Soy Sauce Market Size, Share & Industry Analysis, By Process (Brewed and Blended), By Type (Light Soy Sauce, Dark Soy Sauce, and Others), By End-user (Processed Food, Prepared Foods, and Households), By Distribution Channel (Supermarkets, Hypermarkets, Convenience Stores, Online Sales, HoReCa, and QSR), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

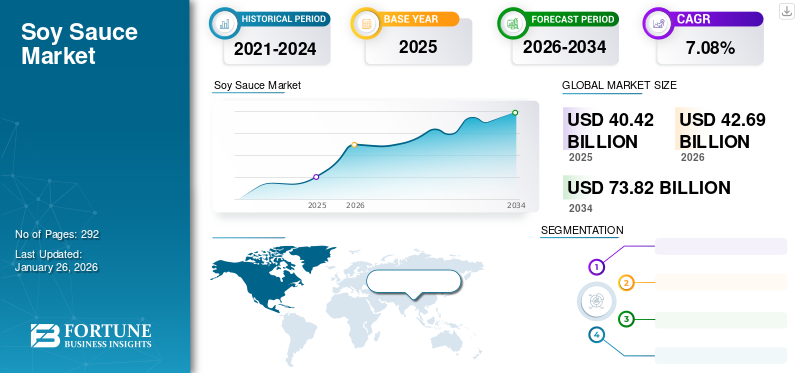

Soy Sauce Market Size and Future Outlook

The global soy sauce market size was valued at USD 40.42 billion in 2025 and is projected to grow from USD 42.69 billion in 2026 to USD 73.82 billion by 2034, exhibiting a CAGR of 7.08% during the forecast period of 2026-2034. Asia Pacific dominated the soy sauce market with a market share of 62.03% in 2025.

The sauces market is one of the long-standing and diverse markets across the world, primarily due to its offerings of savory products to consumers to use in their daily diet. Sauces and condiments have been in huge demand among consumers since ancient times, and the trend is continuing in the global marketplace. Among several oriental table sauces, this sauce is widely consumed as it offers a sensorial appeal to the food. Nowadays, the taste preferences of consumers are becoming experimental, and they are seeking tasty and healthy sauces that have an extended shelf life. The manufacturers are increasingly focusing on introducing new products with a low pH to preserve and increase the taste. The constant advancements in technology and the steady improvement of consumers’ living standards will aid the growth of the market.

Some of the prominent players operating in the market include Foshan Haitian Flavouring & Food Co. Ltd, Jiajia Food Group Co., Ltd., and Kikkoman Corporation, among others.

Download Free sample to learn more about this report.

Soy Sauce Market Key Takeaways

- 2025 Market Size: USD 40.42 billion

- 2026 Market Size: USD 42.69 billion

- 2034 Forecast Market Size: USD 73.82 billion

- CAGR: 7.08% from 2026–2034

- Asia Pacific dominated the soy sauce market with a 62.03% share in 2025.

- The light soy sauce segment is expected to account for 55.19% of the market in 2026.

- The brewed segment is projected to lead the market with a 64.28% share in 2026.

Asia Pacific

Asia Pacific led the global market with a valuation of USD 25.07 billion in 2025 and is expected to reach USD 26.55 billion in 2026.

North America

North America accounted for USD 7.51 billion in 2025 and is projected to reach USD 7.92 billion in 2026.

Europe

Europe generated USD 5.49 billion in 2025 and is expected to reach USD 5.77 billion in 2026.

U.S.

The U.S. soy sauce market is valued at USD 7.42 billion in 2026.

Japan

The Japan soy sauce market is valued at USD 2.25 billion in 2026.

Read More

Soy Sauce Market Trends

Growing Demand for Low-Salt Soy Sauce to Aid Market Growth

Consumers are becoming more aware of their food selections in the market, and the origin of food is becoming a serious concern among them to maintain their health. An increasing number of consumers are reducing the unhealthy components from their diet and seeking clean-labeled products that are free from artificial preservatives. Clean-eating consumers scrutinize the ingredients sourced for the sauce and its manufacturing process, along with the animal welfare practices of the brands in the market. Both the industry regulators and the consumers are seeking sauces with minimal sodium content or gluten-free products. Now, food producers are also keen to take on the challenge of low-sodium production.

- For instance, in October 2023, Ajinomoto, a Japanese food company, introduced its latest less-salt soy sauce, “Phu Si,” especially for the health-conscious population across Vietnam. As per the label of low sodium, the product contains 30% less salt content as compared to the traditional sauce.

Download Free sample to learn more about this report.

Impact of COVID-19

The impact of the COVID-19 pandemic on the foodservice/processing industry was tough. Almost overnight, a global lockdown was imposed, which put workers in confinement, caused supply chain disruptions, and a dip in sales. Due to the pandemic, individuals stopped visiting eateries, cutting off profit generation, which resulted in the permanent/temporary closure of dine-in restaurants. These factors led to a sudden slump in the product demand.

- According to the Kikkoman Corporation, a Japanese producer, soy sauce sales dipped in the foodservice and industrial sectors in 2020 due to the COVID-19 pandemic.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Nutritious Yet Umami Foods Triggers Product Use

Spices and condiments play a vital role in dietary patterns, mainly among Asian consumers across the world. The consumers in the region prefer spicy and umami-flavor foods in their daily diet, which enhances the taste of the food. Nowadays, the trend for Asian foods is growing, as consumers across the world are becoming more experimental in their food choices. The increasing popularity of Asian soy sauces across the world contributes to overall growth. It is one of the most consumed sauces for the preparation of these umami foods. The emergence of the new prepared foods and increasing product innovations in the packaged foods segment are majorly propelling the overall market.

Availability of Abundant Soybeans to Promote Innovations in Soy Sauce

Over the recent decades, the global consumption of soybeans has increased at a decent pace. Currently, it is one of the most widely grown and used commodities globally. The utilization ranges from human consumption to animal feed owing to its natural properties, such as a rich source of protein, carbs, and others. According to the Food Climate Research Network (FCRN) at the University of Oxford, only 6% of the total soybeans produced every year are utilized for human consumption. Thus, manufacturers are utilizing the available raw materials in the production of varied sauces to meet its increased demand from several food sectors and households. Innovations and evolving food preferences of consumers are some of the major factors that are driving the overall market growth.

MARKET RESTRAINTS

Risk of Chronic Ailments and Easy Availability of Substitutes can Obstruct Product Demand

Traditional products consist of concentrated levels of glutamate and sodium, which are responsible for consumers’ adverse health effects. Although sodium and glutamate are mainly added for flavor profile and preservation, their high consumption is associated with severe ailments, such as hypertension and obesity. The other considerable restraint affecting the global soy sauce market growth is the easy availability of substitutes. Korean barbecue, Spicy Habanero, and Sriracha hot sauce are a few of the flavor options being experimented with.

MARKET OPPORTUNITIES

Rising Need for Tailor-Made Soy Sauces Paves Way for Growth Prospects

The artisanal industry is experiencing a high growth trajectory, owing to the demand for unique flavors. In this era, most individuals seek ways to strengthen their culinary experience and gravitate toward “superior quality sauces” composed of exotic ingredients. Also, these artisanal sauces are produced in small batches and can be customized to meet consumer needs. Thus, in order to align with the need, the manufacturers are working toward developing tailor-made sauces, which will appeal to consumers in terms of taste and quality.

MARKET CHALLENGES

Surging Availability of Substitutes Creates Challenges for Market Growth

Another considerable restraint faced by the producers is the easy availability of substitutes. Korean barbecue, Spicy Habanero, and Sriracha hot sauce are a few of the flavor options being experimented. In the current time, consumers are seeking more unique and flavorful sauces, apart from traditional ones. Moreover, the trend of trying new spicy and umami-rich flavored sauces is further driven by the prepared foods, where customers are served with multipurpose culinary sauces to fuel their experience. This factor poses a negative impact on consumption.

Segmentation Analysis

By Type

Light Soy Sauce Accounted for Largest Market Share Due to Its Economical and Wide Use

By type, the market is segmented into light soy sauce, dark soy sauce, and others.

The light soy sauce segment is expected to account for 55.19% of the market in 2026. Light sauce is produced via roasted wheat and steamed soybeans, which are blended and then spread on trays for fermentation. It is mainly applicable for dishes, where the aim is to season and strengthen the palatability without influencing the overall color of the food. A few of the culinary applications where it can be used include stir-frying, marinades, and dressings. Also, as compared to dark versions, the lighter version provides a milder taste and enhances the umami flavor, specifically due to its shorter aging time, which further adds to its value.

Dark sauce is composed of ingredients similar to those of the light variety, but has a longer fermentation procedure. The main goal of using a darker version is to elevate the appearance of cuisines, and it is added often toward the end of cooking. The dark sauce is commonly used in the preparation of noodles & stews, veggies, and meat.

Apart from this, the others segment, which includes white and sweet versions, is at its nascent stage owing to their low awareness and innovation. Other products, such as white sauce, are produced by a brewing method, where mainly wheat and a minimal amount of soybeans are used. Similarly, white sauce and sweet sauce also provide a mild flavor and can be used for barbecue, stir-frying, and glazing.

By Process

Brewed Segment Set to Lead Market Owing to Its Better Flavor

On the basis of process, the market is segmented into brewed and blended.

In 2026, the brewed segment is projected to lead the market with a 64.28% share. The market share for the brewed process was higher in 2024 as compared to the blended sauce, and is predicted to continue its growth in the near term. The brewed sauce contains purely fermented soybeans, primarily with no artificial additives, thereby offering better flavor. This naturally fermented or brewed sauce is developed over a period of months or years, and is prepared by using wheat and soybeans as the major ingredients. Moreover, the brewed sauce comprises nearly 17 to 19% sugars, 1 to 1.6% nitrogen, and 1-2% organic acids. Thus, this gives rise to the demand for brewed sauce across the foodservice and household sectors. Naturally brewed products command premium prices in the market compared to synthetically produced products.

The blended segment is expected to grow at a CAGR of 6.06% from 2025 to 2032. Blended products are produced from ingredients similar to those of brewed products but contain additives, such as molasses and mushroom broth. The foodservice industry is trying to use blended sauce in products, which requires a balance of sweet and spicy flavors.

By End-user

Prepared Foods to Hold Apex Position Fueled by Increasing Adoption of Cross-cultural Food Trends

On the basis of end-user, the market is distributed into processed food, prepared foods, and households.

The prepared foods segment is estimated to lead the end user segment with a 57.02% share of the global market in 2026. Prepared foods comprise foods and beverages that are produced and intended for immediate consumption. Nowadays, the socializing culture has emerged as a popular trend, which contributes significantly to the expansion of the foodservice industry. In the past few years, consumers’ lifestyles have become more chaotic, and the majority of individuals are seeking quick and easy meal options. Along with convenience, consumers also seek unique flavors, which the use of this sauce can fulfill. In Asian cuisines, it has been recognized as one of the essential ingredients to refine the flavor, aroma, and overall delectability of the dishes. Thus, its usage has increased in various parts of the world, and non-Asian consumers can also taste the umami flavor in their local dishes.

The households segment is projected to expand at a CAGR of 7.19% from 2025 to 2032 due to the rising use of this product in home cooking. Since the COVID-19 pandemic, the trend of cooking at home has enormously increased as consumers seek new ways to satisfy their cravings. Also, the emerging food blogs and videos influenced individuals to make their favorite dishes, which augmented the use of this sauce. It is also used as a seasoning in the preparation of processed foods, and its adoption rate is expected to grow during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel

HoReCa Holds Leading Market Position Owing to Increasing Popularity of Dining Out

Based on distribution channel, the market is segmented into supermarkets, hypermarkets, convenience stores, online sales, HoReCa, and QSR.

The HoReCa segment is expected to lead the market, contributing 41.27% globally in 2026. The HoReCa segment leads the market and is expected to witness high traction in the future. Owing to its versatility, this sauce is primarily used as a table condiment in restaurants and can be added to a variety of meals to improve the flavor. A few of its uses include as a glaze for meats and as a dip for sushi. Moreover, the growing culture of dining out and the trend of trying multiple cuisines further increase its usage in the HoReCa sectors.

The supermarkets segment falls in the second position in the global market in terms of distribution channels. Supermarkets provide deals and offers on products, unlike traditional markets, which further enhances their market value. Apart from retail stores, sales of these products through online channels have also increased in recent years.

The Quick Service Restaurants (QSR) segment is forecasted to grow at a CAGR of 5.56% from 2025 to 2032.

The online sales segment is expected to register the fastest growth in the future.

Soy Sauce Market Regional Outlook

Geographically, the market is studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Soy Sauce Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed 62.03% to the global market in 2025, with a valuation of USD 25.07 billion, and is expected to reach USD 26.55 billion in 2026. This growth is majorly attributed to the presence of leading producers, such as China, as the sauce has been a traditional condiment since the beginning. The evolution of society alongside technological advancements has led to the development of several innovative products in the market. The consumption has increased in the past few decades, thereby supporting the market growth.

The Japan market is valued at USD 2.25 billion by 2026, the China market is valued at USD 12.84 billion by 2026, and the India market is valued at USD 0.17 billion by 2026. China is the leading producer and consumer of such products in the Asia Pacific region and globally. This sauce has been used as an everyday ingredient in Asian cuisines, especially in Southeast Asian countries. Moreover, since the COVID-19 pandemic, the trend of cooking at home has reached its peak, and consumers have tried to mimic their dine-out experience at home. In order to fulfill their taste palate, the consumers prepared various cuisines by using these products at home.

North America

In 2025, North America represented USD 7.51 billion, accounting for 18.59% of the worldwide market, and is expected to reach USD 7.92 billion in 2026. North America remains the second-largest consumer in the world, owing to the increasing adoption of varied foods among consumers.

The U.S. market is valued at USD 7.42 billion by 2026. The U.S. is a major market in the region, which is utilizing a huge quantity of these ingredients in the foodservice and packaged foods sectors to cater to the demand for Asian foods. Some of the microbreweries in the U.S., such as Bourbon Barrel Foods, produce for the domestic market.

Europe

The Europe market generated USD 5.49 billion in 2025, representing 13.59% of the global market landscape, and is expected to reach USD 5.77 billion in 2026. This is owing to the rising interest of consumers in various regional cuisines. Thai, Japanese, and Chinese cuisines are gaining huge popularity in the region, which has necessitated the HoReCa sector serving oriental foods in its outlets. The UK market is valued at USD 1.11 billion by 2026, while the Germany market is valued at USD 0.57 billion by 2026. France is expected to achieve a market size of USD 0.41 billion in 2025.

South America

South America is estimated to be the fourth-largest regional market in 2025, reaching USD 1.30 billion in value. The South American tourism industry has evolved to be an attractive sector in the region. The surge in the number of tourists in South America has opened various opportunities for the culinary space as consumers seek flavors that are similar to their taste palates. Moreover, the increasing number of travelers, especially from Southeast Asia, are in search of umami flavors, which can also drive the incorporation of these sauces in the preparation of desired cuisines.

Middle East & Africa

The Middle East & Africa market was valued at USD 1.04 billion in 2025, capturing 2.58% of global revenue, and is estimated to reach USD 1.09 billion in 2026. Saudi Arabia is expected to contribute USD 0.30 billion to the Middle East & Africa soy sauce market in 2025. The Middle Eastern region is known for its culturally diverse society and is recognized as a home to a large number of people from various nationalities. Due to the surge in working migrants, students, and expatriates, the region is witnessing a massive growth of multiculturalism and with individuals of diversified tastes. The migrants always seek the flavor that they are accustomed to, thus increasing the chances of local production. This can also increase the manufacturer’s profit and can be used in innovating cuisines. Such instances are proven to be helpful in supporting regional growth.

Latin America

The market in Latin America reached USD 1.3 billion in 2025, representing 3.21% of total market revenue, and is projected to reach USD 1.36 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders and Emerging Players Focus on Offering Innovative and Nutritious Products to Increase Presence in Developed Nations

The global market structure is moderately organized owing to the presence of various dominant players in the market. These manufacturers are focusing on the production of innovative and nutritious products to keep up with the ongoing trend. Some of the small players and start-ups are also sharing free samples with consumers to help them try out their products before buying them. Haitian Group, Kikkoman Corp., Nestle S.A., Kraft Heinz, and Yamasa Corporation are some of the key players with a major share in key markets. These manufacturers are also strategizing on expanding their footprints in developed countries, such as the U.S., Canada, and Germany, owing to the growing trend of Asian foods in the region, which, in turn, will aid in fueling the market growth in the coming years.

Major Players in the Soy Sauce Market

Foshan Haitian Flavoring & Food Co. Ltd., Kikkoman Corporation, Lee Kum Kee, YAMASA Corporation, and SEMPIO FOODS COMPANY are the largest players in the market. The global market is fragmented, with the top 5 players accounting for around 18.50% of the global soy sauce market share.

To know how our report can help streamline your business, Speak to Analyst

List of Top Soy Sauce Companies Profiled:

- Foshan Haitian Flavouring & Food Co. Ltd (China)

- Jiajia Food Group Co., Ltd. (China)

- Kikkoman Corporation (Japan)

- Koon Chun Hing Kee Soy & Sauce Factory (China)

- Kraft Heinz Company (U.S.)

- Lee Kum Kee (China)

- Marunaka Shouyu (Japan)

- McCormick & Company Inc. (U.S.)

- Nestle S.A. (Switzerland)

- Shoda Shoyu Co. Ltd. (Japan)

- YAMASA Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS:

- October 2024: Winn, a soy sauce company in India, launched authentic and premium Chinese soy sauce products for the HoReCa sector. The product is made of premium ingredients and is free of artificial ingredients.

- April 2024: Lee Kum Kee announced a brand campaign for its new Supreme Soy Sauce, which aimed to promote culinary excellence and celebrate home cooking moments.

- May 2021: Kraft Heinz Company launched a low-salt version of the popular Master Weijixian soy sauce. The new product contains 28% less salt and is made using dried high-quality scallops in order to create a superior umami taste.

- September 2020: Kraft Heinz invested USD 100 million in a new factory in the Guangdong province of China. The new factory is one of its most significant investments and is projected to produce 200,000 tons of soy sauce annually.

- May 2020: Lee Kum Kee Company Limited announced the launch of a new range of soy sauce products in China, viz. Hoisin Sauce. The new product will offer a combination of this and lime water to meet the country’s demand for innovative sauces.

- August 2019: Kikkoman Corporation inaugurated a new research & development center in Japan to reinforce the country’s focus on taste and innovation in these sauces.

Investment Analysis and Opportunities

The demand for soy sauce is attributed to emerging innovations and a rise in foodservice channels. Thus, to cater to the surging consumer demands for vibrant flavors, the key players are expanding their production facilities in different markets. For instance, in April 2024, Kikkoman Corporation, one of the biggest soy sauce brands, expanded its production facility in the U.S. with an investment of USD 800 million.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, market segmentations, product types, global soy sauce market trends, end-users, and leading distribution channels. Besides this, it offers insights into the market trends, key players, and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth prospects of the market in recent years. Along with this, it provides an analysis of the market dynamics and competitive scenario. Various critical insights presented in the report are an overview of related markets, recent developments, such as mergers, acquisitions, the regulatory situation in prominent countries, and key industry trends.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

Global Soy Sauce Market Scope |

|

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.08% from 2026 to 2034 |

|

Unit |

Value (USD Billion), Volume (Kilotons) |

|

Segmentation |

By Type, Process, End-User, Distribution Channel, and Region |

|

Segmentation |

By Type

· Others |

|

By Process

|

|

|

By End-user

|

|

|

By Distribution Channel · HoReCa · QSR · Supermarkets · Hypermarkets · Convenience Stores · Online sales |

|

|

By Region

|

|

Frequently Asked Questions

Fortune Business Insights says that the value of the market was USD 40.42 billion in 2025 and is projected to record a valuation of USD 73.82 billion by 2034.

Recording a CAGR of 7.08%, the market will exhibit steady growth during the forecast period of 2026-2034.

The light soy sauce is expected to be the leading segment based on type in the global market during the forecast period.

Rising demand for umami foods among consumers is a key factor that drives the growth of the market.

Haitian Group, Kikkoman Corp., and Lee Kum Kee are a few key players in the market.

Asia Pacific held the highest market share in 2026.

The prepared foods is expected to grow at a faster rate in the global market.

Innovations and emerging e-commerce platforms are the major growth factors for the market.

- 2021-2034

- 2025

- 2021-2024

- 292

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us