicines are often not prioritized for public coverage. As a result, even though clinical demand for semaglutide is rising, commercial adoption remains uneven across regions due to access barriers rather than a lack of medical need.

- In December 2025, the WHO issued its global guideline on GLP-1 medicines for obesity and warned that, without deliberate action on manufacturing, affordability, and health-system readiness, access to these therapies could worsen existing health disparities. WHO also stated that, even with rapid production expansion, GLP-1 therapies are projected to reach fewer than 10% of people who could benefit by 2030, underscoring the access challenge that is restraining market expansion in lower-income settings.

Segmentation Analysis

By Product

Ozempic Dominated the Market Due to Its Strong Sales

Based on the product, the market is categorized into Ozempic, Rybelsus, Wegovy, and others.

Ozempic

The Ozempic segment dominated the global semaglutide market share due to higher product sales. Furthermore, it addresses the largest established commercial use of semaglutide, which is type 2 diabetes management. It also benefits from very broad physician familiarity and long-standing global uptake. As the diabetes patient pool is larger and more consistently treated over time, Ozempic generated stronger prescription volumes and revenue contribution than other semaglutide brands. This allowed Ozempic to maintain the leading position within the product segment. The other segment is expected to grow at a CAGR of 47.01% over the forecast period.

- For instance, in December 2024, Novo Nordisk announced that the European Medicines Agency's (EMA) Committee for Medicinal Products for Human Use (CHMP) adopted a positive opinion for an update of the Ozempic label to reflect data from the FLOW kidney outcomes trial. This kind of label expansion strengthens Ozempic's clinical value in diabetes care and supports its continued leadership within the semaglutide product market.

Ozempic represents a leading product within the global semaglutide market, primarily indicated for type 2 diabetes management. It has achieved substantial semaglutide market share due to strong clinical efficacy in glycemic control and secondary benefits in weight loss. Physicians widely prescribe Ozempic as a first-line GLP-1 receptor agonist therapy, supported by extensive FDA approvals and clinical evidence.

Demand continues to rise as healthcare providers increasingly recognize its cardiometabolic benefits. Ozempic contributes significantly to the semaglutide market size and remains a key revenue driver for Novo Nordisk. Its established safety profile and widespread availability reinforce its leadership position within the competitive landscape.

Rybelsus

Rybelsus is the first oral formulation of semaglutide, representing a major innovation in GLP-1 therapies. It addresses patient preference for non-injectable treatments, improving adherence and expanding the addressable population. This product has strengthened the semaglutide market growth by enabling access to patients reluctant to adopt injectable therapies.

The oral formulation is particularly attractive in primary care settings, where ease of administration is critical. While adoption is still scaling compared to injectable products, Rybelsus is gaining traction across developed markets. Its role in diversifying treatment options supports long-term semaglutide market trends toward patient-centric therapy design.

Wegovy

Wegovy is positioned specifically for chronic weight management and obesity treatments, making it a key growth engine within the semaglutide market. Its strong efficacy in weight loss has driven rapid adoption, particularly in markets with high obesity prevalence.

Demand for Wegovy has surged due to increasing awareness of obesity as a medical condition requiring pharmacological intervention. Regulatory approvals have expanded its use, reinforcing its contribution to the semaglutide market size. Supply chain constraints have occasionally limited availability, highlighting the need for capacity expansion.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Higher Prescriptions for Type 2 Diabetes Mellitus Fueled Segmental Dominance

Based on disease indication, the market is segmented into type 2 diabetes mellitus, chronic weight management/obesity, cardiometabolic risk management, and others.

Type 2 Diabetes Mellitus

In 2025, the type 2 diabetes mellitus segment dominated the market. Semaglutide was established and scaled commercially in diabetes treatment before expanding more broadly into obesity and cardiometabolic applications. Since diabetes requires continuous long-term management and has a very large diagnosed patient base globally, demand has remained stronger and more consistent in this indication. This has directly supported higher semaglutide use in diabetes. Regulatory approvals from key authorities further reinforce the segment's growth.

- For instance, in January 2026, Novo Nordisk received approval from Health Canada for RYBELSUS (semaglutide tablets) to reduce the risk of major adverse cardiovascular (CV) events (CV death, non-fatal myocardial infarction, or non-fatal stroke) in adults with type 2 diabetes mellitus who have established cardiovascular disease or are at high risk for these events.

Type 2 diabetes remains the primary indication within the semaglutide market, accounting for a substantial share of total demand. GLP-1 receptor agonist therapies are widely adopted due to their effectiveness in glycemic control and cardiovascular risk reduction. Healthcare providers increasingly prefer semaglutide over traditional therapies due to its dual benefits of glucose regulation and weight loss. This segment continues to drive baseline. The other segment is projected to grow at a CAGR of 42.81% over the forecast period.

Chronic Weight Management/Obesity

Chronic weight management is the fastest-growing segment within the global semaglutide market. Increasing recognition of obesity as a chronic disease is driving demand for effective pharmacological treatments. Semaglutide-based therapies have demonstrated significant weight loss outcomes, positioning them as leading obesity treatments. Adoption is expanding rapidly across developed markets, supported by regulatory approvals and growing patient awareness. This segment is a major contributor to the semaglutide market growth and is expected to reshape overall market dynamics.

Cardiometabolic Risk Management

Semaglutide is increasingly used for cardiometabolic risk reduction, reflecting its broader therapeutic potential. Clinical evidence supporting cardiovascular benefits is driving adoption among high-risk patient populations. This segment represents an emerging growth area, with increasing integration into treatment guidelines. It supports diversification within the semaglutide market and enhances long-term value creation.

By Route of Administration

Presence of Major Product Offerings in the Subcutaneously Administered Semaglutide-Boosted Segmental Growth

Based on the route of administration, the market is segmented into subcutaneous and oral.

Subcutaneous (Prefilled Multi-dose Pens and Prefilled Single-dose Pens)

On the basis of route of administration, the subcutaneous segment dominated the market in 2025. Leading semaglutide brands with the highest commercial uptake, namely Ozempic and Wegovy, are injectable products. Since these products account for a much larger revenue base than oral semaglutide, the injectable route has contributed the majority of the market share.

Subcutaneous administration dominates the semaglutide market, supported by established clinical use and strong efficacy. Prefilled pens offer convenience and precise dosing, enhancing patient compliance. Both multi-dose and single-dose formats are widely used across diabetes and weight management indications. This segment contributes the largest share of the semaglutide market size, driven by physician familiarity and proven outcomes.

Major companies operating in the market are focusing on technologically advanced offerings and the regulatory approvals that accompany them to strengthen their market position.

- For instance, in July 2024, Novo Nordisk announced that the European Medicines Agency’s (EMA) Committee for Medicinal Products for Human Use (CHMP) adopted a positive opinion for an update of the Wegovy (semaglutide 2.4 mg) label to reflect data from the SELECT cardiovascular outcomes trial. It is administered subcutaneously.

Oral

Oral formulation represents a transformative development within the semaglutide market. It offers a non-invasive alternative, improving patient acceptance and expanding treatment accessibility. Although still developing, this segment is expected to gain market share over time. Its growth is supported by increasing demand for convenient treatment options and ongoing innovation in drug delivery systems. The oral segment is projected to grow at a CAGR of 14.65% during the forecast period.

By Type

New Product Launches in the Branded Segment Resulted in Growth

Based on type, the market is segmented into branded and generic/non-originator.

Branded

In 2025, the branded segment dominated the market as Novo Nordisk's originator brands still lead semaglutide commercialization, while generic or non-originator competition remains very limited in regulated major markets. This results in most prescriptions and revenues continuing to flow through branded products such as Ozempic, Rybelsus, and Wegovy. Novo Nordisk is the sole manufacturer of approved, branded semaglutide medicines, reinforcing that the branded segment still holds the clear commercial lead in the market.

- For instance, in December 2025, Emcure Pharmaceuticals announced the commercial launch of Poviztra, a semaglutide injection, across India. With this launch, Emcure becomes the first Indian company to exclusively distribute and commercialize Poviztra, a second brand of Novo Nordisk's semaglutide injection for weight management.

Branded products dominate the global semaglutide market, with Novo Nordisk holding a leading position. Strong intellectual property protection and regulatory approvals support premium pricing and high market share. These products benefit from extensive clinical validation and established trust among healthcare providers. Branded therapies are the primary contributors to the semaglutide market size and revenue generation.

Generic/Non-originator

Generic or non-originator semaglutide products are currently limited due to patent protection. However, future market entry is expected to increase competition and improve accessibility. This segment represents a long-term opportunity, particularly in cost-sensitive markets. As patents expire, generic entry could significantly influence semaglutide market trends and pricing dynamics. The generic/non-originator segment is projected to grow at a CAGR of 66.03% during the forecast period.

By Age

Strong Volume of Patients in the Adults Segment Assisted Segmental Growth

Based on age, the market is segmented into pediatric and adult.

Adults

In 2025, the adult segment dominated the market as the main approved semaglutide uses, especially type 2 diabetes and most obesity and cardiometabolic indications, are primarily targeted toward adult patients. While Wegovy does have a pediatric obesity indication for patients aged 12 years and older, the overall treated population remains much larger in adults, especially through Ozempic and Rybelsus, which are approved for adults with type 2 diabetes. This broader adult treatment base has kept the adult segment clearly ahead in market share.

- For instance, in February 2026, Abbott teamed up with Novo Nordisk India to commercialize Extensior for people living with type 2 diabetes. This alliance leveraged Novo Nordisk's leadership in GLP-1s and Abbott's strong distribution network to increase access in India to a high-quality diabetes therapy. Extensior is a second brand of Ozempic, a GLP-1 RA (receptor agonist)

Adults represent the largest segment within the semaglutide market, driven by the high prevalence of type 2 diabetes and obesity. This group accounts for the majority of prescriptions across all indications. Demand is supported by established treatment guidelines and increasing awareness of metabolic health. The adult segment is the primary contributor to the semaglutide market growth globally.

Pediatric

Pediatric use of semaglutide remains limited but is gradually expanding with evolving clinical evidence and regulatory approvals. This segment focuses on obesity management in younger populations. Adoption is cautious due to safety considerations and regulatory requirements. However, the increasing prevalence of childhood obesity is expected to drive future demand. The pediatric segment is projected to grow at a CAGR of 22.14% in the coming years.

By Distribution Channel

Convenience Offered by Retail Pharmacies for Chronic Disease Management Boosted Segmental Dominance

Based on distribution channel, the market is segmented into retail pharmacies, hospital pharmacies, online pharmacies, specialty pharmacies, and others.

Retail Pharmacies

The retail pharmacies segment dominated the market. Semaglutide is largely used as a long-term outpatient therapy for chronic disease management, which makes routine community-based dispensing more common than hospital-based supply. As more ambulatory care settings prescribe semaglutide for diabetes and obesity management, retail pharmacy networks become the most convenient and scalable channel for repeat dispensing. This has strengthened retail pharmacy share, especially as Novo Nordisk continues to widen access through self-pay, telehealth-linked, and pharmacy-based fulfillment models.

- For instance, in December 2025, BIOCON announced the signing of an out-licensing agreement with Ajanta Pharma Ltd, a specialty pharmaceutical formulations company, to market its vertically integrated drug product, Semaglutide, used to improve glycemic control in adults with type-2 diabetes.

Retail pharmacies account for a significant share of the semaglutide market distribution. These channels provide accessibility for outpatient prescriptions and ongoing treatment. Strong presence in developed markets supports consistent supply and patient access, contributing to the overall market size.

Specialty Pharmacies

The specialty pharmacies segment is projected to grow at a CAGR of 15.45% over the study period. Specialty pharmacies focus on high-value therapies, including semaglutide-based treatments. These providers offer patient support programs and adherence monitoring.

Semaglutide Market Regional Outlook

By geography, the market is divided into North America, Asia Pacific, Latin America, Europe, and the Middle East & Africa.

North America semaglutide Market Analysis

North America Semaglutide Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 21.88 billion and maintained its leading position in 2025 at USD 23.85 billion. The market is growing strongly in North America as obesity and type 2 diabetes cases are high, and awareness of prescription weight-management therapies is rising quickly.

North America leads the global semaglutide market, driven by the high prevalence of type 2 diabetes and the demand for obesity treatments. Strong FDA approvals and favorable reimbursement frameworks support the rapid adoption of GLP-1 receptor agonist therapies. Advanced healthcare infrastructure and awareness of chronic weight management contribute to a significant semaglutide market size. Supply chain investments ensure consistent product availability and sustained semaglutide market growth.

U.S. Semaglutide Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 24.10 billion in 2026, accounting for roughly 61.20% of global revenues. The United States dominates North America’s semaglutide market share, supported by early regulatory approvals and the strong commercial presence of Novo Nordisk. High adoption of semaglutide-based therapies for weight loss and diabetes management drives demand. Insurance coverage expansion enhances accessibility. The market reflects strong growth, driven by increasing obesity prevalence, physician acceptance, and continuous innovation in GLP-1 therapies.

Europe semaglutide Market Analysis

Europe is projected to grow at 12.96 % in the coming years, the second-highest among all regions, and reach a valuation of USD 6.61 billion in 2026. The market is growing in Europe as the region has a large cardiometabolic disease burden and an increasing clinical focus on long-term obesity management, fueling demand.

Europe demonstrates steady semaglutide market growth, supported by regulatory approvals and increasing adoption of GLP-1 therapies. Demand is driven by the rising prevalence of type 2 diabetes and obesity. Healthcare systems emphasize cost-effectiveness and clinical outcomes. Supply chain efficiency and a strong pharmaceutical infrastructure support distribution. The region reflects balanced semaglutide market trends with growing focus on chronic weight management.

U.K. Semaglutide Market

The U.K. market is estimated at around USD 1.32 billion in 2026, representing roughly 3.37% of the global revenues. The United Kingdom semaglutide market is expanding steadily, supported by public healthcare initiatives and increasing awareness of obesity treatments. Regulatory approvals and clinical guidelines are facilitating the adoption of GLP-1 therapies. Demand for chronic weight management solutions is rising. The market reflects moderate growth, driven by healthcare accessibility and evolving treatment protocols within the National Health Service framework.

Germany Semaglutide Market

Germany's market is projected to reach approximately USD 1.11 billion in 2026, equivalent to around 2.81% of the global revenues. Germany is a key contributor to Europe’s semaglutide market, driven by advanced healthcare systems and strong reimbursement policies. Adoption of semaglutide-based therapies is increasing across diabetes and obesity treatments. Physicians emphasize evidence-based prescribing. The market benefits from regulatory clarity and pharmaceutical innovation. Germany supports steady semaglutide market growth through consistent demand and strong healthcare infrastructure.

Asia-Pacific semaglutide Market Analysis

Asia Pacific is estimated to reach USD 4.67 billion in 2026 and secure the position of the third-largest region in the market. The market is growing in the Asia Pacific as diabetes and obesity are increasing rapidly across major countries, creating a stronger demand for effective metabolic disease treatment.

Asia Pacific represents a high-growth region in the global semaglutide market, driven by the rising prevalence of type 2 diabetes and obesity. Expanding healthcare access and increasing awareness of GLP-1 therapies support adoption. Regulatory approvals are progressing across key markets. The region offers significant semaglutide market growth potential, supported by large patient populations and improving pharmaceutical supply chain infrastructure.

Japan Semaglutide Market

The Japanese market in 2026 is estimated at around USD 1.11 billion, accounting for approximately 2.81% of the global revenues. Asia Pacific represents a high-growth region in the global semaglutide market, driven by the rising prevalence of type 2 diabetes and obesity. Expanding healthcare access and increasing awareness of GLP-1 therapies support adoption. Regulatory approvals are progressing across key markets. The region offers significant semaglutide market growth potential, supported by large patient populations and improving pharmaceutical supply chain infrastructure.

China Semaglutide Market

The Chinese market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 1.25 billion, representing approximately 3.18% of global sales. China’s semaglutide market is expanding rapidly, driven by the increasing prevalence of obesity and type 2 diabetes. Growing healthcare access and rising awareness of advanced therapies support adoption. Regulatory approvals are enabling market entry. Domestic and international players are strengthening their presence. The market offers strong growth potential, supported by a large population base and an evolving healthcare infrastructure.

India Semaglutide Market

The Indian market in 2026 is estimated at around USD 0.28 billion, accounting for roughly 0.71% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 1.47 billion in 2026. The region is experiencing market growth, as providers seek more portable, cost-effective imaging solutions to expand access beyond major urban centers. In the Middle East & Africa, the GCC is set to reach USD 0.67 billion in 2026.

Latin America’s semaglutide market is developing steadily, supported by rising awareness of obesity treatments and diabetes management. Increasing healthcare access and regulatory approvals are enabling the adoption of GLP-1 therapies. Cost sensitivity remains a challenge. However, expanding pharmaceutical distribution networks supports gradual semaglutide market growth and increasing market size across key countries in the region.

The Middle East and Africa semaglutide market is growing moderately, driven by the rising prevalence of metabolic disorders and improving healthcare access. Demand for weight management and diabetes treatments is increasing. Regulatory approvals are gradually expanding availability. Market growth is supported by healthcare investments and strengthening pharmaceutical supply chain networks across the region.

South Africa Semaglutide Market

The South African market is projected to reach approximately USD 0.19 billion in 2026, accounting for roughly 0.49% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Emphasize R&D Investments to Boost Market Revenue

The global semaglutide market is highly consolidated, with companies such as Novo Nordisk A/S holding the dominating market share. Other key players in the market include Sun Pharmaceutical Industries Limited, Zydus Lifesciences Limited, and NATCO Pharma Limited. Strategic partnerships, critical regulatory approvals, new product launches, research and development initiatives, and increased investments in the sector are projected to drive these companies' market share gains across the forecast period.

- For instance, in February 2026, Zydus launched generic semaglutide injections in India following its patent expiry in March under the brand names SEMAGLYN, MASHEMA, and ALTERME.

Other prominent participants in the global market include Eris Lifesciences Limited, Hangzhou Jiuyuan Gene Engineering Co., Ltd., and Sandoz AG. They focus on R&D, strategic partnerships, and new product introductions to strengthen their positions.

first-mover advantage and comprehensive portfolio of semaglutide-based therapies. Products such as Ozempic, Rybelsus, and Wegovy have secured significant semaglutide market share, supported by extensive clinical data, multiple FDA approvals, and strong brand recognition. This dominance creates high entry barriers for competitors.

The competitive landscape is evolving as pharmaceutical companies intensify focus on GLP-1 therapies and obesity treatments. Several players are investing in research and development to introduce alternative or next-generation therapies targeting similar metabolic pathways. These efforts aim to capture a portion of the expanding semaglutide market size and challenge Novo Nordisk’s leadership.

Strategic collaborations and partnerships are increasingly shaping market dynamics. Companies are forming alliances to accelerate drug development, enhance clinical trial capabilities, and expand geographic reach. These partnerships also support regulatory approvals across multiple regions, facilitating faster market entry.

Innovation in drug delivery systems is a key competitive factor. Development of oral formulation options and long-acting injectables is improving patient adherence and differentiating product offerings. Companies focusing on reducing side effects and improving efficacy are better positioned to gain market share.

LIST OF KEY SEMAGLUTIDE COMPANIES PROFILED

- Novo Nordisk A/S (Denmark)

- Sun Pharmaceutical Industries Limited (India)

- Zydus Lifesciences Limited (India)

- NATCO Pharma Limited (India)

- Eris Lifesciences Limited (India)

- Hangzhou Jiuyuan Gene Engineering Co., Ltd. (India)

- Sandoz AG (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Novo Nordisk announced a more than USD 451.47 million expansion of its Athlone facility. This investment marked a stronger production infrastructure to support the future supply chain of obesity and diabetes therapies and reduce capacity-related growth constraints.

- January 2026: Novo Nordisk launched Wegovy (semaglutide) as a once-daily oral GLP-1 medicine for weight management in the U.S., becoming the first and only approved once-daily oral GLP-1 medicine for weight management in the U.S. This is a major product launch for the market, as it expands semaglutide beyond injectable formulations and can improve adoption among patients who prefer oral treatment.

- August 2025: Eli Lilly said it is making substantial investments to support the launch of oral GLP-1 candidate orforglipron. In its official release on pivotal obesity trial data, Lilly announced substantial investments to meet anticipated demand at launch for orforglipron, its oral GLP-1 candidate.

- July 2025: Hims & Hers announced a Canada expansion following the ZAVA acquisition, timed with the availability of generic semaglutide.

- April 2025: Novo Nordisk announced an investment of USD 1,209.0 million to expand production facilities in Montes Claros, Brazil, to increase its ability to produce injectable treatments for obesity and other serious chronic diseases.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.27% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Disease Indication, Route of Administration, Type, Age, Distribution Channel, and Region |

| By Product |

|

| By Disease Indication |

|

| By Route of Administration |

|

| By Type |

|

| By Age |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 34.52 billion in 2025 and is projected to reach USD 86.05 billion by 2034.

In 2025, the market value in North America stood at USD 23.85 billion.

The market is expected to grow at a CAGR of 10.27% over the forecast period of 2026-2034.

By product type, the Ozempic segment led the market.

The rising global burden of obesity and type 2 diabetes is driving market growth.

Novo Nordisk, Sun Pharmaceutical Industries Limited, and Zydus Lifesciences Limited are top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us