Solar PV Backsheet Market Size, Share & Industry Analysis, By Product (TPT-primed, TPE, PET, PVDF, PEN, Others), By Thickness (< 100 Micrometer, 100 to 500 Micrometer, >500 Micrometer), By Material (Fluoride and Non-fluoride), By Technology (Crystalline, Thin Film, Ultra-thin Film) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

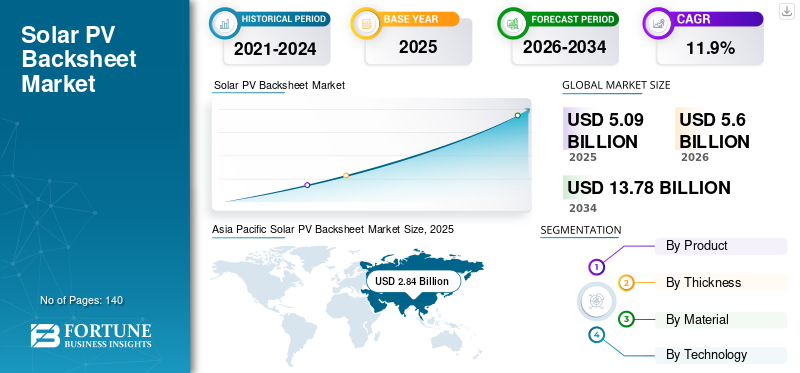

The global solar PV backsheet market size was valued at USD 5.09 billion in 2025 and is expected to reach USD 5.60 billion in 2026. Furthermore, the market is projected to reach USD 13.78 billion by 2034, exhibiting a CAGR of 11.9% during the forecast period of 2026-2034. Asia Pacific dominated the global market with a market share of 55.79% in 2025, supported by large-scale solar installations, aggressive renewable energy targets, and expanding domestic manufacturing capacity in countries such as China, India, and South Korea.

Solar PV backsheets are critical protective layers used on the rear side of photovoltaic modules to ensure electrical insulation, mechanical protection, and long-term durability against environmental stressors such as ultraviolet radiation, humidity, and temperature fluctuations. As global solar deployment accelerates across utility-scale, commercial, and residential segments, demand for high-performance and long-lifespan backsheet materials continues to strengthen.

- According to the International Renewable Energy Agency, global solar PV capacity additions exceeded 400 GW in 2024, with Asia Pacific accounting for more than 55% of total installations, significantly boosting backsheet consumption volumes.

Key manufacturers are actively investing in fluorine-free and recyclable backsheet technologies to address sustainability concerns while maintaining performance standards. Leading players include DuPont, Coveme, Krempel, Cybrid Technologies, and others.

Download Free sample to learn more about this report.

Solar PV Backsheet Market Key Takeaways

- 2025 Market Size: USD 5.09 Billion

- 2026 Market Size: USD 5.60 Billion

- 2034 Forecast Market Size: USD 13.78 Billion

- CAGR: 11.9% from 2026–2034

- Asia Pacific dominated the solar PV backsheet market with a 55.79% share, generating USD 2.84 billion in 2025.

- The TPT-primed segment held the largest market share of 40.2% in 2025.

- The 100 to 500 Micrometer segment dominated the market with a 61.2% share in 2025.

Asia Pacific

Asia Pacific generated USD 2.84 billion in 2025, driven by large-scale solar installations and strong manufacturing capabilities in China, India, and Japan.

North America

North America accounted for USD 0.81 billion in 2025, supported by investments in utility-scale solar projects and grid modernization.

Europe

Europe generated USD 0.93 billion in 2025, driven by steady solar deployment and stringent environmental regulations.

U.S.

The solar PV backsheet market reached USD 0.54 billion in 2025.

Japan

The solar PV backsheet market was valued at USD 0.35 billion in 2025.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Growth of Solar Energy Capacity is Driving Demand for Advanced Backsheet Materials

The rapid growth of solar energy capacity worldwide is driving demand for solar backsheets across all application segments. Governments are increasingly investing in renewable energy infrastructure to reduce carbon emissions and improve energy security. This shift is driving demand for high-quality solar panels and, in turn, reliable backsheet materials that can withstand long-term exposure to heat, moisture, and ultraviolet radiation.

In high-growth regions such as the Asia Pacific, large utility-scale projects require backsheets that provide consistent electrical insulation and environmental resistance under demanding climatic conditions. As solar installations continue to scale up, manufacturers are placing greater emphasis on material performance to ensure stable output and safety throughout the system’s lifespan.

For example, India continues to announce large-scale solar tenders as part of its renewable energy targets, directly supporting demand for PV modules and their associated components, including backsheets.

Focus on Durability and Reliability Supports the Market Growth

As the solar industry matures, buyers are increasingly prioritizing lifecycle value over initial production cost. Module manufacturers now routinely offer warranties of 25 years or more, making long-term performance and reliability a critical selling point. Backsheets that fail prematurely can lead to electrical faults, reduced output, and costly replacements, prompting manufacturers to invest in proven and well-tested solutions.

- In September 2024, several large-scale solar developers in Europe revised procurement guidelines to include extended material testing data for backsheets, reflecting a broader industry shift toward lifecycle-based purchasing decisions. This focus continues to support market growth for high-quality solar backsheets.

This focus on reliability is particularly important in utility-scale solar plants, where maintenance costs and downtime can significantly impact project economics. As a result, demand for high-quality solar backsheets continues to rise, supporting sustained market growth across the globe.

MARKET RESTRAINTS

Raw Material Price Volatility Impacts Production Cost of Solar PV Backsheets

Despite strong demand fundamentals, the market faces challenges related to fluctuating raw material prices. Key backsheet materials such as fluoropolymers and PET films are subject to supply chain disruptions and regulatory pressures, which can increase production costs for manufacturers. Hence, such factors can hinder the market's growth.

- In May 2025, the European Commission advanced discussions on solar module sustainability and recycling requirements under its circular economy framework. This development encouraged several European module manufacturers to prioritize eco-friendly solar PV backsheets, creating fresh opportunities for market expansion.

Smaller players operating in low-growth regions are particularly exposed to these cost pressures, as they have a limited ability to pass price increases on to customers. This creates margin pressure and can slow capacity expansion in certain regions, creating an impact on production costs.

MARKET OPPORTUNITIES

Sustainable Solar PV Backsheet Materials Support the Future Market Expansion across the Globe

Environmental considerations are increasingly shaping purchasing decisions across the solar value chain. Manufacturers are investing in fluorine-free and recyclable backsheet materials to align with sustainability goals and emerging regulations, particularly in Europe.

These developments open new opportunities for market expansion, as eco-friendly solar PV backsheets gain acceptance among module manufacturers seeking to differentiate their products while maintaining performance standards.

MARKET CHALLENGES

Balancing Sustainability Goals with Technical Performance May Impact the Market

While environmentally friendly backsheet materials offer clear long-term benefits, ensuring durability and electrical insulation performance comparable to conventional fluoropolymer-based backsheets remains a key challenge for the solar industry. Traditional backsheets have a long operating history and proven resistance to ultraviolet radiation, moisture ingress, thermal cycling, and mechanical stress across diverse climates. These characteristics are critical for protecting solar panels from electrical leakage, insulation failure, and accelerated degradation over multi-decade operating lifetimes.

In contrast, many newer fluorine-free and recyclable backsheet materials are still progressing through extended field validation phases. Although laboratory testing often shows promising results, real-world operating conditions such as high humidity, desert heat, snow load, and sustained UV exposure can reveal performance gaps over time. Issues such as micro-cracking, reduced adhesion between layers, and gradual loss of electrical insulation properties can emerge only after years of operation, raising concerns for module manufacturers and project developers.

- In November 2024, industry testing agencies highlighted that certain early-generation fluorine-free backsheets showed accelerated aging under extreme UV conditions, underscoring the need for continued material innovation and extended field validation before large-scale adoption.

Overcoming these challenges requires sustained investment in material science, long-duration field testing, and close collaboration between PV backsheet suppliers and module manufacturers. As performance data accumulates and confidence improves, environmentally friendly solar backsheets are expected to see broader acceptance, but achieving parity with established solutions remains a critical hurdle in the near to medium term.

SOLAR PV BACKSHEET MARKET TRENDS

Increasing Adoption of Bifacial Solar Panel Designs Are Influencing the Solar PV Backsheet Demand

The increasing adoption of bifacial solar panels is influencing the design and functionality of solar backsheets. Reflective and transparent backsheets are being used to improve rear side energy yield while maintaining insulation performance.

- In February 2025, multiple utility scale projects in the Middle East adopted reflective backsheets for bifacial modules to enhance output in high albedo environments, reinforcing the relevance of backsheets even as dual glass modules gain traction.

Download Free sample to learn more about this report.

IMPACT OF TARIFFS

U.S. tariffs change the cost of solar PV panels and upstream inputs, which shifts project economics and sourcing, and that ultimately changes the volume and mix of solar PV backsheet materials ordered. At the same time, tariffs encourage local manufacturing and supply chain diversification, especially in regions like the Asia Pacific, North America, and Europe. This can benefit backsheet suppliers with regional production capabilities and strong relationships with domestic module manufacturers.

Overall, tariffs do not change the long term outlook for the solar PV backsheet market, which remains driven by the increasing demand for renewable energy and market growth in solar installations, but they do create short term volatility in demand, pricing, and sourcing decisions.

SEGMENTATION ANALYSIS

By Product Type

TPT primed backsheets accounted for the largest market share in 2025 due to their established reliability and strong resistance to environmental stress.

By Product Type, the Solar PV Backsheets market is segmented into TPT-primed, TPE, PET, PVDF, PEN, and others. TPT-primed dominated the market in 2025, with a market share of 40.2% owing to its strength and volatility.

Meanwhile, PET emerges as the fastest-growing segment, gaining traction through cost-effective blending capabilities, improved furnace flexibility, and rising demand from capacity expansions in emerging steel hubs, reshaping market dynamics with versatile performance.

By Thickness

100 to 500 Micrometer Segment Dominates the Market Due to its balanced mechanical strength, electrical insulation, and cost efficiency.

By thickness, the market is segmented into < 100 Micrometer, 100 to 500 Micrometer and > 500 Micrometer.

100 to 500 Micrometer dominated the market in 2025 with a market share of 61.2%, keeping production cost under control, making it suitable for utility scale, commercial, and residential applications.

Meanwhile, < 100 Micrometer emerges as the fastest-growing segment, driven by the increasing adoption of thinner solar PV backsheets to reduce overall module weight and material usage, especially in cost sensitive and rooftop installations.

By Material

Fluoride-based Backsheets Hold the Largest Market Share Due to Their Proven UV Resistance and Long Operating Life

By material, the market is bifurcated into fluoride and non-fluoride.

Fluoride-based backsheets continue to dominate the Solar PV Backsheet Market due to their proven UV resistance, long operational life, and superior electrical insulation properties. These materials are essential for ensuring the durability and reliability of solar modules, especially in extreme climates where UV exposure and high temperatures are prevalent.

The rigid structure and thermal stability of fluoride-based backsheets make them ideal for protecting solar panels in high-stress environments, where the panels are exposed to prolonged sunlight, fluctuating temperatures, and harsh environmental conditions. Additionally, fluoride-based backsheets help maintain optimal module performance and reduce degradation over time, ensuring that solar panels continue to perform efficiently over their expected lifespan.

- In 2025, a large-scale solar project in the Middle East utilized fluoride-based backsheets for its solar panels, ensuring long-term protection against the region’s harsh desert conditions. The extreme UV exposure and high temperatures made fluoride-based backsheets the ideal choice due to their excellent UV resistance and thermal stability, contributing to the reliability and longevity of the solar modules.

Overall, fluoride-based backsheets remain the top choice for utility-scale solar projects and installations in extreme climates because of their durability, UV protection, and ability to maintain long-term performance in harsh environments.

The Non-Fluoride based segment is projected to grow at a CAGR of 12.9% over the forecast period.

By Technology

To know how our report can help streamline your business, Speak to Analyst

Based on technology, the market is categorized into crystalline, thin film, and ultra-thin film.

Crystalline Technology Dominates the Market Due to Its Widespread Adoption in Global Solar Panel Installations

Crystalline technology remains the dominant force in the Solar PV market, largely due to its widespread adoption and proven efficiency. Crystalline silicon solar panels continue to account for the largest share of global solar panel installations, driving the consistent demand for solar backsheets that ensure electrical insulation and mechanical protection for these panels.

The high efficiency and cost-effectiveness of crystalline technology make it the preferred choice for residential, commercial, and utility-scale solar installations. As crystalline panels make up the majority of deployed solar capacity, their demand for high-performance backsheets continues to grow steadily, securing a large market share for crystalline-backed solar panels.

- In 2024, a utility-scale solar farm in California incorporated crystalline silicon panels with high-quality backsheets to improve performance and extend the lifespan of the system. Given the panel’s significant market share in global installations, the demand for high-quality crystalline silicon solar backsheets grew in line with the farm's expected 30+ year operational life, ensuring long-term protection and efficiency of the solar panels.

Overall, the crystalline technology dominates the market, driven by its widespread adoption and efficiency, ensuring the consistent demand for high-performance backsheets that protect and enhance the lifespan of solar panels across the globe.

The Ultra-thin Film based segment is projected to grow at a CAGR of 15.0% over the forecast period.

SOLAR PV BACKSHEET MARKET REGIONAL OUTLOOK

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Solar PV Backsheet Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific Dominates the Solar PV Backsheet Market due to large scale solar manufacturing, high installation volumes, and strong policy support

The Asia Pacific Solar PV Backsheet Market emerged as the largest market with a valuation of USD 2.84 billion in 2025, supported by China’s extensive solar panel manufacturing base, India’s rapid capacity additions, and steady demand from mature markets such as Japan. Increased demand for solar panels across utility scale and rooftop projects continues to drive market growth in the region.

China Solar PV Backsheet Market

China leads the Regional Market Due to its dominance in solar panel manufacturing and domestic installations.

The China Solar PV Backsheet market was valued at USD 1.54 billion in 2025. High module production volumes, export oriented manufacturing, and continuous solar deployment sustain strong demand for backsheet materials, although gradual shifts toward sustainability standards may influence future material choices.

Japan Solar PV Backsheet Market

Japan maintains Stable Demand Due to its focus on quality, safety standards, and long term reliability.

The Japan Solar PV Backsheet market reached USD 0.35 billion in 2025. Strict performance requirements and long warranty expectations encourage the adoption of high reliability solar backsheets that enhance module durability.

India Solar PV Backsheet Market

India is expected to Witness Strong Growth Due to rapid solar capacity additions and domestic manufacturing initiatives.

The India Solar PV Backsheet market was valued at USD 0.51 billion in 2025. Government-led renewable energy targets and increasing installations are driving demand for cost-effective backsheet materials that balance performance and production cost.

North America

North America Accounts for a Significant Market Share Due to steady utility scale solar expansion and domestic manufacturing incentives.

The North America Solar PV Backsheet Market was valued at USD 0.81 billion in 2025. Ongoing investments in large solar projects and grid modernization support consistent demand, while increasing localization influences supplier selection and competitive dynamics.

U.S. Solar PV Backsheet Market

The U.S. Market is Driven by Utility Scale Installations and Growing Focus on Domestic Supply Chains.

The U.S. Solar PV Backsheet market reached USD 0.54 billion in 2025. Strong solar project pipelines and incentives supporting domestic manufacturing continue to drive demand for reliable and compliant backsheet materials.

Europe

Europe holds the Largest Share Due to strong renewable targets and sustainability focused procurement.

The Europe Solar PV Backsheet Market was valued at USD 0.93 billion in 2025. Solar deployment remains steady across major economies, while environmental regulations and recycling requirements influence material selection and product development.

Germany Solar PV Backsheet Market

Germany remains a Key Market Due to consistent solar installations and high-quality standards.

The German Solar PV Backsheet market was valued at USD 0.18 billion in 2025. Emphasis on performance, safety, and sustainability continues to support demand for advanced backsheet materials.

Latin America

Latin America is Experiencing Market Expansion Due to growing utility scale solar projects.

The Latin America Solar PV Backsheet Market was valued at USD 0.25 billion in 2025. Large solar parks and rising renewable investments in countries such as Brazil and Chile are driving increased demand for solar backsheets.

Brazil Solar PV Backsheet Market

Brazil leads the Regional Market Due to its large scale solar capacity additions.

The Brazil Solar PV Backsheet market reached USD 0.14 billion in 2025. Expanding utility scale projects and favorable solar resources continue to support steady backsheet demand.

Middle East & Africa

Middle East & Africa are emerging as a Growth Region Due to large solar megaprojects and energy diversification efforts.

The Middle East & Africa Solar PV Backsheet Market was valued at USD 0.27 billion in 2025. Solar plays an increasing role in regional energy strategies, driving demand for durable backsheet materials suited for harsh climates.

GCC Solar PV Backsheet Market

GCC Shows Growing Adoption Due to large utility scale solar developments.

The GCC Solar PV Backsheet market was valued at USD 0.12 billion in 2025. Increasing solar investments and high irradiation conditions support demand for high performance backsheets that ensure long term reliability.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Are Engaged in Partnerships and Mergers to Increase Market Share in the Future.

The competitive landscape of the Solar PV Backsheet Market is moderately consolidated, with companies competing on product performance, cost efficiency, and sustainability credentials.

Key Players

List of the Key Solar PV Backsheet Market Companies Profiled:

- DuPont (U.S.)

- Coveme S.p.A. (Italy)

- Krempel GmbH (Germany)

- Cybrid Technologies Inc. (China)

- Hangzhou First Applied Material Co., Ltd. (China)

- Taiflex Scientific Co., Ltd. (Taiwan)

- Isovoltaic AG (Austria)

- Jolywood Solar Technology Co., Ltd. (China)

- SKC Co., Ltd. (South Korea)

- Mitsubishi Chemical Group Corporation (Japan)

- Toray Industries, Inc. (Japan)

- Arkema S.A. (France)

- SABIC (Saudi Arabia)

- 3M Company (U.S.)

- Uflex Limited (India)

- Kuraray Co., Ltd. (Japan)

- Toyobo Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- In October 2025, DuPont expanded its Tedlar backsheet production capacity in Asia to support rising demand from export oriented solar module manufacturers.

- In August 2025, Jolywood Solar launched a new fluorine free backsheet line targeting European markets with strict sustainability requirements.

- In June 2024, Coveme entered into a long term supply agreement with a European module producer to supply PET based solar backsheets

REPORT COVERAGE

The Solar PV Backsheet Market report delivers a detailed insight into the market. It focuses on key aspects, such as leading companies in the Market. Additionally, the report provides regional insights and global market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several other factors and challenges that contributed to the market's growth and decline in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.9% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product · TPT-primed · TPE · PET · PVDF · PEN · Others |

|

By Thickness · <100 Micrometer · 100 to 500 Micrometer · >500 Micrometer |

|

|

By Material · Fluoride · Non Fluoride |

|

|

By Technology · Crystalline · Thin Film · Ultra-Thin Film |

|

|

By Region

|

Frequently Asked Questions

According to a Fortune Business Insights study, the market size was USD 5.09 billion in 2025.

The market is likely to grow at a CAGR of 11.9% over the forecast period (2026-2034).

The TPT-primed segment is expected to lead the market over the forecast period.

The market size of the Asia Pacific stood at USD 2.84 billion in 2025.

Rising Solar Installations Are Driving Demand for Advanced Backsheet Materials

Some of the top players in the market include DuPont, Coveme S.p.A., Krempel GmbH, Cybrid Technologies Inc., and others.

The global market size is expected to reach USD 13.78 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us