Sodium Sulfide Market Size, Share & Industry Analysis, By Form (Flakes/Solid, Solution/Liquid, Crystals/Hydrates, and Others), By End-Use Industry (Pulp & Paper, Leather & Textile, Mining & Metallurgy, Water & Wastewater Treatment, and Others), and Regional Forecast, 2026-2034

Sodium Sulfide Market Overview

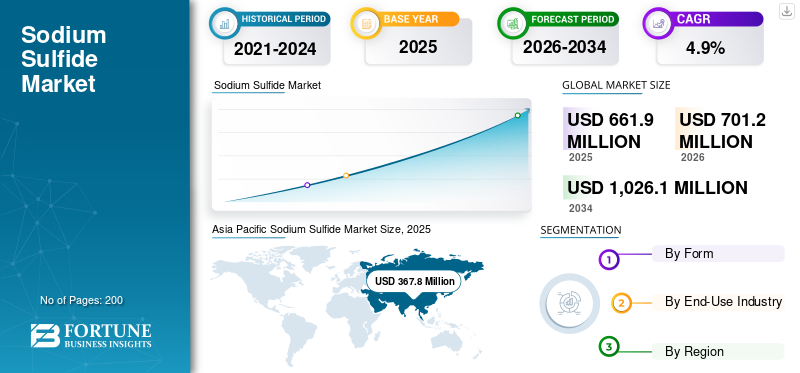

The global sodium sulfide market size was valued at USD 661.9 million in 2025. The market is projected to grow from USD 701.2 million in 2026 to USD 1,026.1 million by 2034, exhibiting a CAGR of 4.9% during the forecast period. Asia Pacific dominated the sodium sulfide market with a market share of 55.56% in 2025.

Sodium sulfide is a widely used industrial chemical that plays an important role in pulp and paper processing, leather treatment, textiles, mining, and selected chemical industries. Demand for sodium sulfide largely depends on activity in downstream industries, where it is valued for its processing efficiency, cost-effectiveness, and reliable performance in sulfur-based operations. The market is mainly supported by stable demand from mature end-use sectors rather than rapid expansion. As a result, market growth tends to remain moderate, with consumption driven more by ongoing industrial requirements and replacement demand across established applications globally today.

The market is dominated by a limited group of integrated chemical producers with established manufacturing assets and proven process technologies. Major players such as Solvay, American Elements, Nouryon, Tangshan Fengshi Chemical Co., Ltd., and Nagao Co., Ltd., and regional producers focus on production reliability, product consistency, and stable supply support, resulting in a moderately consolidated market characterized by steady industrial demand, high switching costs, and disciplined capacity expansion.

Download Free sample to learn more about this report.

Sodium Sulfide Market Key Takeaways

- 2025 Market Size: USD 661.9 million

- 2026 Market Size: USD 701.2 million

- 2034 Forecast Market Size: USD 1,026.1 million

- CAGR: 4.9% from 2026-2034

- Asia Pacific dominated the sodium sulfide market with a 55.56% share in 2025.

- The solution/liquid segment is projected to grow at a CAGR of 5.4% during the forecast period.

- The mining & metallurgy segment is expected to register a CAGR of 6.4% during the forecast period.

Asia Pacific

Asia Pacific accounted for USD 367.8 million in 2025 and is projected to reach USD 392.3 million in 2026.

North America

North America was valued at USD 77.8 million in 2025, remaining a significant regional market.

Europe

Europe reached USD 91.9 million in 2025 and is expected to record steady growth during the forecast period.

U.S.

The market was valued at USD 68.1 million in 2025.

Latin America

The sodium sulfide market was valued at USD 76.4 million in 2025.

Read More

SODIUM SULFIDE MARKET TRENDS

Increasing Demand for Reliable Supply and Consistent Quality across Major End-Use Industries is a Key Market Trend

A key trend in the market is the growing preference for reliable supply and consistent product quality across major end-use industries. Buyers in pulp and paper, leather, mining, and chemical processing are placing more importance on stable performance to avoid process issues and maintain smooth operations. This is encouraging producers to strengthen quality control, improve supply consistency, and provide better commercial support. As a result, competition in the market is increasingly based on reliability and product consistency, rather than solely on price.

- According to the U.S. Forest Service, around 38% of harvested roundwood in the U.S. is used for wood pulp for paper and paper products, highlighting the importance of a steady chemical supply in this end-use sector.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Demand from Pulp and Paper and Leather Processing Fuels Market Growth

The sodium sulfide market growth is mainly driven by its widespread use in pulp and paper manufacturing and leather processing applications. In the pulp industry, it is an important chemical in the kraft process, where it helps improve delignification efficiency and supports stable paper production. In the leather industry, sodium sulfide is widely used for dehairing hides and skins, making it essential for consistent tanning operations. Continued demand from these end-use industries creates a steady consumption base for sodium sulfide, as ongoing industrial production directly supports its use across established processing applications.

- According to the U.S. Forest Service, approximately 38% of harvested roundwood in the U.S. is used for wood pulp for paper and paper products, highlighting the importance of the pulp and paper industry for product demand in kraft pulping.

MARKET RESTRAINTS

Strict Safety and Compliance Requirements Raise Operational Burden

Sodium sulfide demand is restrained by the chemical’s hazardous nature and the strict handling, storage, and wastewater management requirements associated with its use. As a strongly alkaline, sulfur-bearing compound, it requires controlled transportation, strict workplace safety practices, and proper effluent treatment to prevent environmental and operational risks. These compliance requirements increase end-user operating costs, especially in highly regulated industries and regions. As a result, purchasing decisions are often influenced not only by performance and price, but also by regulatory burden, treatment costs, and site-level safety capabilities.

MARKET OPPORTUNITIES

Mining Sector Growth Creates Additional Demand Potential

Sodium sulfide has growth potential through its use in mining and mineral processing, where it is used in ore flotation and separation processes. As mining activity expands in resource-rich regions and investment in mineral production increases, demand for process chemicals is also expected to rise. This creates an opportunity for sodium sulfide suppliers to grow beyond their traditional pulp and leather markets. Increasing focus on efficient metal recovery and broader mineral processing activity can support additional product demand in the coming years.

- According to the U.S. Geological Survey (USGS), U.S. molybdenum concentrate mine production rose 18% to 40,000 tons in 2025 from 34,000 tons in 2024, indicating stronger mining activity that can support sodium sulfide demand in mineral processing.

MARKET CHALLENGES

Limited Ability to Pass on Higher Costs Pressures Margins

Sodium sulfide producers face an ongoing challenge in passing higher raw material, sulfur-based input, and energy costs on to customers quickly. Many end users in the pulp and paper, leather, and mining industries remain price-sensitive, making price increases difficult. Even when demand is stable, sudden changes in input or utility costs can reduce margin visibility and complicate production planning. This increases the need for strong cost control, stable sourcing, and better commercial flexibility across the sodium sulfide value chain.

Segmentation Analysis

By Form

Ease of Storage and Transportation Supported Dominance of Flakes/Solid Segment

Based on form, the market is segmented into flakes/solid, solution/liquid, crystals/hydrates, and others.

The flakes/solid segment accounted for the largest sodium sulfide market share in 2025. Flakes and solid forms lead market consumption as they are easier to store, transport, and handle across major end-use industries such as pulp and paper, leather processing, mining, and chemical manufacturing. They also offer better shelf stability and are widely preferred where controlled dosing and bulk industrial use are important. As industrial buyers continue to focus on operational convenience, supply efficiency, and dependable product handling, flakes and solid sodium sulfide remain the most established and commercially preferred form in the market.

The solution/liquid segment is expected to grow at a 5.4% CAGR over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End-Use Industry

Strong Sodium Sulfide Usage in Kraft Processing Boosted Pulp & Paper Segment Growth

In terms of end-use industry, the market is categorized into pulp & paper, leather & textile, mining & metallurgy, water & wastewater treatment, and others.

The pulp & paper segment accounted for the largest share in 2025. The pulp and paper segment leads sodium sulfide demand, as it is a key chemical in the kraft pulping process, where it improves delignification efficiency and supports stable production performance. The industry relies on consistent chemical inputs to maintain processing efficiency, product quality, and operational continuity in large-scale paper manufacturing. As paper and packaging production remains essential across many industrial and consumer applications, the pulp and paper segment continues to provide a steady and structurally strong demand base for sodium sulfide.

The mining & metallurgy segment is expected to grow at a 6.4% CAGR over the forecast period.

Sodium Sulfide Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Sodium Sulfide Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the sodium sulfide market in 2025, valued at USD 367.8 million, and is expected to retain its leading role in 2026, reaching USD 392.3 million. The region’s leadership is driven by its large pulp and paper base, strong leather processing activity, and broad industrial manufacturing presence. Robust demand from kraft pulping, leather treatment, textile manufacturing, mining, and downstream chemical applications supports sustained product consumption, particularly in high-volume, cost-sensitive industrial operations.

China Sodium Sulfide Market

Based on Asia Pacific’s strong contribution and China’s large-scale industrial base, the China market was valued at USD 178.5 million in 2025, accounting for approximately 48.5% of global revenues. Demand is supported by the country’s extensive pulp and paper production, strong leather and textile processing sector, and broad chemical manufacturing activity, which together sustain China’s global leadership in the market today.

India Sodium Sulfide Market

The India market in 2025 was valued at around USD 52.1 million. Growth is supported by pulp and paper production, expanding leather processing, rising demand for textile treatment, and growth in domestic chemical manufacturing. These factors continue to support product consumption across major industrial applications.

North America

North America remains a significant regional market, valued at USD 77.8 million in 2025. Demand is supported by established pulp and paper operations, leather processing, mining activity, and broader industrial chemical use. The region benefits from stable downstream infrastructure development and consistent industrial demand. However, growth remains moderate due to the maturity of major end-use industries and relatively steady consumption patterns across the region, with limited room for rapid expansion.

U.S. Sodium Sulfide Market

The U.S. market in 2025 was valued at USD 68.1 million, representing approximately 87.5% of global revenues. Demand is supported by pulp and paper manufacturing, mining activity, leather processing, and selected chemical applications. Stable consumption across kraft pulping and other established industrial operations continues to support sodium sulfide use across major end-use sectors nationally.

Europe

Europe was valued at USD 91.9 million in 2025 and is projected to record modest growth over the forecast period. The region is shaped by strict environmental regulations, high energy costs, and heightened compliance requirements across the chemical processing industry. Despite these pressures, continued demand from pulp and paper, leather processing, mining, and other industrial applications supports ongoing sodium sulfide consumption across the region.

Germany Sodium Sulfide Market

Germany’s market was valued at approximately USD 25.3 million in 2025, equivalent to around 27.6% of the global revenues. Demand is supported by industrial manufacturing, pulp and paper activity, chemical processing, and the use of sulfur-based processing chemicals across sectors.

U.K. Sodium Sulfide Market

The U.K. market in 2025 was valued at USD 15.5 million, accounting for roughly 16.8% of global revenues. Consumption is concentrated in pulp and paper processing, selected chemical applications, water treatment, and other industrial uses where sulfur-based processing chemicals are required for stable operational performance.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are expected to witness moderate growth during the forecast period. The Latin America market was valued at USD 76.4 million in 2025, supported by pulp and paper activity, leather processing, mining operations, and broader industrial chemical use. In the Middle East & Africa, demand is driven by mining, water treatment, leather processing, and selected chemical applications, along with gradual industrial development. The Middle East & Africa market was valued at USD 48.0 million in 2025. Growth across both regions remains supported by expanding industrial activity, improved processing capacity, and steady demand from essential end-use sectors that use sulfur-based chemicals.

GCC Sodium Sulfide Market

The GCC market was valued at USD 25.4 million in 2025, representing approximately 52.9% of regional revenues. Demand is supported by mining activity, water treatment needs, selected chemical processing operations, and the region’s growing role in industrial chemical distribution networks.

COMPETITIVE LANDSCAPE

Key Industry Players

High Capital Intensity and Strategic Asset Management Shape Competition in the Market

The market is relatively consolidated, as hazardous chemical handling requirements, environmental compliance standards, and process safety needs create significant barriers to entry. These factors limit new participation and concentrate supply among a small group of chemical producers with established operations and proven manufacturing expertise.

Leading players such as Solvay, American Elements, Nouryon, Tangshan Fengshi Chemical Co., Ltd., and Nagao Co., Ltd., and regional producers focus primarily on maintaining supply reliability, improving product consistency, and strengthening cost efficiency rather than pursuing aggressive capacity expansion. Recent activities across these companies highlight a strategic emphasis on operational efficiency, compliance management, and stable supply support to strengthen long-term market positioning.

LIST OF KEY SODIUM SULFIDE COMPANIES PROFILED

- Solvay (Belgium)

- American Elements (U.S.)

- Nouryon (Netherlands)

- Kishida Chemical Co., Ltd. (Japan)

- Tangshan Fengshi Chemical Co., Ltd. (China)

- Tianjin Ruister International Co., Ltd. (China)

- Merck KGaA (Germany)

- Nagao Co., Ltd. (Japan)

- TIB Chemicals AG (Germany)

- Elchemy (India)

REPORT COVERAGE

The global sodium sulfide market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The sodium sulfide market research report also includes a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.9% from 2026 to 2034 |

| Unit | Value (USD Million) Volume (Kiloton) |

| Segmentation | By Form, End-Use Industry, and Region |

| By Form |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 661.9 million in 2025 and is projected to reach USD 1,026.1 million by 2034.

Recording a CAGR of 4.9%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

By end-use industry, the pulp & paper segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

Consistent demand from pulp and paper mills and leather processing industries boosts market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us