Solar Inverter Market Size, Share & Industry Analysis, By Inverter Type (Central Inverters, String Inverters, and Micro Inverters), By System Configuration (Grid Connected, Standalone, and Hybrid), By Power Rating (Less than 10 kW, 10 -100 kW, 100 kW - 1 MW, and Above 1 MW), By Phase (Single Phase and Three-Phase), By End-User (Residential, Commercial & Industrial, and Utility), and Regional Forecast, 2026-2034

Solar Inverter Market Size and Future Outlook

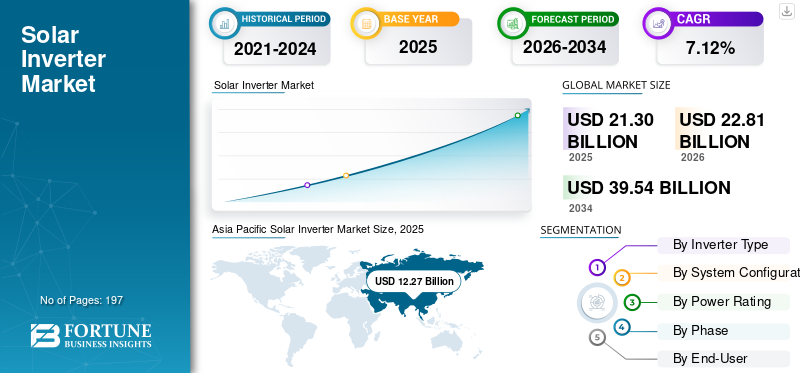

The global solar inverter market size was valued at USD 21.30 billion in 2025. The market is projected to grow from USD 22.81 billion in 2026 to USD 39.54 billion by 2034, exhibiting a CAGR of 7.12% during the forecast period. Asia Pacific dominated the solar inverter market with a market share of 57.60% in 2025.

The market plays a critical role in the global renewable energy ecosystem by enabling the conversion of direct current (DC) electricity generated from solar photovoltaic (PV) systems into usable alternating current (AC) electricity for residential, commercial, industrial, and utility-scale applications. Solar inverters are integrated with advanced power electronics, monitoring software, communication systems, and grid management functionalities to optimize energy generation, improve system efficiency, and ensure grid stability. These systems are widely deployed across rooftop solar installations, distributed generation networks, and large-scale solar farms, making them an indispensable component of modern solar energy infrastructure.

The demand for solar inverters is witnessing strong growth due to the rapid expansion of solar power installations worldwide, increasing investments in renewable energy infrastructure, and supportive government policies promoting clean energy adoption. Rising electricity demand, declining solar power generation costs, and global decarbonization targets are accelerating the deployment of photovoltaic systems across both developed and emerging economies. Additionally, the growing integration of battery energy storage systems, rising adoption of smart energy management solutions, and advancements in digital monitoring technologies are driving the transition toward intelligent and hybrid inverter systems. Industry trends such as decentralized energy generation, grid modernization, smart cities, and energy resilience initiatives are further contributing to market expansion.

The industry is highly competitive and moderately consolidated, characterized by the presence of established power electronics manufacturers, renewable energy technology providers, and regional specialized players. Leading companies including Huawei Technologies Co., Ltd., Sungrow Power Supply Co., Ltd., SMA Solar Technology AG, SolarEdge Technologies Inc., Enphase Energy Inc., and FIMER S.p.A. hold significant market positions through diversified product portfolios, strong distribution networks, and continuous technological innovation. Market participants are increasingly focusing on the development of high-efficiency inverter architectures, AI-enabled monitoring platforms, grid-support functionalities, and energy storage-compatible systems to strengthen their competitive positioning. Strategic initiatives such as capacity expansion, partnerships with EPC contractors and utilities, investments in R&D, and expansion into high-growth solar markets across Asia Pacific, Latin America, and the Middle East & Africa are shaping the competitive landscape and supporting the long-term growth of the market.

Download Free sample to learn more about this report.

Solar Inverter Market Key Takeaways

- 2025 Market Size: USD 21.30 billion

- 2026 Market Size: USD 22.81 billion

- 2034 Forecast Market Size: USD 39.54 billion

- CAGR: 7.12% from 2026–2034

- Asia Pacific dominated the solar inverter market with a 57.60% share in 2025.

- The grid-connected system segment accounted for 77.52% of the market in 2025.

- The three-phase inverter segment held 79.87% of the market in 2025.

Asia Pacific

Valued at USD 12.27 billion in 2025, accounting for 57.60% of the global market.

North America

Reached USD 3.52 billion in 2025, supported by residential and utility-scale solar deployment.

Europe

Accounted for USD 3.89 billion in 2025, driven by strong renewable energy adoption.

U.S

Solar inverter market reached USD 3.07 billion in 2025.

Japan

Market growth is supported by expanding rooftop solar adoption and government renewable energy initiatives.

Read More

Solar Inverter Market Trends

Increasing Deployment of Smart and Hybrid Inverter Technologies to Drive Market Growth

The rapid adoption of smart and hybrid inverter technologies is significantly accelerating the growth of the market. Solar energy system operators and utility providers are increasingly deploying advanced inverter solutions equipped with real-time monitoring, remote diagnostics, artificial intelligence (AI)-enabled optimization, and grid-support functionalities to improve system efficiency and operational reliability. Modern solar inverters are capable of managing dynamic power flows, stabilizing voltage fluctuations, and supporting bidirectional energy transfer between solar systems, battery storage units, and the electricity grid. As solar installations continue to scale across residential, commercial, industrial, and utility applications, the demand for intelligent inverter systems capable of maximizing energy yield and ensuring seamless grid integration is rising substantially.

Furthermore, the growing integration of battery energy storage systems and decentralized renewable energy networks is reinforcing the adoption of hybrid inverter technologies worldwide. Hybrid inverters enable efficient coordination between solar generation, battery storage, and grid electricity, supporting enhanced energy management and backup power capabilities. The increasing implementation of smart grids, distributed energy resources (DERs), and IoT-enabled energy monitoring platforms is also accelerating the transition toward digitally connected inverter ecosystems. These systems improve operational flexibility, reduce energy losses, and enable predictive maintenance, minimizing downtime and maintenance costs.

For instance, in April 2026, Sungrow Power Supply Co., Ltd. introduced its “PowerMatrix” integrated PV-storage platform designed to enhance system-level coordination between solar generation, battery storage, and grid infrastructure. The solution emphasized advanced digital energy management, real-time optimization, and improved grid-forming performance, reflecting the increasing market shift toward AI-enabled and highly integrated renewable energy systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Adoption of Solar Energy and Utility-Scale Projects to Drive Market Growth

The rapid expansion of solar power installations across residential, commercial, industrial, and utility-scale applications is significantly driving solar inverter market growth. Governments and private sector organizations worldwide are increasingly investing in renewable energy infrastructure to reduce carbon emissions, strengthen energy security, and meet long-term decarbonization targets. Inverters based on solar energy play a critical role in photovoltaic systems by converting generated DC electricity into usable AC power while ensuring efficient energy management and grid compatibility. Additionally, the growing deployment of large-scale solar farms and distributed rooftop solar systems is increasing the demand for advanced inverter technologies capable of supporting high energy conversion efficiency, real-time monitoring, and stable grid integration. As solar capacity additions continue to accelerate globally, the demand for reliable and intelligent inverter systems is witnessing substantial growth.

For instance, in February 2025, Huawei Digital Power introduced its next-generation utility-scale smart PV inverter solution featuring advanced grid-forming capabilities and AI-enabled energy optimization functionalities designed to support high-capacity renewable energy integration and large-scale solar deployment projects.

MARKET RESTRAINTS

Intense Price Competition and Margin Pressure to Limit Market Expansion

The market faces significant challenges due to aggressive price competition and declining profit margins. The increasing presence of large-scale manufacturers, particularly from Asia Pacific, has intensified pricing pressure, especially in the utility-scale inverter segment where cost competitiveness plays a critical role in procurement decisions. Rapid technological advancements and frequent product upgrades are further contributing to shorter product replacement cycles and continuous pricing erosion. Additionally, fluctuations in raw material costs, semiconductor supply constraints, and rising logistics expenses can impact manufacturing profitability and operational stability. These factors create financial pressure on manufacturers and may limit the expansion capabilities of smaller and regional market participants.

For instance, in August 2025, SMA Solar Technology highlighted continued pricing pressure and margin challenges within the global inverter industry. This has been observed due to intense competition and declining average selling prices across utility-scale solar projects.

MARKET OPPORTUNITIES

Surging Integration of Energy Storage Systems to Create Growth Opportunities

The increasing deployment of battery energy storage systems alongside solar installations is creating substantial growth opportunities. The growing need for energy resilience, peak load management, and stable renewable energy integration is accelerating the adoption of hybrid inverter systems capable of managing both solar generation and battery storage operations. Advanced hybrid inverters enable bidirectional power flow, intelligent energy optimization, backup power functionality, and enhanced grid interaction, making them increasingly attractive across residential, commercial, and utility-scale applications. Furthermore, the expansion of smart grid infrastructure, virtual power plants, and decentralized energy systems is driving the demand for digitally connected inverter platforms with advanced communication and energy management capabilities.

For instance, in January 2026, SolarEdge Technologies announced the expansion of its hybrid inverter and battery-integrated energy management portfolio aimed at supporting residential and commercial solar-plus-storage deployments with enhanced smart energy optimization capabilities.

MARKET CHALLENGES

Grid Stability Concerns and Regulatory Complexity are Emerging Challenges

The increasing penetration of solar energy into existing electricity networks is creating challenges related to grid stability, power quality management, and regulatory compliance. High levels of intermittent renewable energy generation can lead to voltage fluctuations, frequency instability, and reverse power flow issues, increasing the complexity of grid integration for solar inverter systems. Additionally, evolving grid codes, certification requirements, and country-specific regulatory frameworks require manufacturers to continuously adapt inverter technologies to meet changing compliance standards. Variations in technical standards across different regions can increase development costs and delay product deployment timelines. These challenges are becoming more significant as utilities and grid operators demand advanced inverter functionalities capable of supporting stable and resilient power networks.

For instance, in May 2025, Enphase Energy emphasized the growing importance of advanced grid-support functionalities and compliance-ready inverter architectures designed to address evolving grid stability requirements and regional regulatory standards across high solar penetration markets.

Segmentation Analysis

By Inverter Type

String Inverters Segment Dominated the Market Owing to their Cost Efficiency and Wide Application Range

Based on inverter type, the global market is segmented into central inverters, string inverters, and micro inverters.

The string inverters segment dominated the market in 2025, accounting for approximately 49.20% share, driven by its widespread adoption across residential, commercial, and utility-scale solar installations. String inverters offer a balanced combination of cost efficiency, installation flexibility, simplified maintenance, and high operational reliability, making them highly suitable for distributed as well as medium-to-large-scale photovoltaic systems. The increasing deployment of rooftop solar systems and decentralized renewable energy projects across Asia Pacific, Europe, and North America is further supporting segment growth. Additionally, advancements in smart string inverter technologies with integrated monitoring, remote diagnostics, and grid-support functionalities are strengthening their market position.

The micro inverters segment is an emerging segment poised to grow at a CAGR of 7.58% during the forecast period. The segment growth is driven by the increasing adoption of module-level power electronics in residential solar systems and rising demand for improved energy optimization, panel-level monitoring, and enhanced safety features.

By System Configuration

Grid-Connected Segment Led the Market due to Expanding Utility-Scale Solar Deployment

Based on system configuration, the global market is segmented into grid-connected, standalone, and hybrid systems.

The grid-connected segment dominated the market, accounting for approximately 77.52% share in 2025, driven by the rapid expansion of utility-scale and distributed grid-tied solar projects worldwide. Grid-connected inverters are extensively deployed in residential, commercial, and industrial photovoltaic systems due to their ability to synchronize efficiently with utility grids while enabling optimized power distribution and energy export functionalities. Supportive renewable energy policies, feed-in tariffs, and net metering programs across major solar markets are further accelerating adoption.

The hybrid systems segment is projected to witness the fastest growth, expanding at a CAGR of 13.46% during the forecast period. The segment growth is driven by the increasing integration of battery energy storage systems with solar installations and rising demand for energy resilience and backup power solutions.

By Power Rating

Above 1 MW Segment Led the Market Owing to Rising Usage in Utility-Scale Photovoltaic Installations

Based on power rating, the global market is segmented into up to 10 kW, 10–100 kW, 100 kW–1 MW, and above 1 MW.

The above 1 MW segment dominated the global solar inverter market share, accounting for approximately 29.27% share in 2025, driven by the rapid deployment of large-scale utility solar farms and high-capacity renewable energy projects across China, the Middle East, the U.S., and India. These high-power inverter systems are widely utilized in utility-scale photovoltaic installations due to their ability to support centralized energy conversion, improved operational efficiency, and lower system-level installation costs.

The 10–100 kW segment is emerging as the fastest-growing segment in the global market. The segment is projected to expand at a CAGR of 8.42% during the forecast period. The segment growth is primarily driven by the rapid expansion of commercial & industrial (C&I) solar installations across small and medium-sized enterprises, office buildings, educational institutions, warehouses, retail facilities, and manufacturing units. Businesses are increasingly adopting medium-capacity solar systems to reduce dependence on conventional grid electricity, manage rising energy costs, and meet sustainability and carbon reduction targets.

By Phase

Three-Phase Inverters Segment Held the Largest Share Due to Strong Commercial and Utility Demand

Based on phase, the global market is segmented into single phase and three-phase systems.

The three-phase segment dominated the market, accounting for approximately 79.87% share in 2025, driven by its extensive utilization across commercial, industrial, and utility-scale solar installations. Three-phase inverters provide higher power handling capacity, improved grid stability, and enhanced operational efficiency, making them highly suitable for large-scale photovoltaic systems and energy-intensive applications. The growing deployment of commercial rooftop solar projects, industrial renewable energy systems, and utility-scale solar farms is significantly supporting segment growth.

The single phase segment is projected to grow at a CAGR of 3.43% during the forecast period of 2026-2034.

By End-User

To know how our report can help streamline your business, Speak to Analyst

Utility Segment Dominated the Market Due to Rapid Expansion of Large Solar Projects

Based on end-user, the global market is segmented into residential, commercial & industrial, and utility.

The utility segment dominated the market, accounting for approximately 37.94% share in 2025, driven by the rapid deployment of large-scale photovoltaic power plants across Asia Pacific, the Middle East, North America, and Europe. Utility-scale solar projects require high-capacity and highly efficient inverter systems capable of supporting large energy loads, stable grid integration, and centralized monitoring operations. Increasing government investments in renewable energy infrastructure, rising utility decarbonization targets, and the growing development of gigawatt-scale solar parks are significantly supporting segment growth.

The commercial & industrial segment is emerging as the fastest-growing segment, projected to expand at a CAGR of 7.80% during the forecast period. The segment growth is driven by the increasing adoption of rooftop solar systems across manufacturing facilities, warehouses, office buildings, shopping complexes, healthcare facilities, and educational institutions. Moreover, favorable government incentives, net metering policies, and the rising integration of battery storage systems are accelerating the deployment of medium-capacity commercial solar installations. Advancements in smart inverter technologies, remote monitoring platforms, and AI-enabled energy optimization systems are further enhancing operational efficiency and encouraging wider adoption across the commercial sector.

Solar Inverter Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Solar Inverter Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region dominated the global market, accounting for approximately USD 12.27 billion in 2025. The market in Asia Pacific is growing due to the rapid expansion of utility-scale solar projects, increasing rooftop solar adoption, and strong government support for renewable energy deployment across major economies such as China, India, Japan, and Australia. The region benefits from large-scale photovoltaic manufacturing capacity, aggressive solar installation targets, and rising investments in grid modernization infrastructure, which are accelerating the deployment of advanced string, central, and hybrid inverter systems. Additionally, declining solar generation costs, increasing energy demand, and favorable policy frameworks are further supporting market growth across the region.

China Solar Inverter Market

In 2025, the China market reached approximately USD 6.40 billion. The market is growing due to the extensive deployment of utility-scale solar farms, strong domestic manufacturing capabilities, and increasing adoption of smart inverter technologies across large-scale renewable energy projects. Government initiatives supporting renewable energy expansion and grid modernization are further accelerating market expansion.

India Solar Inverter Market

The India market reached a value of around USD 1.56 billion in 2025. The growth is driven by rising rooftop solar adoption, expanding utility-scale solar capacity, and increasing investments in distributed renewable energy infrastructure. Supportive government schemes and growing demand for decentralized power generation are further strengthening inverter deployment across the country.

North America

The North America market was valued at approximately USD 3.52 billion in 2025. The regional market is growing due to the increasing deployment of residential and utility-scale solar installations, rising adoption of energy storage-integrated solar systems, and favorable clean energy policies across the U.S. and Canada. The region is witnessing strong investments in grid-supportive inverter technologies, smart energy management systems, and solar-plus-storage infrastructure aimed at improving energy resilience and grid stability.

U.S. Solar Inverter Market

The U.S. market reached a value of around USD 3.07 billion in 2025. The growth is driven by increasing utility-scale solar investments, rising residential rooftop solar adoption, and expanding deployment of hybrid inverter systems integrated with battery storage technologies. Federal renewable energy incentives and grid modernization initiatives are further accelerating market expansion.

Europe

The Europe regional market accounted for approximately USD 3.89 billion in 2025. The market in Europe is growing due to strong renewable energy targets, increasing rooftop solar deployment, and rising adoption of smart energy management systems across residential and commercial sectors. The region is at the forefront of energy transition initiatives, with increasing investments in hybrid inverter technologies, battery-integrated solar systems, and grid-supportive renewable infrastructure.

Germany Solar Inverter Market

The Germany market touched a value of approximately USD 1.05 billion in 2025. The market is supported by high rooftop solar penetration, strong adoption of residential battery storage systems, and increasing investments in decentralized renewable energy infrastructure.

Italy Solar Inverter Market

The Italy market reached a value of around USD 0.60 billion in 2025. The growth is driven by expanding commercial rooftop solar installations, favorable renewable energy incentives, and increasing demand for hybrid inverter solutions integrated with smart energy management systems.

Latin America

The Latin America market accounted for approximately USD 1.09 billion in 2025. The market is primarily driven by expanding solar installations across utility-scale and distributed generation projects, particularly in Brazil, Chile, and Mexico. Increasing investments in renewable energy infrastructure, rising electricity demand, and favorable solar resource availability are accelerating the deployment of advanced inverter technologies across the region.

Brazil Solar Inverter Market

The Brazil market reached a value of around USD 0.48 billion in 2025. The growth is supported by strong distributed solar generation adoption, increasing residential and commercial rooftop solar installations, and favorable net metering policies encouraging renewable energy investments.

Middle East & Africa

The Middle East & Africa market accounted for approximately USD 0.53 billion in 2025. The market is witnessing strong growth due to increasing investments in utility-scale solar projects, rising focus on energy diversification, and expanding renewable energy infrastructure across the Gulf countries, South Africa, and North African economies. The gradual adoption of hybrid and grid-supportive inverter technologies is helping utilities and commercial operators improve energy efficiency and grid reliability.

GCC Solar Inverter Market

The GCC market reached a valuation of around USD 0.23 billion in 2025. The growth is driven by large-scale solar park developments, increasing government renewable energy targets, and rising deployment of utility-scale central inverter systems across the region.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS:

Leading Companies to Expand Smart and Hybrid Inverter Portfolios to Strengthen Market Position

The global solar inverter market is moderately consolidated, characterized by the presence of established power electronics manufacturers, renewable energy technology providers, and regional solar equipment companies competing through technological innovation, manufacturing scale, and integrated energy management capabilities. Leading participants such as Huawei Technologies Co., Ltd., Sungrow Power Supply Co., Ltd., SMA Solar Technology AG, SolarEdge Technologies Inc., and others maintain strong market positions through diversified portfolios of string inverters, central inverters, hybrid inverters, battery-integrated systems, and AI-enabled energy management platforms.

In April 2025, Sungrow Power Supply Co., Ltd. launched its next-generation “1+X 2.0 Modular Inverter” platform for utility-scale solar applications featuring AI-enabled fault detection and advanced grid-forming functionalities designed to improve large-scale renewable energy integration.

LIST OF KEY SOLAR INVERTER COMPANIES PROFILED

- Huawei Technologies Co., Ltd. (China)

- Sungrow Power Supply Co., Ltd. (China)

- SMA Solar Technology AG (Germany)

- SolarEdge Technologies Inc. (Israel)

- Enphase Energy Inc. (U.S.)

- FIMER S.p.A. (Italy)

- Delta Electronics, Inc. (Taiwan)

- Fronius International GmbH (Austria)

- Sineng Electric Co., Ltd. (China)

- Growatt New Energy Technology Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- January 2026: SolarEdge Technologies expanded its hybrid inverter portfolio with enhanced smart energy management capabilities for residential and commercial solar-plus-storage systems. The upgraded solutions included advanced energy optimization, battery integration, and real-time monitoring functionalities. The expansion reflected the growing demand for decentralized and intelligent energy management systems.

- November 2025: SMA Solar Technology AG expanded its utility-scale inverter portfolio with new high-capacity central inverter solutions for large solar power plants. The systems incorporated advanced grid-support capabilities, predictive maintenance functionalities, and enhanced power conversion efficiency. The launch focused on improving operational reliability and grid stability in utility-scale renewable energy projects.

- September 2025: Enphase Energy launched upgraded micro inverter systems with improved battery storage compatibility and advanced residential energy management functionalities. The new systems enhanced module-level monitoring, rooftop energy optimization, and smart home energy integration capabilities. The development supported the growing adoption of residential solar-plus-storage systems.

- June 2025: Delta Electronics India bagged an order from KP Group for supplying solar PV inverters with around 1 GW capacity over the following 12 months. The deals forms part of three MoUs (Memorandums of Understanding) inked between the two companies for supporting energy storage, green hydrogen, solar, and EV charging infrastructure projects.

- April 2025: Sungrow Power Supply Co., Ltd. launched its “1+X 2.0 Modular Inverter” platform for utility-scale solar and energy storage projects. The solution featured AI-enabled fault detection, advanced grid-forming capabilities, and modular scalability for large photovoltaic installations. The launch aimed to improve grid stability, operational efficiency, and solar-plus-storage integration across utility-scale renewable energy projects.

REPORT COVERAGE

The global solar inverter market analysis provides an in-depth study of the market size and forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.12% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Inverter Type, By System Configuration, By Power Rating, By Phase, By End-User, and Region |

| By Inverter Type |

|

| By System Configuration |

|

| By Power Rating |

|

| By Phase |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 21.30 billion in 2025 and is projected to reach USD 39.54 billion by 2034.

The market is expected to exhibit a CAGR of 7.12% during the forecast period (2026-2034).

The utility segment led the market in terms of end-user in 2025.

The increasing deployment of smart and hybrid inverter technologies is a key factor driving market growth.

Huawei Technologies Co., Ltd, Sungrow Power Supply, and SMA Solar technology are the prominent players in the market.

Asia Pacific dominated the market with the highest share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 197

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us