Shipbroking Market Size, Share & Industry Analysis, By Service Type (Chartering Services, Sale and Purchase Transaction, and Newbuilding Services), By Broking Type (Dry Cargo Broking, Tanker Broking, Container Vessel Broking, Futures Broking, and Others), By End Use (Oil and Gas, Mining, Agriculture, Chemicals and Pharmaceuticals, Metal and General Manufacturing, Construction Industry, Power Generation and Renewable Energy, Automotive, and Others), and Regional Forecast, 2026 – 2034

KEY MARKET INSIGHTS

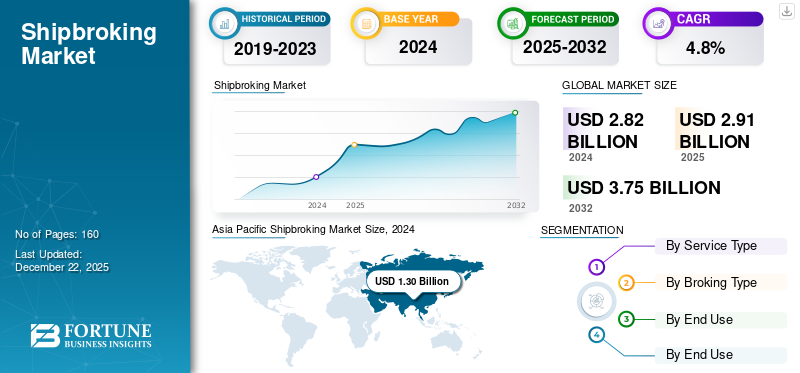

The global shipbroking market size was valued at USD 2.91 billion in 2025. The market is projected to grow from USD 3.01

billion in 2026 to USD 4.08 billion by 2034, exhibiting a CAGR of 3.90% during the forecast period. Asia-specific dominated the global market with a share of 45.00% in 2025.

Growing seaborne transport and rising demand for commodities and raw materials are driving the growth of the market. Increased trade, containerization, growing orders for new ships, green regulations, and shifting supply chain strategies are further boosting market growth. The expansion of e-commerce and increased investment in fleet development continue to drive global market expansion. Growth in maritime infrastructure and new port developments is also contributing to the market. According to the United Nations Conference on Trade and Development (UNCTAD), over 80% of global trade moves by sea, supporting the market. In addition, regulatory policies and sustainability pressures are increasing demand for broking services.

Several key players in the market, such as Clarksons Inc., Braemer Plc, IFCHOR GALBRAITHS, and Howe Robinson, are expanding their service offerings through acquisitions of domestic players, the establishment of offices, and investment in technology platforms to meet regional demands. Similar strategies to enhance the share for key players in the market.

Shifting supply chains and disruptions in shipping routes are further driving demand for broking activities. Growth in ship financing, increased volatility in freight rates, and the adoption of digital platforms are also supporting market growth. However, inconsistent and unpredictable geopolitical scenarios may impact growth.

The COVID pandemic disrupted global trade and temporarily reduced trade volumes across nations. However, in the post-pandemic years, a surge in demand and restructuring of supply chains significantly impacted the market. The market recovered after the pandemic to meet increasing demand in many countries.

Download Free sample to learn more about this report.

IMPACT OF TARIFFS

Trade Route Diversification and Freight Rate Volatility Might Impact Market

Reciprocal tariffs created a significant impact on the shipbroking activities, owing to diversifying trade routes, reduced trade volumes, changing freight rates, rising sale and purchase broking, etc. Evolving supply chain and sourcing strategies are more likely to further support the market demand for shipbroking. However, the market would further be reshaped, owing to shifting trade flows and increasing dependence on brokers’ market.

Shipbroking Market Trends

Clean Energy Transitions Across Industries to Bolster Market Growth

Energy trading is widely evolving across several regions, with increasing demand for clean energy solutions. Clean energy commodities such as LNG, ammonia, or hydrogen-based fuels, and batteries, are largely gaining market traction, owing to rising demand across industries. Several companies are investing in solar projects, offshore and onshore wind energy projects, which would further drive the market growth of broking services via sea routes. For instance, in August 2025, the Ugandan government announced its approval for a 100MW solar PV project where EV modules will be provided by Energy America, built by EA Astrovolt. Energy transition fuels such as battery, ammonia/ hydrogen-based, bio-fuels are increasing in volumes, further generating increased tanker trade flows across global markets.

MARKET DYNAMICS

Market Drivers

Growing Demand for Commodities across Regions to Drive Market

Commodities such as metals, mining, energy, and agricultural products are all supporting the growth. Growing infrastructure activities and investment in the construction sector are expected to boost the demand for metals, construction materials, and mining. Countries are further diversifying their sourcing strategies, resulting in new sea routes and complex trade flows. Increased complexity in trade flows surges demand for broker involvement due to the high risk and complexity. E-commerce growth, especially post-pandemic and rising consumer goods demand globally, further generates demand for brokers in the shipping industry. Growing consumer goods’ steady demand across several countries would further boost the market.

Market Restraints

Economic Slowdown and Geopolitical Uncertainty Might Limit Market Growth

Unprecedented economic conditions, tariffs, environmental regulations, and geopolitical uncertainty might limit growth during the short-term period. High compliance costs and changing seatrade strategies might further limit the shipbroking market growth. However, growing trade volumes and expanding trade routes to further boost the market growth.

Market Opportunities

Financialization of Shipping Activities to Bring Strong Market Opportunities

Financing options such as Forward freight agreements, asset play transactions, ship leasing, and advisory services are evolving opportunities for shipbroking. Increasing ship financing requires the involvement of brokers as intermediaries, driving the demand for shipbrokers. Key players in the market are expanding their service offerings, inclusive of advisory and financial derivatives, to meet customer demand. For instance, Clarksons Inc. in July 2025 announced its launch of a financial derivatives Containers Forward Freight Agreements (FFA) desk.

SEGMENTATION ANALYSIS

By Service Type

Chartering Services to Dominate the Market Owing to Growing Demand for Dry Cargo and Tanker Trades

Based on service type, the market is fragmented into chartering services, sale and purchase transactions, and newbuilding services.

The chartering services segment is projected to dominate the market with a share of 60.13% in 2026 as a result of large-scale demand for dry and liquid cargos. Steady demand for dry cargo and tanker trade to generate market revenue for chartering services. According to UNCTAD in 2023, dry Bulk carriers and tankers represent a significant revenue share of more than 70% of the total seaborne trade volume. Large volumes of transactions and high-value contracts involve significant commission in the chartering services. Increased volatility in the market involves increased brokerage income in the chartering services, resulting in a dominant revenue share of the segment. Furthermore, chartering services cover a wide range of vessel types, including containers, dry bulk, and tankers.

Newbuilding services are gaining market traction through fleet renewal as a result of decarbonization, environment-friendly fuel adoption, green financing, etc. Stringent regulatory policies, ageing fleet, and nearing replacement cycles are projected to drive the highest growth of newbuilding services. Sustainable financing is growing in the marine and offshore industry across several regions, surging the growth of newbuilding services.

To know how our report can help streamline your business, Speak to Analyst

By Broking Type

Tanker Broking to Cater Highest Revenue Market Share Due to Large Fixture Volumes

Based on broking type, the market is segmented as dry cargo broking, tanker broking, container vessel broking, futures broking, and others. Others include specialized broking and offshore vessel broking.

The dry cargo broking segment is expected to account for 40.20% of the market share in 2026. The tanker broking segment accounts for the highest revenue market share, owing to several factors, including growing fixture volumes, volatile freight rates, and increased trade volumes of renewable energy. Volatile freight rates and continuous broker reliance drive the demand for tanker broking across regions. Growing energy trades and high demand for commodities to generating a significant demand for tanker broking.

The futures broking segment is set to witness the highest growth rate over the forecast period due to the expansion of forward freight agreements and a wide array of financing options. Diversification of broking instruments that cover dry bulk carriers, tankers, containers, LNG freight, etc., to drive the market growth of futures broking.

By End Use

Mining Sector to Dominate Highest Revenue Market Share Due to Growing Dry Bulk Commodities

Based on end use, the market is diversified as oil and gas, mining, agriculture, chemicals and petrochemicals, metal and general manufacturing, construction industry, power generation and renewable energy, automotive, and others. Other end uses include semiconductor, paper, textile, packaging, food and beverages, aerospace, defense, and semiconductor.

The mining segment dominated the global market with a market share of 33.89% in 2026. Growing dry bulk commodities and trade volumes to result in the dominance of the mining sector. Mining companies largely engage in long-term agreements and contracts, leading to large transactions in the broking services. High trade volumes and long-term contracts drive the broking market across the industry.

The power generation and renewable energy segment is expected to witness the highest growth rate, owing to the renewable energy transition, the growing offshore wind energy demand, and rising investment in the renewable sector, further supported by government policies and initiatives. For instance, Tata Power Company's renewables segment’s operating profit share rose to 26.3% in the year 2024.

SHIPBROKING MARKET REGIONAL OUTLOOK

The market is classified into North America, Europe, South America, Asia Pacific, and the Middle East & Africa.

Asia Pacific

Asia Pacific Shipbroking Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the shipbroking market share, owing to the rising import and export of dry bulk commodities such as iron ore, steel, and other raw materials. Increasing demand for raw materials, energy products, construction materials, and inventories, supported by a rising population, is further driving the demand for shipbroking in Asian countries. Longer routes and large container dominance in the region generate the highest revenue for shipbrokers across several Asia countries. The Japan market is projected to reach USD 0.13 billion by 2026, the China market is projected to reach USD 0.72 billion by 2026, and the India market is projected to reach USD 0.08 billion by 2026. In 2025, Asia Pacific generated USD 1.31 billion, contributing 45.00% to global market revenue, and is projected to grow to USD 1.35 billion in 2026.

Download Free sample to learn more about this report.

China is expected to dominate the market in the Asia Pacific region, owing to increasing demand for coal, gas, LNG, and other energy products. Growing dry bulk demand and strong demand for capsize/panamax trades to further bolster demand for shipbroking services across the country. For instance, China imported over 1.24 billion tons of iron ore in 2024, with 6.6% year-on-year growth in comparison to 2023.

To know how our report can help streamline your business, Speak to Analyst

Europe

The European market is expected to witness the highest growth during the forecast period as a result of longer sea route considerations, re-routing strategies, etc. Longer routes increase brokerage costs, driving up the market for the region. For instance, according to the Department of Transport, the U.K.’s liquid and dry bulk cargo accounted for about 60% of the total maritime trade in 2021. Large volumes of dry and liquid cargoes, and volatile freight rates to significantly drive the market growth. The U.K. remains dominant in the region, owing to large maritime hubs such as the Baltic Exchange, and a significant number of key players, including Clarksons, diversified global reach, etc. The UK market is projected to reach USD 0.55 billion by 2026, while the Germany market is projected to reach USD 0.14 billion by 2026. Europe maintained a strong presence in the global market, reaching USD 1.17 billion in 2025, accounting for 40.30% share, and is expected to reach USD 1.22 billion in 2026.

North America

The market in North America to witness steady growth as a result of increasing trade flows, reshaping trade routes, and varying prices for commodities and other cargoes. A volatile market and unprecedented scenarios such as trade wars and tariff implications to change the market dynamics in the short term. The U.S. market is projected to reach USD 0.25 billion by 2026. The North America region captured 11.60% of the global market in 2025, generating USD 0.34 billion in revenue, and is projected to reach USD 0.35 billion in 2026.

The U.S. to dominate the market for broking services as a result of growing exports, high demand for energy products, and increasing exports to European and other regions. For instance, in 2024 U.S. exported over 55% of its crude oil and natural gas plant liquids production to Mexico.

South America

The South American market is prominently driven by several factors, such as iron-ore trade, agricultural raw materials, and high volumes of transactions for battery metals such as lithium. For instance, Argentina is aiming to reach mining exports of USD 10 billion by 2027, primarily led by lithium and copper expansions. The South America market was valued at USD 0.04 billion in 2025, capturing 1.30% of global revenue, and is estimated to reach USD 0.04 billion in 2026.

Middle East & Africa

The Middle East & African market is prominently supported by growing LNG capacity, high trade volumes at Red Sea routes, growing crude trade, and expanding port capacities. Several such factors to drive the market demand for shipbroking services across the region are further supported by growing investment and government support in energy projects. Middle East & Africa recorded a market size of USD 0.05 billion in 2025, capturing 1.80% of the global market share, and is projected to reach USD 0.05 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaboration and Expansion of Broking Services Across Industry Segments to Strengthen Key Players' Market Share

The shipbroking market is moderately fragmented, owing to an increasing number of shipbrokers in the industry, growing collaboration, and merger strategies by key players. Key players are adopting new technologies and expanding their service offerings to their customers to develop a strong brand presence and penetration. Key players are focusing on specific industries such as nuclear energy and renewables to generate diversified revenue sources.

Long List of Shipbroking Companies Studied (including but not limited to)

- AGORA SHIPBROKING Corp. (Greece)

- Aries Asia (Singapore)

- BGC Group Inc. (U.S.)

- Braemar Plc (U.K.)

- BRS Group (Switzerland)

- Chowgule Brothers Pvt. Ltd. (India)

- Clarksons PLC (U.K.)

- E.A. Gibson Shipbrokers Ltd. (U.K.)

- Fearnleys AS (Norway)

- Howe Robinson Partners Pte Ltd. (Singapore)

- IFCHOR GALBRAITHS (Switzerland)

- Interocean Group (India)

- Lorentzen and Co. (Norway)

- Maritime London Ltd. (U.K.)

- McQuilling Partners Inc. (U.S.)

- Seacore Shipbrokers Ltd. (Greece)

- SHIPLINKS (India)

- SHIPLINKS. (U.K.)

- Maersk Broker K/S (Denmark)

- Freight Investor Services (U.K.)

- SPI Marine UK Ltd. (U.K.)

- MB Shipbrokers (Denmark)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Charter Haus AG opened its new office in Japan to expand its growth prospects in Asian markets.

- April 2025: Freight Investor Services (FIS) announced its office opening in Geneva to expand its global footprint and shipping markets.

- March 2025: Clarksons USA Inc. announced the acquisition of Euro-America Shipping & Trade, Inc. (“EAST”), which specializes in providing freight contracts.

- February 2025: Five service providers that include Arrow, E.A. Gibson, Howe Robinson, Ifchor Galtraiths, and SSY collaborated to launch a new platform for Recap and Charter Party management.

- May 2024: Ifcor Galbraiths launched its new office in Vancouver, Canada to expand its services across the North American market.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, service types, broking type, and end use of the services. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

|

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service Type

By Broking Type

By End Use

By Region

|

|

Companies Profiled in the Report |

Braemar Plc (U.K.) BRS Group (France) Clarkson Plc (U.K.) E.A. Gibson Shipbrokers Ltd. (U.K.) Howe Robinson Partners Pte Ltd. (Singapore) IFCHOR GALBRAITHS (Switzerland) Simpson Spence Young Ltd. (U.K.) Maersk Broker K/S (Denmark) Freight Investor Services (U.K.) Fearnleys AS (Norway) |

Frequently Asked Questions

The market is projected to reach USD 4.08 billion by 2034.

In 2025, the market was valued at USD 2.91 billion.

The market is projected to grow at a CAGR of 3.90% during the forecast period.

By service type, the chartering services segment led the market.

Growing Demand for Commodities across the Region to Drive the Market Growth.

Braemar Plc, Clarkson Plc, and Howe Robinson Partners Pte Ltd. are a few of the top players in the market.

Asia Pacific holds the highest market share.

By end use, the power generation and renewable energy segment is expected to witness the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us