Surgical Imaging Market Size, Share & Industry Analysis, By Product Type (Fluoroscopy–based Surgical Imaging Systems, CT Scanner, MRI Systems, Ultrasound Systems, and Others), By Technology (2D Imaging Systems, 3D Imaging Systems, AI-Enabled Imaging & Navigation Integration, and Others), By Application (Orthopedic & Trauma Surgery, Gastrointestinal & Abdominal Surgery, Neurosurgery, Cardiovascular & Thoracic Surgery, and Others), By End-user (Hospitals, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

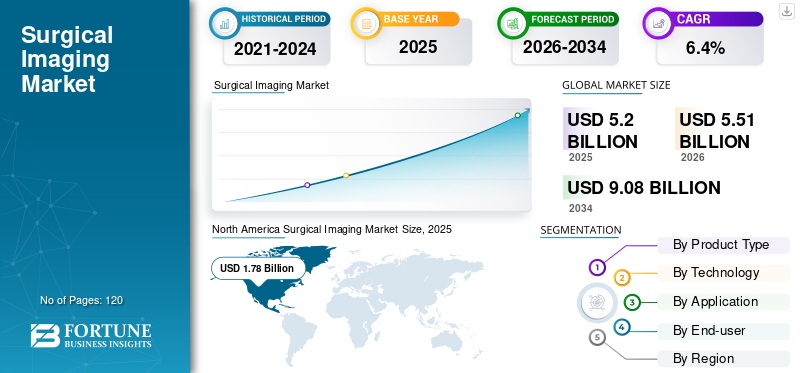

The global surgical imaging market size was valued at USD 5.20 billion in 2025. The market is projected to grow from USD 5.51 billion in 2026 to USD 9.08 billion by 2034, exhibiting a CAGR of 6.4% during the forecast period. North America dominated the global surgical imaging market with a market share of 34.23% in 2025.

The surgical imaging includes intraoperative imaging systems such as mobile and fixed C-arms, fluoroscopy units, hybrid OR solutions, and increasingly 3D & CBCT platforms that provide real-time visualization during surgery. The market’s growth is attributed to the rising demand for advanced technologies coupled with increasing shift of preference toward minimally invasive surgeries. Moreover, the market players are focusing on continuous upgradations in systems with flat-panel detectors, higher power generators, AI-supported image processing and dose optimization features to improve safety and workflow.

The market is dominated by major players, including GE HealthCare, Siemens Healthineers, Philips Healthcare, and Medtronic, among others. These players are involved in innovations and strategic initiatives to expand their market reach.

Download Free sample to learn more about this report.

Surgical Imaging Market Takeaways

- 2025 Market Size: USD 5.20 Billion

- 2026 Market Size: USD 5.51 Billion

- 2034 Forecast Market Size: USD 9.08 Billion

- CAGR: 6.4% from 2026–2034

- North America dominated the surgical imaging market with a 34.23% share in 2025.

- The 2D imaging systems segment is expected to hold a 62.7% market share in 2026.

- The orthopedic & trauma surgery segment is projected to account for 49.5% of the market in 2026.

North America

North America led the global market in 2025 with revenue of USD 1.78 billion, supported by strong adoption of advanced surgical imaging technologies.

Europe

Europe is projected to reach USD 1.38 billion by 2026, expanding at a CAGR of 5.6% during the forecast period.

Asia Pacific

Asia Pacific is expected to attain USD 1.63 billion by 2026, driven by increasing healthcare investments and rising surgical procedure volumes.

U.S.

The surgical imaging market is estimated to reach USD 1.16 billion by 2026, maintaining its position as a key contributor to regional growth.

Japan

The market is expected to witness steady growth, supported by increasing demand for advanced imaging systems and expanding healthcare infrastructure.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growing Burden of Complex Surgeries and Shift to Minimally Invasive Care Boost Market Growth

The global surgical imaging market growth is primarily driven by the rising volume of surgical procedures such as orthopedic, spine, neuro, and cardiovascular. Moreover, rising shift toward minimally invasive techniques that require precise intraoperative guidance is also projected to accelerate market growth. Surgeons increasingly rely on real-time fluoroscopy and cone-beam CT to confirm implant placement, reduce revisions and shorten hospital stays.

- For instance, according to data published by the NCBI in August 2024, the proportion of colorectal minimally invasive surgeries in Germany increased from 26.2% in 2019 to 43.7% in 2023.

MARKET RESTRAINTS

Cautious Adoption of Implant-Based POP Repair Techniques May Deter Market Growth

A key restraint for the surgical imaging market is the high upfront cost of advanced C-arms, hybrid OR imaging systems, and associated infrastructure. Many mid-size hospitals and outpatient centers continue to extend the life of legacy image-intensifier C-arms or purchase refurbished mini-C-arms rather than invest in premium flat-panel or robotic systems. In addition, companies such as Mini C Arm LLC, which refurbishes systems from leading brands and offers them to clinics and surgery centers, illustrate how cost pressure fuels a sizeable secondary market. This dynamic can delay replacement cycles and slow penetration of cutting-edge 3D and motorized systems, particularly in cost-sensitive regions.

MARKET OPPORTUNITIES

Growing Demand for AI-based and Patient Centric Systems to Provide Lucrative Growth Opportunities

The demand for advanced and intelligent tools is rising. As these systems enable workflow automation along with comprehensive analysis, the demand for such technologies is extensively rising. Moreover, healthcare facilities are seeking systems that not only capture images but also guide positioning, standardize protocols, integrate with navigation or robotics and support data-driven decision making. In addition, such systems play a prominent role in streamlining the overall operations along with multiple functionalities.

- In December 2025, GE HealthCare in collaboration with Mayo Clinic announced launch of GEMINI-RT, specifically designed for advanced cancer care.

MARKET CHALLENGES

Operational Complexity, Staffing Gaps and Integration Barriers to Pose Challenge for Market Growth

Despite strong innovation, providers face challenges around staffing, training and IT/OR integration. Advanced C-arms require skilled radiographers or OR staff to manage positioning, dose settings and 3D acquisitions, which can be difficult in environments already affected by workforce shortages.

SURGICAL IMAGING MARKET TRENDS

Rapid Transition from Legacy to Flat-panel, Motorized, and 3D Systems

A notable trend in the surgical imaging market is the transition from conventional image intensifier C-arms to flat-panel detector platforms, motorized C-arms and 3D/CBCT systems that enhance intraoperative control. Moreover, market players are launching compact systems with larger flat-panel detectors, as observed in Ziehm Imaging’s IGZO flat-panel technology. Simultaneously, advanced systems such as GE HealthCare’s OEC 3D and Siemens’ CIARTIC Move bring 3D volumes and automated positioning to routine spine and trauma workflows.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Fluoroscopy–based Surgical Imaging Systems Lead with their Extensive Range of Applications

Based on product type, the market is classified into fluoroscopy–based surgical imaging systems, CT scanner, MRI systems, ultrasound systems, and others.

To know how our report can help streamline your business, Speak to Analyst

The fluoroscopy–based surgical imaging systems segment accounted for the largest global surgical imaging market share in 2025 due to its versatility across orthopedic, trauma, cardiovascular, urology and pain management procedures. In addition, continual technological improvements coupled with advancements in flat panel technologies are also estimated to boost segment growth.

- For instance, in November 2025, Shimadzu Medical Systems USA announced launch of its new mobile C-arm with advanced functionalities.

The MRI systems segment is expected to grow at a CAGR of 8.7% during the forecast period.

By Technology

Superior Functionalities Offered by 2D Technologies Across Modalities Assists their Top Position

Based on technology, the market is sub-segmented into 2D imaging systems, 3D imaging systems, AI-enabled imaging & navigation integration, and others.

By technology, the 2D imaging systems segment accounted for the largest share in 2025 due to its extensive availability, adoption, and superior functionalities. Moreover, most mobile C-arms installed worldwide provide high-quality 2D fluoroscopy that is sufficient for fracture fixation, joint replacement and hardware verification at a lower cost. In 2026, the segment is set to hold 62.7% market share.

The AI-enabled imaging & navigation integration segment is projected to grow at a CAGR of 7.5% during the forecast period.

By Application

Considerable Prevalence of Orthopedic Conditions to Drive the Segment Growth

Based on application, the market is segmented into orthopedic & trauma surgery, gastrointestinal & abdominal surgery, neurosurgery, cardiovascular & thoracic surgery, and others.

In 2025, the orthopedic & trauma surgery was the leading application in the global market as it is directly associated with the utilization of fluoroscopy and MRI technologies for assessment of fractures and joint reconstructions. In addition, rising incidence of osteoporosis-related fractures, sports injuries and high-energy trauma are projected to offer substantial opportunity for market growth. Furthermore, the segment is set to hold a 49.5% market share in 2026.

The neurosurgery segment is projected to grow at a CAGR of 7.2% during the forecast period.

By End-user

Hospitals is the Leading End-user Owing to Availability of Advanced Infrastructure and Substantial Surgical Volumes

Based on end-user, the market is segmented into hospitals, specialty clinics, and others.

In 2025, the hospitals segment dominated and is anticipated to hold a 58.6% surgical imaging market share in terms of end-user. Hospitals lead because most surgical procedures take place in these settings. In addition, these facilities are equipped with intelligent and advanced instruments, which enables streamlining of surgical procedure.

The specialty clinics segment is projected to grow at a CAGR of 7.1% during the forecast period.

Surgical Imaging Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Surgical Imaging Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America’s market size in in 2024 was at USD 1.69 billion and maintained its leading share in 2025 by accounting USD 1.78 billion. The region’s growth is favored by rising prevalence of chronic conditions, substantial surgical volumes, and introduction of advanced technologies. In 2026, the U.S. market is estimated to reach USD 1.16 billion.

- In March 2021, GE HealthCare received FDA approval for its OEC 3D surgical imaging system, which provides both 3D and 2D imaging to support spine and orthopedic procedures.

Europe and Asia Pacific

Europe and Asia Pacific are projected to experience notable growth during the forecast period. Europe’s projected growth rate for the forecast period is 5.6% while capturing a revenue of USD 1.38 billion in 2026. The region’s robust growth is due to the presence of major players in Germany, the U.K., and France, which will capture a revenue of USD 0.31 billion, USD 0.22 billion, and USD 0.18 billion respectively in 2026.

Asia Pacific is estimated to reach USD 1.63 billion in 2026 and secure third position as in 2026, India and China are estimated to attain USD 0.36 billion and USD 0.54 billion respectively.

Latin America and the Middle East & Africa

The Latin America and the Middle East & Africa are expected to showcase moderate growth. Latin America’s market size in 2026 is expected to hit USD 0.33 billion favored by the increasing awareness of surgical care in the region. In the Middle East & Africa, the GCC is set to reach USD 0.10 billion iy 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Product Launches and Approval to Strengthen the Position of Key Players

In 2025, major players such as GE HealthCare, Siemens Healthineers, Philips Healthcare, Medtronic, and others accounted for the largest surgical imaging market share with focus on innovations and other strategic initiatives, including partnerships, acquisitions, and collaborations.

Other prominent companies, such Canon Medical Systems, Ziehm Imaging, Shimadzu Corporation, and Samsung NeuroLogica are focused on increasing product supply to emerging countries, which is expected to help them gain a significant market share.

LIST OF KEY SURGICAL IMAGING MARKET COMPANIES PROFILED

- GE HealthCare Technologies Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Medtronic plc (Ireland)

- Canon Medical Systems Corporation (Japan)

- Ziehm Imaging GmbH (Germany)

- Shimadzu Corporation (Japan)

- NeuroLogica Corp. (U.S.)

- Deerfield Imaging, Inc. (IMRIS) (U.S.)

- Stryker Corporation (U.S.)

- Olympus Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Orthoscan introduced the VERSA portable mini C-arm at AAOS 2025, featuring a compact form factor and 180° rotation.

- February 2025: FUJIFILM Healthcare Americas Corporation received contract from Defense Logistics Agency to provide surgical C-arm systems.

- March 2024: Siemens Healthineers received FDA approval for its CIARTIC Move, a self-driving mobile C-arm.

- March 2023: Koninklijke Philips N.V. announced launch of its new C-arm system called as Zenition 10.

- October 2023: Body Vision Medical reported successful validation of its AI-driven LungVision system across the Ziehm mobile C-arm portfolio, enabling advanced intraoperative imaging for bronchoscopy

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.4% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Technology, Application, Application, End-user, and Region |

|

By Product Type |

· Fluoroscopy–based Surgical Imaging Systems · CT Scanner · MRI Systems · Ultrasound Systems · Others |

|

By Technology |

· 2D Imaging Systems · 3D Imaging Systems · AI-Enabled Imaging & Navigation Integration · Others |

|

By Application |

· Orthopedic & Trauma Surgery · Gastrointestinal & Abdominal Surgery · Neurosurgery · Cardiovascular & Thoracic Surgery · Others |

|

By End-user |

· Hospitals · Specialty Clinics · Others |

|

By Geography |

· North America (By Product Type, Technology, Application, End-user, and Country) o U.S. (By Product Type) o Canada (By Product Type) · Europe (By Product Type, Technology, Application, End-user, and Country/Sub-region) o Germany (By Product Type) o U.K. (By Product Type) o France (By Product Type) o Spain (By Product Type) o Italy (By Product Type) o Scandinavia (By Product Type) o Rest of Europe (By Product Type) · Asia Pacific (By Product Type, Technology, Application, End-user, and Country/Sub-region) o China (By Product Type) o Japan (By Product Type) o India (By Product Type) o Australia (By Product Type) o Southeast Asia (By Product Type) o Rest of Asia Pacific (By Product Type) · Latin America (By Size, Procedure, End-user, and Country/Sub-region) o Brazil (By Product Type) o Mexico (By Product Type) o Rest of Latin America (By Product Type) · Middle East & Africa (By Product Type, Technology, Application, End-user, and Country/Sub-region) o GCC (By Product Type) o South Africa (By Product Type) o Rest of the Middle East & Africa (By Product Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.20 billion in 2025 and is projected to reach USD 9.08 billion by 2034.

In 2025, North Americas market value stood at USD 1.78 billion.

The market is expected to exhibit a CAGR of 6.4% during the forecast period.

The fluoroscopy–based surgical imaging systems segment led the market by product type.

The key factors driving the market are the increasing number of surgical procedures and technological advancements.

GE HealthCare, Siemens Healthineers, Philips Healthcare, and Medtronic are some of the prominent players in the market.

North America dominated the market in 2025 in terms of market share.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us