Space Semiconductor Market Size, Share & Industry Analysis, By Application (Satellite, Launch Vehicles, Deep Space Probe, Rovers and Landers, and Others), By Type (Radiation Hardened Grade, Radiation Tolerant Grade, and Others), By Component (Integrated Circuits, Discrete Semiconductors Devices, Optical Devices, Microprocessor, Memory, Sensors, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

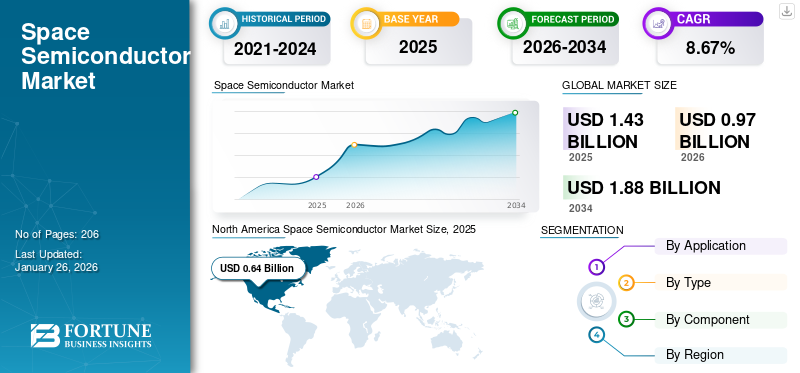

The space semiconductor market size was valued at USD 1.43 billion in 2025. The market is projected to grow from USD 0.97 billion in 2026 to USD 1.88 billion by 2034, exhibiting a CAGR of 8.67% during the forecast period. North America dominated the semiconductor market with a 44.06% market share in 2025.

Space semiconductors are electronic components that are specifically designed, manufactured, and qualified to operate reliably in the harsh and demanding environment of space. The conditions in space present numerous challenges for electronic components, including extreme temperatures, radiation, vacuum, and microgravity. Silicon and alternatives, such as Gallium Arsenide (GaAs) are primary semiconductor materials, while Silicon Carbide (SiC) is valued for its thermal and electrical properties. Space semiconductors are engineered to withstand these conditions and provide robust and reliable performance for space missions.

Space semiconductors are typically used in satellites, spacecraft, and other space electronics applications and are more expensive than regular semiconductors. However, they are much more reliable when it comes to operating in extreme environments and conditions. The growing constellation of satellites is expected to drive satellite manufacturing which, in turn, will propel the growth of the market size from 2024 to 2032.

Border closures, lockdowns, and restrictions on movement due to the COVID-19 pandemic had adversely impacted the timely delivery of components, which led to delays in manufacturing. As per the Semiconductor Industry Association, the global semiconductor industry experienced challenges in meeting the soaring demand for chips, primarily due to the prolonged COVID-19-related shutdown of manufacturing facilities. This anomaly significantly affected global businesses, resulting in an increased need for advanced chips across various consumer sectors.

Research and development activities related to the innovation and improvement of semiconductor technologies were hampered due to restrictions on physical presence in laboratories and disruptions in collaborative efforts.

Download Free sample to learn more about this report.

Space Semiconductor Market Key Takeaways

- 2025 Market Size: USD 1.43 billion

- 2026 Market Size: USD 0.97 billion

- 2034 Forecast Market Size: USD 1.88 billion

- CAGR: 8.67% from 2026–2034

- North America dominated the space semiconductor market with a 44.06% share in 2025.

- The satellite segment held a 79.13% market share in 2026.

- The radiation hardened segment accounted for a 55.69% market share in 2026.

North America

North America held 44.06% of the global market, valued at USD 0.64 billion in 2025.

Asia Pacific

Accounted for 26.45% of the global market, reaching USD 0.38 billion in 2025

Europe

Europe captured 19.05% of the global market, valued at USD 0.27 billion in 2025.

U.S

The U.S. space semiconductor market is projected to reach USD 0.39 billion by 2026.

Japan

The Japan space semiconductor market is projected to reach USD 0.02 billion by 2026.

Read More

SPACE SEMICONDUCTOR MARKET TRENDS

Use of System-on-Chip (SoC), Artificial Intelligence (AI), and Machine Learning (ML) Algorithms are Key Market Trends

A system-on-chip is a type of Integrated Circuit (IC) design that combines many or all of the high-level functional elements of an electronic device on a single chip, rather than using separate components mounted on a motherboard as is the case in a traditional electronics design. A traditional motherboard-based computer or electronic device contains separate components, such as a Central Processing Unit (CPU), Graphics Processing Unit (GPU), modem, dedicated signal processor, peripherals, primary & secondary storage, and more. Each component functions as a separate component. An SoC, on the other hand, incorporates these functions into a single microchip.

In October 2023, Coherent Logix Inc. announced the launch of HyperX: Midnight, a fourth generation HyperX SoC for space and defense industries. HyperX: Midnight delivers up to 4x more computing throughput at half the power and 40% lower price than leading radiation-hardened FPGAs. This powerful, low SWaP (size, weight, power) combination is critical for Space 2.0 companies, allowing much greater capacity to be accommodated with smaller satellite bus sizes, thereby significantly reducing launch costs. Moreover, quantum technology, AI & ML algorithms, private & public entities’ partnerships, collaborations, product innovations, and government initiatives are key trends in the market.

Download Free sample to learn more about this report.

SPACE SEMICONDUCTOR MARKET GROWTH FACTORS

Surge in Satellite Constellations to Boost Global Space Semiconductor Market Growth

Surge in the deployment of satellite constellations serving diverse purposes, such as Earth observation, communication, and navigation is driving the demand for space-grade semiconductors. These constellations necessitate the use of advanced electronics to guarantee consistent and reliable operation within the challenging space environment. A satellite constellation, also known as a swarm, constitutes a network of identical or similar artificial entities pursuing a common objective and under the control of the same entity. These groups communicate with ground stations globally and are occasionally interconnected, operating as a cohesive system designed to complement one another.

With numerous satellite constellations currently orbiting the Earth, the planet is poised to witness a substantial increase in satellite launches over the next few years. For instance, in September 2022, the U.S. Government Accountability Office (U.S. GAO), an independent, nonpartisan government agency providing services for the U.S. Congress, reported a significant rise in the number of active satellites. The count steadily increased over the past few years, surging from 1,400 in 2015 to 5,500 by the spring of 2022.

This upward trajectory is expected to continue, with the U.S. GAO anticipating a further escalation in this trend. According to the government agency’s projections, 58,000 new satellites are forecasted to be launched by the end of the decade, more than doubling the current number of operational spacecraft. The increase in the number of satellites is expected to propel the demand of space semiconductors.

Download Free sample to learn more about this report.

Technological Advancements in Semiconductor Manufacturing and Processing Techniques to Propel Market Growth

Technological advancements and innovations in semiconductor manufacturing, processing, and packaging are vital in this market. Major players in this market are focusing on developing technologically advanced semiconductors to sustain the conditions of space environment and improve their reliability and efficiency. Gallium oxide exhibits the capacity to support high currents and voltages with minimal energy losses and can be easily turned into high-quality films using cost-effective techniques. As a semiconductor, gallium oxide, while typically is a poor electrical conductor, can effectively carry electric currents with the addition of specific impurities. Its advantages over silicon, the semiconductor prevalent in most computer chips, are manifold.

Electronic devices based on gallium oxide have emerged as a prominent choice for operation in challenging environments, particularly in space exploration, owing to their ability to endure high temperatures and radiation without significant degradation. Facing hazards, such as exposure to radiation and extreme temperature fluctuations, space probes encounter numerous challenges. To overcome such challenges, in August 2023, researchers at KAUST (King Abdullah University of Science and Technology) developed the world's first flash memory device using gallium oxide, showcasing superior resilience to extreme temperatures compared to traditional electronics.

RESTRAINING FACTORS

Supply Chain Disruptions and Geopolitical Tensions to Hinder Market Growth

Supply chain disruptions, stemming from factors, such as raw material shortages, transportation issues, and geopolitical instabilities, pose a significant threat to the smooth operation of the space semiconductor market growth. These disruptions can result in delays, increased costs, and hampered production efficiency, impacting the sales of space semiconductors.

For instance, in September 2022, Philippine Long Distance Telephone Company (PLDT Inc.) announced that one of the major challenges faced by Low Earth Orbit (LEO) satellite manufacturers is the delayed delivery of essential chips required for the production of space-based equipment. The persistent shortage of semiconductor chips, affecting manufacturers globally, could potentially impact producers of LEO satellites, which are crucial for telecommunications services. This chip scarcity is a major issue for semiconductor manufacturers worldwide due to geopolitical tensions affecting both production and the shipment of goods.

Additionally, geopolitical tensions further compound the challenges faced by the space semiconductor sector. Strained international relations and trade conflicts can lead to restrictions on the movement of critical components and technologies essential for manufacturing space semiconductors. This not only hinders the pace of innovation, but also raises concerns about the reliability and accessibility of crucial components required for space applications.

SPACE SEMICONDUCTOR MARKET SEGMENTATION ANALYSIS

By Application Analysis

Rising Demand for Satellite Communication and Navigation Services Boosted Product Adoption

By application, the market is classified into satellite, launch vehicles, deep space probe, rovers and landers, others.

The satellite segment is the dominated the global space semiconductor market with a share of 79.13% in 2026 and is estimated to grow significantly during forecast period due to the growing demand for satellite communication and navigation services. Semiconductors are designed for use in artificial satellites orbiting the Earth. These are crucial for satellite communication, earth observation, navigation, and scientific research.

The launch vehicle segment is estimated to be the fastest growing segment during the forecast period due to the increasing demand for advanced and compact semiconductors. This segment encompasses semiconductors that are used in the electronic systems of launch vehicles, such as rockets and space shuttles. These semiconductors play a vital role in navigation, control, and communication during the launch phase.

To know how our report can help streamline your business, Speak to Analyst

By Type Analysis

Radiation Hardened Semiconductors Gained Major Traction Owing to Growing Demand for Semiconductors that Withstand Harsh Environment

By type, the market is segregated into radiation hardened grade, radiation tolerant grade, and others.

The radiation hardened segment dominated the market with a share of 55.69% in 2026 and is estimated to be the fastest growing segment due to the rising demand for semiconductors that can withstand space radiation environment. Radiation hardened semiconductors are specifically designed to withstand the harsh radiation environment present in space. These components are hardened to resist damage from ionizing radiation, ensuring their reliability and longevity in space missions.

The radiation tolerant segment is expected to grow significantly due to the increasing demand for low cost and precise semiconductors. Radiation tolerant semiconductors are designed to endure certain levels of radiation without complete hardening. While they are not as robust as radiation-hardened components, they offer a balance between performance and cost-effectiveness for missions with lower radiation exposure.

By Component Analysis

Integrated Circuits Becomes Popular Due to Growing Demand for Multi-Functional Semiconductors

By component, the market is segmented into integrated circuits, discrete semiconductors devices, optical devices, microprocessor, memory, sensors, and others.

The integrated circuit segment is the dominating one with a share of 28.85% in 2026 and is estimated to grow significantly during the forecast timeline due to the growing demand for multi-functional semiconductors. Integrated Circuits (ICs) consist of numerous electronic components, such as transistors, resistors, and capacitors, which are fabricated on a single semiconductor substrate. ICs play a pivotal role in space applications, serving functions, such as data processing, amplification, and control within a compact and efficient package.

REGIONAL INSIGHTS

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and Rest of the World.

North America Space Semiconductor Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, North America held 44.06% of the global market share, reaching a valuation of USD 0.64 billion, and is projected to grow to USD 0.43 billion in 2026. This growth is attributed to the presence of major OEMs and operators in this region. For instance, in August 2022, Microchip Technology secured a major agreement with the U.S. government through the CHIPS and Science Act, aiming to strengthen the local chip industry in the face of competition from China. As a strategic move to enhance its domestic semiconductor sector, the U.S. government disclosed plans to allocate approximately USD 162 million in funding to a specific company within the industry. The official announcement was made by the U.S. Department of Commerce.The U.S. market is projected to reach USD 0.39 billion by 2026.

Europe

The market in Europe reached USD 0.27 billion in 2025, representing 19.05% of total market revenue, and is projected to reach USD 0.18 billion in 2026. Europe captured the second-largest market share in the base year. This market’s growth is due to the growing space-based applications of semiconductors, coupled with increasing investments. In February 2023, Infineon Technologies AG began the construction of a new factory for analog/mixed-signal technology and power semiconductors. After a comprehensive analysis, Infineon's Board of Directors and the supervisory authority granted permission for the factory to be located in Dresden. The Federal Ministry for Economic Affairs and Climate Protection (BMWK) agreed to an early start on the project so that construction can begin before the financial review by the European Commission is completed.The UK market is projected to reach USD 0.07 billion by 2026, while the Germany market is projected to reach USD 0.01 billion by 2026.

Asia Pacific

Asia Pacific contributed approximately USD 0.38 billion to the global market in 2025, accounting for 26.45% share, and is expected to reach USD 0.26 billion in 2026. Asia Pacific is expected to be the fastest growing region during the forecast period. It held a significant share in the base year. The market’s growth in this region is due to the strong economic development of emerging countries. For instance, in 2022, executives from global companies such as AMD, Micron Technology, Applied Materials, and Foxconn pledged to invest in India's semiconductor ecosystem. While AMD announced a USD 400 million investment in India over five years and the opening of the world's largest R&D campus of 500,000 square meters in Bangalore, Micron is building the country's first semiconductor factory in Gujarat.The Japan market is projected to reach USD 0.02 billion by 2026, the China market is projected to reach USD 0.15 billion by 2026, and the India market is projected to reach USD 0.05 billion by 2026.

Rest of the World

The Rest of the World market accounted for USD 0.14 billion in 2025, representing 9.90% of the global industry, and is expected to reach USD 0.1 billion in 2026. Rest of the world including the Middle East & Africa and Latin America are also expected to grow significantly during the forecast period. The growth is attributed to increasing government initiatives for space-based technologies.

LIST OF KEY COMPANIES IN SPACE SEMICONDUCTOR MARKET

Technological Advancements, Product Innovations, and Expansion into Emerging Markets are Key Focus Areas of Leading Players

This market is consolidated with key players, such as Advanced Micro Devices, Inc., Infineon Technologies AG, Microchip Technology Incorporated, Texas Instruments Incorporated, STMicroelectronics N.V., and others. These companies are focusing on technological advancements, product innovations, and entry into emerging markets to increase their market share. For instance, in April 2022, Infineon Technologies LLC, a division of Infineon Technologies AG, unveiled the pioneering radiation-hardened (rad-hard) Ferroelectric RAM (F-RAM) with a serial interface designed for the space industry's extreme environments. These novel devices claim to offer unparalleled reliability and data retention, surpassing the performance of non-volatile EEPROM and serial NOR Flash devices in terms of energy efficiency for space applications.

LIST OF KEY COMPANIES PROFILED:

- Advanced Micro Devices, Inc. (U.S.)

- Infineon Technologies AG (Germany)

- Microchip Technology Incorporated (U.S.)

- Texas Instruments Incorporated (U.S.)

- STMicroelectronics N.V. (Switzerland)

- Renesas Electronics Corporation (Japan)

- Cobham Limited (U.K.)

- Solitron Devices, Inc. (U.S.)

- BAE Systems Plc (U.K.)

- Teledyne Technologies Incorporated (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- March 2023 - SEEQC, a quantum computer startup based in New York, revealed the successful development of a digital chip designed to function at temperatures colder than the outer space. This innovation makes it compatible with quantum processors commonly housed in cryogenic chambers. Two additional chips currently in the development phase are anticipated to operate in a slightly warmer region within the cryogenic chamber.

- February 2023 - Lux Semiconductors secured USD 2.3 million in funds to advance the development and commercialization of its innovative "System-on-Foil" process aimed at enhancing the performance of microelectronics. Lux Semiconductors' System-on-Foil technology is specifically crafted to decrease the size and enhance the performance of microelectronics to cater to applications in spacecraft, aircraft, and various other domains.

- November 2022 - Texas Instruments (TI) unveiled an expansion in its range of space-grade analog semiconductors and its related products housed in exceptionally reliable plastic packages designed for a diverse array of missions. Introducing a novel device screening specification named Space High-Grade (SHP) in plastic for radiation-hardened products, TI also presented new Analog-to-Digital Converters (ADCs) aligning with the SHP qualification.

- August 2022 - Microchip Technology (MCHP) has secured a USD 50 million federal contract grant to develop the next-generation processor for spaceflight computing. Chosen by NASA's Jet Propulsion Laboratory for a three-year project, Microchip will spearhead the design of a high-performance spaceflight computing (HPSC) system. This innovative HPSC is anticipated to offer computing capabilities that are 100 times more powerful than current systems.

- March 2022 - STMicroelectronics launched a series of radiation-hardened power, analog, and logic ICs, housed in low-cost plastic packages and playing crucial roles in the electronic circuitry of satellites. The initial nine devices in this series include a data converter, a voltage regulator, an LVDS transceiver, a line driver, and five logic gates utilized in various systems, such as power generation & distribution, on-board computers, telemetry star trackers, and transceivers. ST plans to enhance the series by incorporating additional functionalities in the coming months, providing designers with a broader range of choices.

REPORT COVERAGE

The report provides a detailed market analysis. It comprises all major aspects, such as R&D capabilities and optimization of the operating services. Moreover, it offers insights into the market’s share, trends, regional analysis, porter’s five forces analysis, and competitive landscape of various companies profiled with market competition. It also highlights key industry developments. In addition to the above-mentioned factors, the report focuses on several other factors that have contributed to the market’s growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.67% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Application

|

|

By Type

|

|

|

By Component

|

|

|

By Geography

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 1.43 billion in 2025.

The market is likely to display a CAGR of 8.67% over the forecast period of 2026-2034.

The satellite segment led the market owing to the rising demand for satellite communication and navigation services.

The market value in North America stood at USD 0.64 Billion in 2025.

Surge in satellite constellations and technological advancements in space semiconductor manufacturing and processing techniques are expected to drive the market.

Some of the top players in the market are Advanced Micro Devices, Inc., Infineon Technologies AG, Microchip Technology Incorporated, Texas Instruments Incorporated, STMicroelectronics N.V. and others.

The U.S. dominated the market in 2025.

Supply chain disruptions and geopolitical tensions are expected to hamper the market’s growth.

- 2021-2034

- 2025

- 2021-2024

- 206

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us