Smart Container Market Size, Share & Industry Analysis, By Container Type (Dry Containers, Refrigerated Containers, Tank Containers, and Special-Purpose Containers), By Component Type (Hardware, Connectivity, Platform/Software, and Services), By End-user (Shipping Lines/Ocean Carriers, Freight Forwarders & 3PLs/NVOCCs, Shippers/Cargo Owners, Port Operators & Terminal Authorities, Rail & Intermodal Operators, and Leasing Companies & Container Fleet Owners), By Vertical/Application, By Deployment Type, and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

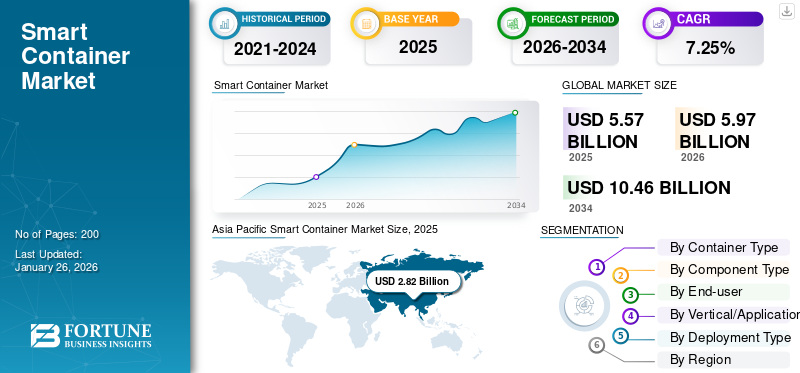

KEY MARKET INSIGHTS

The global smart container market size was valued at USD 5.57 billion in 2025 and is projected to grow from USD 5.97 billion in 2026 to USD 10.46 billion by 2034, exhibiting a CAGR of 7.25% during the forecast period. Asia Pacific dominated the smart container market with a market share of 50.72% in 2025.

Smart containers integrate IoT sensors, GPS tracking, and telematics systems within traditional shipping containers to enable real-time monitoring of location, temperature, humidity, shock, and door status throughout the logistics chain. Widely used across maritime, rail, and road freight, they enhance cargo visibility, operational efficiency, and security. The market is driven by the rising demand for supply chain transparency, growth in cross-border e-commerce, and increasing adoption of digital logistics platforms. Additionally, regulatory emphasis on cargo traceability, integration with blockchain and AI-based analytics, and rising adoption among cold chain logistics operators are further propelling market growth. Smart containers also play a key role in reducing cargo losses, optimizing fleet utilization, and enabling predictive maintenance, positioning them as a core enabler of connected and intelligent logistics ecosystems.

Key players in the market include Traxens, Orbcomm Inc., Globe Tracker, SM Group, and CMA CGM Group. These companies focus on developing advanced technologies such as IoT-enabled real-time tracking and monitoring systems, cloud-based monitoring platforms, and data analytics solutions to enhance cargo visibility, asset utilization, and supply chain efficiency. Strategic collaborations with shipping lines, freight forwarders, and logistics technology providers, along with investments in AI-driven predictive analytics, blockchain-based traceability, and energy-efficient sensor modules, strengthen their position in the global logistics ecosystem. Continuous innovation in real-time monitoring, temperature-controlled container management, and integrated fleet intelligence enables these players to support the digital transformation of global trade and smart logistics infrastructure.

Download Free sample to learn more about this report.

Smart Container Market Takeaways

- 2025 Market Size: USD 5.57 billion

- 2026 Market Size: USD 5.97 billion

- 2034 Forecast Market Size: USD 10.46 billion

- CAGR: 7.25% from 2026–2034

- Asia Pacific dominated the smart container market with a 50.72% share in 2025.

- The dry containers segment is projected to account for 46.39% of the global market share in 2026.

- The hardware segment is expected to lead by component type with a 44.71% share in 2026.

North America

North America accounted for USD 1.31 billion in 2025 and is expected to grow to USD 1.40 billion in 2026.

Europe

Europe generated USD 1.19 billion in 2025, representing 21.38% of global revenue, and is projected to reach USD 1.26 billion in 2026.

Asia Pacific

Asia Pacific led the global market in 2025 with USD 2.82 billion in revenue and is projected to reach USD 3.06 billion in 2026.

U.S.

The smart container market is projected to reach USD 0.96 billion by 2026.

Japan

The market is projected to reach USD 0.30 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for End-to-End Supply Chain Visibility Drives Product Adoption

The global shift toward real-time logistics visibility is significantly driving the adoption of the market. Companies now require continuous cargo monitoring to track position, temperature, and security status throughout complex multimodal routes. By embedding IoT sensors, GPS, and telematics, smart containers reduce losses, prevent spoilage, and improve asset utilization. This capability is vital in sectors such as pharmaceuticals, food, and electronics, where time-sensitive delivery and compliance are crucial. Enhanced transparency also supports predictive logistics and sustainability reporting, fueling demand in the smart container market during the forecast period. In March 2025, Folk Maritime became the Middle East’s first dry-container fleet to deploy ORBCOMM’s smart container technology, improving operational efficiency through real-time visibility.

MARKET RESTRAINTS

High Connectivity and Energy Costs Restrain Large-Scale Fleets Deployment

Despite their clear operational advantages, the widespread adoption of containers integrated with smart technologies is restrained by high connectivity and energy costs. Maintaining data transmission during transoceanic journeys often requires expensive satellite IoT communication rather than terrestrial networks, substantially raising operating expenses. Furthermore, powering onboard sensors and telematics for extended periods demands advanced and costly batteries or energy-harvesting systems. These factors increase the total cost of ownership and delay ROI for shipping operators managing large fleets.

MARKET OPPORTUNITIES

Emerging Regulatory Traceability Standards to Create Growth Opportunities in Market

Growing emphasis on regulatory compliance and traceability presents strong growth opportunities and demand for smart containers. Governments are increasingly enforcing digital cargo visibility, tamper-proof documentation, and real-time condition monitoring for perishable, pharmaceutical, and high-value goods. Smart technology-integrated containers equipped with blockchain-ready IoT sensors and geofencing capabilities offer verified chain-of-custody data, ensuring faster customs clearance and reduced fraud risk. Vendors that align their technologies with evolving global trade and customs standards can capture long-term government and logistics contracts. In February 2025, the Smart Container Alliance was launched to support traceability frameworks and establish unified data standards, advancing regulatory harmonization across global trade corridors. This is expected to boost the overall smart container market demand.

Smart Container Market Trends

Integration of AI and Predictive Analytics into Container Management Systems Boosts Market Expansion

One of the major smart container market trends is the integration of artificial intelligence and predictive analytics into container management systems. By analyzing continuous real-time data streams from IoT sensors, AI models can forecast maintenance needs, detect anomalies, and optimize routes based on traffic or weather conditions. This transition from reactive monitoring to predictive decision-making enables logistics providers to cut downtime and improve asset utilization. The adoption of AI-based analytics also drives new revenue streams through data services and efficiency gains. In June 2025, ORBCOMM launched CrewView, integrating vessel operations with container data to enable predictive and AI-driven decision-making.

MARKET CHALLENGES

Rising Cybersecurity Threats Challenge Safe Integration of Market Ecosystems

The rapid digitalization of logistics has made smart technology-integrated containers increasingly vulnerable to escalating cybersecurity threats. As containers communicate with shipboard networks, long-range wide area networkss, ports, and cloud systems, they become potential targets for data breaches, GPS spoofing, and malicious firmware attacks. A single vulnerability can compromise shipment integrity or disrupt entire global supply chains. Ensuring device authentication, encryption, and secure data transmission across thousands of connected units remains an operational and regulatory challenge for carriers. In January 2025, the U.S. Department of Homeland Security introduced the Cybersecurity in the Marine Transportation System rule, mandating stronger security standards for maritime IoT assets, including connected containers.

Download Free sample to learn more about this report.

Segmentation Analysis

By Container Type

Broad Utilization and Fleet Retrofit Programs Drive Dry Container Dominance

The container type segment covers dry containers, refrigerated containers, tank containers, and special-purpose containers.

The dry containers segment is projected to dominate the smart container market, accounting for 46.39% of the global market share in 2026. The dry container segment is dominating as it supports the widest variety of non-temperature-sensitive goods (electronics, garments, consumer goods) and thus captures the bulk of container traffic. Its dominance is reinforced by widespread retrofit programs, as upgrading existing dry boxes with sensors is more cost-effective than replacing entire fleets. Economies of scale, the proven reliability of sensor modules, and carriers’ familiarity with standard container formats further strengthen this segment’s leadership. In April 2024, Hapag-Lloyd launched its Live Position dry container tracking product, enabling door-to-door IoT visibility across its dry container fleet and eliminating blind spots in global logistics.

The refrigerated containers segment is the fastest-growing, driven by escalating cold-chain demands, stricter temperature-humidity control regulations, and rising volumes of perishable food, vaccines, and biologics.

By Component Type

Hardware Reliability and Sensor Innovation Sustain Hardware Segment Growth

In terms of component type, the market is categorized into hardware, connectivity, platform/software, and services.

The hardware segment is expected to lead by component type, contributing 44.71% globally in 2026, as sensors, GPS & communication modules, embedded controllers, and rugged enclosures form the indispensable physical backbone of smart container systems. Since hardware establishes the baseline for reliability, carriers and integrators prioritize investments in sensor durability, energy efficiency, and marine ratings. Once hardware is deployed across fleets, software and analytics can stack on top; however, hardware remains fundamental to market share and operational reliability.

The platform/software segment is expected to grow at the fastest CAGR, propelled by increasing demand for analytics, route optimization, anomaly detection, predictive maintenance, and real-time dashboards in logistics.

To know how our report can help streamline your business, Speak to Analyst

By End-user

Fleet Ownership and Global Networks Cement Shipping Lines /Ocean Carriers Segment Growth

By end-user, the market is segmented into shipping lines/ocean carriers, freight forwarders & 3PLs/NVOCCs, shippers/cargo owners, port operators & terminal authorities, rail & intermodal operators, and leasing companies & container fleet owners.

The shipping lines/ocean carriers segment is projected to remain the leading end user, accounting for 31.99% of the global market share in 2026, as these entities own and manage large container fleets, giving them both the incentive and capacity to deploy advanced, technology-integrated container systems. They benefit from improved utilization, risk reduction, theft prevention, and better customer transparency across maritime routes. Their scale and capital resources allow upfront investments in sensor retrofits across thousands of containers, reinforcing their dominance in adoption. In August 2025, Smart Freight Centre joined the Mærsk Mc-Kinney Møller Center for Zero Carbon Shipping as a Knowledge Partner to support decarbonization efforts and smart logistics deployment in maritime freight.

The freight forwarders & 3PLs/NVOCCs segment is the fastest-growing, as intermediaries increasingly adopt smart container solutions to offer high-visibility services and strengthen their competitive position through margin control.

By Vertical/Application

Traceability and Spoilage Reduction Reinforce Food & Beverage Logistics Segment Leadership

On the basis of vertical/application, the market is fragmented into food & beverage logistics, pharmaceutical & life sciences, electronics & high-value goods, automotive components, chemicals & petrochemicals, retail & e-commerce, and industrial & manufacturing goods.

The food & beverage logistics segment is dominating the industry, since it handles the highest volumes of perishable traffic, characterized by stringent freshness, traceability, and compliance requirements. Smart containers enable continuous monitoring of temperature, humidity, and shock, driving down spoilage and loss. As food supply chains are global and time-sensitive, carriers and producers have been among the earliest adopters of smart container technologies.

The pharmaceutical & life sciences vertical is the fastest-growing, driven by vaccine logistics, biologics shipments, strict regulatory and audit demands, and demand for end-to-end traceability.

By Deployment Type

Cost Efficiency and Fleet Modernization Support Retrofitted Containers Segment Dominance

Based on deployment type, the market is segmented into OEM-integrated smart containers, retrofitted containers, and disposable/single-use smart loggers.

The retrofitted containers segment is expected to dominate by deployment type, holding 57.94% of the global market share in 2026, as most shipping lines and container operators prefer upgrading existing assets rather than deploying entirely new builds. Retrofitting enables rapid scaling, mitigates capital expenditure, and allows phased rollouts. With advances in plug-and-play sensor kits and modular connectivity packages, retrofit adoption continues to grow, reinforcing dominance in product deployments.

The OEM-integrated smart containers segment is the fastest-growing, as new builds integrate sensors, power, connectivity, and data architecture during manufacturing, lowering long-term cost and improving system coherence.

Smart Container Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific Smart Container Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 2.82 billion in 2025, accounting for 50.72% share, and is expected to reach USD 3.06 billion in 2026. The region is also expected to witness the fastest-growing, propelled by rapid manufacturing, expansion of refrigerated exports, digitization of ports, and rising adoption of 5G/IoT in logistics. Nations such as China, India, and Southeast Asian states invest heavily in trade corridors and smart port infrastructure. Additionally, regional carriers are also leveraging this technology to differentiate via enhanced visibility services. In November 2024, TMA Solutions signed a strategic partnership with Tan Thanh Container to develop autonomous smart trailers and integrated monitoring systems for container transport in Vietnam. The Japan market is projected to reach USD 0.30 billion by 2026, the China market is projected to reach USD 1.61 billion by 2026, and the India market is projected to reach USD 0.33 billion by 2026.

North America

In 2025, the North America market stood at USD 1.31 billion, representing 23.56% of global demand, and is projected to grow to USD 1.4 billion in 2026. In the region, the growing push for end-to-end shipment visibility, tight cold-chain logistics requirements, and investments in maritime IoT are driving the uptake of these containers. Large U.S. carriers and refrigerated cargo operators demand precise temperature monitoring and theft protection. Additionally, government and customs modernization programs incentivize digital shipping documentation and traceability. In June 2025, KLOG Transport Solutions in Europe, which serves transatlantic and intra-EU routes, adopted ORBCOMM’s satellite IoT technology to overcome coverage gaps and ensure full visibility, including during North American segments of transit. The U.S. market is projected to reach USD 0.96 billion by 2026.

U.S.

In the U.S., the smart container market growth is fueled by the expansion of e-commerce, strict pharmaceutical cold-chain mandates, and federal infrastructure grants supporting port modernization. U.S. operators are among the early adopters of sensor-driven logistics, and regulations (FDA, USDA) require rigorous compliance. Additionally, tech partnerships continue to accelerate innovation. In July 2025, HARMAN and ORBCOMM announced a strategic collaboration to expand industrial IoT, data, and platform engineering capabilities, bolstering U.S. smart container solutions and accelerating regional deployments.

Europe

The Europe region captured 21.38% of the global market in 2025, generating USD 1.19 billion in revenue, and is projected to reach USD 1.26 billion in 2026. Europe’s adoption is driven by strict regulatory and environmental standards, cross-border trade complexity, and robust intermodal networks. Shippers demand carbon footprint visibility, product provenance, and high security across high-density trade corridors. Governments within the EU are supporting digital customs and green logistics programs. In June 2025, KLOG Transport Solutions (Portugal) deployed ORBCOMM’s satellite IoT stack to close visibility gaps across European rail corridors that lack cellular coverage. The UK market is projected to reach USD 0.22 billion by 2026 and the Germany market is projected to reach USD 0.35 billion by 2026.

Rest of the world

The Rest of the World market generated USD 0.24 billion in 2025, representing 4.34% of the global market landscape, and is expected to reach USD 0.26 billion in 2026. In the rest of the world, regions including Latin America, Africa, and the Middle East, the smart container market demand is being driven by increasing exports of perishables, demand for cold-chain in tropical climates, and infrastructure upgrades. Governments’ efforts to promote trade facilitation also encourage digitization in ports and customs. In March 2025, Folk Maritime, a Saudi regional feeder operator, became the first in the Middle East to deploy ORBCOMM’s smart dry container technology, signaling growing adoption across the broader Rest of World region.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements and OEM Collaborations by Key Players Define Competitive Landscape

The global smart container market is fiercely contested among technology firms, telematics providers, and container operators assembling vertical IoT stacks and analytics platforms. Companies such as Traxens, Orbcomm Inc., Globe Tracker, SM Group, and CMA CGM Group, which lead the market, differentiate through sensor innovation, deep analytics, connectivity models (LoRa, satellite, and hybrid), and strong logistics partnerships. Competition emphasizes interoperability, secure APIs, lifespan battery efficiency, and platform scalability across fleets and geographies. Strategic alliances with carriers, port authorities, and customs bodies help lock in customers and raise switching costs. In March 2025, Hoopo joined the SMDG (Standardisation in Maritime Data Group) as a member to bring smart technology-integrated container expertise into global EDI standards, boosting interoperability and promoting container intelligence adoption in maritime communications.

LIST OF KEY SMART CONTAINER COMPANIES PROFILED

- ORBCOMM (U.S.)

- Traxens (France)

- Globe Tracker (Denmark)

- Nexxiot (Switzerland)

- CIMC Smart Technologies (China)

- Seaco Global Ltd. (Singapore)

- Singamas Container Holdings Ltd. (China)

- Maersk Line (Denmark)

- Hapag-Lloyd AG (Germany)

- Emerson Electric Co. (U.S.)

- Sensitech Inc. (U.S.)

- Roambee Corporation (U.S.)

- Phillips Connect Technologies (U.S.)

- Hoopo Systems Ltd. (Israel)

- Arviem AG (Switzerland)

- Tive Inc. (U.S.)

- Eelink Communication Technology Co., Ltd. (China)

- Gurtam (Wialon Platform) (Lithuania)

- Samsara Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In September 2025, Hellmann Worldwide Logistics expanded its partnership with Siemens Smart Infrastructure by taking over management of Siemens’ central warehouse in Nuremberg. The collaboration integrates smart warehouse logistics and intelligent systems to enhance operational efficiency.

- In March 2025, Folk Maritime, serving Middle East-Asia routes, deployed ORBCOMM’s smart container monitoring across its fleet, underscoring demand for the product in Asia-adjacent corridors.

- In November 2024, ZIM Integrated Shipping accelerated the deployment of smart containers by integrating Hoopo’s hoopoSense Solar trackers across its global fleet. The solution offers a 12-year battery life, door-open alerts, and all-in-one tracking for enhanced operational visibility.

- In April 2025, Traxens publicly advocated for unified smart container standards and interoperability across shipping lines, reinforcing its position as a core provider and driving standardization momentum in the industry.

- In January 2024, ZIM Integrated Shipping signed an agreement with Hoopo Systems to deploy Hoopo’s tracking devices across its dry-van container fleet, reinforcing asset visibility, geofencing, door-open alerts, and fleet intelligence capabilities.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 7.3% from 2025-2032 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Container Type, By Component Type, By End-user, By Vertical/Application, By Deployment Type, and Region |

|

By Container Type |

|

|

By Component Type |

|

|

By End-user |

|

|

By Vertical/Application |

|

|

By Deployment Type |

|

|

By Geography |

North America (By Container Type, By Component Type, By End-user, By Vertical/Application, By Deployment Type, and Country)

Europe (By Container Type, By Component Type, By End-user, By Vertical/Application, By Deployment Type, and Country)

Asia Pacific (By Container Type, By Component Type, By End-user, By Vertical/Application, By Deployment Type, and Country)

Rest of the World (By Container Type, By Component Type, By End-user, By Vertical/Application, By Deployment Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market size is projected to grow from USD 5.97 billion in 2026 to USD 10.46 billion by 2034

In 2025, the market value stood at USD 5.57 billion.

The market is expected to exhibit a CAGR of 7.25% during the forecast period (2026-2034).

The dry container segment leads the market by container type.

Rising Demand for end-to-end supply chain visibility is a key factor driving the market.

Key players in the smart container market, include Traxens, Orbcomm Inc., Globe Tracker, Smart Containers Group, and CMA CGM Group, dominate the market.

Asia Pacific held the largest share of the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us