Smart Module Market Size, Share & Industry Analysis, By Type (Communication Modules, Processor, Sensor Modules, Display Modules, Power Modules, and Others), By Technology (Cellular (4G/LTE/5G), Short-Range (Wi-Fi/BLE/Zigbee), LPWAN (NB-IoT/LoRa/LTE-M) and Others), By End-user (Consumer Electronics, Industrial, Automotive, Healthcare, Telecom and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

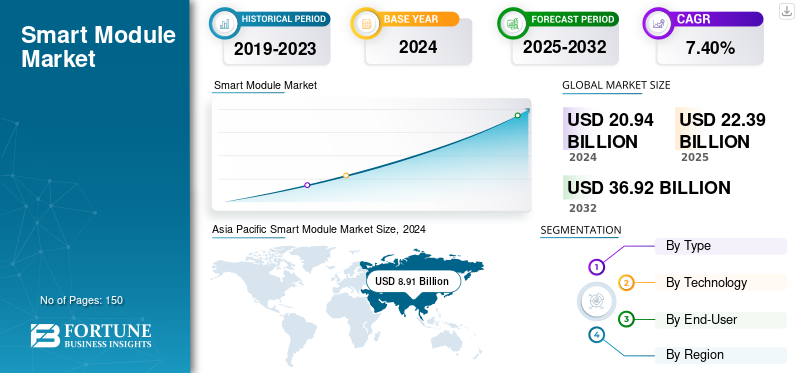

The global smart module market size was valued at USD 22.39 billion in 2025. The market is projected to grow from USD 23.98 billion in 2026 to USD 38.99 billion by 2034, exhibiting a CAGR of 6.26% during the forecast period.Asia Pacific dominated the smart module market with a market share of 43.04% in 2025.

A smart module is a high tech electronic component that combines a memory, microprocessor, and communication interface in a single unit. This aids in efficient connectivity, data processing, and automation across different devices.

The market is growing driven by the increase in demand for smart homes, connected vehicles, IoT applications and automation in industries. Surge in adoption of advanced technologies such as artificial intelligence, edge computing, and 5G also accelerates the market growth as it improves device performance and real time data exchange.

Few prominent key players in the market include Quectel Wireless Solutions Co., Ltd., Sierra Wireless, Inc., u-blox Holding AG, Fibocom Wireless Inc., Telit Cinterion Ltd., Thales Group, and others. Such companies adopt strategies including partnerships, product diversification, and technological innovations to sustain market competition and enhance their position.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Demand for Connected Devices Across Diverse Applications Drives the Market Development

The growing demand for connected devices across various consumer electronics, industrial and automotive arenas majorly drives the smart module market growth. Across the consumer electronics sector, the smart modules allow for a seamless connectivity in home automation systems, smartphones and wearables. In the automotive industry, the smart modules are used in vehicle tracking, advanced telematics, and infotainment systems, thus aiding in the adoption of connected and autonomous devices.

Additionally, in the industrial sector, smart modules help in powering predictive maintenance, machine-to-machine communication. And –process automation, thus aiding in operational efficiency. With increasing IoT adoption, the need for compact, reliable, and high-performance connectivity solutions grows, driving market growth globally.

Market Restraints

High Integration Costs and Growing Complexity Hampers the Market Growth

Growing integration costs and surging complexities in designs are a major restraint for the market. Innovative modules that including different technologies such as 5G, GPS, AI and IoT demands an advanced engineering, skilled labors, and costly components, raising the product cost. Small and medium sized companies tend to struggle for such higher investments, thus limiting the market expansion.

Additionally, embedding these technologies into a single compact module surges the challenges related to design, heat management, system compatibility, and power efficiency. Such complexities lead to a longer development cycles, potential reliability issues, and higher testing requirements.

Market Opportunities

Expansion of 5G Networks and IoT Infrastructure Offers Lucrative Growth Opportunities

The growing IoT infrastructure and 5G networks across emerging economies including Asia Pacific presents a prominent growth opportunity for the market. With 5G enabling a faster data transmission, higher connectivity, and ultra-low latency, smart modules support the deployment of advanced IoT devices across various industries such as healthcare, automotive, manufacturing and smart cities.

Markets in emerging countries such as China, India, and Southeast Asia are highly investing in digital infrastructure, thus increasing the demand for high-performance smart modules. This enables companies to offer an enhanced connectivity solution, thus supporting a real-time analytics and allowing effective edge computing.

SMART MODULE MARKET TRENDS

Growing Adoption of AI and IoT Technologies Has Emerged as a Prominent Market Trend

The increase in adoption of IoT and AI technologies has evolved as a major market trend, enabling efficiency and innovation across industries. Smart modules tend to integrate with AI enabled intelligent data analysis, automated decision making and predictive maintenance to improve overall system performance.

Similarly, IoT connectivity also allows for a seamless communication between devices, this improving real-time monitoring and control across smart homes, automotive, healthcare and industrial automation. This promotes a faster data processing, improved user experience and energy efficiency.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Increasing Applications Boosts Communication Modules’ Segment Growth

Based on type, the market is segmented into communication modules, processor, sensor modules, display modules, power modules, and others.

The Communication Modules segment is projecteed to dominate the market with a share of 32.27% in 2026. communication modules segment held the largest smart module market share and with a revenue share of USD 6.66 billion. This growing is majorly attributed to its widespread use across smart appliances, connected systems and IoT devices. Increasing demand for communication modules is owing to its constant wireless connectivity across these varied applications.

Additionally, sensor modules segment held the highest CAGR of 9.24% in 2024. This growing is majorly driven by the growing adoption of smart sensing technologies for environmental monitoring, automation and data-driven decision-making.

By Technology

Extensive Deployment of Cellular (4G/LTE/5G) in 5G and 4G Networks to Drive the Segment Growth

The market is divided into Cellular (4G/LTE/5G), Short-Range (Wi-Fi/BLE/Zigbee), LPWAN (NB-IoT/LoRa/LTE-M), and others, based on technology.

The Cellular (4G/LTE/5G) segment is expected to lead the market, contributing 40.81% globally in 2026. Among these, the Cellular (4G/LTE/5G) segment dominated the market with a revenue share of USD 8.47 billion in 2024. This segment’s growth is owing to its extensive deployment in 5G and 4G networks. This allows for a large-scale and reliable IoT connectivity across telecom, automotive, and industrial usages.

On the other hand, the LPWAN (NB-IoT/LoRa/LTE-M) segment held highest CAGR of 9.16% in 2024. The growth of Low Power Wide Area Network (LPWAN) technologies is owing to its energy efficient features, long range and low costs. These characteristics makes it ideal for large-scale IoT and remote monitoring applications.

By End-User

To know how our report can help streamline your business, Speak to Analyst

Growing Demand for Connected Devices to Drive Consumer Electronics Segment Growth

The market is divided into consumer electronics, industrial, automotive, healthcare, telecom, others, based on end-user.

The Industrial segment is projecteed to dominate the market with a share of 29.55% in 2026. Among these, the consumer electronics segment dominated the market with a revenue share of USD 5.81 billion in 2024. This segmental growth is attributed to the growing demand for connected devices including wearables, smartphones, and smart home systems. These demand contributes to the enhanced use of embedded communication and processing modules.

On the other hand, the industrial segment held highest CAGR of 9.63% in 2024. This growth is due to the rising adoption of Industry 4.0 technologies, predictive maintenance, automation systems and other solutions that are powered by smart modules.

SMART MODULE MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

Asia Pacific Smart Module Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market in North America reached USD 6.09 Billion in 2025, representing 27.21% of total market revenue, and is projected to reach USD 6.51 Billion in 2026. The region holds a second largest share due to the growing demand for advanced infrastructure and connected devices. Additionally, the higher investment across smart technologies by healthcare, automotive and industrial sectors by the U.S. also boosts the regional market growth. The U.S. market is projected to reach USD 3.83 billion by 2026.

Europe

Europe contributed approximately USD 4.38 Billion to the global market in 2025, accounting for 19.55% share, and is expected to reach USD 4.62 Billion in 2026. This growing is attributed to the presence of well-established industrial automation and automotive sectors in the region. Additionally, the strict energy efficiency and digitalization schemes also augments the regional growth. The UK market is projected to reach USD 1.1 billion by 2026. The Germany market is projected to reach USD 0.96 billion by 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 9.64 Billion, representing 43.04% of global demand, and is projected to grow to USD 10.45 Billion in 2026. The market is also expected to reach USD 9.64 billion in 2025. This dominance is associated with its strong electronic manufacturing base and surging industrialization. Additionally, the increasing adoption of IoT and 5G technologies across countries including The Japan market is projected to reach USD 2.47 billion by 2026. The China market is projected to reach USD 3 billion by 2026. The India market is projected to reach USD 1.93 billion by 2026.

South America

The South America market is projected to reach USD 1.27 billion by 2025. Market growth remains steady, supported by gradual industrial development and increasing demand across end-use sectors, although lower manufacturing capacity, limited technological adoption, and slower infrastructure development continue to moderate the pace of expansion compared to other regions.

Middle East & Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 1.01 Billion in 2025, accounting for 4.51% share, and is expected to reach USD 1.08 Billion in 2026. Growth is supported by ongoing economic development and sector-specific investments, despite challenges related to manufacturing capabilities, technology adoption, and infrastructure advancement. The GCC countries market is projected to reach USD 0.32 billion by 2025, contributing significantly to regional growth.

The Latin America market accounted for USD 1.27 Billion in 2025, representing 5.69% of the global industry, and is expected to reach USD 1.33 Billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Focus of Adopting Innovative Technologies to Sustain their Dominating Market Positions

The smart module industry consists of different players operating in the market. These include Quectel Wireless Solutions Co., Ltd., Sierra Wireless, Inc., u-blox Holding AG, Fibocom Wireless Inc., Telit Cinterion Ltd., Thales Group and others. These firms are implementing different key strategies including mergers and collaborations, adoption of innovative technologies, new product launches and others to sustain their market position.

LIST OF KEY SMART MODULE COMPANIES PROFILED

- Quectel Wireless Solutions Co., Ltd. (China)

- Sierra Wireless, Inc. (Canada)

- u-blox Holding AG (Switzerland)

- Fibocom Wireless Inc. (China)

- Telit Cinterion Ltd. (U.K.)

- Thales Group (France)

- Espressif Systems (Shanghai) Co., Ltd. (China)

- Silicon Laboratories Inc. (U.S.)

- Sequans Communications S.A. (France)

- Cavli Wireless, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In March 2025, Embedded and hobbyist electronics specialist Seeed Studio announced the launch of two new long-range low-power communications modules based on the Wi-Fi HaLow standard and a XIAO add-on board for those who would prefer to use LoRa instead.

- In March 2025, Quectel Wireless Solutions, a global IoT solutions provider, announced the launch of the SC200V smart module, powered by a Qualcomm Technologies processor. Designed to deliver exceptional performance across system capabilities, multimedia functions, network connectivity, and terminal development, this module is ideal for high-speed and multimedia-intensive applications, industrial handheld terminals, in-vehicle devices, robots, and beyond, unlocking new opportunities for next-generation intelligent solutions.

- In July 2024, to strengthen presence and revolutionise the electric vehicle (EV) landscape, MediaTek, a leading fabless semiconductor company, and JioThings Limited, subsidiary of Jio Platforms Limited, announced the launch of “Made in India” Smart Digital Cluster and Smart Module specially tailored for the two-wheeler (2W) market.

- In February 2024, Fibocom unveiled the 5G smart module solution that is compatible with Android, Linux and Windows operating systems, propelling the resilience of SoC-based wireless solution in the high-end AIoT market. The solution is developed to adapt the diverse programming languages in the application layer and open convenience for software engineers in the field of industrial computers, smart retail payment terminals, in-vehicle infotainment tablets, industrial cameras, robots, and others.

- In April 2021, the International Organization for Standardization 3GPP (3rd Generation Partnership Project) announced that the 5G standard Release 16 was frozen, marking the completion of the first evolution version of 5G standard. The Release 16 freeze will empower 5G with stronger vitality, richer application scenarios, and inject new energy into the 5G industry.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the smart module market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Growth Rate |

CAGR of 6.26% from 2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Type, Technology, End-User and Region |

|

By Type |

|

|

By Technology |

|

|

By End-User |

|

|

By Region |

Europe (By Type, Technology, End-User and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 22.39 billion in 2025 and is projected to reach USD 38.99 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 6.26% during the forecast period.

Rising demand for connected devices across consumer electronics, automotive, and industrial applications drives the market growth.

Quectel Wireless Solutions Co., Ltd., Sierra Wireless, Inc., u-blox Holding AG, Fibocom Wireless Inc., Telit Cinterion Ltd., Thales Group, Espressif Systems (Shanghai) Co., Ltd. and others are some of the top players in the market.

The Asia Pacific region held the largest market share.

Asia Pacific was valued at USD 9.64 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us