Space Mining Market Size, Share & Industry Analysis, By Celestial Body (Asteroids, Moon, and Mars), By Resource Type (Metals, Water/Ice, Helium-3, Rare Earth Elements, and Others), By Technology (Robotic Mining, Human-Assisted Missions, and ISRU (In-Situ Resource Utilization)), By Application (Propellant, Life Support, Export to Earth, Construction Material, and Others), and Regional Forecast, 2026-2034

Space Mining Market Size and Future Outlook

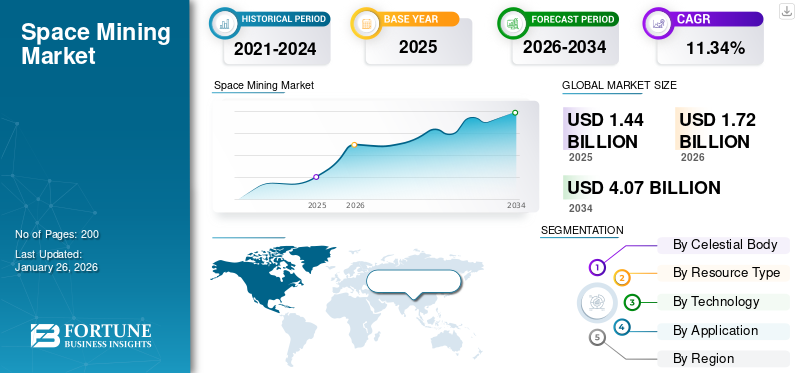

The global space mining market size was valued at USD 1.44 billion in 2025. The market is projected to grow from USD 1.72 billion in 2026 to USD 4.07 billion by 2034, exhibiting a CAGR of 11.34% during the forecast period. North America dominated the ESG Investing market with a market share of 72.25% in 2025.

Space mining refers to the process of extracting and utilizing resources obtained from celestial bodies including Moon, asteroids, and Mars. The main motive of space mining is to extract and supply materials for fuel, life support, and construction in space. Space mining is expected to reduce launch costs and make deep space missions more sustainable. The key targets of the mining missions are lunar polar water ice, near-Earth asteroids rich in platinum-group metals.

Key government and space agencies involved in the industry including NASA, European Space Agency (ESA), JAXA (Japan) fund various missions such as VIPER, Hayabusa are used to map and test resource extraction. Moreover, private key players such as AstroForge, ispace are developing technology for asteroid sampling and lunar resource delivery.

Download Free sample to learn more about this report.

Space Mining Market KEY TAKEAWAYS

- 2025 Market Size: USD 1.44 billion

- 2026 Market Size: USD 1.72 billion

- 2034 Forecast Market Size: USD 4.07 billion

- CAGR: 11.34% from 2026–2034

- North America dominated the space mining market with a 72.25% share in 2025.

- The moon segment is expected to account for the largest market share of 61.26% in 2026.

- The water/ice segment is expected to capture the largest market share of 50.92% in 2026.

North America

Valued at USD 1.04 billion in 2025, supported by strong government and private investments in space exploration and ISRU technologies.

Europe

Valued at USD 0.20 billion in 2025, driven by strategic collaborations and investments in lunar exploration and resource extraction technologies.

Asia Pacific

Valued at USD 0.15 billion in 2025, driven by expanding space exploration programs and lunar resource missions in China, Japan, and India.

U.S.

Projected to reach USD 1.13 billion by 2026, supported by NASA-led lunar missions and growing private sector investments.

Japan

Projected to reach USD 0.02 billion by 2026, driven by increasing participation in space exploration and resource utilization initiatives.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rise in Demand for Critical Metals and Rare Minerals, and Rare Earth Elements to Propel Market Growth

The increase in demand for critical metals and rare minerals is expected to act as a major driver of the market during the forecast period. These materials encompass platinum, nickel, cobalt, and other rare earth elements. Such materials are essential for high-tech industries such as electronics, renewable energy, and electric vehicles. As the reserves of these metals are limited on Earth and concentrated in a few countries, this is expected to create supply issues.

- For instance, in February 2025, AstroForge, a California-based aerospace company, launched its Odin mission as part of its ambitious plan to extract precious metals from asteroids.

Therefore, increase in demand for critical metals and rare earth metals required for high tech industries coupled with limitations related to terrestrial mining is pushing the growth of the market during the forecast period.

MARKET RESTRAINTS

High Cost & Technical Complexity to Restrict Market Expansion

A major restraint that the market is facing is the high cost and technical complexity of developing and operating extraterrestrial resource-extraction missions. The mining activities on the Moon, asteroids and other celestial bodies requires highly specialized spacecraft, robotic systems, and processing equipment capable of withstanding extreme conditions such as radiation, vacuum, and severe temperature fluctuations. The design, testing, and deployment of such technologies require significant investment and cutting-edge engineering expertise.

MARKET OPPORTUNITIES

Development of In-Situ Resource Utilization (ISRU) Infrastructure and Services to Create Lucrative Growth Opportunities

As lunar and deep-space missions’ increase, there is a significant opportunity for companies to design, build, and operate ISRU systems that convert mined materials into usable products such as oxygen, building aggregates, and radiation-shielding blocks. The establishment of processing plants on the Moon is expected to decrease mission spending for space agencies and space firms in the private sector as it reduces resupplying materials from Earth. Such facilities can be then used to design lunar habitats, landing pads and solar arrays to help long duration stays during space missions. Moreover, numerous space agencies are investing in the development of missions and programs aimed to test technologies for In-Situ Resource Utilisation (ISRU).

- For instance, in September 2025, The European Space Agency (ESA) is developing a lunar surface mission to test technologies for In-Situ Resource Utilisation (ISRU). Its main objective is to prove by 2025 that oxygen and possibly water can be produced directly from lunar soil (regolith).

SPACE MINING MARKET TRENDS

Surge in Integration of Robotics and Autonomous Systems for Off-Earth Resource Extraction is a Significant Market Trend

A notable market trend in the space mining industry is the increasing integration of robotics and autonomous systems for off-Earth resource extraction. Since the extraction of resources from lunar and asteroid environments is extremely difficult and hazardous, numerous companies and space agencies are focusing on development and use of advanced robotics for this procedure.

- For instance, in March 2025, China revealed the “Interstellar Miner,” a six-legged bionic robot built by the China University of Mining and Technology to mine resources on the Moon and near-Earth asteroids.

Download Free sample to learn more about this report.

Such technologies focus on the improvement of efficiency, reduction of mission risks, and cutting costs by reducing the need for human intervention in resource extraction process/task. In addition, there is a rise in involvement of private space agencies such as Asteroids in this trend by the creation of robotic systems capable of prospecting and sampling asteroids. All such factors are expected to present significant growth opportunities for the space mining market growth.

MARKET CHALLENGES

Lack of a Clear and Unified Legal framework to Hamper Market Growth

A critical restraint to the growth of the market is the lack of clear and unified regulatory framework for the operation of the space mining industry. Currently, the Outer Space Treaty of 1967 guides the outer space and prohibits any national appropriation or claiming of celestial bodies but it also does not define commercial property rights. Such ambiguity in the definition brings uncertainty for the companies about the legal ownership of celestial or other bodies. Some nations, such as the U.S., Luxembourg, the United Arab Emirates (UAE), and Japan, have introduced domestic laws recognizing private ownership of space resources, but these rules are not universally accepted. Therefore, lack of a globally accepted legal regime is expected to promote further innovation and expansion of the market.

Segmentation Analysis

By Celestial Body

Proximity to Earth and Abundant Lunar Resources Contributed to Segmental Growth

On the basis of celestial body, the market is classified into asteroids, moon, and mars.

The moon segment is expected to account for the largest space mining share of 61.26% in 2026. The segment growth is attributed to a close proximity to Earth. Therefore, it makes missions more cost-effective and technically feasible compared with asteroids or Mars. Moreover, moon missions provide valuable resources such as water, ice, helium, and other metals that can help in maintaining life-support systems and fuel production necessary for long lasting missions for deep space industries.

- For instance, NASA’s VIPER rover is scheduled to explore the lunar South Pole for water ice to support ISRU. ESA’s ISRU Demonstration Mission aims to produce oxygen from lunar regolith by 2025.

The asteroids segment is the fastest growing segment in the market during the forecast period due to the presence of rare metals and platinum group metals on asteroids which are scarce on Earth. Private companies such as AstroForge and Planetary Resources are actively pursuing asteroid mining missions, which is expected to fuel the segment growth during the forecast period.

- For instance, in February 2025, AstroForge launched its Odin mission to extract precious metals from near-Earth asteroids.

To know how our report can help streamline your business, Speak to Analyst

By Resource Type

Rise in Demand for Water/Ice for Life Support and Propellant Fueled Growth of Segment

In terms of resource type, the market is categorized into metals, water/ice, helium-3, rare earth elements, and others.

The water/ice segment is expected to capture the largest share of 50.92% of the market in 2026. Water acts as a critical resource for supporting human life in space, including drinking, hygiene, and oxygen production. Moreover, the water is split into hydrogen and oxygen to create rocket fuel which further reduces the dependency on fuel transported from Earth for the rocket propulsion.

- Government missions such as NASA’s VIPER rover and ESA’s ISRU Demonstration Mission are focused on locating and harvesting water ice, which is fueling the growth of the segment.

Helium-3 is expected to be the fastest growing segment due to rising demand for alternative clean energy. Helium-3 is a rare isotope with potential applications in clean nuclear fusion, offering a high-energy, low-waste fuel alternative for future energy needs.

- For instance, in May 2025, Seattle-based startup Interlune announced an agreement with the U.S. Department of Energy to deliver helium-3 harvested from the Moon to Earth by 2029. The plan involves extracting three liters of helium-3 from lunar soil using a pilot plant on the Moon

By Technology

Automation and Remote Operations Supplemented Robotic Mining Segment Growth

Based on technology, the market is segmented into robotic mining and ISRU (In-Situ Resource Utilization).

The robotic mining segment is expected to hold the dominating market share of 57.83% in 2026. The segment is growing as the robotic mining is carried out extensively as it can be done in harsh, low-gravity, and high-radiation environments where human presence is risky and costly. Moreover, robotic mining allows precise excavation, sample collection, and material handling without the need for extensive life-support infrastructure.

The ISRU (In-Situ Resource Utilization) segment is anticipated to be the fastest growing segment during the forecast period. The segment is growing as it enables the conversion of mined materials into useful products such as oxygen, water, propellant, and building materials directly on the Moon or other celestial bodies. ESA’s ISRU Demonstration Mission (planned for 2025) will extract oxygen from lunar regolith, while NASA is testing molten regolith electrolysis to produce oxygen and metals on the Moon.

By Application

Strategic Importance of In-Space Fuel Production Propelled Segment Growth

Based on application, the market is segmented into propellant, life support, export to earth, construction material, and others.

The propellant segment is expected to account for the largest space mining market share of 40.81% in 2026. due to rise in demand for in-space fuel production to reduce the need to launch fuel from Earth. There is emphasis on the in-space fuel generation to lower mission costs and promote deeper space exploration.

- For instance, in September 2025, Blue Origin announced the completion of the Critical Design Review of Blue Alchemist, an in-space resource utilization system. In the future, it will extract oxygen from lunar regolith to create propellant-grade oxygen that can refuel spacecraft on the Moon

In 2024, the construction material segment was expected to grow with the fastest CAGR in the market, due to increasing demand for construction materials for establishment of lunar bases and deep-space habitats requiring substantial construction materials. The construction material segment is experiencing rapid growth as space agencies and private companies invest in technologies to produce and utilize local materials.

Space Mining Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and Rest of the World.

NORTH AMERICA

North America dominated the market with a valuation of USD 1.04 billion in 2025 and is projected to reach USD 1.25 billion in 2026. The North America region held the dominant share and is expanding with a significant rate. The market in North America is witnessing growth due to high investments made from both government agencies such as NASA and private companies such as Blue Origin. Countries in the region such as the U.S. have been at the forefront of space exploration and technology development, with numerous missions focused on understanding and utilizing space resources. The United States market is estimated to reach USD 1.13 billion by 2026.

- For instance, NASA's Artemis program, aiming to return humans to the Moon, is expected to significantly boost the demand for in-situ resource utilization (ISRU) technologies and lunar mining operations.

EUROPE

In 2025, the Europe market stood at USD 0.2 billion, representing 13.61% of global demand, and is projected to grow to USD 0.23 billion in 2026. Europe is anticipated to witness a notable growth during the forecast period. The growth is driven by strategic collaborations and infrastructure development. Countries in the Europe region such as Germany, the U.K., and the Netherlands are investing in space exploration initiatives. Such efforts are expected to create strong partnerships between governmental agencies and private enterprises, beneficial for the resource extraction and other technology innovation in the market The United Kingdom market is estimated to reach USD 0.05 billion by 2026, while the Germany market is estimated to reach USD 0.07 billion by 2026.

- For instance, Second Space Resources Challenge (SRC), launched in January 2025 is created to advance technologies for lunar regolith excavation and processing.

ASIA PACIFIC

The Asia Pacific region captured 10.65% of the global market in 2025, generating USD 0.15 billion in revenue, and is projected to reach USD 0.19 billion in 2026. The Asia Pacific region is witnessing steady growth in the market. The market is due to space programs and exploration missions by various countries such as China, Japan, and India. The space exploration programs launched by China, including lunar missions and asteroid mining projects, are propelling the market growth in the region. The Japan market is estimated to reach USD 0.02 billion by 2026, the China market is estimated to reach USD 0.08 billion by 2026, and the India market is estimated to reach USD 0.02 billion by 2026.

For instance, in February 2025, China launched Chang'e-7 mission, aimed at exploring lunar resources which is expected to enhance the country's capabilities in space mining.

REST OF THE WORLD

In 2025, Rest of the World represented USD 0.05 billion, accounting for 3.49% of the worldwide market, and is projected to grow to USD 0.06 billion in 2026. During the forecast period, the Rest of the World which includes Latin America and Middle East & Africa regions would witness a moderate growth in this market space. Countries in the Middle East, such as the United Arab Emirates, are investing in space exploration to diversify their economies.

- For instance, in March 2025, The UAE Space Agency successfully completed the Critical Design Review for its Emirates Mission to the Asteroid Belt (EMA).

Such developments and achievement strengthens the country’s capability in asteroid exploration, for potential future space mining initiatives in the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Missions, Technological Innovation, and Public-Private Collaborations Supports Market Expansion of Key Players

The global space mining market is influenced by a rise in investments in deep-space exploration, asteroid and lunar resource prospecting. The market is also driven by growing interest of governments and private companies in in-situ resource utilization (ISRU). Key players in this market include NASA (via Artemis program), ESA, Blue Origin, Planetary Resources, AstroForge, and Interlune, each company contributing through the spacecraft design, development of autonomous mining robots, and cost effective resource extraction technologies.

Companies are providing a wide range of solutions such as robotic prospecting systems, lunar and asteroid landers, ISRU modules, and resource processing technologies for extracting water, metals, helium-3, and rare earth elements. Moreover, for market expansion, these key companies are increasingly investing heavily in the design of advanced robotics, AI-based autonomous systems, in-orbit refining, and other technologies. In addition, government space agencies and private space exploration companies are rapidly partnering on strategic missions to expand operational capabilities and reduce cost and risks involved in space resource extraction.

LIST OF KEY SPACE MINING COMPANIES PROFILED:

- NASA (U.S.)

- ESA (France)

- Blue Origin (U.S.)

- Planetary Resources (U.S.)

- AstroForge (U.S.)

- Interlune (U.S.)

- SpaceFab.US, Inc (U.S.)

- Trans Astronautica Corporation (U.S.)

- iSpace (Japan)

- Moon Express (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- April 2025: Blue Origin’s Blue Alchemist system completed its Critical Design Review, advancing plans to turn lunar regolith into oxygen, metals, and solar arrays for future propellant production.

- March 2025: Startup AstroForge confirmed its Vestri asteroid-mining probe and will launch with Intuitive Machines’ IM-3 mission, aiming to sample a metallic near-Earth asteroid in late 2025.

- February 2025: NASA announced the PRIME-1 payload on Intuitive Machines’ IM-2 mission will drill for water ice and analyze lunar soil to test resource extraction for oxygen and fuel.

- December 2024: Japan’s ispace partnered with Magna Petra to explore extracting helium-3 from lunar regolith for clean-energy applications on Earth.

- October 2025: Fleet Space Technologies secured USD 150 million to scale satellite and AI tools for mineral prospecting, including future lunar resource mapping.

REPORT COVERAGE

The global space mining market demand analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics, and market trends expected to drive the market during the forecast period. The market analysis includes porters five forces analysis which illustrates the potency of buyers suppliers in the market. The market forecast offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The space mining market report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.34% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Celestial Body, By Resource Type, By Technology, By Application, and Region |

| By Celestial Body |

|

| By Resource Type |

|

| By Technology |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.44 billion in 2025 and is projected to reach USD 4.07 billion by 2034.

In 2025, the market value stood at USD 1.04 billion.

The market is expected to exhibit a CAGR of 11.34% during the forecast period of 2026-2034.

The moon segment led the market by celestial body.

The key factors driving the market are growth of market are rise in demand for critical metals and rare minerals.

NASA (U.S.), ESA (Europe), Blue Origin (U.S.), AstroForge (U.S.) and others are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us