Silicon Metal Market Size, Share & Industry Analysis, By Application (Aluminum Alloys, Silicones, Polysilicon, and Others), and Regional Forecast, 2026-2034

Silicon Metal Market Overview

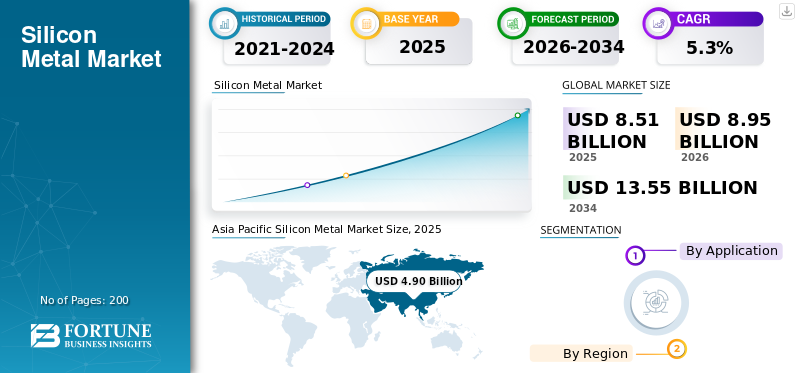

The global silicon metal market size was USD 8.51 billion in 2025. The market is projected to grow from USD 8.95 billion in 2026 to USD 13.55 billion by 2034 at a CAGR of 5.3% during the 2026-2034 period. Asia Pacific dominated the global market with a market share of 57.57% in 2025.

Silicon metal is a high-purity, metallurgical-grade form of silicon (typically 98–99.99% Si) produced by the carbothermic reduction of quartz in electric arc furnaces. It is a critical intermediate material, rather than a finished product, that forms the backbone of several downstream value chains. The major demand driver for this metal is its use in aluminum alloys, where it improves castability, strength, and corrosion resistance, making it essential for automotive light weighting, electric vehicles, and construction.

Ferroglobe, Elkem ASA, Hoshine Silicon Industry Co., Ltd., and RIMA are the key players operating in the market.

Download Free sample to learn more about this report.

Silicon Metal Market KEY TAKEAWAYS

- 2025 Market Size: USD 8.51 billion

- 2026 Market Size: USD 8.95 billion

- 2034 Forecast Market Size: USD 13.55 billion

- CAGR: 5.3% from 2026–2034

- Asia Pacific dominated the silicon metal market with a 57.57% share in 2025.

- The aluminum alloys segment is expected to hold the largest market share during the forecast period.

- The polysilicon segment is projected to be the fastest-growing segment, registering a CAGR of 6.6% through 2034.

Asia Pacific

Asia Pacific is expected to remain the leading market, supported by strong manufacturing activity, solar energy expansion, and infrastructure development.

North America

North America maintains steady demand driven by aluminum alloy applications in automotive, aerospace, and packaging industries.

Europe

Europe records resilient demand due to widespread use in construction, healthcare, electronics, and industrial processing applications.

U.S.

U.S. The market was valued at approximately USD 1.17 billion in 2025, accounting for around 13.7% of global silicon metal sales.

Japan

Japan The market reached approximately USD 0.27 billion in 2025, representing about 3.2% of global silicon metal sales.

Read More

SILICON METAL MARKET TRENDS

Silicon Metal Shifts from Commodity to Strategic Material is Reshaping Market

The global market is undergoing a structural transition from a low-margin, commodity-driven market to a strategically important materials sector. This shift is driven by rising demand from solar panel manufacturing, electric vehicles, and advanced silicones, which require higher consistency and tighter specifications. Producers are increasingly investing in furnace efficiency, renewable power sourcing, and downstream integration to stabilize margins. At the same time, buyers are prioritizing supply security and carbon footprint, elevating silicon metal from a purely cost-driven input to a strategic procurement item tied closely to energy transition, driving silicon metal market growth in tandem.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Energy Transition and Solar PV Expansion to Drive Market Growth

The key driver of the market is the accelerating global energy transition, which is directly increasing demand across multiple downstream applications. The rapid expansion of solar photovoltaic capacity is boosting polysilicon consumption, while the increasing adoption of electric vehicles and lightweight automotive designs is driving higher use of aluminum silicon alloys. These trends are reinforced by government policies focused on decarbonization, renewable energy adoption, and energy efficiency. As a result, demand for silicon metal is becoming less dependent on short-term industrial cycles and more closely linked to long-term policy and sustainability objectives, supporting steady market growth.

MARKET RESTRAINTS

High Energy Dependence and Rising Environmental Costs to Restrain Market Growth

Silicon production is constrained by its heavy dependence on electricity and growing environmental compliance costs. Power expenses account for a significant portion of total production costs, while stricter carbon regulations and environmental standards are leading to furnace curtailments and capacity rationalization, particularly in coal-based regions. Securing long-term, affordable electricity has become a critical challenge for producers. These structural constraints limit the pace of new capacity additions and restrict supply flexibility, preventing the industry from responding rapidly to demand growth and increasing its exposure to regulatory risk.

MARKET OPPORTUNITIES

Low-Carbon Silicon Creates Premium Market Segments with High Growth Opportunities

The global shift toward sustainability is creating a meaningful opportunity for the silicon industry to move beyond cost competition. Customers in the solar, electronics, and silicones industries are increasingly seeking low-carbon silicon to meet their own decarbonization commitments. Producers that can rely on renewable electricity, improve furnace efficiency, or use biomass-based reductants are gaining a clear advantage. This allows them to secure long-term supply contracts, command modest price premiums, and build closer customer partnerships. Regions with access to clean power are especially well-positioned to turn sustainability into a durable competitive edge.

MARKET CHALLENGES

Supply Concentration and Volatility to Create Challenges for Market Growth

One of the biggest challenges in the silicon industry is its heavy dependence on a highly concentrated supply base, particularly in China. When policies change, power shortages occur, or environmental rules tighten, the impact is felt almost immediately across global markets. For downstream manufacturers, this creates uncertainty in pricing, availability, and planning, often forcing them to make reactive sourcing decisions rather than strategic ones. For producers outside China, competing on cost while maintaining stable operations remains a significant challenge. Until supply becomes more geographically balanced, volatility and supply risk are likely to continue shaping decision-making across the product value chain.

SEGMENTATION ANALYSIS

By Application

To know how our report can help streamline your business, Speak to Analyst

Lightweighting Push in Electric Vehicles Powers Demand in Aluminum Alloys Growth

Based on application, the market is segmented into aluminum alloys, silicones, polysilicon, and others.

The aluminum alloys segment is anticipated to hold the dominant silicon metal market share during the forecast period. The primary factor driving demand for product in aluminum alloys is the global push for lightweighting across automotive, transportation, and construction sectors. Silicon improves aluminum’s castability, strength, and durability, making it essential for producing complex, high-performance components. As electric vehicles gain market share, manufacturers are increasingly relying on aluminum-silicon alloys to offset battery weight and improve efficiency. This shift toward lighter materials is anticipated to prompt steady demand in aluminum alloy applications.

The polysilicon segment is anticipated to rise with a CAGR of 6.6% during the forecast period. The key factor driving silicon metal demand in polysilicon is the global acceleration of solar power deployment. The metal serves as the essential raw material for polysilicon used in solar cells, directly linking demand to renewable energy policies and climate commitments. As governments prioritize energy security and decarbonization, large-scale solar installations are expected to continue expanding. This policy-driven growth, supported by long-term investment and infrastructure planning, positions polysilicon as the fastest-growing segment in the market.

SILICON METAL MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Silicon Metal Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region is expected to dominate the market during the forecast period. Asia Pacific is the largest market for this metal, driven by its vast manufacturing base, rapid urbanization, and leadership in solar energy. China dominates demand through its integrated polysilicon production and extensive use of aluminum alloys in the automotive, infrastructure, and machinery sectors. At the same time, India and Southeast Asia contribute to growth as industrialization and construction accelerate. Rising solar installations and electronic devices manufacturing further strengthen demand. Together, large-scale industrial activity and policy-led energy transition firmly position the region as the primary engine of global consumption, driving market growth in tandem.

Japan Silicon Metal Market

Japan’s market reached the valuation of approximately USD 0.27 billion in 2025, equivalent to around 3.2% of global silicon metal sales.

China Silicon Metal Market

China’s market was one of the largest globally, with 2025 revenues valued at around USD 3.58 billion, representing roughly 42.1% of global silicon metal sales.

India Silicon Metal Market

India’s market reached the valuation of approximately USD 0.48 billion in 2025, equivalent to around 5.6% of global market.

North America

North American silicon demand is primarily driven by aluminum alloys used in automotive, aerospace, and packaging applications, which are supported by the need for lightweighting and increased efficiency. A strong base of silicone production and specialty materials for electronics and healthcare provides additional stability. While overall industrial growth is mature, silicon remains a critical input for strategic manufacturing sectors.

U.S. Silicon Metal Market

The U.S. market was analytically approximated at around USD 1.17 billion in 2025, accounting for roughly 13.7% of global silicon metal sales.

Europe

In Europe, demand is primarily driven by silicone applications used in construction, industrial processing, healthcare, and electronics. These applications require consistent, high-quality metal and are less volume-cyclical than aluminum. Additionally, Europe’s strong emphasis on sustainability and low-carbon materials supports steady consumption of silicon with traceable, renewable-powered origins. Demand growth is moderate but resilient, reflecting Europe’s focus on value-added, regulation-driven industrial use rather than heavy volume expansion.

U.K. Silicon Metal Market

The U.K.’s market reached the valuation of approximately USD 0.13 billion in 2025, equivalent to around 1.5% of global silicon metal sales.

Germany Silicon Metal Market

Germany’s market reached the valuation of approximately USD 0.29 billion in 2025, equivalent to around 3.4% of global market.

Latin America

In Latin America, metal demand is overwhelmingly driven by the aluminum value chain, particularly in Brazil. Abundant bauxite resources and established aluminum production support consistent consumption of silicon for alloying applications. Demand growth is closely tied to regional infrastructure development, transportation needs, and export-oriented manufacturing. The limited development of the silicone and polysilicon industries keeps demand concentrated in metallurgical uses, making the region’s silicon consumption more cyclical and closely linked to aluminum market conditions.

Brazil Silicon Metal Market

Brazil’s market reached the valuation of approximately USD 0.23 billion in 2025, equivalent to around 2.7% of global silicon metal sales.

Middle East & Africa

In the Middle East and Africa, metal demand is driven by the expansion of aluminum smelting and downstream alloying, especially in Gulf countries. Energy-intensive aluminum operations benefit from competitive power costs, indirectly supporting product consumption. Infrastructure development and construction activity further reinforce aluminum demand. While silicone and polysilicon use remains limited, the region’s focus on industrial diversification and metals-based growth shows steady growth from a relatively small base.

Saudi Arabia Silicon Metal Market

Saudi Arabia’s market reached the valuation of approximately USD 0.08 billion in 2025, equivalent to around 0.9% of global market.

COMPETITIVE LANDSCAPE

Key Industry Players

China-Led Supply Concentration and Energy Economics Redefine Competition in Market

The market is marked by a highly concentrated supply base, intense cost competition, and growing strategic differentiation. China leads global production, providing domestic producers with significant scale and cost advantages. In contrast, producers outside China compete by emphasizing operational reliability, sustainability, and lower carbon footprints. Hoshine Silicon Industry, Ferroglobe, and Elkem anchor global supply, while RIMA Industrial plays a key role as a competitive Latin American exporter. As the market evolves, competition is increasingly shaped by access to affordable energy, environmental regulations, and downstream integration, with buyers prioritizing supply security and low-carbon sourcing alongside pricing.

LIST OF KEY SILICON METAL COMPANIES PROFILED

- Ferroglobe (U.K.)

- Elkem ASA (Norway)

- GCL TECH (China)

- Hoshine Silicon Industry Co., Ltd. (China)

- Mississippi Silicon (U.S.)

- RIMA (Brazil)

- RusAL (Russia)

- Wacker Chemie AG (Germany)

- HENAN ANYANG METALLURGY MATERIAL CO.,LTD. (China)

- PCC SE (Germany)

KEY INDUSTRY DEVELOPMENTS

- October 2022 - Ferroglobe PLC announced plans to restart its 55,000-ton silicon metal plant in Polokwane, South Africa, in response to strong global demand and volatile European energy markets. The facility offers lower-cost production due to favorable energy rates and a strategic location. The restart aligns with Ferroglobe’s strategy to optimize its global asset footprint and secure long-term customer contracts.

- October 2022 - GCL Tech has announced a major manufacturing project in Wuhai, Inner Mongolia, adding 100,000 tons/year of granular silicon and 150,000 tons/year of high-purity nanocrystalline silicon capacity. This expansion will boost its total granular output to 500,000 tons/year. Known for its low-energy, low-emission production process, GCL has secured long-term contracts totaling 814,300 tons. Chairman Zhu Gongshan emphasized the material’s critical role in enabling low-cost, green solar energy, aligning with global clean energy goals.

- April 2021 - Elkem has approved a USD 0.38 billion expansion of its Xinghuo Silicone Plant in China, aimed at strengthening its position in the rapidly growing silicone market. The upgrade will boost capacity by over 50% and cut energy use by 57%, raw materials by 11%, and solid waste by 30%, reinforcing Elkem’s ESG leadership.

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies and leading applications of the product. Additionally, it provides insights into the analysis of key market trends and highlights significant industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Volume (Kiloton); Value (USD Billion) |

|

Growth Rate |

CAGR of 5.3% during 2026-2034 |

|

Segmentation |

By Application, and By Region |

|

By Application |

· Aluminum Alloys · Silicones · Polysilicon · Others |

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 8.51 billion in 2025 and is projected to record a valuation of USD 13.55 billion by 2034.

In 2025, Asia Pacific stood at USD 4.90 billion.

Registering a CAGR of 5.3%, the market is expected to exhibit steady growth during the forecast period of 2026-2034.

The aluminium alloy application is expected to lead this market during the forecast period.

The global energy transition and solar PV expansion are expected to drive market growth.

Ferroglobe, Elkem ASA, Hoshine Silicon Industry Co., Ltd., and RIMA are the major players operating in the market.

Asia Pacific dominated the market in terms of share in 2025.

Lightweighting and electric vehicle penetration to create market growth opportunities.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us