Semiconductor Capital Equipment Market Size, Share & Industry Analysis, By Equipment Type (Front-End Equipment, Back-End Equipment, and Other Equipment), By End User (IDMs (Integrated Device Manufacturers), Foundries, OSATs (Outsourced Semiconductor Assembly & Test), and Others), and Regional Forecast, 2026 - 2034

Semiconductor Capital Equipment Market Size and Future Outlook

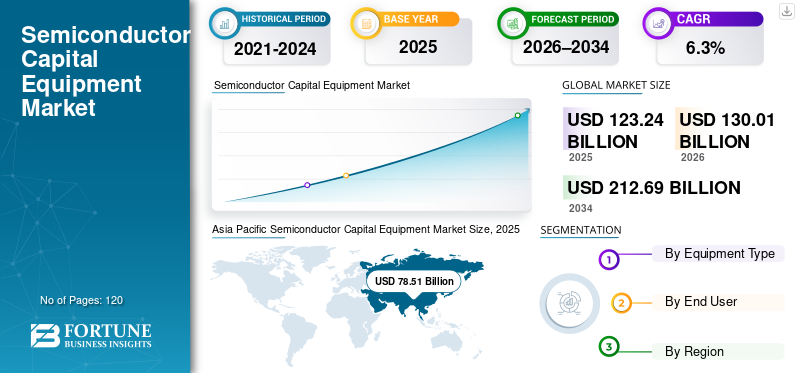

The global semiconductor capital equipment market size was valued at USD 123.24 billion in 2025. The market is projected to grow from USD 130.01 billion in 2026 to USD 212.69 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period. Asia Pacific dominated the semiconductor capital equipment market with a market share of 63.7% in 2025.

Semiconductor capital equipment includes front-end and back-end tools used in wafer fabrication, assembly, packaging, and testing processes. Increasing demand from data center infrastructure and high-performance computing applications is accelerating investments in advanced process technologies and production equipment. The market is experiencing sustained growth, driven by rising investments in semiconductor manufacturing capacity to support expanding applications across consumer electronics, automotive, and industrial sectors. Chipmakers are expanding and upgrading fabrication facilities to meet performance, efficiency, and scalability requirements.

Key industry players such as ASML, Applied Materials, Lam Research, Tokyo Electron, and KLA Corporation continue to drive innovation in lithography, deposition, etching, and inspection systems to support advanced nodes and next-generation semiconductor production.

Download Free sample to learn more about this report.

SEMICONDUCTOR CAPITAL EQUIPMENT MARKET TRENDS

Rising Investments in Advanced Node and Packaging Technologies are a Key Market Trend

Currently, in the semiconductor capital equipment sector, there is a heightened investment trend toward advanced process nodes (i.e., device characteristics used to manufacture next-generation devices) and new advanced packaging technologies. In addition, foundry and integrated device manufacturers will continue to ramp up production capacity to meet increasing demand for logic, memory, AI Accelerators, and High Performance Computing (HPC) chips. The use of multiple applications such as EUV (Extreme Ultra Violet) Lithography, Advanced Deposition and Etching Systems, and Heterogeneous Integration, will continue to evolve equipment purchase patterns in the semiconductor industry. The increased need to diversify geopolitically in semiconductor manufacturing has driven the construction of New Fabs across various inorganic regions, providing an additional driver for maintaining equipment investment rates.

- For example, ASML has indicated continued demand growth for its EUV lithography systems, driven by increased production and demand for both Advanced Logic and Memory manufacturing.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Strong Demand for Semiconductors across AI, Automotive, and Consumer Electronics is Driving Market Growth

The expanding use of semiconductors across artificial intelligence, automotive electronics, 5G infrastructure, and consumer devices is a major driver of the market. Rising chip complexity and performance requirements are pushing manufacturers to invest in next-generation fabrication and testing equipment. Government-backed semiconductor incentive programs and national manufacturing strategies are also accelerating fab expansion and equipment procurement. These factors are driving long-term capital expenditure cycles across both front-end and back-end semiconductor manufacturing.

- For instance, in March 2025, TSMC and Samsung announced multi-year capital investment plans to expand advanced semiconductor manufacturing capacity.

MARKET RESTRAINTS

High Capital Intensity and Cyclical Nature of Semiconductor Investments Restrict Market Stability

The semiconductor capital equipment sector is highly capital-intensive, with cyclical demand patterns serving as major constraints on the industry. The purchase of capital equipment is directly correlated to semiconductor pricing cycles, inventory corrections, and macroeconomic conditions. When supply is overly high or end-market demand is weak, chip manufacturers delay or cut back on capital spending for equipment. Furthermore, due to the high cost of advanced equipment (e.g., EUV lithography systems), only a small number of large manufacturers adopt this type of equipment. The result is a volatile revenue stream for the suppliers of equipment within this sector. For example, periods of semiconductor inventory correction have historically led to short-term reductions in equipment spending.

MARKET OPPORTUNITIES

Expansion of Advanced Packaging and Regional Fab Localization Creates Growth Opportunities

The increasing demand for advanced packaging technologies such as 2.5D and 3D integration is creating new opportunities for semiconductor capital equipment market growth. Chiplet-based architectures and heterogeneous integration are driving increased demand for assembly, packaging, and testing equipment. In parallel, regional semiconductor manufacturing initiatives in North America, Europe, and Asia are opening opportunities for equipment suppliers to support new fab construction and localization efforts. These developments are expected to support sustained equipment demand over the long term.

- For example, Applied Materials has expanded its portfolio to address advanced packaging and materials engineering requirements.

Segmentation Analysis

By Equipment Type

Front-End Equipment Held Largest Share, Driven by Advanced Node and Capacity Expansion Investments

Based on the equipment type, the market is divided into front-end equipment, back-end equipment, and other equipment.

In 2025, the front-end equipment segment accounted for the highest semiconductor capital equipment market share. Front-end equipment includes lithography, etching, deposition, and cleaning tools essential to wafer fabrication. Increasing investments in advanced logic and memory nodes, along with capacity expansion by leading semiconductor manufacturers, are driving sustained demand for front-end tools. The increasing complexity of chip designs and the transition toward smaller process nodes further reinforce the dominance of front-end equipment in overall capital spending.

- For example, ASML has reported continued growth in demand for EUV lithography systems as chipmakers expand advanced manufacturing capacity.

The back-end equipment segment is anticipated to rise with a CAGR of 6.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Integrated Device Manufacturers Led Capital Spending Due to Vertically Integrated Operations

Based on the end user, the market is segmented into IDMs (integrated device manufacturers), foundries, OSATs (outsourced semiconductor assembly & test), and others.

In 2025, the IDMs (integrated device manufacturers) segment held the highest market share. IDMs manage both chip design and manufacturing in-house, resulting in large, consistent capital expenditures across front-end and back-end production processes. These companies invest heavily in upgrading fabrication facilities to support advanced technologies, improve yield, and enhance production efficiency. Continued demand for semiconductors across automotive, industrial, and consumer electronics applications supports sustained capital investment by IDMs.

- For example, Intel has announced long-term investments to expand semiconductor manufacturing capacity and modernize fabrication facilities.

The foundries segment is projected to grow at a CAGR of 6.9% over the forecast period.

Semiconductor Capital Equipment Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Semiconductor Capital Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held a dominant position in the market in 2024 and maintained its leading share in 2025, with a market valuation of USD 78.51 billion. The region’s market growth is supported by the strong concentration of semiconductor manufacturing facilities, extensive investments in new fabs, and leadership in advanced logic and memory production. Countries such as China, South Korea, and Japan account for a significant portion of global semiconductor fabrication capacity, driving sustained demand for front-end and back-end equipment.

Japan Semiconductor Capital Equipment Market

The Japan market in 2026 is estimated at around USD 11.20 billion, accounting for roughly 8.6% of global revenue.

China Semiconductor Capital Equipment Market

The China market in 2026 is estimated at around USD 29.75 billion, accounting for roughly 22.9% of the global market.

India Semiconductor Capital Equipment Market

The India market in 2026 is estimated at around USD 3.48 billion, accounting for roughly 2.7% of the global market.

North America

North America is expected to reach a market valuation of USD 26.87 billion by 2026, making it one of the fastest-growing regions in the market. Renewed investments in domestic semiconductor manufacturing and advanced technology development drive the market. The region benefits from the presence of leading integrated equipment manufacturers and equipment suppliers, as well as strong government-backed incentives to strengthen local chip production.

U.S. Semiconductor Capital Equipment Market

The U.S. market in 2026 is estimated at USD 24.26 billion, accounting for roughly 18.7% of global revenues. The U.S. market continues to benefit from large-scale fab construction projects and the modernization of existing facilities, positioning it as a key contributor to global equipment spending.

Europe

Europe is expected to record a market valuation of USD 13.51 billion in 2026. The region is witnessing steady market growth, supported by strategic initiatives to enhance regional semiconductor self-sufficiency. Investments in automotive semiconductors, power electronics, and industrial chips are driving demand for fabrication and testing equipment. Various countries play a critical role in supporting equipment demand through their strong automotive and industrial electronics manufacturing bases.

U.K. Semiconductor Capital Equipment Market

The U.K. market in 2026 is estimated at around USD 1.80 billion, representing roughly 1.4% of global revenues.

Germany Semiconductor Capital Equipment Market

Germany’s market is projected to reach USD 3.39 billion in 2026, equivalent to around 2.6% of global sales.

South America and Middle East & Africa

The South America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. South America is projected to reach a market valuation of USD 2.81 billion in 2026. Market growth in the region is supported by the gradual expansion of electronics manufacturing and assembly activities, as well as increased interest in semiconductor testing and packaging. The Middle East & Africa market is expected to reach USD 3.83 billion in 2026. Regional initiatives focused on technology diversification, electronics manufacturing, and industrial development are supporting emerging demand for semiconductor manufacturing and testing equipment, particularly within GCC countries.

GCC Semiconductor Capital Equipment Market

The GCC market is projected to reach around USD 1.55 billion in 2026, representing roughly 1.2% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Advanced Process Technologies and Capacity Expansion to Strengthen Market Positions

The semiconductor capital equipment market is highly concentrated, with a limited number of companies accounting for a large share of overall equipment sales volume. The top global suppliers (ASML, Applied Materials, Lam Research, Tokyo Electron, and KLA Corporation) control most of the supply, as they have established technological capabilities, the largest installed customer base, and strong relationships with leading semiconductor manufacturers. These companies provide the key enablers for producing advanced logic, memory, and foundry products through their continued innovation in lithography, deposition, etching, and inspection technologies. The competitive strategies of leading suppliers are to continue developing new process nodes, support heterogeneous integration, and optimize yield while expanding their global support capabilities for customers. Additionally, their long-term supply agreements, co-development programs with chip manufacturers, and investments in next-generation equipment platforms are part of their competitive strategy in the future.

LIST OF KEY SEMICONDUCTOR CAPITAL EQUIPMENT COMPANIES PROFILED

- Advantest (Japan)

- Applied Materials (U.S.)

- ASM International (Netherlands)

- ASML (Netherlands)

- Hitachi High-Tech (Japan)

- KLA Corporation (U.S.)

- Lam Research (U.S.)

- SCREEN Holdings (Japan)

- Teradyne (U.S.)

- Tokyo Electron (Japan)

KEY INDUSTRY DEVELOPMENTS

- January 2026: ASML reported record quarterly orders of about USD 15.70 billion for advanced lithography capital equipment, reflecting strong global demand as semiconductor fabs expand capacity for high-performance chips.

- December 2025: NY Creates and Japanese semiconductor equipment maker SCREEN agreed to a 10-year, USD 75 million research collaboration focused on advancing chipmaking technologies, including wet-etch and high-NA EUV lithography.

- September 2025: ASML invested USD 1.5 billion in French AI startup Mistral AI and formed a strategic partnership to integrate AI into chipmaking tools and R&D, strengthening semiconductor equipment innovation.

- August 2025: Applied Materials formed a strategic partnership with Apple and Texas Instruments to supply U.S.-made semiconductor equipment and to invest in a new Arizona facility, strengthening domestic chipmaking capacity and advancing the deployment of advanced tools.

- April 2025: Applied Materials acquired a 9% stake in BE Semiconductor Industries to co-develop the industry’s first fully integrated hybrid bonding equipment solution, boosting advanced packaging

- March 2025: ASML and IMEC signed a five-year strategic partnership agreement to support semiconductor research and sustainable innovation in Europe, combining expertise in advanced chipmaking technologies.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.3% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Equipment Type, End User, and Region |

|

By Equipment Type |

|

|

By End User |

|

|

By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 123.24 billion in 2025 and is projected to reach USD 212.69 billion by 2034.

In 2026, the market value of North America will reach USD 26.87 billion.

The market is expected to exhibit a CAGR of 6.3% during the forecast period of 2026-2034.

By equipment type, the front-end equipment segment led the market.

The market is driven by strong demand for advanced chips across AI, automotive, 5G, and consumer electronics, along with government support for semiconductor manufacturing expansion.

ASML, Applied Materials, Lam Research, Tokyo Electron, and KLA Corporation are the major players in the global market.

Asia Pacific dominated the market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us