Semiconductor Memory Market Size, Share & Industry Analysis, By Type (SRAM, MRAM, DRAM, Flash ROM (NAND Flash and NOR Flash), and Others), By End-Use (Consumer Electronics, IT & Telecommunication, Automotive, Healthcare, Aerospace & Defense, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

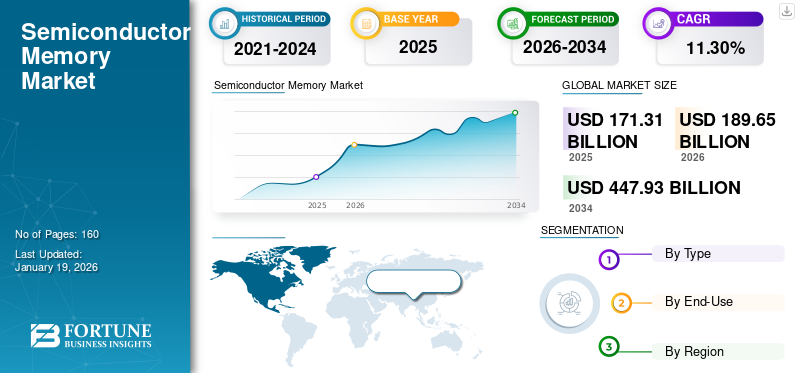

The global semiconductor memory market size was valued at USD 171.31 billion in 2025 and is projected to grow from USD 189.65 billion in 2026 to USD 447.93 billion by 2034, exhibiting a CAGR of 11.30% during the forecast period. The Asia Pacific dominated the global market with a share of 40.50% in 2025. The industry growth is driven by AI-driven data demand, advanced computing workloads, and next-generation storage technologies across key industries.

Semiconductor memory is a type of semiconductor device tasked with storing data. It functions as computer memory/chips by employing Integrated Circuit (IC) technology. These memory types are classified according to the kind of data storage and access techniques offered, including non-volatile ROM and volatile RAM.

Factors, including the growing usage of technologies, including AI, cloud computing, and big data, and rising sales of high-bandwidth memories, drive the growth of this market. TechInsights anticipates HBM shipments to increase 70% YoY in 2025. The increasing popularity of smartphones, tablets, laptops, and other portable gadgets has significantly elevated the need for semiconductor memory. Moreover, the transition to 3D NAND technology is also a key trend for market growth.

The semiconductor memory market is entering a structurally transformative phase, driven by exponential data generation, artificial intelligence workloads, and the expansion of high-performance computing ecosystems. Memory technologies are no longer viewed as commoditized components; instead, they represent a strategic enabler for performance differentiation across industries. This shift is redefining both market positioning and capital allocation strategies among leading semiconductor manufacturers.

The semiconductor memory market size continues to expand in alignment with demand from data centers, consumer electronics, and automotive electronics. Hyperscale cloud providers and AI infrastructure investments are materially increasing demand for high-bandwidth memory and advanced DRAM architectures. NAND flash demand is similarly expanding, supported by storage-intensive applications such as edge computing, video streaming, and enterprise data management.

The semiconductor memory market growth trajectory is closely tied to capital intensity and technology transitions. Leading players continue to invest heavily in fabrication capacity, particularly in advanced nodes such as 3D NAND and next-generation DRAM. These investments are essential to maintain competitiveness but also introduce supply-side volatility. At the same time, diversification of end-use applications is stabilizing demand cycles. Automotive, industrial automation, and AI-driven applications are reducing reliance on traditional consumer electronics cycles.

The major players included in this market are Samsung Electronics Co., Ltd., Micron Technology, Inc., SK Hynix Inc., Intel Corporation, Toshiba Corporation, Western Digital Corporation, Kingston Technology Company, Inc., Infineon Technologies AG, Renesas Electronics Corporation, and Advanced Micro Devices, Inc.

Download Free sample to learn more about this report.

Semiconductor Memory Market Key Takeaways

- 2025 Market Size: USD 171.31 billion

- 2026 Market Size: USD 189.65 billion

- 2034 Forecast Market Size: USD 447.93 billion

- CAGR: 11.30% from 2026–2034

- Asia Pacific dominated the semiconductor memory market with a 40.50% share in 2025.

- The DRAM segment is projected to lead the market with a 30.81% share in 2026.

- The consumer electronics segment is anticipated to dominate with a 27.72% share in 2026.

Asia Pacific

Asia Pacific generated USD 69.4 billion in 2025, supported by strong semiconductor manufacturing, consumer electronics production, and data center investments.

North America

North America generated USD 53.47 billion in 2025 and is projected to reach USD 59.95 billion in 2026, driven by cloud services and data center expansion.

Europe

Europe accounted for 17.30% of global demand in 2025 and is projected to reach USD 32.74 billion in 2026.

U.S.

The semiconductor memory market is projected to reach USD 43.83 billion by 2026, fueled by AI workloads, cloud infrastructure, and high-performance computing demand.

Japan

The semiconductor memory market is projected to reach USD 16.98 billion by 2026, supported by strengths in materials, equipment, automotive electronics, and industrial applications.

Read More

CURRENT EVENTS AND THEIR IMPACT ON THE MARKET

|

Event |

Description |

|

Impact of Reciprocal Tariffs |

The supply chain of memory is complex and requires specific materials, including silicon wafers, specialized gases, and photoresists, as well as sophisticated equipment such as lithography and etching tools, in addition to back-end assembly operations that are scattered throughout the U.S., South Korea, Taiwan, Japan, and China. With each handoff, the additional cost of taxes applied at each location is heavy, with inflated tariff costs. Moreover, data centers, the largest consumers of DRAM and NAND, may face increased TCO (total cost of ownership), leading to deferred investments. |

|

Impact of Generative AI |

Generative AI is revolutionizing the semiconductor memory sector by generating demand for SRAM, advanced DRAM, and NAND, which is resulting in increased average selling prices, speeding up innovation in memory designs, and altering relationships between suppliers and GPUs. This trend is expected to support a prolonged growth phase and change the landscape of competitive positioning. According to an industry analyst's estimates, DRAM demand for gen-AI by 2030 is expected to be between 5 and 13 million wafers (DRAM-light scenario) or 7 and 21 million wafers (DRAM-base scenario). |

|

Memory Technology Transition and Innovation Race |

Each quarter, the uptake of DDR5 referrals is accelerating, and demand is increasing for both data center and consumer electronics. As an example, in early January 2025, Samsung's DDR5 DRAM referrals surged from cloud data centers, while some of the smaller suppliers are experiencing an oversupply of DDR4 inventory. |

Key Market Dynamics

Semiconductor Memory Market Trends

Transition to 3D NAND Technology to Emerge as a Key Market Trend

Standard 2D NAND memory technology is being replaced by 3D NAND that uses a three-dimensional assembly and architecture to more efficiently organize memory cells in one or more layers to maximize data storage density and efficiency by utilizing existing space effectively. 3D NAND consumes minimum power and costs less to manufacture. 3D NAND also has the benefit of scalability that can accommodate more data storage capacity, while also providing more performance speed, and is rapidly emerging as the dominant implant for SSDs and smartphones. For instance, in July 2023, NEO Semiconductor announced the commercialization of its 3D X-DRAM technologies.

The semiconductor memory market is increasingly shaped by structural demand shifts rather than purely cyclical supply dynamics. The emergence of artificial intelligence, machine learning, and data-intensive applications is fundamentally altering memory architecture requirements. High-bandwidth memory (HBM) and advanced DRAM configurations are becoming critical components in AI accelerators and high-performance computing systems.

One of the most defining semiconductor memory market trends is the transition toward higher-density and vertically stacked memory architectures. NAND flash technology has evolved significantly with the adoption of 3D NAND, enabling greater storage capacity within constrained physical footprints. This transition improves cost efficiency per bit while supporting large-scale data storage requirements.

Another important trend is the growing role of automotive applications. Advanced driver-assistance systems (ADAS), autonomous driving platforms, and in-vehicle infotainment systems require significant memory capacity and reliability. This segment is becoming a stable demand contributor. Additionally, supply discipline among major manufacturers has improved compared to previous cycles. Companies are aligning production with demand forecasts more cautiously, reducing extreme price volatility.

Semiconductor Memory Market Growth Factors

Growing Demand in Data Centers and Cloud Computing to Aid Market Growth

The rapid growth in data production driven by big data, AI, and the Internet of Things (IoT) has heightened the need for high-performance memory solutions. In order to enable the storage and management of large amounts of data, data centers require a substantial amount of dynamic random-access memory (DRAM) and non-volatile memory. WifiTalents recently noted that an estimated 8 million data centers exist globally. These factors collectively contribute to the semiconductor memory market growth.

The semiconductor memory market growth is driven by a combination of technological evolution and expanding data consumption across industries. The proliferation of connected devices, cloud computing, and artificial intelligence workloads continues to increase demand for both volatile and non-volatile memory solutions. Data center expansion remains a primary growth catalyst. Hyperscale operators are investing heavily in infrastructure to support AI training, real-time analytics, and large-scale storage. These workloads require high-performance memory with low latency and high throughput, significantly boosting demand for DRAM and advanced memory technologies.

Consumer electronics also contribute to sustained demand. Smartphones, gaming devices, and personal computing systems continue to require higher memory capacities to support advanced functionalities. While growth rates in this segment are moderating, unit volumes remain substantial. Another significant factor is technological innovation. Continuous advancements in memory density, speed, and energy efficiency enable new applications and improve system performance. This innovation cycle supports long-term semiconductor memory market growth.

Additionally, geopolitical considerations and supply chain resilience strategies are influencing investment decisions. Governments and corporations are prioritizing domestic semiconductor manufacturing capabilities, which indirectly supports memory production capacity expansion.

Market Restraints

Scaling Limitations and Enhancement-Related Issues to Hinder Market Expansion

One critical concern is the physical limitation of enhancing semiconductor memory. Producers are striving for higher density and smaller chip sizes, which brings up issues related to data integrity and reliability. Decreasing the number of memory cells leads to higher leakage currents and reduced retention times, especially for DRAM and NAND flash.

Despite strong demand fundamentals, the semiconductor memory market faces several structural constraints that influence profitability and investment cycles. One of the most significant challenges is the inherent cyclicality of pricing. Memory markets historically experience periods of oversupply followed by sharp price corrections, impacting revenue stability.

Capital intensity represents another major barrier. Semiconductor memory manufacturing requires substantial investment in fabrication facilities, equipment, and research and development. These high capital requirements limit market entry and concentrate production among a few large players.

Technological complexity also poses challenges. As memory technologies scale to smaller nodes and higher densities, manufacturing processes become increasingly complex. Yield management and defect control are critical factors that directly affect profitability. Additionally, geopolitical tensions and trade restrictions are influencing the semiconductor ecosystem. Export controls and regional policy interventions can disrupt supply chains and limit access to advanced technologies.

Market Opportunities

Rise in Adoption of Nonvolatile Memory (NVM) Technologies to Create Lucrative Market Opportunities

Non-volatile memory types, including MRAM (Magneto resistive RAM) and ReRAM (Resistive RAM), are increasingly favored as they can retain data without requiring power. These technologies surpass traditional memory types such as DRAM in speed, endurance, and energy efficiency. NVM technologies are particularly beneficial in automotive, industrial, and IoT applications where energy efficiency and data integrity are essential.

The semiconductor memory market presents significant opportunities driven by structural shifts in computing paradigms and digital infrastructure. One of the most compelling opportunities lies in artificial intelligence and high-performance computing. These applications require advanced memory architectures capable of handling large datasets with minimal latency.

High-bandwidth memory (HBM) represents a particularly strong opportunity segment. Its integration with AI processors and graphics processing units enables faster data transfer and improved computational efficiency. Demand for HBM is expected to grow as AI workloads become more complex and widespread. Automotive electronics offer another high-growth avenue. As vehicles become more software-driven, memory requirements increase significantly. This trend supports long-term demand stability beyond traditional consumer markets.

Emerging memory technologies also present opportunities for differentiation. Magnetoresistive random-access memory (MRAM) and resistive random-access memory (ReRAM) offer advantages in speed, endurance, and energy efficiency. While still in early stages, these technologies could reshape the competitive landscape.

SEGMENTATION ANALYSIS

By Type

Demand for Powerful Computing Systems and Exceptional Features Boosted the Expansion of the DRAM Segment

Based on type, the market is segmented into SRAM, MRAM, DRAM, Flash ROM (NAND Flash and NOR Flash), and others.

DRAM (Dynamic Random-Access Memory)

By type, the DRAM segment dominated with the largest semiconductor memory market share in 2024. The segment is expected to lead with a 30.81% share in 2026. DRAM plays a crucial part in the memory industry due to its exceptional data retrieval speed and high responsiveness. Other trends are also developing and influencing the DRAM segment due to continuous improvements in technology, escalating demand for high-performance computing platforms, and data-centric applications in the cloud.

Dynamic random-access memory (DRAM) remains a cornerstone of the semiconductor memory industry, accounting for a substantial portion of global revenue. DRAM is widely used in computing systems, data centers, and mobile devices due to its balance between performance and cost.

Technological advancements such as DDR5 and high-bandwidth memory (HBM) are enhancing DRAM performance. These innovations support high-throughput applications, particularly in AI and high-performance computing. DRAM pricing remains cyclical, influenced by supply-demand imbalances. Despite this, DRAM continues to dominate the semiconductor memory market share due to its broad applicability.

SRAM (Static Random-Access Memory)

The SRAM segment will achieve the highest compound annual growth rate (CAGR) of 13.36% during the forecast period due to increasing demand for memory in AI/data centers (high bandwidth, speed). Static random-access memory (SRAM) occupies a specialized but critical role within the semiconductor memory market. It is primarily used in cache memory for processors, where speed and low latency are essential. Unlike DRAM, SRAM does not require periodic refreshing, enabling faster access times.

SRAM demand is closely tied to processor performance advancements. As central processing units (CPUs) and graphics processing units (GPUs) become more powerful, the need for larger and faster cache memory increases. This dynamic sustains SRAM demand despite its higher cost structure. While SRAM does not dominate the semiconductor memory market size, its strategic importance in high-performance computing ensures stable demand growth.

MRAM (Magnetoresistive Random-Access Memory)

Magnetoresistive random-access memory (MRAM) represents an emerging segment with significant long-term potential. MRAM combines the speed of SRAM with the non-volatility of flash memory, offering a unique value proposition. MRAM is gaining traction in embedded systems, industrial applications, and automotive electronics. These sectors prioritize reliability, durability, and energy efficiency, making MRAM an attractive alternative.

However, cost constraints and scalability challenges currently limit widespread adoption. As manufacturing processes mature, MRAM is expected to capture a larger share of the semiconductor memory market.

Flash ROM (NAND Flash and NOR Flash)

Flash memory, particularly NAND flash, represents a major segment within the semiconductor memory market. NAND flash is widely used for data storage in consumer electronics, enterprise storage systems, and mobile devices. NOR flash, while smaller in market share, is used in applications requiring fast read speeds and reliable code storage, such as embedded systems and automotive electronics.

The transition to 3D NAND has significantly increased storage capacity and reduced costs. This evolution supports the growing demand for data-intensive applications. Flash memory remains a key contributor to semiconductor memory market growth, particularly in storage-driven applications.

By End-Use

Consumer Electronics Dominated Due to Increasing Need for Data Requirements and Enhanced Memory Architectures

Based on the end-use, the market is categorized into consumer electronics, IT & telecommunication, automotive, healthcare, aerospace & defense, and others.

Consumer Electronics

The consumer electronics segment was leading in 2024. In 2026, the segment is anticipated to dominate with a 27.72% share. In the dynamic world of the consumer electronics industry, the need for memory solutions that can accommodate the growing data requirements is crucial. The ongoing progress, marked by the launch of higher-density chips and enhanced memory architectures, has been pivotal in satisfying these rising demands.

Consumer electronics remain a foundational segment within the semiconductor memory market. Devices such as smartphones, laptops, gaming consoles, and wearable technology require substantial memory capacity to support advanced functionalities. Although growth rates are moderating, the segment continues to contribute significantly to the semiconductor memory market size due to its scale.

IT & Telecommunication

The IT and telecommunication segment represents one of the fastest-growing areas within the semiconductor memory market. Data centers, cloud infrastructure, and networking equipment require high-performance memory solutions. This segment is less sensitive to consumer cycles and provides more stable demand. High-bandwidth memory and advanced DRAM solutions are particularly relevant in this context.

Automotive

The automotive segment is emerging as a critical growth driver within the semiconductor memory market. Modern vehicles incorporate advanced electronics, requiring significant memory capacity. Memory requirements in vehicles are increasing rapidly, driven by software complexity and data processing needs. This trend supports long-term semiconductor memory market growth.

Healthcare

Healthcare applications are increasingly utilizing semiconductor memory in medical imaging, diagnostics, and patient monitoring systems. These applications require reliable and high-performance memory solutions. While smaller in market share, healthcare represents a stable and high-value segment.

The healthcare sector is most likely to see the highest CAGR of 14.96% during the forecast period through increasing demand for high-speed, high-capacity memory in medical imaging, diagnostics, remote monitoring, and AI-powered analytics. Moreover, wearables and home healthcare devices push the adoption of low-power, reliable SRAM, DRAM, and non-volatile memory.

Aerospace & Defense

The aerospace and defense segment demands highly reliable and durable memory solutions capable of operating in extreme environments. Applications include avionics, satellite systems, and defense electronics. This segment prioritizes performance and reliability over cost, making it less sensitive to pricing cycles.

To know how our report can help streamline your business, Speak to Analyst

Regional Insights

By region, the market is divided into North America, Europe, South America, the Middle East & Africa, and Asia Pacific.

Asia-Pacific Semiconductor Memory Market Analysis

Asia Pacific Semiconductor Memory Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 40.50% of the global market in 2025, generating USD 69.4 billion in revenue, and is projected to reach USD 76.61 billion in 2026. This is due to rising investments in data centers in countries such as Singapore, India, and Indonesia, which are driving significant demand for semiconductor memory in the area. Furthermore, emerging economies in the region, including China, India, and Japan, are contributing to market growth for a variety of reasons, such as rising production of consumer electronics and memory chips, increasing adoption of high-tech devices, and expanding digitization efforts.

As reported by the Japan Electronics and Information Technology Industries Association (JEITA), the overall output of the Japan market is projected to reach USD 16.98 billion by 2026, the China market is projected to reach USD 27.85 billion by 2026, and the India market is projected to reach USD 10.51 billion by 2026.

Asia-Pacific dominates the global semiconductor memory market in both production and consumption. The region hosts major fabrication facilities and leading manufacturers. Demand is driven by consumer electronics, data centers, and industrial applications. Government support and investment in semiconductor infrastructure reinforce regional leadership. The concentration of supply chains, however, introduces geopolitical and operational risks that influence global market dynamics.

Japan Semiconductor Memory Market

Japan maintains a strong position in the semiconductor memory ecosystem, particularly in materials, equipment, and specialized memory technologies. Demand is supported by automotive electronics and industrial applications. The country focuses on technological innovation and supply chain integration. Strategic collaborations and government initiatives aim to strengthen domestic semiconductor capabilities, enhancing resilience within the broader semiconductor memory market.

China Semiconductor Memory Market

China represents a rapidly evolving semiconductor memory market, driven by domestic demand and strategic investment in local manufacturing capabilities. Government initiatives prioritize self-sufficiency in semiconductor production. Demand is concentrated in consumer electronics, telecommunications, and data infrastructure. While technological gaps remain, ongoing investment and policy support are expected to strengthen China’s position within the global semiconductor memory industry.

Download Free sample to learn more about this report.

North America Semiconductor Memory Market Analysis

North America contributed approximately USD 53.47 billion to the global market in 2025, accounting for 31.20% share, and is expected to reach USD 59.95 billion in 2026. The region's expansion is driven by increasing use of cloud services and the setup of data centers, which generates a demand for advanced semiconductor chip solutions that can manage large amounts of data produced and handled. Backed by these factors, countries including the US market are projected to reach USD 43.83 billion by 2026, and Canada is projected to record USD 9.65 billion in 2025.

North America represents a strategically significant semiconductor memory market, driven by strong demand from data centers, AI infrastructure, and enterprise computing. The region benefits from advanced technological ecosystems and substantial investment in semiconductor manufacturing. Hyperscale cloud providers are key demand drivers. Government initiatives supporting domestic semiconductor production further strengthen supply chain resilience and long-term competitiveness within the semiconductor memory industry.

United States Semiconductor Memory Market

The United States dominates regional demand, supported by leading technology companies and hyperscale data center operators. Semiconductor memory consumption is concentrated in AI workloads, cloud infrastructure, and high-performance computing. Federal incentives promoting domestic semiconductor manufacturing are accelerating capacity expansion. However, reliance on global supply chains persists, requiring strategic diversification to mitigate geopolitical risks and ensure long-term stability within the semiconductor memory market.

To know how our report can help streamline your business, Speak to Analyst

Europe Semiconductor Memory Market Analysis

In 2025, the Europe market stood at USD 29.64 billion, representing 17.30% of global demand, and is projected to grow to USD 32.74 billion in 2026. The market is expanding swiftly, fueled by the rise of electric vehicles, the rollout of 5G, and the integration of Industry 4.0 and IoT technologies. Initiatives from the government, such as the EU Chips Act and efforts toward digital sovereignty, are also enhancing regional investment and manufacturing capabilities. The UK market is projected to reach USD 6.96 billion by 2026, while the German market is projected to reach USD 6.38 billion by 2026.

Europe demonstrates steady growth in the semiconductor memory market, supported by industrial automation, automotive electronics, and data infrastructure development. The region emphasizes technological sovereignty and supply chain resilience. Demand is driven by advanced manufacturing and digital transformation initiatives. However, limited large-scale fabrication capacity constrains regional production, increasing reliance on imports despite ongoing investments in semiconductor ecosystem development.

Germany Semiconductor Memory Market

Germany leads the European semiconductor memory market, driven by its strong automotive and industrial base. Memory demand is closely tied to advanced driver-assistance systems, industrial automation, and manufacturing digitization. Government initiatives supporting semiconductor investments are enhancing domestic capabilities. However, dependence on external suppliers remains a structural limitation, influencing strategic partnerships and long-term supply chain planning within the semiconductor memory industry.

United Kingdom Semiconductor Memory Market

The United Kingdom semiconductor memory market is characterized by demand from data centers, telecommunications, and advanced research applications. The country focuses on design and innovation rather than large-scale manufacturing. Memory consumption is supported by cloud computing expansion and digital infrastructure development. Policy efforts to strengthen semiconductor capabilities are emerging, though limited fabrication capacity constrains full ecosystem integration.

Latin America Semiconductor Memory Market Analysis

Latin America recorded a market size of USD 6.52 billion in 2025, capturing 3.80% of the global market share, and is projected to reach USD 7.04 billion in 2026. Latin America presents emerging opportunities within the semiconductor memory market, primarily driven by increasing digital adoption and telecommunications expansion. Demand remains relatively limited compared to developed regions. Infrastructure constraints and limited manufacturing capabilities influence market development. However, gradual growth in data centers and enterprise computing is expected to support incremental demand over the medium term. The South America market in 2025 is set to record USD 6.52 billion as its valuation. The region is experiencing expanding prospects fueled by rising investments in semiconductor production capabilities and memory systems.

Middle East & Africa Semiconductor Memory Market Analysis

In 2025, Middle East & Africa generated USD 12.27 billion, contributing 7.20% to global market revenue, and is projected to grow to USD 13.31 billion in 2026. The Middle East and Africa semiconductor memory market is at an early stage of development, with demand driven by digital infrastructure and telecommunications growth. Investment in data centers is increasing, particularly in Gulf countries. However, limited local manufacturing and reliance on imports constrain market expansion, requiring continued infrastructure and ecosystem development. Over the forecast period, the Middle East & Africa regions would witness a moderate growth in this market. In the Middle East & Africa, GCC is set to attain the value of USD 4.84 billion in 2025.

Competitive Landscape

KEY INDUSTRY PLAYERS

Notable Players to Implement Strategic Strategies to Expand Business Reach

Key players present in this market are offering innovative semiconductor memory to provide users with fast, energy-efficient, and reliable data storage and retrieval. They concentrate on holding contracts with small and local businesses to grow their business. Moreover, such mergers & acquisitions, partnerships, and investments will create a surge in demand for this technology.

The semiconductor memory market is highly consolidated, with a limited number of global players controlling a significant share of production capacity and technological innovation. Market leadership is defined by advanced fabrication capabilities, process node leadership, and the ability to scale production efficiently across multiple memory types.

Leading companies maintain strong positions through continuous capital investment and technology differentiation. These firms operate integrated business models, encompassing design, fabrication, and advanced packaging. Their competitive advantage is reinforced by high entry barriers, including capital intensity, intellectual property requirements, and manufacturing complexity.

Competition is particularly intense in DRAM and NAND flash segments, where pricing cycles influence profitability. Market leaders actively manage production output to mitigate price volatility while maintaining long-term customer relationships with hyperscale cloud providers and enterprise clients.

Niche players and emerging companies focus on specialized memory technologies such as MRAM, ReRAM, and other non-volatile memory solutions. These firms aim to address specific application requirements, including low power consumption, high endurance, and embedded system integration. While their market share remains limited, they contribute to technological diversification.

Strategic partnerships are increasingly important. Memory manufacturers collaborate with processor designers, cloud providers, and system integrators to optimize performance and ensure compatibility with evolving computing architectures. These collaborations enhance ecosystem integration and accelerate the adoption of advanced memory solutions.

List of Key Semiconductor Memory Companies Studied (including but not limited to):

- Samsung Electronics Co., Ltd.(South Korea)

- Micron Technology, Inc. (U.S.)

- SK Hynix Inc. (South Korea)

- Intel Corporation (U.S.)

- Toshiba Corporation (Japan)

- Western Digital Corporation (U.S.)

- Kingston Technology Company, Inc. (U.S.)

- Infineon Technologies AG(Germany)

- Renesas Electronics Corporation (Japan)

- Advanced Micro Devices, Inc. (U.S.)

- Powerchip Technology Corporation (Taiwan)

- Etron Technology, Inc. (Taiwan)

- Nanya Technology Corporation (Taiwan)

- Fujitsu Limited (Japan)

- Macronix International Co., Ltd. (Taiwan)

- Winbond Electronics Corporation (Taiwan)

- Weebit Nano (Israel)

- Microchip Technology Inc. (U.S.)

- ROHM Semiconductor (Japan)

- Shanghai Huali Microelectronics Corporation (HLMC) (China)

KEY INDUSTRY DEVELOPMENTS:

- August 2025: NEO Semiconductor introduced a new Extreme High Bandwidth Memory (X-HBM) architecture designed for AI chips to address the increasing requirements of generative AI and high-performance computing.

- February 2025: Everspin Technologies, Inc. revealed that its PERSYST MRAM has received validation for use with all Lattice Semiconductor Field Programmable Gate Arrays (FPGAs).

- December 2024: Kioxia Corporation revealed the development of OCTRAM (Oxide-Semiconductor Channel Transistor DRAM), a novel form of 4F2 DRAM made up of an oxide-semiconductor transistor that features both a high ON current and an exceptionally low OFF current.

- August 2024: Samsung Electronics made a differentiation into the low-power DRAM market with their mass production of the 12-nanometer (nm) class LPDDR5X DRAM packages, which are 12 GB and 16 GB versions.

- June 2023: Micron Technology, Inc. revealed its intentions to establish a new assembly and testing facility in Gujarat, India. The new facility by Micron will facilitate the assembly and testing of both DRAM and NAND products, catering to the needs of both domestic and international markets.

- January 2025: Samsung Electronics announced expansion of its high-bandwidth memory production capacity, aiming to support AI and data center applications through advanced HBM technology and enhanced packaging integration capabilities.

INVESTMENT ANALYSIS AND OPPORTUNITIES

The semiconductor memory industry is experiencing a wave of investment driven by AI, cloud computing, 5G, automotive, and other accelerating demands. Emerging technologies such as MRAM are joining the ranks to either add incrementally to the overall growth or impact consumer supply chains. The growth in data centers, EVs, and specialized memory startups will offer opportunities. Still, there remain obstacles in the form of price cycles, heavy capital requirements in the form of covered investments, and potential geopolitical challenges. In summary, investors are focusing on long-term profitability from advanced nodes, 3D architectures, and innovative memory formats.

- According to Reuters, global investment in semiconductor equipment is projected to hit USD 400 billion during 2025-27, with USD 123 billion spent in 2025 alone.

- Samsung Electronics to receive up to USD 6.4 billion in direct funding under the CHIPS and Science Act.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects, such as leading companies, product/types, and the leading end-use of the product. Besides, it offers insights into the semiconductor memory market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| Global Semiconductor Memory Market Scope | |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.30% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

By Type

By End-Use

By Region

|

|

Frequently Asked Questions

The market is projected to reach a valuation of USD 447.93 billion by 2032.

In 2025, the market was valued at USD 171.31 billion.

The market is projected to record a CAGR of 11.30% during the forecast period.

By type, the DRAM segment led the market in 2025.

Growing demand in data centers and cloud computing to aid market growth.

Samsung Electronics Co., Ltd., Micron Technology, Inc., SK Hynix Inc., Intel Corporation, Toshiba Corporation, Western Digital Corporation, Kingston Technology Company, Inc., Infineon Technologies AG, Renesas Electronics Corporation, and Advanced Micro Devices, Inc. are the top players in the Semiconductor Memory market.

Asia Pacific held the highest market share in 2025.

By End-Use, the consumer electronics segment is expected to record the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us