Surgical Equipment Market Size, Share & Industry Analysis, By Product (Surgical Sutures & Staplers, Handheld Surgical Devices {Forceps & Spatulas, Retractors, Dilators, Graspers, Auxiliary Instruments, Cutter Instruments, and Others}, Electrosurgical Devices, and Others), By Application (General Surgery, Orthopedic Surgery, Cardiovascular Surgery, Neurosurgery, Obstetrics & Gynecology Surgery, Urology Surgery, Plastic & Reconstructive Surgery, and Others), By End-user (Hospitals and ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Surgical Equipment Market Size & Future Outlook

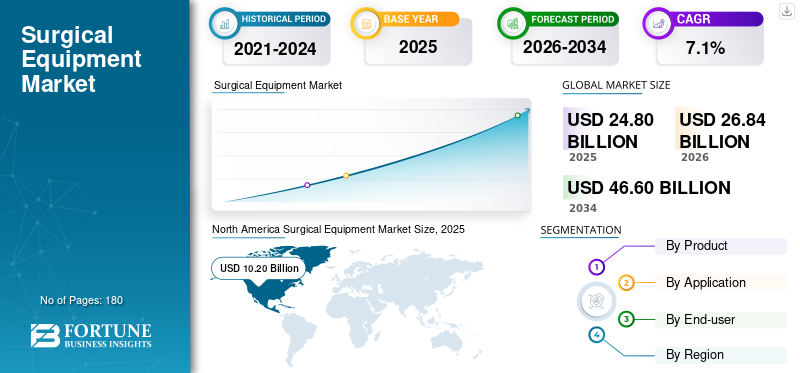

The global surgical equipment market size was valued at USD 24.80 billion in 2025. The market is projected to grow from USD 26.84 billion in 2026 to USD 46.60 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period. North America dominated the surgical equipment market with a market share of 41.12% in 2025.

The global market includes a wide range of instruments and devices used by surgeons and operating room teams to cut, grasp, dissect, retract, seal, suture, staple, and manage tissue during surgical procedures. These products include surgical sutures and staplers, handheld surgical instruments such as forceps, retractors, dilators, graspers, cutters, auxiliary instruments, electrosurgical devices, and other procedure-supporting surgical tools. The market is growing steadily as surgical volumes continue to rise across developed and emerging economies. Aging populations, increasing prevalence of chronic diseases, expanding access to hospital-based and outpatient surgeries, and growing demand for minimally invasive procedures are strengthening product adoption. In addition, hospitals and ambulatory surgical centers are investing in advanced, durable, and procedure-specific instruments to improve surgical precision, reduce operating time, and enhance patient outcomes. The shift toward disposable and single-use surgical accessories is also supporting the growth of the market by improving infection control and workflow efficiency.

Johnson & Johnson, Medtronic plc, B. Braun SE, and Stryker Corporation held the highest share in 2025, supported by strategic initiatives aimed at expanding their market presence and diversifying product portfolios through new product introductions.

Download Free sample to learn more about this report.

SURGICAL EQUIPMENT MARKET TRENDS

Shift Toward Single-use, Ergonomic, and Specialty-specific Instruments is Boosting Product Demand

A key trend in the surgical equipment market is the move toward single-use, ergonomic, and specialty-specific products. Hospitals are increasingly using disposable surgical accessories and selected single-use instruments to reduce infection risk, simplify operating room workflows, and avoid the burden of sterilization. This trend is especially strong for products such as electrosurgical pencils, electrodes, grounding pads, blades, trocars, stapler reloads, and certain procedure-specific accessories. Surgeons are also demanding instruments that offer better grip, lighter weight, improved tactile feedback, and reduced hand fatigue during long procedures. This is pushing manufacturers to redesign traditional handheld surgical tools with improved ergonomics and specialty-specific features.

Another significant trend is the growing use of advanced energy-based surgical devices that support cutting, coagulation, vessel sealing, and tissue management within a single workflow. Although traditional surgical instruments remain essential, product innovation is increasingly focused on improving precision, safety, and operating room efficiency. Hospitals are also paying greater attention to instrument traceability, lifecycle management, and standardization of surgical trays. These changes are gradually shifting purchasing behavior from basic instrument replacement toward higher-value, performance-oriented surgical equipment procurement.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Number of Surgical Procedures to Drive Product Demand

The growing number of surgical procedures worldwide is one of the strongest drivers of the global surgical equipment market. The growing burden of chronic diseases such as cardiovascular disorders, cancer, orthopedic conditions, urological diseases, and gynecological disorders is leading to higher demand for both emergency and elective surgeries. At the same time, aging populations are driving an increase in orthopedic, cardiovascular, general, and neurosurgical procedures, all of which require a broad range of surgical instruments and devices. Hospitals are also witnessing growth in complex surgical procedures that need specialized tools for precise tissue handling, cutting, coagulation, suturing, and wound closure. This trend is strengthening demand for handheld surgical devices, electrosurgical devices, sutures, and staplers.

Another important growth factor is the expansion of ambulatory surgical centers, especially in North America and Europe, where many procedures are moving from inpatient settings to outpatient care. These centers require compact, efficient, and cost-effective surgical equipment to support high-throughput procedures. As a result, manufacturers are increasingly focusing on durable, ergonomic, and specialty-specific devices that help surgeons to perform procedures with greater control, safety, and efficiency.

MARKET RESTRAINTS

Pricing Pressure and Reprocessing Concerns May Limit Market Growth

Despite steady demand, the surgical equipment market faces restraint from pricing pressure, especially in public healthcare systems and tender-driven procurement markets. Hospitals and government buyers often purchase surgical instruments and consumables through competitive bidding, which places pressure on manufacturers to reduce prices while maintaining quality standards. This trend is particularly visible in Europe, Latin America, and parts of the Asia Pacific, where bulk procurement and centralized purchasing systems are common.

In addition, reusable surgical instruments require repeated cleaning, sterilization, inspection, and maintenance, increasing the total cost of ownership for hospitals. Poor reprocessing practices may also increase the risk of surgical site infections, instrument damage, and procedure delays. While single-use devices help reduce some of these risks, they create additional cost and waste management concerns. Smaller hospitals and clinics in emerging markets may delay instrument replacement due to budget constraints, which can slow the adoption of new surgical equipment. Moreover, premium surgical staplers, advanced electrosurgical products, and high-quality specialty instruments may remain unaffordable for some healthcare facilities. These factors can restrict market penetration, especially in cost-sensitive regions, even though underlying surgical demand remains strong.

MARKET OPPORTUNITIES

Expansion of Minimally Invasive and Outpatient Surgical Procedures to Create Strong Growth Opportunities

The growing shift toward minimally invasive and outpatient surgical procedures is creating a major opportunity for surgical equipment manufacturers. Surgeons and healthcare providers are increasingly adopting techniques that require smaller incisions, shorter hospital stays, faster recovery, and lower complication risks. This transition is increasing demand for advanced graspers, cutters, electrosurgical tools, staplers, and specialty handheld instruments designed for laparoscopic, endoscopic, urologic, gynecologic, and orthopedic procedures. Ambulatory surgical centers are also expanding rapidly, especially in developed markets, as they offer lower-cost care and greater patient convenience. This is creating demand for standardized surgical instrument sets, disposable accessories, and compact electrosurgical platforms.

In emerging markets, rising healthcare investment, expanding private hospital networks, and improved access to surgery are creating new opportunities for mid-priced, locally distributed surgical equipment. Manufacturers that can offer durable instruments, value-based pricing, and strong after-sales support are likely to gain share in these regions. There is also an opportunity in procedure-specific kits and bundled product offerings, where suppliers provide instruments, sutures, staplers, and accessories tailored to specific surgeries. This approach helps hospitals simplify procurement and improve operating room efficiency.

MARKET CHALLENGES

Supply Chain Volatility, Sterilization Burden, and Regulatory Compliance to Remain Key Market Challenges

The surgical equipment market continues to face challenges related to supply chain stability, sterilization requirements, product quality, and regulatory compliance. Many surgical instruments are made using high-grade stainless steel, polymers, electronics, and precision components, making manufacturers vulnerable to fluctuations in raw material prices and component availability. Supply chain disruptions can delay hospital procurement and create pricing uncertainty for distributors and healthcare systems. Another major challenge is the burden of sterilization and reprocessing for reusable instruments. Hospitals must invest in trained staff, sterilization infrastructure, tracking systems, and maintenance protocols to ensure that instruments remain safe and functional. Any failure in this process can lead to infection risk, instrument failure, or surgical delays. Regulatory requirements are also becoming stricter, particularly for device safety, biocompatibility, traceability, and post-market surveillance. Compliance adds cost and complexity for manufacturers, especially smaller companies trying to expand internationally. In addition, the market includes many low-cost local suppliers, which increases competition and can make it difficult for premium brands to defend pricing. Balancing affordability, quality, durability, and regulatory compliance will remain a major challenge for companies operating in this market.

Segmentation Analysis

By Product

Handheld Surgical Devices Segment Dominates Due to its Broad Usage Across Surgical Specialties

Based on product, the market is segmented into surgical sutures & staplers, handheld surgical devices, electrosurgical devices, and others. Handheld surgical devices are further segmented into forceps & spatulas, retractors, dilators, graspers, auxiliary instruments, cutter instruments, and others.

Handheld surgical devices captures the major surgical equipment market share as they are used across almost all surgical specialties and procedure types. Instruments such as forceps, retractors, graspers, cutters, dilators, and auxiliary tools are essential in both open and minimally invasive surgeries. Unlike highly specialized capital equipment, handheld devices are required in large quantities across operating rooms, surgical trays, emergency departments, and specialty procedure settings. Their recurring replacement needs, frequent sterilization-related wear, and wide use in general, orthopedic, cardiovascular, gynecological, urological, and plastic surgeries support steady demand.

To know how our report can help streamline your business, Speak to Analyst

The electrosurgical devices segment is projected to grow at a 8.6% CAGR during the forecast period.

By Application

General Surgery Segment Leads due to Growing Usage of Basic Surgical Tools

By application, the market is segmented into general surgery, orthopedic surgery, cardiovascular surgery, neurosurgery, obstetrics & gynecology surgery, urology surgery, plastic & reconstructive surgery, and others.

General surgery held the highest market share in 2025 as it covers a broad range of high-volume procedures, including abdominal, gastrointestinal, hernia, gallbladder, appendectomy, trauma, and soft-tissue surgeries. These procedures require extensive use of sutures, staplers, forceps, retractors, cutters, graspers, electrosurgical devices, and other basic surgical tools. General surgery is performed in almost every hospital and many ambulatory surgical centers, making it one of the most consistent sources of surgical equipment demand. Moreover, the segment is estimated to hold a 30.3% share by 2026.

The plastic & reconstructive surgery segment is anticipated to grow at a 8.5% CAGR over the forecast period.

By End-user

Hospitals & ASCs Segment Dominated Due to Increasing Volume of Surgical Procedures

On the basis of end-user, the market is segmented into hospitals and ASCs, specialty clinics, and others.

In 2025, hospitals and ASCs held the largest market share as most surgical procedures are performed in these settings. Hospitals manage complex surgeries, emergency cases, inpatient procedures, and specialty operations, creating continuous demand for surgical instruments, electrosurgical devices, sutures, staplers, and procedure-specific tools. ASCs are also becoming important buyers as more orthopedic, general, urology, gynecology, and plastic surgery procedures shift to outpatient settings. These facilities purchase surgical equipment in bulk, maintain multiple operating rooms, and regularly replace instruments due to wear and sterilization cycles. Furthermore, the segment is set to hold 83.5% share by 2026.

The specialty clinics segment is projected to grow at a CAGR of 9.5% during the forecast period.

Surgical Equipment Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Surgical Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest market share in 2024, valued at USD 9.43 billion. The market in North America was valued at USD 10.20 billion in 2025. The growth is driven by high surgical procedure volumes, strong healthcare spending, advanced hospital infrastructure, and the rapid adoption of premium surgical technologies. The U.S. contributes the majority of regional demand, supported by a large base of hospitals and ambulatory surgical centers performing general, orthopedic, cardiovascular, urology, gynecology, and plastic surgeries.

U.S Surgical Equipment Market

The U.S. is anticipated to reach USD 10.20 billion by 2026, accounting for approximately 38.0% of the global sales.

Europe

Europe is projected to record a growth rate of 5.8% during the forecast period, the second-highest globally. The maeket is likely to reach USD 8.70 billion by 2026. The region is projected to grow steadily due to its large base of surgical procedures, well-established public healthcare systems, and ongoing demand for replacement surgical instruments across hospitals. Countries such as Germany, the U.K., France, Italy, and Spain perform a high volume of general, orthopedic, cardiovascular, urology, and gynecological surgeries, supporting consistent consumption of sutures, staplers, handheld devices, and electrosurgical products.

U.K. Surgical Equipment Market

The U.K. market is projected to reach USD 1.77 billion by 2026, representing approximately 6.6% of global revenues.

Germany Surgical Equipment Market

Germany's market is expected to reach USD 1.39 billion by 2026, accounting for approximately 5.2% of global revenue.

Asia Pacific

By 2026, the market in Asia Pacific is projected to reach approximately USD 5.65 billion, making it the third-largest market worldwide. The region is expected to record the fastest growth in the market, driven by rising surgical volume procedures, expanding hospital infrastructure, growing medical tourism, and improving access to advanced healthcare services. China and India are major contributors to the surgical equipment marker growth due to their large patient populations, increasing healthcare investments, expanding private hospital networks, and rising burden of chronic diseases requiring surgical intervention.

Japan Surgical Equipment Market

Japan is projected to generate approximately USD 1.21 billion in revenue by 2026, representing nearly 4.5% of the global revenues.

China Surgical Equipment Market

China’s market is anticipated to reach around USD 1.93 billion by 2026, accounting for nearly 7.2% of global revenues.

India Surgical Equipment Market

India’s market is expected to reach approximately USD 0.76 billion by 2026, accounting for around 2.8% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate growth. The market is estimated to reach approximately USD 3.09 billion by 2026. Growth in the region is supported by improving access to surgical care, increasing private healthcare investment, and rising demand for elective and specialty procedures. Brazil and Mexico are the key markets, with large hospital networks, growing medical tourism, and increasing use of surgical consumables such as sutures, staplers, blades, and electrosurgical accessories. The Middle East and Africa market is also expected to grow steadily as countries continue invest in healthcare infrastructure, surgical capacity, and advanced healthcare services. The GCC countries are the primary contributors to regional growth, supported by government healthcare spending, medical tourism, private hospital expansion, and the adoption of premium surgical equipment.

GCC Surgical Equipment Market

By 2026, the GCC market is estimated to reach approximately USD 0.33 billion, representing around 1.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Expanding their Distribution Channels to Improve Their Market Position

The global surgical equipment market is moderately fragmented, with a mix of large multinational medtech companies and specialized surgical instrument manufacturers. Leading players such as Johnson & Johnson, Medtronic plc, B. Braun SE, and Stryker Corporation hold strong positions due to broad product portfolios, global distribution networks, hospital procurement relationships, and established surgeon preference.

The market includes many other players, such as Becton, Dickinson and Company, Olympus Corporation, Smith+Nephew plc, and Zimmer Biomet Holdings, Inc. These players often compete on price, local distribution strength, and product availability. Competition is strongest in sutures & staplers, electrosurgical devices, and handheld surgical instruments, where companies compete on product quality, pricing, surgeon familiarity, ergonomics, durability, safety, and availability of procedure-specific solutions. Large companies dominate premium and advanced surgical products, while regional and local manufacturers remain important in reusable handheld instruments and price-sensitive markets.

LIST OF KEY SURGICAL EQUIPMENT MARKET COMPANIES PROFILED

- Johnson & Johnson (U.S.)

- Medtronic plc (Ireland)

- Braun SE (Germany)

- Stryker Corporation (U.S.)

- Becton, Dickinson and Company (U.S.)

- Olympus Corporation (Japan)

- Smith+Nephew plc (U.K.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- CONMED Corporation (U.S.)

- Integra LifeSciences Holdings Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Olympus launched THUNDERBEAT II, a next-generation hybrid surgical energy device for hemostatic cutting and vessel sealing in laparoscopic and open surgery.

- July 2025: Medtronic received CE Mark for LigaSure RAS vessel-sealing technology on the Hugo robotic-assisted surgery system for gynecologic, general, and urologic procedures in Europe.

- June 2025: Johnson & Johnson MedTech launched the ETHICON 4000 Stapler in the U.S., designed to improve staple-line integrity and manage tissue complexity across surgical specialties.

- October 2024: Corza Medical launched Onatec ophthalmic microsurgical sutures at the American Academy of Ophthalmology conference.

- August 2024: CooperSurgical acquired obp Surgical, adding single-use cordless surgical retractors with integrated multi-LED light sources, smoke evacuation channels, and suction devices.

REPORT COVERAGE

The surgical equipment market report provides a comprehensive analysis of all market segments, outlining key growth drivers and emerging trends. The report also provides opportunities, restraints, and challenges influencing the industry. In addition, it offers detailed insights into technological advancements, major industry developments, recent product launches, market share analysis, and in-depth profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.1% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Application, End-user, and Region |

| By Product |

|

| By Application |

|

| By End-user |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 24.80 billion in 2025 and is projected to reach USD 46.60 billion by 2034.

In 2025, the market value stood at USD 10.20 billion.

The market is expected to exhibit a CAGR of 7.1% during the forecast period.

The handheld surgical devices segment leads the market by product.

The key factors driving the market is the rising number of surgical procedures.

Johnson & Johnson, Medtronic plc, B. Braun SE, and Stryker Corporation are among the top players in the market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us