Smart Faucets Market Size, Share & Industry Analysis, By Type (Touchless, Touch-Activated, and Voice-Activated), By Application (Bathroom and Kitchen), By End-User (Residential and Commercial), By Distribution Channel (E-commerce/Online and Retail Outlets/Offline), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

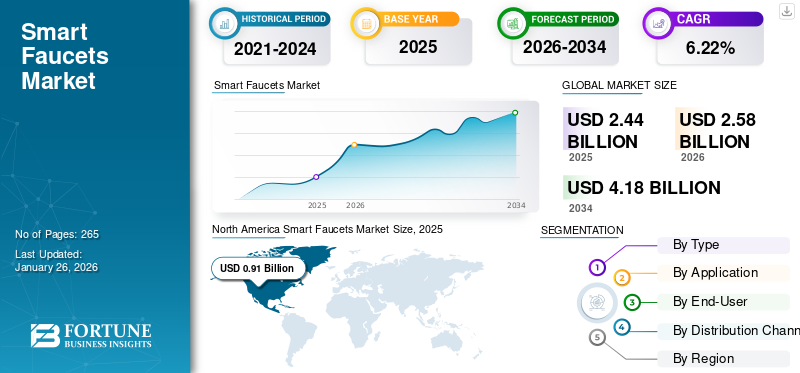

The global smart faucets market size reached USD 2.44 billion in 2025 and is projected to grow from USD 2.58 billion in 2026 to USD 4.18 billion by 2034, exhibiting a CAGR of 6.22% over the forecast period. North America dominated the smart faucets market with a market share of 37.17% in 2025.

Smart faucets are the advanced plumbing fixture that uses infrared sensors and motion detection to control the water flow and temperature in various residential and commercial settings. These faucets serve multiple purposes, which includes providing access to clean water for cooking, drinking, and hygiene, as well as for washing dishes or hands and filling containers while improving water efficiency. The technological advancements in faucets covers features, such as touchless operation, temperature control, water conservation capabilities, and connectivity with smart home technologies via Wi-Fi, Bluetooth, or voice control assistants such as Google Assistant and Alexa. Key market drivers include rising awareness regarding water conservation, advancements in sensor technologies, and growing adoption of smart homes.

Key players in the market include Kohler Co., Lixil Group, Moen Incorporated, Delta Faucet Company, and Hansgrohe SE. Major strategies adopted by leading companies include integrating advanced features such as touchless operation, voice activation, and temperature control to enhance user experience, convenience, and hygiene.

Download Free sample to learn more about this report.

GLOBAL SMART FAUCETS MARKET SNAPSHOT

Market Size & Forecast:

- 2025 Market Size: USD 2.44 billion

- 2026 Market Size: USD 2.58 billion

- 2034 Forecast Market Size: USD 4.18 billion

- CAGR: 6.22% from 2026–2034

Market Share:

- North America dominated the market with a 37.17% % share in 2025, driven by widespread smart home adoption and strong tech integration in residential and commercial infrastructure.

- Touchless faucets held the largest market share in 2024, fueled by hygiene concerns and demand for hands-free use in bathrooms and kitchens.

- Retail outlets/offline channels led distribution due to product demonstrations and after-sales support, while e-commerce is growing fastest on digital convenience and influencer marketing.

Key Country Highlights:

- U.S.: Largest contributor in North America; strong demand from hospitals, offices, and homes using voice-activated and app-connected faucets.

- Canada & Mexico: Rapid adoption driven by smart home trends and water conservation initiatives in commercial and public infrastructure.

- Germany & U.K.: Sustainability regulations and high disposable incomes boost premium smart fixture sales in home renovations.

- China & India: Fastest growth fueled by urbanization, rising middle class, and smart city infrastructure development.

- UAE & Brazil: Water scarcity concerns and upscale property development increase demand for eco-efficient, touchless fixtures in hotels and malls.

SMART FAUCETS MARKET TRENDS

Growing Emphasis on Eco-Friendly and Water Conserving Innovations are Emerging New Market Trends

An emerging trend in the market include growing emphasis on eco-friendly and cutting-edge water-saving technologies. Manufacturers are designing and developing faucets with features such as real-time water usage tracking, customizable flow rates, and automatic shutoff to minimize water wastage. These innovations cater to environmentally conscious consumers and support global sustainability goals. With growing demand and increasing regulatory pressure for green products, advanced faucets are becoming a standout segment, blending efficiency with environmental responsibility in modern kitchens and bathrooms.

MARKET DYNAMICS

Market Drivers

Rising Demand for Touchless and Hygienic Solutions to Fuel Market Growth

The growing emphasis on hygiene and contactless technologies especially after the COVID-19 pandemic has significantly shifted preference for smart faucets amongst consumers. For instance, according to the report by World Health Organization (WHO), published in 2022, contactless products are forecasted to expand by 20% annually, with environments prioritizing hygiene and safety. These devices minimize physical contact, reducing the spread of germs and cross-contamination in residential, commercial, and institutional settings. Restaurants, hospitals, and public restrooms are rapidly integrating smart taps systems to enhance sanitation standards, which is fueling the smart faucets market growth.

Integration of Smart Home Technology to Increase Product Adoption

The rising trend of smart home technologies has led consumers to adopt connected devices that offer convenience, efficiency, and automation. Advanced faucets, equipped with features such as voice command, temperature control, and water usage monitoring, align perfectly with this trend. Integration with smart home systems such as Alexa or Google Assistant further enhances their appeal, leading the adoption among tech-savvy homeowners and contributing to the market’s expansion.

Market Restraints

High Installation and Maintenance Costs to Restrain Market Growth

The market faces major growth limitations due to high cost of smart faucets, including purchase, installation, and the need for skilled professionals to setup the smart product. Additionally, maintenances and repair costs can be significantly higher compared to traditional faucets, deterring budget-conscious consumers. The residential uses who might not see immediate value in the investments are hesitant to use the product. While, in commercial settings, retrofitting existing infrastructure to support smart taps can also incur substantial expenses. Moreover, the integration of advanced features such as sensors, connectivity, and app controls increases the likelihood of technical issues, further deterring smart faucets market growth.

Market Opportunity

Rising Demand in Commercial and Hospitality Sectors to Offer Lucrative Growth Opportunities

Expanding adoption of smart plumbing fixture solutions across commercial and hospitality industries provides numerous growth opportunities for manufacturers. Hotels, restaurants, airports, malls, and corporate office spaces are increasingly investing in advanced fixtures to enhance hygiene, improve user experience, and reduce water wastage. Touchless-technologies and water-saving features aligns well with sustainability goals, making these solutions more attractive for high-traffic environments. Additionally, the premium appeal of such solutions adds value to upscale properties. As businesses prioritize smart infrastructure and eco-friendly practices, this sector offers strong growth potential for manufacturers and solution providers in the industry.

Market Challenge

Increasing Concern of Data Privacy and Lack of Security to Pose as Challenge

Ensuring data privacy and cybersecurity stands as key challenge in the smart plumbing fixtures market. As these devices often connect to home networks and mobile apps, they can be vulnerable to hacking and unauthorized access. Users may hesitate to adopt such technology due to the fear of data misuse or breaches. Manufacturers must implement strong encryption and secure data protocols, but building consumer trust remains difficult, especially as cyber threats continue to evolve rapidly in the IoT landscape.

Impact of COVID-19

Initially, COVID-19 negatively affected the market due to global chain disruption, factory shutdowns, and reduced construction activity. Consumer spending declined amid economic uncertainty, delaying home improvement projects and commercial installations. These factors led to slowed production and lower sales, temporarily stalling market growth. However, hygiene-driven demand later spurred market recovery. Consumers sought contactless solutions, boosting adoption in home and public spaces. Manufacturers such as Delta Faucet expanded offering with voice-activated models reflecting broader trend towards smart, health-conscious living environments.

SEGMENTATION ANALYSIS

By Type

Modern Aesthetics and Tech Appeal Led to the Highest Share of Touchless Segment

Based on type, the market is segmented into touchless, touch-activated, and voice-activated.

The touchless segment exhibited a majority market share, accounting for 56.20% of the market share in 2026. These touchless faucets offer convenience by responding to the user’s presence and hand movement, allowing for a contactless enhanced hygienic experience. Touchless faucets work using magnetic docking system located within the spout. The demand for touchless faucets experienced surge especially after COVID-19 pandemic to minimize cross-contamination.

Touch-activated faucets segment is expected to grow at the fastest CAGR during the forecast years. Such advanced faucets systems permit users to start and stop the stream of water with a single touch. These taps adds sleek and modern look to kitchens and bathrooms and appeal to tech-savvy consumers who enjoy smart phone upgardes.

To know how our report can help streamline your business, Speak to Analyst

By Application

Hands-Free Hygiene and Compact Design Needs Spurred Bathroom Segment Growth

Based on application, the market is bifurcated into bathroom and kitchen.

The bathroom segment accounted for the majority of the smart faucets market share, accounting for 62.02% of the market share in 2026. In bathroom, users often prefer avoiding touching fixtures after using the toilet or before brushing teeth. Moreover, faucets that dispense water at preset temperatures and duration are favored in bathroom routines, reducing waste and optimizing usage, which market growth.

Kitchen segment is projected to grow at the fastest CAGR over the forecast period 2026-2034. Reducing touchpoints when dealing with raw meat or sticky ingredients helps prevent contamination, which is a major concern in kitchen. Also, kitchens are among the most-used spaces in a home, so consumers are more willing to invest in smart upgrade that makes everyday tasks rapid and easier.

By End-User

Lifestyle Improvements and More Receptiveness to Premium Products Boosts Residential Segment Expansion

Based on end-user, the market is segmented into residential and commercial.

The residential segment dominated the global market, accounting for 63.95% of the market share in 2026. Growing consumer interest in smart home technology, hygiene, and convenience boosts smart tap systems adoption in residential segment. Homeowners are increasingly adopting touchless and voice-activated faucets in kitchens and bathrooms to improve cleanliness, reduce water waste, and elevate the modern aesthetic of their living spaces.

On the other hand, commercial end-user including hotels, offices, restaurants, hospitals, and more are projected to grow at the fastest CAGR over the forecast period. The adoption of advanced faucets is growing primarily for hygiene and water conservation purpose. These faucets help reduce touchpoints in high-traffic public areas and support sustainability goals.

By Distribution Channel

Installation Services and After-Sales Support of Retail Outlets to Fuel Segment Growth of Retail Outlets/Offline

Based on distribution channel, the market is segmented into e-commerce/online and retail outlets/offline.

The retail outlets/offline segment accounted for the largest market share, accounting for 79.07% of the market share in 2026. Offline stores allow for live demonstration, which helps in showcasing the features of the advanced faucets including motion sensors, temperature control, and app connectivity. Users can understand the quality of the smart faucets and other product attributes while shopping products from specialty sanitaryware shops. Increasing product purchases from these from specialty sanitaryware shops drives the segment at a second fastest growth rate during 2025-2032

The e-commerce/online segment is anticipated to expand at the highest CAGR over the assessment period from 2025-2032. Wide product selection due to broader inventory and easy accessibility of advanced faucets on online platforms such as Amazon, Wayfair, and other manufacturer websites have attracted more consumers. Online platforms offer more models, brands, and price points than typical offline stores. Additionally, online reviews, YouTube demos, and influencer content help buyers make informed decisions without needing in-person sales representative, which is further expected to boost segmental growth.

Smart Faucets Market Regional Outlook

Regionally, the market is divided into North America, South America, Europe, Asia Pacific, and the Middle East & Africa.

North America

North America Smart Faucets Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the North America market stood at USD 0.91 billion, representing 37.17% of global demand, and is projected to grow to USD 0.95 billion in 2026. The region's growth is driven by rising demand for smart homes where consumers are more inclined to install smart plumbing fixtures such as faucets to enhance convenience, efficiency, and connectivity. Strong adoption of advanced technology led by tech-savvy consumers, has fueled the market growth in the region.

U.S., accounted for the majority of the share in North America market and the growth is mainly driven by developed commercial infrastructure including healthcare, hospitality, and corporate spaces, that supports adoption of smart plumbing fixtures. Additionally, integration of IoT technologies into advanced faucets aligns strongly with the rising penetration of smart home ecosystems in the country, further consolidating market growth. The US market is projected to reach USD 0.78 billion by 2026.

Download Free sample to learn more about this report.

Europe

The Europe region captured 30.74% of the global market in 2025, generating USD 0.75 billion in revenue, and is projected to reach USD 0.8 billion in 2026. Europe stood at a second position in the global market in 2024 and is projected to grow at second highest CAGR over the forecast years. Rising investments in upgrading residential and commercial properties, specifically in urban centers, contributes to market expansion. Strong emphasis on sustainability and water conservation further leads businesses and consumers to adopt water-saving systems such as advanced faucets. Moreover, in Europe higher income levels allow consumers to spend more on premium smart home upgrades. The UK market is projected to reach USD 0.11 billion by 2026, while the Germany market is projected to reach USD 0.14 billion by 2026.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 0.57 billion in 2025, accounting for 23.16% share, and is expected to reach USD 0.6 billion in 2026. The growing middle-class population, rising standards of living, and rising disposable income in these emerging economies have triggered adoption of modern home and commercial fixtures such as cutting edge faucets solutions. Moreover, water consumption takes up a significant share of a building’s utility cost. Thus, smart sanitary ware and bathroom fittings integrated with temperature lock and low-flow function helps reduce water consumption considerably, driving product adoption. In addition, environmental sustainability movements have prompted end-users to invest in advanced water-conservation technologies. The Japan market is projected to reach USD 0.13 billion by 2026, the China market is projected to reach USD 0.2 billion by 2026, and the India market is projected to reach USD 0.08 billion by 2026.

South America and the Middle East & Africa

The Middle East & Africa market accounted for USD 0.08 billion in 2025, representing 3.23% of the global industry, and is expected to reach USD 0.08 billion in 2026. South America accounted for USD 0.14 billion in 2025, representing 5.70% of the global market share, and is projected to reach USD 0.14 billion in 2026. The South America and the Middle East & Africa market is projected to witness notable growth over the coming years as these regions faces water scarcity on large scale due to climate change and rapid urbanization. UAE, Israel, Saudi Arabia, Jordan, Kuwait, Libya, Lebanon, Bahrain, Oman, among others are listed in the category of countries experiencing extremely low baseline water stress which is likely to build the demand for smart faucets.

Competitive Landscape

Key Industry Players

Innovative Features and Aesthetic Design Drive Demand, Forcing Brands to Evolve Market Strategies

Key players in the market compete through innovation, pricing, product differentiation, and distribution channel. Manufacturer in the market are forming strategic partnerships with smart home platforms to expand ecosystem compatibility. Customization options and sleek designs are also gaining traction to appeal to style-conscious consumers. Furthermore, businesses are investing in online and offline marketing to boost brand visibility and are expanding into emerging markets with growing smart home adoption. Continuous R&D, sustainable manufacturing, and energy-efficient products are becoming crucial differentiators to gain and retain market share in this rapidly evolving industry.

LIST OF KEY SMART FAUCETS COMPANIES PROFILED IN THE REPORT

- Kohler Co. (U.S.)

- Moen Incorporated (U.S.)

- LIXIL Group (Japan)

- Delta Faucet Company (U.S.)

- Hansgrohe SE (Germany)

- Roca Sanitario, S.A. (Spain)

- Jaquar Group (India)

- TOTO Ltd. (Japan)

- CERA Sanitaryware Ltd. (India)

- Pfister (U.S.)

Key Industry Developments

- July 2024: Studio McGee and Kohler together created six collection of kitchen and bathroom outfitting, including faucets, vanities, and light fixtures for a wide range of interior design styles. The Edalyn Kitchen Faucet Collection features four kitchen faucet varieties and a wall-mounted pot filler. Another range, Castia Bathroom Faucet Collection, offers sleek yet aesthetic and classic bath fixtures in multiple finishes.

- May 2024: U.S.-based, Delta Faucet Company, announced the launch of Touch2O with Touchless Technology. The contactless technology makes multi-tasking even easier and mess-free by offering three ways to control the water flow: placing a hand near the faucet to activate the motion sensor, using the standard handle for manual control, or tapping anywhere on the faucet surface.

- February 2024: Delta Faucet unveiled a range of innovative kitchen and bathroom products using their Touch₂O with Touchless Technology that lets user take control of water flow through motion, flow, or manual control. Designed for convenience and modern living, this range features a TempSense Indicator that changes color based on water temperature.

- January 2022: Moen Incorporated, an American product line of faucets and other fixtures, launched Smart Faucet with Motion Control at Consumer Electronic Show (CES) 2022. This unique Motion Control technology is so advanced, that the faucet is designed without a handle and can be operated with simple hand motions. The range also offers features and benefits of the other Moen Smart Faucets including four ways to control the faucet, voice-activated capabilities, and remote management and activation with the Moen Smart Water App.

- February 2021: Jaquar Group, India-based, bathroom and lighting company, launched exclusive Blush Sensor range of faucets with sensory intelligence. The range smartly integrates high-precision, new-gen, quick-response sensor technology promoting touch-free and germ-kill functionalities for reduction of energy and water consumption.

REPORT COVERAGE

The smart faucets market report provides a detailed analysis of the market and focuses on key aspects such as the competitive landscape, services, and leading product types. It also offers global market industry trends and insights and highlights key industry developments. In addition to the aforementioned factors, the report on the global market outlook includes several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.22% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Application

|

|

|

By End-User

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the worldwide market size was USD 2.44 billion in 2025 and is anticipated to reach USD 4.18 billion by 2034.

In 2025, the global market stood at USD 2.44 billion.

The market will grow at a CAGR of 6.22% and exhibit a steady growth rate during the forecast period.

By type, the touchless faucets segment dominated the market.

Rising awareness regarding water conservation, advancements in sensor technologies, and growing adoption of smart homes drive global market growth.

Kohler Co., Moen Incorporated, LIXIL Group, Delta Faucet Company, and Hansgrohe SE are among the few significant players in the global market.

North America held the highest market share in 2025.

Growing emphasis on eco-friendly and cutting-edge water-conserving technologies is likely to drive the markets growth.

- 2021-2034

- 2025

- 2021-2024

- 265

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us