Structural Heart Devices Market Size, Share & Industry Analysis By Product (Instruments [Heart Value Devices, Occlusion & Closure Devices and Others] and Accessories), By Procedure Type (Valve Replacement Procedures [Transcatheter Aortic Valve Replacement, Transcatheter Mitral Valve Replacement, and Others], Repair Procedures [Mitral Edge-to-Edge Repair, Tricuspid Edge-to-Edge Repair, and Others], Structural Heart Closure Procedures [Atrial Septal Defect Closure, Ventricular Septal Defect Closure, and Others]), By Indication, By End User, and Regional Forecast, 2026-2034

Structural Heart Devices Market Size and Future Outlook

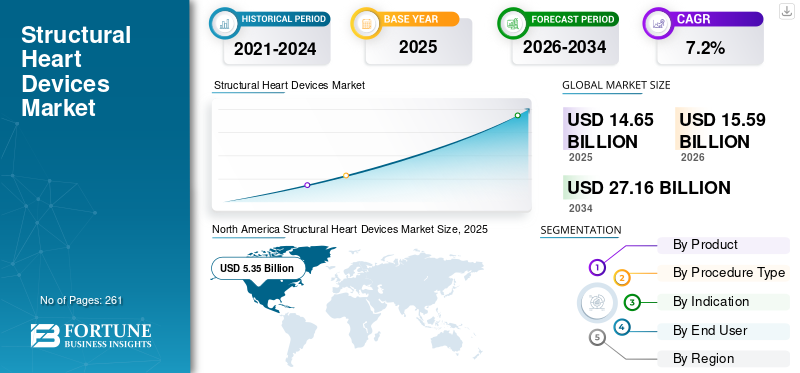

The global structural heart devices market size was valued at USD 14.65 billion in 2025 and is projected to grow from USD 15.59 billion in 2026 to USD 27.16 billion by 2034, exhibiting a CAGR of 7.2% during the forecast period. North America dominated the global structural heart devices market with a market share of 36.52% in 2025.

Structural heart devices refer to medical devices that are used in minimally invasive procedures to treat abnormalities in the heart’s structure, including issues in chambers, walls, and others. The growing prevalence of heart abnormalities such as heart failure, congenital heart defects, and others is resulting in an increasing number of patient admissions in clinical settings. The growing patient pool and technological advancements in these systems are further boosting the adoption of transcatheter procedures, which enable the treatment of patients suffering from high-risk diseases among the patient population.

- For instance, according to the 2024 statistics published by the Journal of Cardiac Failure (JCF), approximately 6.7 million Americans over 20 years of age have heart failure in the U.S.

Additionally, the growing geriatric population and expanding indication sets for transcatheter therapies are also major factors contributing to the growing demand for these devices in the market. This, coupled with a growing focus on research and development initiatives among key players such as Abbott, Medtronic, Boston Scientific Corporation, and others, is expected to support the growth of the global structural heart devices market.

Download Free sample to learn more about this report.

Structural Heart Devices Market Key Takeaways

- 2025 Market Size: USD 14.65 billion

- 2026 Market Size: USD 15.59 billion

- 2034 Forecast Market Size: USD 27.16 billion

- CAGR: 7.2% from 2026–2034

- North America dominated the structural heart devices market with a 36.52% share in 2025.

- The instruments segment held the largest market share in 2025.

- The heart valve diseases segment accounted for 75.5% of the market share in 2025.

North America

North America remained the leading regional market, reaching USD 5.35 billion in 2025, supported by strong adoption of advanced structural heart interventions.

Europe

Europe reached USD 5.10 billion in 2025 and is projected to expand steadily, driven by increasing demand for minimally invasive cardiac procedures.

Asia Pacific

Asia Pacific was valued at USD 3.11 billion in 2025, supported by improving healthcare infrastructure and rising awareness of cardiovascular disease treatment options.

U.S.

The U.S. structural heart devices market was estimated at USD 4.98 billion in 2025, driven by a large patient pool and continued technological advancements in cardiac care.

Japan

Japan remains a key market in Asia Pacific, supported by its aging population, growing prevalence of heart valve disorders, and increasing adoption of innovative structural heart therapies.

Read More

Market Dynamics

Market Drivers

Growing Prevalence of Heart Disorders to Boost Demand for Structural Heart Devices

There is a rising prevalence of heart diseases, such as congenital heart defects and others, further resulting in the increasing demand for structural heart devices among the patient population, driving the adoption rate of these devices in the market.

Moreover, the growing geriatric population, improved diagnostic capabilities, and other factors are additional factors supporting the increasing adoption of these devices among the patient population, thereby fueling global demand for structural heart devices. This, along with the increasing number of key players launching innovative products, is expected to boost the adoption rate, thereby contributing to the global structural heart devices market size.

- For instance, according to 2024 data published by Nature, approximately 5% of adults over the age of 65 are affected by aortic stenosis in the U.S.

Other Prominent Drivers:

- Growth in mitral and tricuspid transcatheter therapies as clinical evidence and device maturity progress.

- Minimally invasive approaches, shorter hospital stays, and faster recovery are driving clinician and patient preference.

- Emerging markets adoption and increased screening/diagnosis of valvular disease are fueled by aging populations.

Market Restraints:

High Cost Associated with Devices and Procedures to Limit the Market Growth

There is an increasing demand for structural heart systems to treat heart abnormalities among the patient population. However, the high cost associated with these products and procedures is anticipated to limit the adoption rate for these devices, particularly in emerging nations, including Mexico, India, and others.

The complex designs and adoption of biocompatible materials to manufacture these systems, especially transcatheter heart valves and repair products, are resulting in their growing cost in the market. This, along with stringent regulatory requirements among the regulatory bodies, also requires continuous upgradation of devices, which further adds to the cost barrier in the market.

Additionally, procedural expenses such as advanced imaging and limited reimbursement policies also pose major challenges among the patients, especially in emerging countries, thereby impacting the overall growth of the market globally.

- For instance, according to 2024 data published by the International Journal of Scientific Research (IJSR), it was reported that the estimated procedure cost for transcatheter aortic valve replacement (TAVR) is around USD 35,000.0 in India.

Market Opportunities

Increasing Acquisitions and Collaborations to Create Market Opportunities

There is an increasing prevalence of chronic heart conditions, such as valvular heart diseases and others, resulting in rising demand for structural heart products in the market. The increasing demand for advanced technologies, such as transcatheter valve repair and replacement procedures, is resulting in a rising focus among key players on expanding their product portfolios through strategic initiatives globally.

Key players are investing in acquisitions and collaborations with other companies, particularly in emerging nations, creating a lucrative opportunity for those operating in the industry.

Furthermore, increasing collaborations between research institutes and key companies is enabling advanced clinical evidence generation and faster development cycles for these products. The investors are also emphasizing early-stage companies developing innovative repair and replacement products, thereby fueling the adoption rate for these products globally.

- In July 2024, Edwards Lifesciences Corporation acquired JenaValve and Endotronix with an aim to expand its portfolio for structural heart products.

Market Challenges:

Limited Access in Emerging Markets to Hinder the Market Growth

There is a growing demand for advanced devices to treat structural heart diseases among the patient population. However, despite increasing demand for these advanced devices, adoption of technologies such as TAMR, TAVR, and others remains significantly limited owing to inadequate reimbursement policies, limited innovation of healthcare infrastructure, reduced number of trained professionals, and others, especially in developing countries such as Mexico and others.

Additionally, many healthcare facilities in emerging nations lack the necessary imaging modalities, such as cardiac CT, MRI, and others, required for accurate deployment of devices for the treatment of these procedures. Therefore, all the factors mentioned above are resulting in limited access to healthcare facilities among patients, further expected to hinder the market growth.

- For instance, according to a 2020 article published by Science Direct, it was reported that there is only 1 cardiothoracic surgeon per 4 million population in Africa.

Other Prominent Challenges:

- Intense competition among leading device makers is leading to pricing pressure in key product segments.

- Regulatory and clinical evidence requirements for newer mitral/tricuspid devices can prolong time-to-market.

- Procedural training, access to hybrid ORs / cath labs, and physician learning curves for complex repairs.

Structural Heart Devices Market Trends

Technological Advancements in the Next-Generation Transcatheter Fuels Product Demand

There is a growing advancement of next-generation transcatheter products and innovation in customized implant biomaterials and design. Key players are focusing on the development and introduction of advanced systems with retrievable and repositionable valves, which further supports the adoption rate of these products in the market.

Along with this, a growing preference for personalized treatment plans that utilize patient-specific valve geometry, 3D modeling, and other techniques is enabling accurate device sizing and improving long-term outcomes. These innovations in technology are expanding the patient pool to include younger individuals or those with lower risk, requiring longer-lasting devices.

- In September 2025, Foldax, in partnership with Dolphin Life Science LLP, launched the TRIA mitral valve with an aim to strengthen its presence in India.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product

Increasing Number of Product Launches to Drive Instruments Segment Dominance

Based on the product, the market is classified into instruments and accessories. Instruments are further segmented into heart valve devices, occlusion & closure devices, and others.

To know how our report can help streamline your business, Speak to Analyst

The instruments segment held the largest market share in 2025. The growth is owing to the increasing number of patient admissions for the treatment of heart abnormalities, resulting in a rising demand for advanced structural heart systems globally. This, coupled with the increasing focus of prominent companies towards receiving approvals for structural heart products, is further expected to support the segmental growth.

- In September 2025, Genesis MedTech received approval for the J-Valve Transfemoral Transcatheter Aortic Valve Replacement (TAVR) System from China's National Medical Products Administration (NMPA) for the treatment of aortic regurgitation in China.

The accessories segment is expected to grow at a CAGR of 8.0% over the forecast period.

By Procedure Type

Increasing Number of Valve Replacement Procedures Led to the Dominance of the Segment

Based on procedure type, the market is bifurcated into valve replacement procedures, repair procedures, and structural heart closure procedures. Valve replacement procedures are further bifurcated into transcatheter aortic valve replacement (TAVR), transcatheter mitral valve replacement (TMVR), and others. Repair procedures are divided into mitral edge-to-edge repair, tricuspid edge-to-edge repair, and others. Structural heart closure procedures are segmented into atrial septal defect closure, ventricular septal defect closure, and others.

The valve replacement procedures segment dominated the market in 2025. In 2026, the segment is anticipated to dominate with a 53.1% share. The dominant share is owing to the increasing prevalence of heart valve defects, resulting in a growing number of valve replacement procedures among the patient population, thereby supporting the segmental growth in the market.

- According to statistics published by ScienceDirect, approximately 300,000 heart valve procedures were performed globally in 2021. Also, this number is projected to increase to 800,000 annually by 2050.

The repair procedures segment is expected to grow at a CAGR of 7.7% in the market during the forecast period.

By Indication

The Increasing Prevalence of Heart Valve Diseases Led to the Dominance of the Segment

Based on indication, the market is segmented into heart valve diseases, congenital heart defects, and others.

The heart valve diseases segment dominated the global market in 2025. By indication, the heart valve diseases segment held the share of 75.5% in 2025. The growth is due to the increasing prevalence of heart valve diseases such as stenosis, regurgitation, and others, further resulting in a rising adoption and demand for innovative structural heart products such as valve repair systems among the patient population in the market.

- For instance, according to the 2024 data published by the Centers for Disease Control and Prevention (CDC), it was reported that more than 5 million people are diagnosed with heart valve disease each year in the U.S.

The segment of congenital heart defects is set to flourish with a growth rate of 9.2% across the forecast period.

By End-user

Increasing Number of Hospitals & ASCs Led to the Segment’s Dominance

Based on end user, the market is bifurcated into hospitals & ASCs, specialty clinics, and others.

The hospitals and ASCs segment dominated the market in 2025. The growing prevalence of heart abnormalities, increasing patient admissions, the rising number of hospitals and ambulatory surgical centers, and others are some of the vital factors supporting the growth of the segment in the market. Furthermore, the segment is set to hold an 80.5% share in 2026.

- For instance, according to 2024 statistics published by the Ministry of Health, Labour and Welfare of Japan (MHLW), it was reported that there are about 8,122 hospitals in Japan.

In addition, specialty clinics’ end users are projected to grow at a CAGR of 8.2% during the study period.

Structural Heart Devices Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Structural Heart Devices Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America:

North America dominated the structural heart devices market in 2024, valued at USD 5.11 billion, and also took the leading share in 2025 with USD 5.35 billion. The dominance of the region is due to distinct factors, including the growing prevalence of heart abnormalities, the growing number of heart valve operations, and the growing adoption of transcatheter valve replacement procedures, established ewe, among others. In 2025, the U.S. market is estimated to reach USD 4.98 billion.

- For instance, according to 2025 statistics published by The Texas Heart Institute at Baylor College of Medicine, it was reported that about 106,000 heart valve operations are performed each year in the U.S.

Other regions, such as Europe and the Asia Pacific, are expected to witness significant growth in the forecast period. During the study period, the European region is projected to record a growth rate of 5.7% and reach the valuation of USD 5.10 billion in 2025. This is due to the growing adoption of advanced transcatheter-based heart devices and the rising number of procedural volumes, such as mitral and tricuspid interventions, in the region. Moreover, the increasing prevalence of heart defects, as well as the improvement of healthcare infrastructure in countries such as China, South Korea, Japan, and India, are some of the other contributing factors to market growth. Backed by these factors, countries such as the U.K. are expected to record the valuation of USD 0.73 billion, Germany to record USD 1.29 billion, and France to record USD 0.89 billion in 2025. After Europe, the market in the Asia Pacific is estimated to reach USD 3.11 billion in 2025 and secure the position of the third-largest region in the market. In the region, India is estimated to reach USD 0.36 billion while China is estimated to reach USD 1.06 billion in 2025.

Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market. The Latin America market in 2025 is set to record USD 0.63 billion as its valuation. The increasing adoption of advanced technologies, increasing access to specialized cardiac care, and other factors are expected to boost product adoption in these regions. In the Middle East & Africa, GCC is set to attain the value of USD 0.23 billion in 2025.

Competitive Landscape

Key Industry Players

Growing Acquisitions and Collaborations Among the Key Companies to Led Their Market Dominance

A strong geographical presence, along with a significant focus on R&D activities to develop and introduce novel products, is one of the major factors contributing to the dominance of these companies in the market. Abbott, Medtronic, and Boston Scientific Corporation are prominent companies in the market in 2025. Furthermore, the increasing emphasis of key players on acquisitions and mergers to increase their brand presence is expected to support the global structural heart devices market share.

- For instance, in October 2025, Medtronic collaborated with DASI Simulations, a player in AI-driven predictive modeling and digital-twin technology, to improve access to DASI technology to optimize outcomes for patients undergoing transcatheter aortic valve replacement (TAVR) in the U.S.

Other key players, including Edwards Lifesciences Corporation, and others, are also growing in the market, primarily owing to their rising focus on R&D activities to launch novel products to widen their product portfolio in the market.

List of Key Structural Heart Devices Companies Profiled:

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- Genesis MedTech (Singapore)

- Artivion, Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- Corcym Group (U.K.)

- LivaNova PLC (U.K.)

- JenaValve (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- November 2025 – RapidAI received U.S. FDA approval for the Aortic Management part of the Rapid Aortic product, a comprehensive, deep clinical AI solution designed to transform the acute assessment and longitudinal management of aortic disease. This helped the company in strengthening its presence.

- November 2025 – Koninklijke Philips N.V., collaborated with Edwards Lifesciences Corporation to launch DeviceGuide to support clinicians during cardiac procedures. This helped the company in strengthening its presence.

- August 2025 – Corcym Group announced that its Perceval Plus sutureless aortic heart valve was used in a First-Ever robotic aortic valve replacement, through a tiny incision in the neck of a patient at the Cleveland Clinic's Heart, Vascular & Thoracic Institute. This helped the company in strengthening its presence.

- August 2025 – Abbott launched its MitraClip G5 and TriClip G5 systems, advancing minimally invasive treatment options for patients with heart valve disease with an aim to strengthen its product offerings.

- July 2025 – JenaValve Technology, Inc. conducted the New York Valves 2025 conference, showcasing the expanding use of the Trilogy system in patients with aortic regurgitation (AR). This helped the company in strengthening its brand presence.

REPORT COVERAGE

The market report provides a detailed global structural heart devices market analysis and focuses on key aspects such as leading companies, product, procedure type, indication, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.2% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product, Procedure Type, Indication, End User, and Region |

|

By Product |

· Instruments o Heart Valve Devices o Occlusion & Closure Devices o Others · Accessories |

|

By Procedure Type |

· Valve Replacement Procedures o Transcatheter Aortic Valve Replacement (TAVR) o Transcatheter Mitral Valve Replacement (TMVR) o Others · Repair Procedures o Mitral Edge-to-Edge Repair o Tricuspid Edge-to-Edge Repair o Others · Structural Heart Closure Procedures o Atrial Septal Defect closure o Ventricular Septal Defect closure o Others |

|

By Indication |

· Heart Valve Diseases · Congenital Heart Defects · Others |

|

By End User |

· Hospitals & ASCs · Specialty Clinics · Others |

|

By Region |

· North America (By Product, By Procedure Type, By Indication, By End User, and by Country) o U.S. (By Indication) o Canada (By Indication) · Europe (By Product, By Procedure Type, By Indication, By End User, and by Country/Sub-region) o U.K. (By Indication) o Germany (By Indication) o France (By Indication) o Italy (By Indication) o Spain (By Indication) o Scandinavia (By Indication) o Rest of Europe (By Indication) · Asia Pacific (By Product, By Procedure Type, By Indication, By End User, and by Country/Sub-region) o China (By Indication) o Japan (By Indication) o India (By Indication) o Australia (By Indication) o Southeast Asia (By Indication) o Rest of Asia Pacific (By Indication) · Latin America (By Product, By Procedure Type, By Indication, By End User, and by Country/Sub-region) o Brazil (By Indication) o Mexico (By Indication) o Rest of Latin America (By Indication) · Middle East & Africa (By Product, By Procedure Type, By Indication, By End User, and by Country/Sub-region) o GCC (By Indication) o South Africa (By Indication) o Rest of the Middle East & Africa (By Indication) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 14.65 billion in 2025 and is projected to reach USD 27.16 billion by 2032.

In 2025, the North America regional market value stood at USD 5.35 billion.

Growing at a CAGR of 7.2%, the market will exhibit steady growth over the forecast period (2026-2034).

By product, the instruments segment is the leading segment in this market.

The introduction of novel structural heart systems is one of the key factors driving the market's growth.

Abbott and Medtronic are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of heart abnormalities, the increasing number of heart valve procedures, among others, are some of the major factors anticipated to fuel the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us