Steel Slag Market Size, Share & Industry Analysis, By Type (BF-BOF Slag and Steelmaking Slag), By Application (Construction, Cement & Concrete, Fertilizers, and Others), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

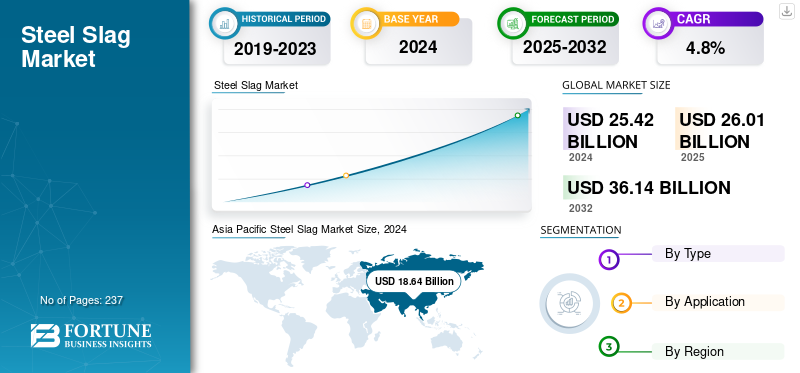

Steel Slag Market Size and Future Outlook

The global steel slag market size was valued at USD 26.32 billion in 2025. The market is projected to grow from USD 27.53 billion in 2026 to USD 39.79 billion by 2034, exhibiting a CAGR of 4.7% during the forecast period. Asia Pacific dominated the steel slag market with a market share of 73.32% in 2025.

Steel slag is a byproduct of steel production, formed when impurities in the raw materials react with oxidants and fluxes in the steelmaking process. It consists of various minerals and can be used as a construction material due to its high hardness, durability, and ability to improve concrete properties. The rising steel production has increased slag supply, aiding market growth. It is used in cement manufacturing, which yields high strength and low heat generation when mixed with water. It has strong chemical resilience. These characteristics make it an optimal option for the cement and construction industries. However, the market growth has been hampered by harmful ingredients in slag. Toxic additives such as nickel, chromium, strontium, and cadmium are often found in slag. These compounds can be hazardous to the environment and human health.

Furthermore, the market encompasses several key players with ArcelorMittal, Nippon Steel Corporation, and JFE Steel Corporation at the forefront. A broad portfolio, innovative product launches, and strong geographical expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

STEEL SLAG MARKET TRENDS

Circular Economy and Decarbonization are the Emerging Market Trends

As construction owners pursue lower-carbon materials, steel slag is transitioning from a waste product to a sustainable resource, serving as both high-performance aggregate and, following accelerated carbonation, a supplementary cementitious material (SCM). The utilization of Electric Arc Furnace (EAF)/Basic Oxygen Furnace (BOF) slag as aggregate can significantly reduce embodied environmental impacts by circumventing energy-intensive quarrying processes.

- Recent Life Cycle Assessment (LCA) studies on a mid-rise building have demonstrated that substituting natural coarse aggregate with steel slag aggregate resulted in a reduction of approximately 69 tons of CO₂ emissions, while still satisfying structural performance requirements.

Overall, the growing acceptance of standards, proven environmental benefits from LCAs, and the development of CO₂-mineralized steel-slag SCMs are driving a strong market shift toward using slag-based materials to cut carbon emissions and promote circular use of industrial byproducts.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand in Road Construction to Drive Market Growth

Road construction is a vital sector that significantly influences the steel slag market growth, given its extensive application in the building of highways and roads. The slag is preferred in this sector due to its remarkable characteristics, making it an essential material for modern infrastructure. One of the standout properties of the product is its exceptional load-bearing capacity, which makes it highly suitable for use as aggregate in road bases and sub-bases. The robust and resilient nature of slag aggregates ensures that they can withstand heavy traffic loads, contributing to the longevity and durability of roadways.

Furthermore, its unique intrinsic properties, such as its weather resistance and high alkalinity, play a critical role in minimizing the leaching of harmful substances into the environment. These features align well with the growing emphasis on environmentally friendly construction practices, reinforcing the case for steel slag in road building. Government regulations and standards that advocate for sustainable infrastructure practices have increasingly favored the incorporation of slag into road construction projects. Several countries have recognized the numerous benefits associated with this material and have included guidelines in their regulatory frameworks to promote its use.

MARKET RESTRAINTS

Steel Slag Management and Disposal May Affect Market Growth

Environmental constraints often serve as the primary barrier in the market. Steel slag, a by-product of steel manufacturing, contains various chemical compounds that can harm the environment if not properly managed. Consequently, governments and regulatory agencies have imposed strict regulations for the safe handling, treatment and disposal of slag generated from steel manufacturing.

One of the key challenges is the need for appropriate disposal methods. It is commonly used as aggregate in road construction, cement, and concrete production. However, usage restrictions vary by region or country, with some areas banning its use due to regulatory concerns. For example, certain regions require special treatment of the slag to prevent toxin leaching into the environment, increasing both costs and the complexity of its application in construction.

Environmental laws also focus on limiting the emission of pollutants from the slag, which may contain heavy metals and other hazardous substances. To address these issues, manufacturers have invested in advanced technologies such as solidification/stabilization, washing, and leaching methods.

MARKET OPPORTUNITIES

Water Treatment and Land Reclamation to Increase Product Consumption

The market offers promising opportunities for land reclamation and water treatment. Steel slag's unique properties make it well-suited for these uses. Its high adsorption capacity makes it effective in cleaning contaminated water as its large surface area and porosity enable it to absorb elements such as phosphate, silica, magnesium, iron, aluminum, and calcium from sewage. This makes the slag valuable for industrial effluent and wastewater treatment. It can serve as filter media in artificial wetlands, where microorganisms use it as a substrate to break down organic materials and remove pollutants biologically and chemically.

Overall, the market is driven by the demand for sustainable, cost effective solutions, creating potential in water treatment and land reclamation. By leveraging its adsorption and soil-improving properties, industries and governments can address environmental concerns, increase resource efficiency, and promote sustainable development.

MARKET CHALLENGES

Heterogeneity and Quality Control Challenges to Hamper Market Growth

The chemistry and phase composition of steel slag exhibit significant variability depending on the type of furnace, operational practices, and the nature of the scrap or feedstock used. This variability renders performance unpredictable without meticulous processing and quality control measures. The regular sampling and analysis of slag are standard procedures in EAF facilities to monitor key oxides within the CaO-MgO-FeO-SiO₂ system and to maintain MgO/CaO ratios within safe parameters. However, these procedures incur additional testing costs and introduce variability risks. Elevated levels of free lime (f-CaO) and free MgO can lead to detrimental expansion after placement. Consequently, producers are required to crush, screen, and subsequently weather or age stockpiles. In the U.K., many operations retain windrows for a minimum of approximately three months and only release material following successful expansion tests in accordance with EN 1744-1, which may result in reduced throughput.

- Slag also contains entrained metallic iron, often approximately 10 to 40 weight percent, which must be removed through magnetic separation to satisfy aggregate specifications, thereby introducing an additional quality control step.

Segmentation Analysis

By Type

Bf-BOF Slag Segment Dominated the Market Owing to High Usage in Civil Engineering Applications

Based on type, the market is segmented into BF-BOF slag and steelmaking slag.

The BF-BOF slag segment accounted for a major steel slag market share in 2025, as the integrated BF-BOF route remained the predominant method of steel production worldwide, notably in China, Japan, South Korea, Germany, Brazil, and other major steel-producing nations. This segment benefited from substantial, consistent slag generation with converter-based crude steel production. BF-BOF slag is predominantly used in civil engineering applications, including road construction, concrete aggregates, embankments, and asphalt mixtures owing to its hardness, durability, and suitability as a substitute for natural aggregates. Nonetheless, the growth of this segment was moderate relative to EAF-based slag, given that BF-BOF steelmaking is an established industrial process and faces long-term challenges from decarbonization initiatives and the gradual transition to scrap-based and DRI-EAF steelmaking methods. Furthermore, this segment is projected to exhibit a CAGR of 4.6% throughout the analysis period.

The steelmaking slag segment, encompassing EAF slag, ladle slag, induction furnace slag, AOD/VOD slag, and other secondary refining slags, showed the fastest growth. This growth was facilitated by increased EAF steel production, higher scrap utilization, the expansion of DRI-EAF routes in regions such as the Middle East, India, Europe, and North America, and greater use of secondary steelmaking by-products. EAF and refining slags are progressively being employed in construction aggregates, road base materials, cementitious compounds, soil stabilization, and metallurgical recycling applications. Moreover, it is anticipated that this segment will experience a CAGR of 4.8% over the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Cement & Concrete Segment to Grow at the Fastest CAGR Owing to Rising Demand in the Construction Sector

Based on application, the market is segmented into construction, cement & concrete, fertilizers, and others.

The cement & concrete segment is anticipated to experience the fastest growth over the analysis period. The increasing demand for these products in the building materials industry, owing to their properties such as high tensile strength, water resistance, hardness, and chemical compatibility with a range of materials, is driving segment growth. Furthermore, this segment is projected to grow at a CAGR of 5.3% over the analysis period.

The construction segment dominates the market and the demand is primarily driven by the rising use of steel slag in the construction industry for soil stabilization and in mortar for masonry. As quarry permitting becomes increasingly stringent and extraction costs escalate, processed slag offers a more cost-effective solution on a per-functional-performance basis, thereby improving bid competitiveness for public projects and accelerating its adoption. Furthermore, the segment is projected to grow at a CAGR of 4.7% over the forecast period.

Steel Slag Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Asia Pacific

Asia Pacific Steel Slag Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region held the largest market share with a value of USD 18.64 billion and maintained its leadership in 2025, recording a market value of USD 19.30 billion. The Asia Pacific is home to several developing economies, including major contributors such as China and India. These countries have a significant untapped economic growth potential likely to be realized during the forecast period as they progress in their economic expansion, growing urbanization, and a boost in construction activities to support the product demand in the region.

China Steel Slag Market

By 2026, the China market is projected to attain a valuation of USD 14.52 billion. China is the largest consumer and producer of slag within the Asia Pacific region. The dominance can be attributed to China producing substantial slag as it is the world’s largest steel producer. The utilization of slag in the country is a well-established market, particularly in the cement and concrete markets. It is frequently used in China as an additional cementitious material, which helps make slag cement. It is used for various purposes, including stabilizing and building roads.

To know how our report can help streamline your business, Speak to Analyst

Japan Steel Slag Market

The Japan market is estimated to be around USD 1.24 billion in 2026, accounting for roughly 4.5% of the global revenues.

India Steel Slag Market

The India market is estimated at around USD 2.18 billion in 2026, accounting for roughly 7.9% of the global revenues.

Europe

The Europe market is expected to experience substantial growth in the coming years. Over the forecast period, the region is projected to grow at a CAGR of 4.3%, reaching a market valuation of USD 3.72 billion by 2026. In Europe, the high demand for the product is associated with the rapid growth in infrastructure and industrial developments. The largely produced slag is utilized in road construction projects. Likewise, the electric arc furnace slag has high stability, durability, and frictional properties, making it suitable for ballast for asphalt development in the entire value chain.

U.K. Steel Slag Market

The U.K. market is estimated to touch around USD 0.06 billion in 2026, accounting for roughly 0.2% of global revenues.

Germany Steel Slag Market

The Germany market is estimated at around USD 0.83 billion in 2026, accounting for roughly 3.0% of global revenues.

North America

In North America, the U.S. and Canada are the leading contributors. The rapid expansion of the cement and concrete industries has fueled the regional market growth. In the U.S., the construction sector contributes 4% of GDP and the demand for construction products is increasing in both the residential and commercial sectors. Thus, it creates a domestic boost in slag demand from major end-use industries, driving the market in the region.

U.S. Steel Slag Market

Given the U.S. dominance in the region, the U.S. market is estimated to touch around USD 1.20 billion in 2026, accounting for roughly 4.4% of global sales.

Latin America and the Middle East & Africa

Latin America is one of the swiftly advancing regions in terms of urbanization and technological advancement. Significant steel manufacturers, such as Bekaert and ArcelorMittal, are expected to drive product growth in the region. Brazil remained the primary contributor, owing to its integrated steelmaking infrastructure. Meanwhile, Mexico demonstrated greater growth potential owing to its EAF-based steel production and its connection with North American construction and manufacturing demand. In the Middle East & Africa, the GCC countries and other Middle Eastern producers demonstrated rising demand, driven by the expansion of DRI-EAF steel production, infrastructure development, and greater utilization of slag in construction applications. However, in various developing markets, growth was constrained by limited slag-processing capacity, inconsistent regulatory acceptance, logistical challenges, and low adoption of value-added slag applications. The Latin America market is projected to reach USD 0.79 billion by 2026.

GCC Steel Slag Market

The GCC market is estimated to reach USD 0.26 billion in 2026, accounting for approximately 0.9% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Steel Producers to Strengthen Slag Valorization to Capture Value from Construction Demand

The global market remained moderately consolidated at the production level, as slag availability was closely linked to crude steel output from leading steel producers. Companies such as ArcelorMittal, NIPPON STEEL CORPORATION, POSCO, Tata Steel, JFE Steel, Kobe Steel, United States Steel Corporation, and voestalpine AG held strong positions due to their large BF–BOF and EAF steelmaking operations. These companies generated substantial volumes of converter slag, EAF slag, ladle slag, and other steelmaking by-products, thereby supporting their role as primary suppliers to slag processors, aggregate producers, cement companies, road contractors, and infrastructure developers.

The market competition was primarily influenced by regional factors such as availability, processing capacity, product quality, logistical reach, and end-use certification, rather than by the global slag trade. Given that steel slag is a dense, low-value bulk material, suppliers located near infrastructure projects such as road construction, cement manufacturing, aggregate markets, and industrial clusters held a distinct competitive advantage. Companies with pre-established systems for slag aging, metal recovery, crushing, screening, leaching control, and grading were better equipped to supply certified slag products for use in construction, road base, asphalt, cement, and concrete, as well as soil improvement applications.

Major steelmakers are increasingly prioritizing by-product valorization and circular-economy strategies to enhance slag utilization and reduce dependence on landfills. Established markets such as Japan, Europe, the U.S., and China exhibit high rates of slag utilization, thereby encouraging producers to move beyond basic disposal methods and develop higher-value applications. Specifically, collaborations with cement producers, construction material companies, and road infrastructure agencies have become essential for advancing the commercialization of slag-based products. Consequently, competitive advantage is driven by the ability to transform steel slag from a low-value by-product into a certified recycled material with consistent quality and dependable end-use performance.

LIST OF KEY STEEL SLAG COMPANIES PROFILED

- ArcelorMittal (Luxembourg)

- Nippon Steel Corporation (Japan)

- United States Steel Corporation (U.S.)

- JFE Steel Corporation (Japan)

- Tata Steel (India)

- POSCO (South Korea)

- Voestalpine Group (Austria)

- thyssenkrupp Steel Europe (Germany)

- Optimus Steel (U.S.)

- KOBE STEEL, LTD. (Japan)

KEY INDUSTRY DEVELOPMENTS

- July 2025: ArcelorMittal Nippon Steel India (AM/NS India) received the first license for a new "steel slag valorization" technology developed by India's Central Road Research Institute (CSIR-CRRI). The technology allows the company to process this slag into aggregates for road construction at its flagship Hazira plant in Gujarat.

- February 2023: Nippon Steel Corporation announced its agreement with Elk Valley Resources Ltd. (EVR) to indirectly acquire up to 10% of common shares, preferred shares, and royalty interest in the latter.

- July 2022: thyssenkrupp Steel announced plans to work with BP p.l.c. The purpose of the strategic collaboration is to decarbonize steel production, as thyssenkrupp Steel accounts for 2.5% of Germany's CO2 emissions. The company and BP p.l.c. are planning to replace the coal-fired blast furnaces to produce green steel and products.

- March 2022: ArcelorMittal acquired Scottish recycling business John Lawrie Metals Ltd., as part of the company’s strategy of increasing the usage of scrap steel to reduce carbon dioxide emissions from steelmaking.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market shares and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.7% from 2026-2034 |

| Unit | Value (USD Billion) and Volume (Kiloton) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 26.32 billion in 2025 and is projected to reach USD 39.79 billion by 2034.

The market is slated to exhibit steady growth at a CAGR of 4.7% during the forecast period of 2026-2034.

The construction application segment dominates the market.

The construction application segment dominates the market.

The continuous growth in the construction industry is a key factor driving the market.

- 2021-2034

- 2024

- 2021-2024

- 240

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us