Smart EV Charging Networks Market Size, Share & Industry Analysis, By Charging Level (Level 1 (Low Power AC), Level 2 (Medium Power AC), and DC Fast Charging (High Power)), By Deployment (Residential and Commercial), By Grid Interaction Capability (Unidirectional Smart Charging and Bidirectional Charging Enabled Networks), By Connectivity Technology (Cellular (4G/5G), Wi-Fi/Ethernet, Power Line Communication (PLC), and RF/IoT-Based Networks), and Regional Forecast, 2026-2034

Smart EV Charging Networks Market Size and Future Outlook

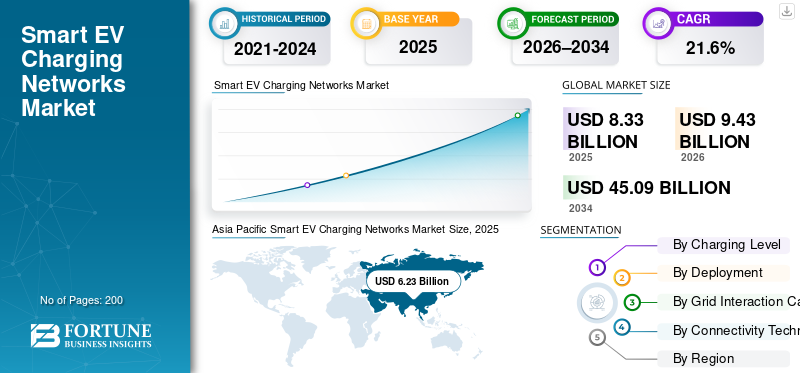

The global smart EV charging networks market size was valued at USD 8.33 billion in 2025. The market is projected to grow from USD 9.43 billion in 2026 to USD 45.09 billion by 2034, exhibiting a CAGR of 21.6% during the forecast period. Asia Pacific dominated the smart EV charging networks market with a market share of 74.79% in 2025.

The market refers to integrated, software-enabled charging infrastructure that optimizes electric vehicle charging through connectivity, data analytics, load management, and grid integration for efficient, scalable mobility support.

Key drivers include rising EV adoption, government incentives, grid modernization, renewable integration, urbanization, smart energy management demand, cost optimization, and need for scalable, interoperable charging infrastructure across residential commercial fleets.

The smart EV charging networks market is led by key players such as ChargePoint, ABB, Siemens, Schneider Electric, Tesla, Shell Recharge, EVBox, and BP Pulse. These companies focus on expanding charging networks across residential, commercial, and public applications. Strong emphasis is placed on advanced software platforms, energy management, and grid integration. Strategic partnerships, acquisitions, and geographical expansion remain key competitive strategies.

Download Free sample to learn more about this report.

Smart EV Charging Networks Market Key Takeaways

- 2025 Market Size: USD 8.33 billion

- 2026 Market Size: USD 9.43 billion

- 2034 Forecast Market Size: USD 45.09 billion

- CAGR: 21.60% (2026–2034)

- Asia Pacific dominated the market with a 74.79% share in 2025.

- The DC Fast Charging (High Power) segment held the largest market share.

- The Commercial Deployment segment dominated the market due to widespread installation across public charging stations.

Asia Pacific

Asia Pacific dominated the global market and is expected to remain the fastest-growing region, driven by strong EV adoption, government incentives.

North America

North America is the third-largest market, supported by rising EV adoption, government funding, and expansion of smart charging infrastructure.

Europe

Europe is the second-largest regional market and is projected to grow at a 20.9% CAGR during the forecast period.

U.S.

U.S. market is estimated to reach USD 0.09 billion by 2026.

Japan

Japan market is estimated to reach USD 0.18 billion by 2026.

Read More

SMART EV CHARGING NETWORKS MARKET TRENDS

Growth of Software-Defined and AI-Driven Charging Networks as a Market Trend

A major trend shaping the smart EV charging networks market is the shift toward software-defined, AI-enabled platforms. Charging infrastructure is increasingly differentiated by intelligence rather than hardware alone. Advanced software enables real-time monitoring, predictive maintenance, dynamic pricing, and automated load balancing across multiple locations. Artificial intelligence and machine learning algorithms optimize charger utilization, forecast demand, and reduce downtime. Cloud-based platforms allow seamless scalability and remote management of large charging networks. Interoperability standards and open protocols are also gaining traction, enabling integration with utilities, fleet management systems, and energy markets. This software-centric evolution is transforming charging networks into data-driven energy management ecosystems.

MARKET DYNAMICS

MARKET DRIVERS

Rising Electric Vehicle Adoption and Policy Support to Drive Market Expansion

Rapid growth in electric vehicle adoption globally is a primary driver for the smart EV charging networks market. Governments across major economies are enforcing stricter emission norms, offering EV purchase subsidies, and funding public charging infrastructure. These measures are accelerating EV penetration across passenger vehicles, commercial fleets, and shared mobility. As vehicle volumes rise, the need for intelligent, connected charging networks capable of managing load, billing, authentication, and energy optimization becomes critical. Smart charging networks enable utilities and operators to balance demand, reduce peak loads, and integrate renewable energy sources. Additionally, fleet electrification by logistics, ride-hailing, and public transport operators is further driving the demand for centralized, software-driven charging ecosystems.

- In November 2024, the U.S. Department of Transportation announced USD 635 million in awards under the Charging and Fueling Infrastructure (CFI) program to accelerate EV charging buildout, supporting the policy-led expansion.

MARKET RESTRAINTS

Low Utilization Rates in Early-Stage Markets to Restrain Revenue Generation

In several regions, especially in early-stage EV adoption markets, low charger utilization rates may restrain the smart EV charging networks market growth. While infrastructure deployment is increasing, the EV penetration in these markets remains limited, resulting in underused charging assets. This mismatch between infrastructure rollout and vehicle adoption delays return on investment for network operators. Low utilization impacts revenue stability, making it difficult to justify expansion or advanced software upgrades. Public and semi-public charging point stations are particularly affected, as demand patterns are still evolving. Until EV adoption reaches critical mass, subdued utilization levels will continue to restrain profitability and slow large-scale smart charging network investments.

MARKET OPPORTUNITIES

Integration of Renewable Energy and Energy Storage to Create Growth Opportunities

The convergence of smart EV charging networks with renewable energy and energy storage systems presents a significant opportunity. Smart charging platforms can align EV charging schedules with solar or wind power availability, improving grid stability and reducing carbon intensity. Integration with battery energy storage allows operators to store off-peak energy and deploy it during peak demand, enhancing economic viability. Vehicle to grid (V2G) and vehicle-to-building (V2B) technologies further expand revenue streams by enabling EVs to act as distributed energy resources. As utilities and governments prioritize decarburization and grid resilience, charging networks that offer advanced energy orchestration capabilities are well-positioned to gain long term competitive advantage.

- In January 2025, the U.S. Department of Energy released a Vehicle-Grid Integration (VGI) assessment and roadmap, supporting opportunities such as smart load coordination, bidirectional charging, and grid-friendly charging orchestration.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Lack of Standardization and Interoperability to Remain a Key Market Challenge

The absence of universal standards across charging hardware, communication protocols, and software platforms remains a critical challenge. Fragmentation across regions and manufacturers leads to compatibility issues between chargers, vehicles, payment systems, and network operators. This complexity increases deployment costs, limits roaming capabilities, and can negatively impact user experience. For charging network operators, managing multi-vendor environments complicates maintenance and system integration. From a consumer perspective, inconsistent authentication, pricing transparency, and access methods reduce confidence in public charging infrastructure. While industry bodies are working toward common standards, slow alignment across stakeholders continues to challenge the seamless scaling of smart EV charging networks globally.

Segmentation Analysis

By Charging Level

Rapid Highway Deployment and Fleet Electrification to Propel DC Fast Charging Segmental Dominance

Based on segmentation by charging level, the market is classified into Level 1 (low power AC), Level 2 (medium power AC), and DC fast charging (high power).

The DC fast charging (high power) segment dominates the smart EV charging networks market due to its critical role in enabling long-distance travel, high vehicle throughput, and fleet operations. High-power chargers significantly reduce charging time and increase charging speed making them essential for highways, urban fast-charging hubs, commercial fleets, and ride-hailing services. Governments and private operators prioritize DC ultra-fast chargers for public infrastructure projects to address range anxiety and support mass EV adoption. Their compatibility with next-generation EVs, coupled with growing investments by oil & gas majors and utilities, ensures strong utilization rates and sustained network expansion.

The Level 2 charging segment holds the second-largest market share and is expected to grow at a CAGR of 21.0% over the forecast period. The segment growth is driven by expanding residential, workplace, and destination charging installations, supported by lower costs, easier grid integration, and longer vehicle dwell times.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

High Utilization across Public and Fleet Depots to Propel Commercial Deployment Segmental Dominance

In terms of deployment, the market is categorized into residential and commercial.

The commercial deployment segment dominates the smart EV charging networks market due to widespread installation across public charging stations, workplaces, retail centers, highways, and fleet depots. High traffic volumes and multi-vehicle usage result in superior charger utilization compared to residential settings. Commercial sites increasingly deploy smart networked chargers to enable load management, dynamic pricing, access control, and remote monitoring. Government-backed public charging programs and private investments from utilities, oil & gas companies, and charging network operators further strengthen commercial dominance, supporting scalable infrastructure expansion and recurring service revenues.

The residential deployment segment represents the second largest smart EV charging networks market share and is projected to grow at a CAGR of 20.6% over the forecast period. Increasing EV ownership, preference for overnight home charging, and declining Level 2 charger costs continue to support steady residential smart charging adoption.

By Grid Interaction Capability

Grid Stability and Optimized Load Management to Propel Unidirectional Smart Charging Segmental Dominance

Based on grid interaction capability, the market is segmented into unidirectional smart charging and bidirectional charging enabled networks.

The unidirectional smart charging segment dominates the market due to its widespread deployment, technological maturity, and compatibility with existing grid infrastructure. These systems enable controlled energy flow from the grid to electric vehicles, allowing load balancing, peak shaving, and time-of-use optimization. Utilities and charging operators prefer unidirectional solutions as they are easier to integrate, cost-effective, and supported by most EV models. Their extensive use across residential, commercial, and public charging applications ensures high adoption rates and consistent network scalability.

The bidirectional charging enabled networks segment is the fastest-growing segment and is projected to expand at a CAGR of 23.2% over the forecast period. The segmental expansion is driven by vehicle-to-grid and vehicle-to-building applications, enabling EVs to act as distributed energy assets and support grid resilience.

By Connectivity Technology

Wide-Area Coverage and Real-Time Network Control to Propel Cellular Connectivity Segmental Dominance

Based on connectivity technology, the market is segmented into Cellular (4G/5G), Wi-Fi/Ethernet, Power Line Communication (PLC), and RF/IoT-based networks.

The cellular (4G/5G) connectivity segment dominates the smart EV charging networks market due to its ability to support wide-area deployments, real-time data transmission, and reliable remote management. Public and commercial charging stations rely on cellular networks for seamless communication without dependence on local infrastructure. High bandwidth and low latency enable advanced features such as dynamic pricing, remote diagnostics, firmware updates, and grid coordination. The rapid rollout of 5G further enhances scalability, security, and responsiveness, reinforcing cellular connectivity as the preferred choice for large, geographically distributed charging networks.

The Wi-Fi/Ethernet segment represent the second-largest connectivity segment, supported by a projected CAGR of 21.5% over the forecast period. These technologies are widely adopted in residential, workplace, and depot-based charging environments where stable local networks already exist.

Smart EV Charging Networks Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Smart EV Charging Networks Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the smart EV charging networks market and is also the fastest-growing region, driven by rapid EV adoption in China, Japan, South Korea, and emerging Southeast Asian economies. Strong government mandates, large-scale public charging investments, and aggressive electrification targets support network expansion. High urban density and growing electric two-wheeler, passenger car, and fleet adoption accelerate the demand for smart, high-utilization charging solutions. Domestic manufacturers and utilities actively deploy software-enabled networks, reinforcing regional leadership.

China EV Charging Networks Market

The China market is estimated to touch around USD 6.55 billion in 2026, accounting for a dominant share. Growth is driven by large EV parc, government mandates, and dense public fast-charging deployment.

Japan EV Charging Networks Market

In 2026, the Japan market is estimated to reach a value of around USD 0.18 billion, accounting for a modest share. Growth is supported by grid-integrated charging, urban electrification, and OEM-led smart infrastructure initiatives.

Europe

Europe represents the second-largest market share and is expected to grow at a CAGR of 20.9% over the forecast period. Stringent emission regulations, strong renewable energy integration, and well-defined EV policies drive smart charging adoption. Countries such as Germany, the Netherlands, France, and the Nordics focus on grid-integrated, interoperable charging networks. The high penetration of home, workplace, and public charging combined with the early adoption of vehicle-to-grid initiatives supports regional smart EV charging networks market growth.

Germany EV Charging Networks Market

In 2026, the Germany market is estimated to touch a valuation of around USD 0.49 billion, accounting for a significant share in the Europe market. Strong growth is driven by renewable integration, strict emission norms, and widespread public and workplace charging.

North America

North America ranks as the third-largest market, supported by rising EV penetration in the U.S. and Canada and large-scale public infrastructure funding. Federal and state-level incentives, along with utility-led smart grid programs, are accelerating the deployment of networked charging stations. Strong presence of leading charging network operators and technology providers drives innovation in software platforms, load management, and payment & charging systems. Growth is further supported by expanding commercial fleets and highway fast-charging corridors.

U.S. EV Charging Networks Market

The U.S. market is estimated to reach around USD 0.09 billion in 2026, accounting for a smaller share. Growth is supported by federal funding, highway fast-charging corridors, and expanding commercial fleet electrification.

Rest of the World

The market in the rest of the world is gradually expanding, led by parts of Latin America, the Middle East, and select African countries. Growth is driven by urban electrification initiatives, pilot EV programs, and increasing private-sector investment in public charging infrastructure. While EV penetration remains relatively low, improving grid infrastructure and declining charger costs are encouraging adoption. Government-led smart city projects and fleet electrification initiatives are expected to support long-term market development.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Deploy Large-Scale and Networked Charging Infrastructure to Strengthen Market Positions

The smart EV charging networks market is dominated by established charging network operators and global power and automation leaders such as ChargePoint, ABB, Siemens, Schneider Electric, Tesla, Shell Recharge, BP Pulse, and EVBox. These players leverage extensive hardware portfolios, software platforms, and utility partnerships to deploy large-scale, networked charging infrastructure across public, commercial, and fleet locations. Their offerings span DC fast chargers, Level 2 AC chargers, cloud-based network management systems, payment platforms, and energy management solutions, enabling end-to-end charging ecosystem integration.

Key market participants are increasingly focusing on software differentiation through AI-driven load management, real-time monitoring, predictive maintenance, and dynamic pricing capabilities. Strategic collaborations with utilities, renewable energy providers, and cloud technology firms support grid integration, data analytics, and scalable platform deployment. Additionally, companies are pursuing geographical expansion, acquisitions, roaming agreements, and investments in vehicle-to-grid readiness to strengthen competitive positioning amid intensifying global EV adoption.

LIST OF KEY SMART EV CHARGING NETWORK COMPANIES PROFILED

- ChargePoint Holdings, Inc (U.S.)

- Tesla, Inc. (U.S.)

- ABB Ltd. (Switzerland)

- Siemens AG (Germany)

- Schneider Electric (France)

- EVgo Inc. (U.S.)

- BP Pulse (U.K.)

- EVBox Group (Netherlands)

- Shell Recharge (Netherlands)

- Electrify America, LLC (U.S.)

- Blink Charging Co (U.S.)

- Tritium (Australia)

- Wallbox Chargers Inc. (Spain)

KEY INDUSTRY DEVELOPMENTS

- January 2026: U.K.-based charging network operator Osprey Charging reported 158% annual sales growth, operating 1,500 rapid chargers across 400+ locations while securing USD 138 million in debt to expand infrastructure using its Iris platform.

- January 2026: U.K.-based Connected Kerb achieved 82.7% sales growth, deploying almost 10,000 EV charging points and securing USD 90 million funding to install 30,000 more by 2028.

- January 2026: Walmart announced plans to install 400 kW fast EV chargers at 78 parking lots across 19 U.S. states, targeting charging deserts to boost convenience and attract EV drivers amid fading federal incentives.

- January 2026: EV charging startup RoadGrid raised USD 1.33 million in pre-Series A funding to scale manufacturing, software, and nationwide charging deployments in India, backed by Venture Catalysts and angel investors.

- October 2025: India announced plans to expand public EV chargers to 3,079 stations by November, aiming to support rising EV registrations, but experts flagged the target as insufficient for demand.

- April 2025: Amic Energy expanded its fast EV charging footprint in Austria, adding multiple charging stations at commercial locations and retail partnerships to strengthen regional infrastructure.

- March 2025: GM, EVgo, and Pilot expanded their coast-to-coast EV charging network to 130 truck stop locations across 25 U.S. states, pushing broader fast-charging access along major interstates for long-distance travel.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 21.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Charging Level, By Deployment, By Grid Interaction Capability, By Connectivity Technology, and By Region |

|

By Charging level |

· Level 1 (Low Power AC) · Level 2 (Medium Power AC) · DC Fast Charging (High Power) |

|

By Deployment |

· Residential · Commercial |

|

By Grid Interaction Capability |

· Unidirectional Smart Charging · Bidirectional Charging Enabled Networks |

|

By Connectivity Technology |

· Cellular (4G/5G) · Wi-Fi / Ethernet · Power Line Communication (PLC) · RF / IoT-Based Networks |

|

By Geography |

· North America (By Charging Level, By Deployment, By Grid Interaction Capability, By Connectivity Technology, and by Country) o U.S. (By Deployment) o Canada (By Deployment) o Mexico (By Deployment) · Europe (By Charging Level, By Deployment, By Grid Interaction Capability, By Connectivity Technology, and by Country) o Germany (By Deployment) o U.K. (By Deployment) o France (By Deployment) o Rest of Europe (By Deployment) · Asia Pacific (By Charging Level, By Deployment, By Grid Interaction Capability, By Connectivity Technology, and by Country) o China (By Deployment) o Japan (By Deployment) o India (By Deployment) o Rest of Asia Pacific (By Deployment) · Rest of the World (By Charging Level, By Deployment, By Grid Interaction Capability, By Connectivity Technology, and by Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.33 billion in 2025 and is projected to reach USD 45.09 billion by 2034.

In 2025, the market value stood at USD 6.23 billion.

The market is expected to exhibit a CAGR of 21.6% during the forecast period of 2026-2034

The commercial segment leads the market by deployment.

Increased vehicle connectivity and telematics integration are key factors driving the market growth.

Asia Pacific dominates the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us