Software-Defined Military Radio Market Size, Share & Industry Analysis, By Component (Hardware and Software), By Type (General Purpose Radio, Joint Tactical Radio System (JTRS), Cognitive/Intelligent Radio, and Terrestrial Trunked Radio (Tetra)), By Frequency Band (MF/HF, VHF, UHF, and Other Bands), By Platform (Airborne, Naval, Land, and Space), and Regional Forecast, 2026-2034

Software-Defined Military Radio Market Size and Future Outlook

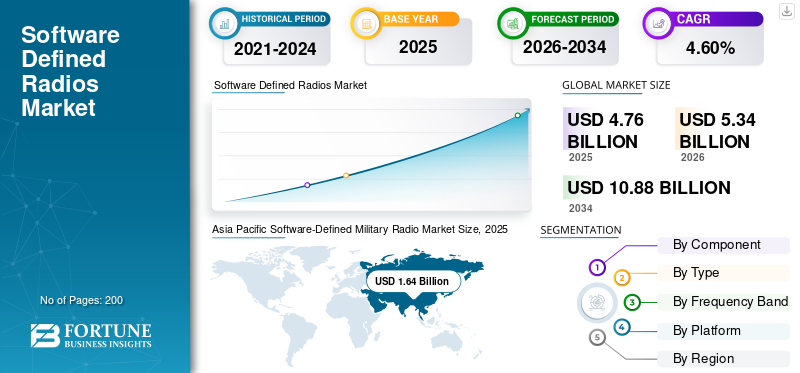

The global software-defined military radio market size was valued at USD 4.76 billion in 2025. The market is projected to grow from USD 5.34 billion in 2026 to USD 10.88 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period. Asia Pacific dominated the software defined radio market with a market share of 34.45% in 2025.

The market represents a critical evolution in defense communications, enabling flexible, adaptable platforms that replace rigid hardware-defined systems with software-configurable waveforms. This shift supports network-centric warfare by allowing seamless interoperability across land, air, naval, and space domains, even in contested electromagnetic environments jammed by adversaries. Driven by global military modernization efforts, the market emphasizes cognitive radios that dynamically optimize spectrum usage, integrate with emerging 5G networks, and incorporate AI for enhanced signal processing and security.

Key players including BAE Systems (U.K.), Northrop Grumman (U.S.), Raytheon Technologies/RTX (U.S.), Elbit Systems (Israel), Thales (France), L3Harris (U.S.), General Dynamics (U.S.), Viasat (U.S.), Leonardo (Italy), and Rohde & Schwarz (Germany) are dominating the market through secure tactical communications portfolios, large-scale defense program wins. Long-term upgrade/support models are turning radio procurement into a multi-year modernization cycle across land, air, and naval forces.

Download Free sample to learn more about this report.

Software Defined Radio Market KEY TAKEAWAYS

- 2025 Market Size: USD 4.76 Billion

- 2026 Market Size: USD 5.34 Billion

- 2034 Forecast Market Size: USD 10.88 Billion

- CAGR: 9.3% from 2026–2034

- Asia Pacific dominated the software-defined military radio market with a 34.45% share in 2025.

- The hardware segment is anticipated to account for the largest market share.

- The general purpose radio segment dominated the market in 2025.

Asia Pacific

Asia Pacific accounted for USD 3.0 billion in 2025 and is projected to reach USD 4.0 billion in 2026.

North America

North America generated USD 5.2 billion in 2025 and is projected to reach USD 5.5 billion in 2026.

Europe

Europe accounted for USD 4.7 billion in 2025 and is projected to reach USD 5.0 billion in 2026.

U.S.

The software-defined military radio market is estimated to reach USD 1.44 billion in 2026.

Japan

The software-defined military radio market is estimated to reach USD 0.31 billion in 2026.

Read More

SOFTWARE-DEFINED MILITARY RADIO MARKET TRENDS

Rising Adoption of Adaptable SDR Platforms is the Latest Trend in the Market

The market is experiencing robust growth, driven by defense modernization and integration with 5G infrastructure. Key trends include the shift to cognitive radios for spectrum optimization, reduced size-weight-power via semiconductor advances, and the global adoption of SDR technology in most tactical military radios. This evolution supports network-centric warfare, extending equipment lifecycles and enhancing interoperability in contested environments.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Defense Modernization and Budget Increases Driving the Market Growth

Surging global defense budgets prioritize SDR for tactical advantages, including flexible frequency reconfiguration, secure data transfer, and seamless interoperability across platforms. Military programs such as the U.S. Joint Tactical Radio System and rising geopolitical tensions drive adoption, with over 40,000 of units delivered to Ukraine by L3Harris Technologies, Inc. in 2025 for jamming-resistant updates. Integration with 5G, AI signal processing, and network-centric operations further drives demand by enhancing voice clarity, bandwidth, and lifecycle cost savings compared to legacy hardware.

MARKET RESTRAINTS

High Costs and Implementation Complexity Hinders the Market Growth

Elevated initial investments and FPGA expenses limit broader adoption, particularly for new entrants facing steep development hurdles. Cybersecurity vulnerabilities, export controls, and thermal management issues constrain scalability, while reliance on specialized expertise slows deployment. These factors limit the growth despite strong demand, as the high system complexity requires rigorous certification to military standards, extending timelines and increasing operational expenses. Maintenance difficulties for subsystems also hinder sustained use in diverse environments.

MARKET OPPORTUNITIES

AI-Enabled Cognitive Radios and Exports are the Opportunities in the Market

Significant opportunities arise from AI-integrated adaptive architectures for real-time spectrum management in contested electromagnetic spaces, alongside expansion into space-based SDR and unmanned systems integration. Defense exports, international collaborations, and commercial 5G crossovers, such as cloud-bundled industrial-edge stacks, enable rapid network launches and lower barriers to entry via Open RAN. Emerging markets in the Asia Pacific, fueled by rising military spending in China and India, as well as modernization in Europe and North America, further amplify growth potential through government-backed programs. These factors drive the software-defined military radio market growth.

MARKET CHALLENGES

Interoperability and Security Barriers Challenging the Market Growth

Integrating SDR with legacy systems poses major hurdles due to mismatches in protocols, modulation schemes, and technical specifications, complicating upgrades across mixed fleets. Stringent security requirements vary by nation, restricting waveforms and market access, while certification for electromagnetic compatibility and cyber threats prolongs qualification. Evolving threats like electronic warfare jamming demand constant software updates, straining resources amid geopolitical export limits and supply chain dependencies.

Segmentation Analysis

By Component

Large-Scale Fleet Replacement and Ruggedization Requirements Drives the Hardware Segment Growth

Based on component, the market is segmented into hardware and software.

The hardware segment is anticipated to account for the largest market share. Hardware demand remains high as forces still need large volumes of radios for soldiers and vehicles. Replacement cycles, ruggedization needs, and secure, standardized terminals drive procurement.

The software segment is anticipated to rise with a CAGR of 9.7% over the forecast period.

By Type

Routine Frontline Voice-And-Data Needs across Units Drives General Purpose Radio Segment Growth

Based on type, the market is segmented into general purpose radio, Joint Tactical Radio System (JTRS), cognitive/intelligent radio, and Terrestrial Trunked Radio (Tetra).

In 2025, the general purpose radio segment dominated the global market. General purpose radio demand is steady as it covers everyday tactical voice and data needs across units. Buyers prefer proven models with simpler integration, strong availability, and upgrade paths.

The cognitive/intelligent radio segment is projected to grow at a CAGR of 10.4% over the forecast period.

By Frequency Band

Need for Reliable Performance across Complex Terrain and Air-Ground Coordination Drives UHF Segment Growth

Based on frequency band, the market is segmented into MF/HF, VHF, UHF, and other bands.

The UHF segment is anticipated to witness a dominating market share over the forecast period. UHF demand is strong due to its balance of range, penetration, and reliable tactical performance in complex terrain. It supports air-ground coordination and mobile units, making it a procurement priority.

The other bands segment is projected to grow at a CAGR of 10.3% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Due to the Army Being the Largest User Base for Tactical Radios, the Demand of Land Segment is Growing

Based on platform, the market is segmented into airborne, naval, land, and space.

The land segment dominated with the largest software-defined military radio market share. Armies deploy the most radios across infantry, vehicles, and command posts. Modernization programs prioritize secure networking, wide fielding, and consistent upgrades for frontline readiness.

In addition, space segment is projected to grow at a CAGR of 10.6% during the forecast period.

Software-Defined Military Radio Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and rest of the world.

Asia Pacific

Asia Pacific contributed approximately USD 3 billion to the global market in 2025, accounting for 20.90% share, and is expected to reach USD 4 billion in 2026. The regional demand grows fastest, driven by border tensions, maritime security, and force expansion. Buyers seek affordable, scalable SDRs, domestic production, and rapid fielding, especially for army modernization and joint operations.

Asia Pacific Software-Defined Military Radio Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Japan Software-Defined Military Radio Market

The Japan market share in 2026 is estimated at around USD 0.31 billion, with a CAGR of 9.3% during the forecast period. Japan’s demand is increasing to strengthen island defense and improve coordination across the Self-Defense Forces. Buyers emphasize secure communications, resilience, and interoperability with U.S. systems, alongside modernization for maritime patrol operations.

China Software-Defined Military Radio Market

China’s market is projected to be one of the largest in the Asia Pacific, with 2026 revenues estimated at around USD 0.66 billion. China’s demand is driven by force modernization and joint command upgrades across services. It is focused on production, networked radios for land and maritime theaters, and security control through domestic supply chains.

India Software-Defined Military Radio Market

The Indian market in 2026 is estimated at around USD 0.34 billion. Product demand in India is surging as services replace legacy systems and drive indigenization. Contracts prioritize locally produced SDRs, scalable rollout, and affordable upgrades, supporting large army deployments and growing joint-air operations.

North America

In 2025, North America held 32.90% of the global market share, reaching a valuation of USD 5.2 billion, and is projected to grow to USD 5.5 billion in 2026. North America’s demand stays strong as the U.S. refreshes tactical networks and allies align on interoperability. The region is focused on secure, software-upgradable radios for land, air, and naval platforms, with steady upgrade-funded budgets.

U.S. Software-Defined Military Radio Market

Based on North America’s strong impact and the U.S. dominance in the region, the U.S. market is estimated at around USD 1.44 billion in 2026, accounting for roughly 9.2% of global sales. U.S. demand leads the market, powered by large-scale tactical networking programs and continuous upgrades. Priorities include secure connectivity across services, better resilience in contested environments, and rapid software refresh cycles.

Europe

The market in Europe reached USD 4.7 billion in 2025, representing 30.10% of total market revenue, and is projected to reach USD 5 billion in 2026. Europe’s demand is rising as nations modernize coalition communications and build sovereign industrial capacity. Programs prioritize secure communications, cross-border compatibility, and lifecycle support, with procurement spread across many mid-sized contracts.

U.K. Software-Defined Military Radio Market

The U.K. market is estimated to grow at around USD 0.30 billion in 2026, representing a roughly 9.0% CAGR of global sales during the forecast period. U.K. demand is steady, focused on modernizing deployable communications and maintaining interoperability with NATO partners. Procurement emphasizes upgradeable radios, sovereign support, and integration across land, maritime, and air fleets.

Germany Software-Defined Military Radio Market

Germany’s market is projected to reach approximately USD 0.33 billion in 2026. Germany’s demand is expanding as Bundeswehr digitization accelerates and coalition deployments require reliable communications. Buyers favor secure, standardized radios and long-term sustainment, with strong emphasis on domestic integration and testing.

Rest of the World

The Rest of the World market accounted for USD 2.6 billion in 2025, representing 16.20% of the global industry, and is expected to reach USD 2.7 billion in 2026. The rest of the world includes the Middle East & Africa, and Latin America. These regions are expected to witness moderate growth in this market during the forecast period. The Middle East & Africa and Latin America markets are set to reach valuations of USD 0.19 billion and USD 0.10 billion, respectively, in 2026. The rest of the world’s demand is uneven but increasing, particularly in regions where internal security and regional conflicts persist. Investments prioritize rugged radios, secure voice/data, and training packages, often funded through multi-year assistance.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Strengthen Modernization Programs and Long-Term Upgrade Ecosystems to Gain Market Advantage

Key players are driving the software-defined military radio market by helping armies and air forces replace older radios with modern, software-upgradable systems. Major U.S. players such as Northrop Grumman, Raytheon, L3Harris, General Dynamics, Viasat, and BAE Systems win large programs, deliver radios at scale, and keep them relevant through upgrades and long-term support. European leaders such as Thales and Leonardo are growing the market by focusing on cross-country interoperability, national manufacturing partnerships, and service contracts that keep fleets running for years. Elbit Systems expands its market share through proven tactical radios designed for fast deployment and harsh battlefield conditions. Rohde & Schwarz supports wider adoption by improving testing, reliability, and secure performance standards. Overall, these firms are expanding the market by turning radio procurement into a multi-year upgrade and support business, not just one-time hardware sales.

LIST OF KEY SOFTWARE-DEFINED MILITARY RADIO COMPANIES PROFILED

- BAE Systems PLC (U.K.)

- Northrop Grumman Corporation (U.S.)

- Raytheon Technologies Corporation (U.S.)

- Elbit Systems Ltd. (Israel)

- Thales Group S.A. (France)

- L3Harris Technologies, Inc. (U.S.)

- General Dynamics Corporation (U.S.)

- Viasat, Inc. (U.S.)

- Leonardo S.p.A. (Italy)

- Rohde & Schwarz GmbH & Co. KG (Germany)

KEY INDUSTRY DEVELOPMENTS

- October 2025: The Indian Army placed an order for its first homegrown software-defined radios, based on a DRDO design and to be manufactured by Bharat Electronics Limited (BEL).

- July 2025: Indra and Bittium signed a non-binding agreement outlining cooperation on SDR development. The plan is to explore Bittium technology transfer while Indra adapts and advances the solution and helps build Spain’s industrial capability to deliver a Europe-based, fully proprietary SDR and waveform solution.

- June 2024: Thales secured a major deal to equip Ireland’s Army, Naval Service, and Air Corps with SDR systems and support. The arrangement includes an initial supply of more than 3,500 SquadNet radios and roughly 2,500 radios from the SYNAPS range under a framework agreement.

- February 2024: The Indian Air Force signed a contract with BEL to procure lightweight, software-based, man-portable radio communication sets.

- January 2023: Elbit Systems stated that Spain’s DGAM selected its E-LynX tactical SDR solution for an urgent procurement program focused on V/UHF SDR radio equipment.

REPORT COVERAGE

This research offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, By Type, By Frequency Band, By Platform, and Region |

| By Component |

Software |

| By Type |

|

| By Frequency Band |

|

| By Platform |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.76 billion in 2025 and is projected to reach USD 10.88 billion by 2034.

In 2025, the Asia Pacific’s market value stood at USD 1.64 billion.

The market is expected to exhibit a CAGR of 9.3% during the forecast period.

By hardware segment is expected to dominate the market.

Defense modernization and budget increases are the key factors driving market growth.

BAE Systems PLC (U.K.), Northrop Grumman Corporation U.S.), Raytheon Technologies Corporation (U.S.), Elbit Systems Ltd. (Israel), Thales Group S.A. (France), and L3Harris Technologies, Inc. (U.S.) are few major players in the global market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us