Shape Memory Alloys Market Size, Share & Industry Analysis, By Type (Nickel-Titanium (Nitinol), Copper-based, Iron-based and Others), By End-use Industry (Biomedical, Aerospace & Defense, Automotive, Consumer Electronics and Others), and Regional Forecast, 2026-2034

SHAPE MEMORY ALLOYS MARKET SIZE AND FUTURE OUTLOOK

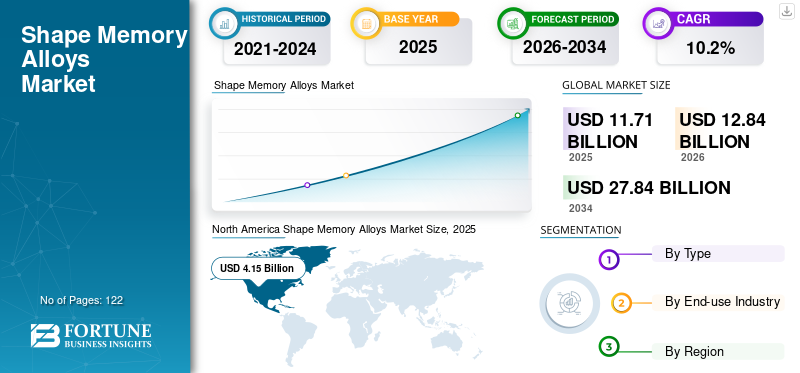

The shape memory alloys market size was valued at USD 11.71 billion in 2025. The market is projected to grow from USD 12.84 billion in 2026 to USD 27.84 billion by 2034 at a CAGR of 10.2% during the forecast period. North America dominated the shape memory alloys market with a market share of 35.43% in 2025.

The Shape Memory Alloys (SMA) is a specialized, performance-driven segment within advanced materials, enabling actuation, superelastic recovery, and vibration/strain management in compact, high-reliability designs. Unlike conventional alloys selected primarily for strength or corrosion resistance, shape memory alloys are chosen for functional behavior recoverable strain, force output and temperature-triggered transformation making them a design-enabling material in applications where motors, springs, and complex linkages are difficult to package or maintain.

Demand is structurally linked to medical device production, aerospace and defense actuation/thermal management, and high-value industrial/precision components, with value growth driven less by bulk tonnage and more by specification intensity. Key players operating in the market include Resonetics, Confluent Medical Technologies, ATI Inc., Fort Wayne Metals, ADMEDES, among others.

Download Free sample to learn more about this report.

SHAPE MEMORY ALLOYS MARKET TRENDS

Medical-grade Nitinol Processing and Componentization is a Key Market Trend

The market is shifting from “SMA as a material” toward “SMA as a qualified, End-use Industry-ready solution,” where value increasingly concentrates in semi-finished forms and components rather than base alloy. Medical OEMs and tier suppliers are placing greater emphasis on tight control of transformation temperatures, inclusion cleanliness, surface finish and fatigue performance, accelerating demand for vertically integrated or tightly managed supply chains that can deliver consistent wire/tube and component performance at scale.

In parallel, non-medical adoption is growing where compact actuation and silent motion provide a system-level advantage such as in aerospace airflow/thermal management, industrial valves, robotics grippers and precision mechanisms. This trend supports value growth beyond unit volumes as customers pay for validated performance rather than simple material weight, reinforcing a “high-mix, high-spec” market structure.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Biomedical Device Demand Drives the Market Growth

Biomedical device application remain the primary demand engine as Nitinol’s superelastic and shape-memory behaviors translate directly into device performance particularly in minimally invasive tools and implantable structures where flexibility, kink resistance and controlled force delivery are critical. As procedure volumes rise and device designs become more complex, shape memory alloys usage expands not only by units but also by specification intensity, including tighter tolerances on wire/tube geometry, surface finish and fatigue life, which increases realized value per kilogram.

This driver also creates structural resilience with medical programs typically require long qualification cycles and validated suppliers, supporting repeat orders and sticky customer relationships. As a result, the shape memory alloys market growth is often less sensitive to short-term price movements and more tied to device pipeline strength, regulatory approvals and supplier capability to meet stringent quality requirements.

MARKET RESTRAINTS

Qualification Burden, Processing Complexity and Cost Sensitivity Limit Wider Penetration

The product adoption is constrained by the fact that performance depends not only on chemistry but on processing history melting cleanliness, thermomechanical treatment, shape-setting and surface conditioning. For many buyers, the cost of adopting product is not just material cost; it is the qualification burden with testing, reliability validation and design iteration to ensure stable transformation temperatures and acceptable fatigue life across real operating conditions.

This restraint is especially visible outside medical and aerospace, where customers may compare shape memory alloys against lower-cost alternatives (small motors, springs, solenoids, elastomers) that are easier to source and integrate. In cost-driven segments, SMAs must justify themselves by reducing parts count, assembly steps, or maintenance risk otherwise adoption can stall despite technical fit.

MARKET OPPORTUNITIES

Industrial Miniaturized Actuation and Reliability-Driven Design Create New Growth Opportunities

A key opportunity lies in industrial systems where compact actuation or self-regulating mechanical response can reduce complexity. Shape memory alloys can enable silent, lightweight, and low-part-count mechanisms in valves, latches, safety releases and precision controls especially where packaging constraints or maintenance costs make conventional actuators unattractive. As automation spreads into smaller form factors, SMAs can gain share as a mechanical intelligence material that converts temperature or electrical input into motion.

Another opportunity is the expansion of iron-based SMAs in construction and infrastructure strengthening, where the value proposition is different and not miniaturized actuation, but prestressing/shape recovery behavior in civil engineering applications. If standardization advances and installers gain experience, Fe-based systems can create a second growth engine alongside Nitinol, broadening the market beyond medtech-centric demand.

MARKET CHALLENGES

Fatigue Performance, Thermal Response Limits and Execution Variability Increase Design Risk

The central execution challenge is that SMA performance is strongly shaped by cycle life and strain amplitude. Many applications demand repeated actuation or continuous flexing; if designs push strain too high, fatigue life can drop sharply, increasing warranty and reliability risk. Thermal response is another constraint with thermally actuated SMAs, heating/cooling rates govern speed, which can limit use in high-frequency applications unless thermal management is engineered carefully.

In addition, performance consistency can vary across production lots if process control is weak, especially for transformation temperatures and surface-related fatigue behavior. This makes supplier selection and QA/QC critical, and can slow adoption among customers who lack the testing infrastructure or engineering depth to qualify and monitor product behavior over time.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade friction and geopolitical instability can influence the market by increasing volatility in nickel and titanium inputs, specialized processing equipment lead times, and cross-border shipment reliability for medical-grade wire/tube and precision components. As many end-use industries require tightly qualified supply chains, disruptions can trigger costly requalification efforts or dual-sourcing programs. Thus, suppliers and OEMs increasingly prioritize regional manufacturing footprints, redundant capacity, and supply chain traceability, especially for regulated medical and defense-linked programs.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in SMAs is focused on improving fatigue life, transformation stability and manufacturability while expanding use cases beyond traditional medical and aerospace niches. For Nitinol, innovation centers on cleaner melts, tighter control of transformation temperatures, advanced thermomechanical processing and surface engineering (finishing/coatings) that improves fatigue resistance and corrosion behavior. Work is also advancing on designable actuator architectures (springs, bundles, laminated forms) and improved control strategies to manage hysteresis and response time.

Sustainability-linked R&D is emerging through process yield improvements, scrap reduction and recycling of high-value alloys, and lower-energy processing routes where feasible. In parallel, iron-based SMA research targets broader structural applications, emphasizing cost-effective production, repeatable recovery stress, and standardization of installation practices steps that could meaningfully expand addressable demand if performance and field reliability are proven at scale.

SEGMENTATION ANALYSIS

By Type

Nickel Titanium (Nitinol) Segment Dominates Due to Superior Superelasticity and High-Value Semi-Finished Forms

Based on type, the global market is segmented into Nickel-Titanium (Nitinol), Copper-based, Iron-based and others.

Among these, Nickel-Titanium (Nitinol) holds the dominant shape memory alloys market share. This leadership is structurally driven by the fact that NiTi offers the most commercially proven combination of shape memory behavior, superelasticity, corrosion resistance and fatigue performance, which is critical for high-reliability applications. The segment’s value is also amplified by where NiTi is consumed and much of its demand sits in medical-grade wire and tubing, laser-cut blanks, and precision components that require tight control over transformation temperature, surface finish and cleanliness.

Copper segment accounts significant market share during the forecast period. Copper-based systems are used where price sensitivity is higher, and operating conditions and fatigue-life requirements are less demanding than medical or aerospace. The segment benefits from relatively easier alloying routes and lower raw material cost in some cases, supporting adoption in actuation elements, thermal triggers, and low-to-mid duty industrial mechanisms. However, copper-based alloys typically face constraints around stability, repeatability and manufacturability at high specification levels, which keeps them structurally below NiTi in value share. The segment register growth rate of 8.6% during the forecast period.

Iron-based systems are attractive when the objective is recovery stress and strengthening/retrofit performance at a potentially more economical alloy base compared with NiTi. Adoption is growing in selective geographies and applications, but the segment remains smaller as end-use uptake depends on standardization, contractor familiarity and proven long-term field performance, which takes time to develop.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Biomedical Segment Dominates Market Due to High Nitinol Intensity in Minimally Invasive Devices and Implantable Structures

Based on end-use industry, the market is segmented into biomedical, aerospace & defense, automotive, consumer electronics, and others.

Biomedical represents the dominant end-use industry segment. The growth reflecting the high SMA intensity in medical devices where superelasticity and shape memory behavior directly translate into clinical and device performance outcomes. The segment is structurally value-intensive as medical applications frequently demand tight mechanical tolerances, fatigue resistance, controlled force delivery, and consistent transformation temperatures, especially in wire/tube-based device architectures.

Aerospace & Defense account positive growth. The growth is supported by the need for compact, lightweight, and reliable actuation in systems where packaging constraints and maintenance risks are high. The product adoption is most attractive where it reduces part count or enables functionality in constrained geometries, such as thermal-driven actuation, airflow/thermal management elements, and precision mechanisms. This segment’s value share is supported by stringent qualification requirements and reliability expectations, but overall volume remains smaller than biomedical due to longer program cycles and selective adoption where SMAs provide a clear system-level advantage. The segment register growth rate of 10.0% during the forecast period.

Automotive industry growth is driven by targeted use-cases where SMAs replace conventional actuators or simplify mechanical systems, such as latches, valves, vents, or compact control mechanisms. The automotive segment tends to be more cost sensitive and is therefore shaped by a strict “value vs. alternative” test as SMAs scale best when they reduce assembly complexity, enable compact packaging, or improve durability. Growth is typically strongest in applications with clear performance payoff and where suppliers can deliver consistent properties at automotive-grade quality and cost.

SHAPE MEMORY ALLOYS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Shape Memory Alloys Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is predicted to account for dominant share during the forecast period. The growth is driven by a combination of medical device innovation, aerospace program density, and high-value component manufacturing. The region’s product demand is structurally weighted toward premium, specification-intensive applications, particularly in biomedical and aerospace & defense. North America also tends to support higher realized value per unit as end users place stronger emphasis on qualification depth, reliability validation and mature supplier ecosystems.

U.S. Shape Memory Alloys Market

In 2025, The U.S. represented USD 3.72 billion market in North America, driven primarily by strong demand from the medical and aerospace sector. The U.S. accounts for roughly 31.8% of global market sales.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

Asia Pacific accounted for the significant market share in 2025. The growth is supported by its scale in advanced manufacturing ecosystems and its growing depth in medical device production and precision processing. The region benefits from strong downstream demand in electronics and industrial manufacturing and is also a key base for high-volume production of components and assemblies. Growth is reinforced by expanding technical capability in precision metallurgy and processing, which supports both local consumption and participation in global supply chains.

China Shape Memory Alloys Market

The China market in 2025 was at USD 1.62 billion, representing roughly 13.9% of global market revenues.

Europe

European demand is reinforced by strong engineering standards and a focus on performance compliance, which supports adoption where SMAs enable compact actuation or reliability improvements. The region also retains meaningful activity in specialty materials and component manufacturing, supporting stable demand even when specific end markets shift.

Germany Shape Memory Alloys Market

The Germany market in 2025 was at USD 0.85 billion, representing roughly 7.3% of global market revenues.

U.K. Shape Memory Alloys Market

The U.K. market in 2025 was at around USD 0.74 billion, representing roughly 6.3% of global market revenues.

Latin America

Latin America demand tied primarily to selective industrial and automotive activity, and smaller but growing opportunities in medical supply chains as manufacturing footprints expand. The region’s market remains comparatively smaller due to limited local processing depth for high-spec SMA forms, but the growth can emerge where industrial modernization or localized device manufacturing increases adoption.

Brazil Shape Memory Alloys Market

The Brazil market in 2025 was at around USD 0.19 billion, representing roughly 1.6% of global market revenues.

Middle East & Africa

The region growth reflecting early-stage adoption across a mix of industrial and energy-related applications, along with smaller medical and aerospace value pools. Demand growth is typically constrained by limited specialized manufacturing capacity and narrower qualification ecosystems, but opportunities exist where high-reliability mechanisms are required in harsh operating environments and where import-led supply chains can support specialized product usage.

GCC Shape Memory Alloys Market

The GCC market in 2025 was at around USD 0.18 billion, representing roughly 1.5% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Medical-Grade Nitinol Specialists and Precision Component Manufacturers Shape Market Competition

The global market is structurally quality- and specification-led, with competition shaped less by commodity pricing and more by metallurgical process control, transformation-temperature consistency, fatigue performance, and qualification track record. The competitive core is concentrated in nitinol supply chains serving biomedical and aerospace programs, where customers demand repeatability across lots, validated surface condition, and high reliability over long cycle life. Leading producers, such as Resonetics, Confluent Medical Technologies, ATI Inc., Fort Wayne Metals, ADMEDES are directing capital toward process optimization, product quality enhancement and environmentally aligned manufacturing practices. Innovation efforts are increasingly focused on enhancing purity consistency, reducing the environmental footprint, and developing grades suitable for advanced products.

LIST OF KEY SHAPE MEMORY ALLOYS COMPANIES PROFILED

- Resonetics (U.S.)

- Confluent Medical Technologies (U.S.)

- ATI Inc. (U.S.)

- Fort Wayne Metals (U.S.)

- ADMEDES (Germany)

- Cirtec Medical (U.S.)

- Vascotube (Germany)

- SAES Getters S.p.A. (Italy)

- Dynalloy, Inc. (U.S.)

- Lighteum Medical (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Medical Device Components (MDC) announced it rebranded as Lighteum Medical after becoming a standalone company post-divestment and completing the acquisition of Lighteum LLC. The release frames the new identity around leadership in precision components made from precious metals and nitinol, reinforcing the continued strategic push toward value-added component manufacturing rather than raw material supply.

- January 2024: Confluent announced a partnership with ATI to invest more than USD 50 million over several years in ATI’s Nitinol melting and materials conversion infrastructure. The announcement explicitly states this investment would more than triple ATI’s melt capacity for medical Nitinol, a major signal that demand growth is stressing upstream capacity.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, type, and end-use industry. Additionally, it provides valuable insights into the market and current industry trends, as well as highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Growth Rate | CAGR of 10.2% from 2026 to 2034 |

| Segmentation | By Type, By End-use Industry and Region |

| By Type |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 11.71 billion in 2025 and is projected to reach USD 27.84 billion by 2034.

Recording a CAGR of 10.2%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

Biomedical end-use industry segment led in 2025.

North America held the highest market share in 2025.

Biomedical production and electrification drive market growth.

- 2021-2034

- 2025

- 2021-2024

- 122

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us