Superconducting Wire Market Size, Share & Industry Analysis, By Type (Low-temperature Superconductor (LTS), Medium-temperature Superconductor (MTS), and High-temperature Superconductor (HTS)), By End User (Medical, Defense, Energy & Power, Transportation, and Others), Regional Forecast, 2026-2034

Superconducting Wire Market Size and Future Outlook

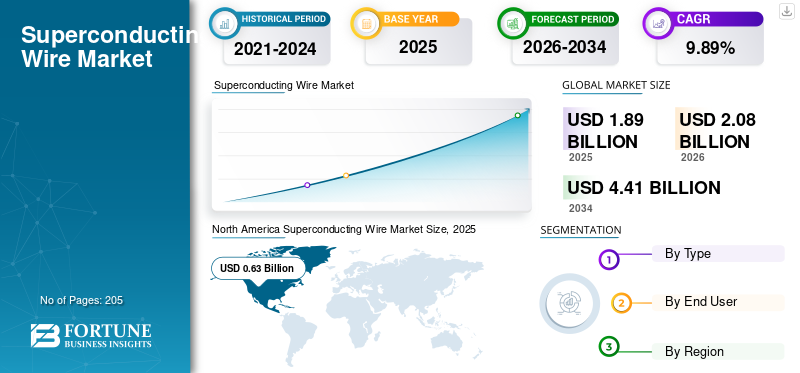

The global superconducting wire market size was valued at USD 1.89 billion in 2025. The market is projected to grow from USD 2.08 billion in 2026 to USD 4.41 billion by 2034, exhibiting a CAGR of 9.89% during the forecast period. North America dominated the superconducting wire market with a market share of 33.33% in 2025.

Superconducting wire refers to a specialized conductor made from materials that exhibit zero electrical resistance and expulsion of magnetic fields (Meissner effect) when cooled below a critical temperature. These wires, typically composed of low-temperature superconductors (NbTi, Nb₃Sn) or high-temperature superconductors (Yttrium Barium Copper Oxide (YBCO), Bismuth Strontium Calcium Copper Oxide (BSCCO)), are used in applications requiring high current density and strong magnetic fields, such as magnetic resonance imaging (MRI) systems, particle accelerators, fusion reactors, and advanced power cables. The growing demand for energy-efficient and high-performance electrical systems, particularly in healthcare and energy sectors, is driving the market. Increasing demand for efficient power transmission and compact high-performance systems is driving the adoption of high-temperature superconductors (HTS).

According to the International Energy Agency, global electricity demand is expected to grow by ~3% annually through 2026, increasing the need for efficient transmission technologies such as superconducting cables. Additionally, the World Health Organization (WHO, 2022) highlights expanding access to diagnostic imaging, with MRI installations rising in emerging economies, further driving demand for the product. These trends collectively support sustained adoption across medical, energy, and scientific applications.

- For instance, in March 2023, Bruker Corporation expanded its superconducting wire production capabilities to support the rising demand for high-field MRI and NMR systems. The company focused on enhancing NbTi and Nb₃Sn wire performance to enable higher magnetic field strengths for advanced research applications. This initiative aligns with increasing global demand for precision diagnostics and scientific instrumentation, reinforcing Bruker’s position in supplying high-performance superconducting technology for medical and research sectors.

Some of the leading companies operating in the industry include Bruker Corporation, Fujikura Ltd., Sumitomo Electric Industries, Ltd., SuperPower Inc., and others. Fujikura Ltd. is a leading Japanese manufacturer of advanced materials and cable technologies, with a strong focus on high-temperature superconducting (HTS) wires and coated conductors. The company plays a key role in developing superconducting solutions for power transmission, energy infrastructure, and next-generation grid applications.

Download Free sample to learn more about this report.

SUPERCONDUCTING WIRE MARKET Key Takeaways

- 2025 Market Size: USD 1.89 billion

- 2026 Market Size: USD 2.08 billion

- 2034 Forecast Market Size: USD 4.41 billion

- CAGR: 9.89% from 2026–2034

- North America dominated the superconducting wire market with a market share of 33.33% in 2025.

- The High-temperature Superconductor (HTS) segment recorded the fastest growth, expanding at a CAGR of 10.83%.

- The energy & power segment is anticipated to grow at a CAGR of 11.34% during the forecast period.

North America

North America held the highest share in 2025, valued at USD 0.63 billion, and is expected to take a significant share in 2026 with USD 0.69 billion. The market in the region is primarily driven by strong investments in advanced research, healthcare infrastructure, and energy innovation programs.

Asia Pacific

Asia Pacific reached USD 0.59 billion in 2025, securing the second-largest market share due to increasing adoption of superconducting technologies across energy and transportation sectors.

Europe

Europe is projected to record a growth rate of 9.52% in the coming years, reaching a valuation of USD 0.45 billion in 2025, supported by large-scale fusion and accelerator programs.

U.S.

The market was estimated at approximately USD 0.55 billion in 2025, supported by investments in fusion energy research, MRI installations, and high-field magnet development programs.

Japan

The Japanese market in 2025 reached around USD 0.12 billion, accounting for roughly 6.50% of global revenues. Demand is supported by the ongoing development of the Chuo Shinkansen maglev project and strong R&D in HTS materials.

Read More

SUPERCONDUCTING WIRE MARKET TRENDS

Advancements in Ultra-High-Field Magnets and Energy Systems to Boost Product Adoption

The superconducting wire market is witnessing strong momentum, driven by advancements in high-field magnet applications and next-generation energy systems. A key trend is the increasing development of ultra-high-field magnets (>20 Tesla) for scientific research and fusion, requiring advanced Nb₃Sn and HTS wires with superior current density. For instance, in December 2023, CERN progressed work on next-generation accelerator magnets under the Future Circular Collider program, highlighting growing demand for high-performance superconductors. Another trend is the emergence of superconducting technologies in hydrogen infrastructure, where compact and efficient systems are needed for electrolysis and storage integration.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Advanced Medical Imaging and Diagnostic Imaging Procedures to Drive Market Growth

The market is significantly influenced by the expanding demand for advanced medical imaging systems, particularly MRI and NMR technologies. Superconducting wires are essential for generating strong and stable magnetic fields required in these systems. According to the World Health Organization (WHO), 2022, there is a substantial gap in MRI availability, with low- and middle-income countries having less than 1 MRI unit per million populations, compared to over 30 units per million in high-income regions. This disparity is driving investments in healthcare infrastructure globally. Additionally, the 2023 OECD reports stated that the steady growth in diagnostic imaging procedures across developed economies is further increasing equipment utilization and replacement demand. These factors are anticipated to drive superconducting wire market growth during the forecast period.

MARKET RESTRAINTS

High Cost and Complexity of Cryogenic Cooling Infrastructure to Hamper Market Demand

The superconducting wire market faces a significant restraint due to the high cost and complexity of cryogenic cooling systems required for operation. Superconductors must be maintained at extremely low temperatures, often using liquid helium or liquid nitrogen, which adds substantial capital and operational expenses. According to the U.S. Department of Energy, cryogenic cooling can account for a considerable portion of total system costs in superconducting applications. Additionally, in 2021, the International Institute of Refrigeration highlighted an increasing pressure on helium supply, with periodic shortages impacting availability and pricing. These factors make large-scale deployment challenging, particularly in cost-sensitive regions and emerging markets.

MARKET OPPORTUNITIES

Emerging Applications in Electric Aviation and Advanced Mobility Systems to Amplify Product Demand

The market is creating new opportunities through its application in electric aviation and advanced mobility systems, where high power density and weight reduction are critical. Superconducting motors and generators enable significantly higher efficiency and compact designs compared to conventional systems. According to the 2023 International Energy Agency Reports, aviation accounts for nearly 2–3% of global CO₂ emissions, prompting accelerated development of electrified propulsion technologies.

Superconducting systems can reduce electrical losses by up to 50% in high-power applications, making them suitable for next-generation aircraft and hybrid propulsion systems. Several aerospace research programs are exploring superconducting components to improve energy efficiency and reduce overall system weight. This trend opens substantial long-term opportunities for superconducting wire manufacturers, particularly in high-temperature superconductors, as the aviation industry transitions toward sustainable and electrified solutions.

MARKET CHALLENGES

Limited Standardization and Scalability Challenges Across Emerging Superconducting Applications Hinders Market Demand

The superconducting wire market faces challenges due to limited standardization and scalability across different applications and regions. Variations in material specifications, performance requirements, and system integration standards make large-scale deployment complex. According to the International Electrotechnical Commission, standardization efforts for superconducting components are still evolving, particularly for high-temperature superconductors. Additionally, scaling production while maintaining uniform quality and performance remains difficult, especially for advanced HTS tapes.

Segmentation Analysis

By Type

Low-temperature Superconductor (LTS) Segment Dominated Due to their Well-Established Technology

Based on type, the market is classified into Low-temperature Superconductor (LTS), Medium-temperature Superconductor (MTS), and High-temperature Superconductor (HTS).

In 2025, Low-temperature Superconductor (LTS) held the dominant superconducting wire market share. Low-temperature superconductors (LTS), particularly NbTi and Nb₃Sn, dominate the market due to their well-established technology, reliability, and large-scale commercial deployment. These materials are extensively used in MRI systems, particle accelerators, and fusion projects, where consistent performance and proven track records are critical. According to the International Atomic Energy Agency (IAEA, 2022), thousands of MRI systems globally rely on NbTi-based superconductors, ensuring stable demand. Medium temperature superconductors enable improved performance at moderate cooling requirements, bridging the gap between LTS reliability and HTS efficiency.

The High-temperature Superconductor (HTS) segment is experiencing the highest growth and is expected to grow at a CAGR of 10.83% during the study period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Medical Segment Led due to the Widespread Usage of Superconductors in MRI and NMR Systems

Based on end user, the market is classified into medical, defense, energy & power, transportation, and others.

In 2025, the medical segment dominated the global market. This growth is primarily due to the extensive use of superconductors in MRI and NMR systems, which require stable and high-intensity magnetic fields. These systems rely heavily on NbTi-based superconducting wires for accurate imaging and diagnostics. Additionally, growing investments in healthcare infrastructure and early disease detection are driving the installation of advanced imaging systems globally. The product ensures high precision, reliability, and efficiency, making them indispensable in medical applications.

The energy & power segment is expected to grow at a CAGR of 11.34%.

Superconducting Wire Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Superconducting Wire Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the highest share in 2025, valued at USD 0.63 billion, and is expected to take a significant share in 2026 with USD 0.69 billion. The market in the region is primarily driven by strong investments in advanced research, healthcare infrastructure, and energy innovation programs. The region has a high concentration of MRI installations and diagnostic imaging facilities, supporting steady demand for superconducting materials. Additionally, the U.S. Department of Energy (DOE) continues to fund fusion energy and high-field magnet research, increasing the need for Nb₃Sn and HTS wires.

U.S. Superconducting Wire Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.55 billion in 2025, accounting for roughly 28.99% of the global market sales.

Europe

Europe is projected to record a growth rate of 9.52% in the coming years, which is the third-highest among all regions, reaching a valuation of USD 0.45 billion in 2025. Europe’s market is strongly driven by large-scale fusion and accelerator programs, particularly through ITER (France) and CERN (Switzerland), which require high volumes of Nb₃Sn and advanced superconducting materials. The European Commission’s Fusion for Energy (F4E) program continues to fund superconducting magnet procurement and system integration. Additionally, countries such as Germany and the Netherlands are advancing HTS cable demonstration projects for urban grid applications, supported by EU energy transition policies.

Germany Superconducting Wire Market

The Germany’s market in 2025 reached around USD 0.12 billion 2025 and is estimated at around USD 0.13 billion in 2026, representing roughly 6.27% of the global revenues.

Asia Pacific

Asia Pacific reached USD 0.59 billion in 2025 and secure the second-largest share of the market.

Asia Pacific’s market is driven by strong national programs in fusion, high-speed transport, and power infrastructure modernization. China is advancing large-scale projects such as the EAST fusion reactor, increasing demand for Nb₃Sn and HTS materials. Japan continues development of superconducting maglev systems (Chuo Shinkansen), requiring high-performance superconducting wires. South Korea’s KSTAR fusion program also contributes to steady demand for advanced conductors.

Japan Superconducting Wire Market

The Japanese market in 2025 reached around USD 0.12 billion, accounting for roughly 6.50% of global revenues. In Japan, the product demand is supported by the ongoing development of the Chuo Shinkansen maglev project, which utilizes advanced superconducting magnet systems. Additionally, strong R&D in HTS materials and industrial superconducting applications continues to drive technological advancement and domestic demand.

China Superconducting Wire Market

China’s market is projected to be significant worldwide during the study period, with 2025 revenues stood at around USD 0.23 billion, representing roughly 12.41% of the global market.

India Superconducting Wire Market

The Indian market in 2025 reached around USD 0.06 billion, accounting for roughly 3.01% of global revenues.

Latin America

Latin America is expected to witness moderate growth in the market during the forecast period. The Latin America market reached a valuation of USD 0.12 billion in 2025. The region’s market is primarily influenced by select high-end medical infrastructure and research collaborations rather than large-scale industrial deployment. Brazil leads regional demand through its network of advanced hospitals and participation in international scientific research programs requiring superconducting components. Mexico contributes through integration into North American medical equipment supply chains.

Brazil Superconducting Wire Market

Brazil's market reached around USD 0.06 billion in 2025, representing roughly 3.42% of global revenues.

Middle East & Africa

The Middle East & Africa is expected to witness significant growth in this market during the forecast period. The market reached a valuation of USD 0.09 billion in 2025, driven by targeted investments in advanced research and high-end medical infrastructure, particularly in the GCC region. Countries such as the UAE and Saudi Arabia are expanding specialized healthcare facilities equipped with high-field MRI systems, supporting demand for NbTi wires. Additionally, Israel contributes through research programs in particle physics and advanced materials, creating niche demand.

GCC Superconducting Wire Market

The GCC market reached around USD 0.05 billion in 2025, representing roughly 2.58% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Major players are Focusing on Bolstering their Partnerships to Increase their Market Share

The global superconducting wire market holds a consolidated market structure, constituting prominent players such as Alfa Laval, Danfoss, Kelvion Holding GmbH, SWEP International AB, and others. Companies operating in the industry are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in July 2023, Fujikura Ltd. advanced its high-temperature superconducting (HTS) wire technology by developing improved YBCO-based coated conductors for power transmission applications. The company collaborated with utility partners in Japan to demonstrate stable, high-capacity power flow using HTS cables.

Other key players in the global market include Japan Superconductor Technology, Inc. (JASTEC),

Furukawa Electric Co., Ltd., Theva Dünnschichttechnik GmbH, American Superconductor Corporation, and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY SUPERCONDUCTING WIRE COMPANIES PROFILED

- Bruker Corporation (U.S.)

- Fujikura Ltd. (Japan)

- Sumitomo Electric Industries, Ltd. (Japan)

- SuperPower Inc. (U.S.)

- Luvata (Finland)

- Western Superconducting Technologies Co., Ltd. (China)

- Japan Superconductor Technology, Inc. (JASTEC) (Japan)

- Furukawa Electric Co., Ltd. (Japan)

- Theva Dünnschichttechnik GmbH (Germany)

- American Superconductor Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2023: SuperPower Inc. announced advancements in second-generation (2G) HTS wire manufacturing, improving current-carrying capacity and cost efficiency. The company supported multiple pilot projects in North America focused on superconducting cables and fault current limiters. These developments align with increasing investments in resilient and efficient power grids, positioning SuperPower as a key player in HTS deployment.

- April 2023: Western Superconducting Technologies expanded production of NbTi and Nb₃Sn wires to support China’s fusion and high-field magnet projects. The company focused on domestic supply chain strengthening and technological improvements in superconducting materials. This initiative aligns with China’s increasing investments in advanced energy and research infrastructure.

- November 2022: Sumitomo Electric Industries strengthened its product portfolio by supplying HTS cables for a grid demonstration project in Japan. The project highlighted enhanced transmission efficiency and reduced energy losses using superconducting materials. The company also focused on scaling production of YBCO wires to meet growing demand from energy and industrial sectors, reinforcing its leadership in HTS technology development.

- September 2022: Luvata continued supplying NbTi and Nb₃Sn superconducting wires for large-scale research projects, including fusion and particle accelerator programs. The company enhanced its manufacturing processes to improve wire uniformity and performance under high magnetic fields. This supports growing demand from international research collaborations and reinforces Luvata’s role in high-performance superconducting materials.

- June 2022: JASTEC advanced its superconducting wire production by supplying high-performance Nb₃Sn conductors for international fusion research projects. The company emphasized improving mechanical strength and current density to meet the stringent requirements of high-field magnets. This reflects JASTEC’s role in supporting global fusion initiatives and advanced scientific research.

REPORT COVERAGE

The global superconducting wire market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.89% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, End User, and Region |

| By Type |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.89 billion in 2025 and is projected to reach USD 4.41 billion by 2034.

In 2025, the North America market value stood at USD 0.63 billion.

The market is expected to exhibit a CAGR of 9.89% during the forecast period.

The Low-temperature Superconductor (LTS) segment led the market by type.

Increasing demand for advanced medical imaging and diagnostic imaging procedures is the key factor driving market growth.

Bruker Corporation, Fujikura Ltd., Sumitomo Electric Industries, Ltd., SuperPower Inc., and others are some of the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us