Sustainable Consulting Market Size, Share & Industry Analysis, By Service Type (Strategic Sustainability & ESG Advisory, Regulatory Compliance & Reporting, Environmental & Climate Consulting, Implementation & Operational Support, and Others), By End-User Industry (Energy & Utilities, Manufacturing & Industrial, Construction & Real Estate, Oil & Gas & Mining, Agriculture & Food & Beverage, Government & Public Sector, and Others), and Regional Forecast, 2026-2034

Sustainable Consulting Market Size and Future Outlook

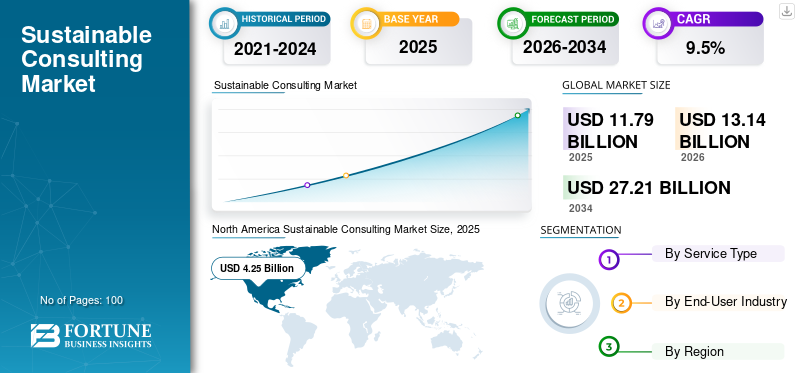

The global sustainable consulting market size was valued at USD 11.79 billion in 2025. The market is projected to grow from USD 13.14 billion in 2026 to USD 27.21 billion by 2034, exhibiting a CAGR of 9.5% during the forecast period. North America dominated the sustainable consulting market with a market share of 36.05% in 2025.

Sustainable consulting services support organizations in integrating Environmental, Social, And Governance (ESG) principles into corporate strategy, operations, reporting, and regulatory compliance. These services span sustainability strategy development, ESG risk assessment, regulatory reporting, climate advisory, and operational implementation across industries.

The market is experiencing strong growth as organizations respond to intensifying climate regulations, investor scrutiny, and stakeholder expectations around transparency and accountability. Global sustainability consulting has transitioned from a compliance-driven function to a strategic enabler of long-term value creation, resilience, and risk management. Enterprises are increasingly embedding ESG considerations into capital allocation, supply-chain management, and operational decision-making.

Leading firms such as Accenture, Deloitte, EY, PwC, KPMG, and McKinsey & Company are expanding sustainability-focused advisory capabilities, digital ESG platforms, and industry-specific climate solutions to support enterprise-scale transformation initiatives.

- For instance, in May 2024, Deloitte expanded its Global Sustainability & Climate practice, strengthening its advisory capabilities in ESG strategy, climate risk, and regulatory reporting for multinational clients.

Download Free sample to learn more about this report.

SUSTAINABLE CONSULTING MARKET TRENDS

Integration of ESG into Core Business Strategy is a Key Market Trend

A major trend shaping the sustainable consulting market is the integration of ESG considerations into core business and financial strategies rather than treating sustainability as a standalone compliance function. Companies are increasingly linking ESG performance to enterprise risk management, investment decisions, and long-term competitiveness.

In parallel, demand is rising for data-driven ESG insights supported by digital tools, scenario modeling, and climate analytics. Consulting firms are responding by combining strategic advisory with technology-enabled ESG reporting and performance management solutions.

- For instance, in 2024, EY enhanced its EY Carbon platform, enabling clients to manage emissions data, regulatory reporting, and decarbonization strategies through integrated digital workflows.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Regulatory Pressure and Investor Scrutiny Accelerating Market Growth

The sustainable consulting market growth is primarily driven by tightening global regulations related to climate disclosures, sustainability reporting, and corporate governance. Frameworks such as mandatory climate-risk disclosures and ESG reporting standards are compelling organizations to seek expert advisory support to navigate compliance requirements effectively.

In addition, investors and financial institutions increasingly incorporate ESG metrics into capital allocation decisions. This has elevated sustainability consulting from an operational necessity to a strategic priority, particularly for large enterprises and publicly listed companies.

- For instance, in 2024, PwC expanded its ESG reporting and assurance services in response to growing regulatory disclosure requirements across Europe and North America.

MARKET RESTRAINTS

High Consulting Costs and Limited Internal Alignment to Restrict Adoption

Despite rising demand, high consulting fees associated with comprehensive sustainability transformation programs can restrain adoption, particularly among small and mid-sized enterprises. Strategic ESG advisory, climate modeling, and implementation support often require long-term engagements, increasing cost sensitivity.

Limited internal alignment and unclear sustainability ownership within organizations can delay consulting engagements. Without executive-level sponsorship, sustainability initiatives may face resistance, reducing consulting effectiveness and slowing market penetration.

- For instance, industry surveys published in 2024 highlighted budget constraints as a key barrier to the adoption of ESG consulting among mid-sized enterprises.

MARKET OPPORTUNITIES

Decarbonization and Net-Zero Commitments Creating New Consulting Demand

Corporate commitments toward net-zero emissions and decarbonization targets are creating significant opportunities for sustainable consulting providers. Organizations require specialized expertise to design credible transition pathways, assess climate risks, and operationalize sustainability initiatives across value chains.

Furthermore, increasing focus on Scope 3 emissions, supply-chain sustainability, and climate resilience is expanding the scope of consulting engagements beyond reporting into execution-oriented advisory.

- For instance, in 2025, Accenture expanded its sustainability services portfolio, supporting enterprise clients with decarbonization roadmaps and operational ESG implementation.

Segmentation Analysis

By Service Type

Strategic Sustainability & ESG Advisory Leads Due to Enterprise-Wide Adoption

Based on service type, the market is segmented into strategic sustainability & ESG advisory, regulatory compliance & reporting, environmental & climate consulting, implementation & operational support, and others.

The strategic sustainability & ESG advisory segment holds the highest market share, as organizations increasingly seek long-term sustainability roadmaps aligned with business strategy, investor expectations, and regulatory requirements. These services often form the foundation for broader sustainability initiatives.

- For instance, McKinsey & Company continues to expand its sustainability strategy advisory offerings, supporting enterprise-level ESG transformation programs.

This segment is also expected to register the highest CAGR of 10.7% during the forecast period, driven by rising demand for integrated, board-level sustainability decision support.

To know how our report can help streamline your business, Speak to Analyst

By End-User Industry

Manufacturing & Industrial Sector Dominates Due to Surging Need for Supply-Chain Emission Management

Based on end-user industry, the market is segmented into energy & utilities, manufacturing & industrial, construction & real estate, oil & gas & mining, agriculture & food & beverage, government & public sector, and others.

The manufacturing & industrial segment holds the highest market share, driven by regulatory pressure, supply-chain emissions management, and energy-efficiency requirements. Manufacturers increasingly rely on sustainability consultants to optimize operations and meet compliance targets.

- For instance, in 2024, KPMG expanded its sustainability advisory services to focus on industrial decarbonization and supply-chain ESG compliance.

The energy & utilities segment is expected to grow at the highest CAGR during the forecast period, driven by the accelerating renewable energy transition and grid modernization initiatives.

Sustainable Consulting Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Sustainable Consulting Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest sustainable consulting market share, supported by early adoption of ESG frameworks, strong regulatory oversight, and high investor scrutiny. Enterprises across the region are actively integrating sustainability into their corporate strategy, financial disclosures, and risk management, driving sustained demand for strategic ESG advisory and climate consulting services. The presence of leading global consulting firms and mature capital markets further reinforces regional dominance.

U.S. Sustainable Consulting Market

The U.S. market in 2026 is estimated at around USD 3.50 billion, representing approximately 26.7% of global revenues. Growth is driven by mandatory climate and ESG disclosures, rising investor pressure, and corporate decarbonization commitments across industrial, energy, and financial sectors. Increased focus on Scope 3 emissions and supply-chain transparency is encouraging enterprises to engage sustainability consultants for long-term transformation initiatives.

Europe

Europe represents a highly regulated and mature market for sustainable consulting, driven by comprehensive climate policies, mandatory ESG reporting standards, and aggressive decarbonization targets. Organizations across industries rely heavily on consulting firms to navigate evolving regulatory frameworks, implement sustainability strategies, and manage climate-related financial risks. Europe’s leadership in sustainability regulation makes it a key revenue-generating region.

U.K. Sustainable Consulting Market

The U.K. market in 2026 is estimated at around USD 1.00 billion, representing approximately 7.6% of global revenues, driven by strong adoption of ESG reporting, climate-risk disclosures, and sustainability assurance practices. Financial services, infrastructure, and real estate sectors are major contributors to consulting demand.

Additionally, regulatory alignment with global sustainability standards continues to expand advisory opportunities.

Germany Sustainable Consulting Market

Germany’s market in 2026 is estimated at around USD 0.89 billion, accounting for approximately 6.8% of global revenues, supported by industrial decarbonization initiatives and energy-transition policies. Manufacturing firms increasingly rely on sustainability consultants to reduce emissions and align operations with EU climate regulations.

Asia Pacific

Asia Pacific is expected to register the highest CAGR of 12.9% during the forecast period, driven by rapid industrialization, infrastructure development, and increasing regulatory focus on sustainability. Enterprises across the region are expanding ESG adoption to align with global investor expectations and international supply-chain requirements. Growing awareness of climate risks and resource efficiency is accelerating consulting engagements.

Japan Sustainable Consulting Market

Japan’s market in 2026 is estimated at around USD 0.58 billion, representing approximately 4.4% of global revenues, supported by corporate governance reforms and long-term carbon neutrality commitments. Large enterprises increasingly engage sustainability consultants for climate-transition planning and ESG integration.

China Sustainable Consulting Market

China’s market in 2026 is estimated at around USD 1.04 billion, representing approximately 7.9% of global revenues, driven by industrial emissions reduction programs and expanding sustainability disclosure requirements. Consulting demand is particularly strong across manufacturing, energy, and state-linked enterprises.

India Sustainable Consulting Market

India’s market in 2026 is estimated at around USD 0.60 billion, representing approximately 4.6% of global revenues, supported by infrastructure growth, renewable energy expansion, and rising ESG awareness among corporates. Adoption of sustainability consulting is increasing across the industrial and construction sectors.

South America and Middle East & Africa

South America and the Middle East & Africa are expected to witness steady growth as sustainability frameworks and regulatory oversight continue to evolve. Infrastructure development, energy transition projects, and increasing investor scrutiny are encouraging organizations to adopt structured sustainability strategies. Consulting demand is gradually expanding beyond compliance into strategic and operational advisory.

GCC Sustainable Consulting Market

The GCC market in 2026 is estimated at around USD 0.59 billion, representing approximately 4.5% of global revenues, driven by national sustainability agendas, energy transition strategies, and large-scale infrastructure and smart city projects. Governments and enterprises increasingly engage sustainability consultants to support ESG reporting and climate-aligned development goals.

COMPETITIVE LANDSCAPE

Key Industry Players

Expansion of ESG Strategy and Digital Capabilities Strengthens Market Positioning

The sustainable consulting market is moderately consolidated, with leading firms expanding through capability enhancement, digital ESG platforms, and sector-specific solutions. Providers focus on integrating strategy, compliance, and operational execution to deliver end-to-end sustainability transformation.

- For instance, in 2024, PwC expanded its ESG advisory and assurance offerings, strengthening integrated sustainability consulting services.

LIST OF KEY SUSTAINABLE CONSULTING COMPANIES PROFILED

- Accenture plc (Ireland)

- Deloitte Touche Tohmatsu Limited (U.K.)

- Ernst & Young Global Limited (U.K.)

- PricewaterhouseCoopers International Limited (U.K.)

- KPMG International Limited (Netherlands)

- McKinsey & Company (U.S.)

- Boston Consulting Group (U.S.)

- Bain & Company (U.S.)

- ERM Group (U.K.)

- AECOM (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Accenture announced the integration of its sustainability consulting capabilities with its Accenture Sustainability Innovation Hub, expanding delivery of decarbonization roadmaps, ESG data platforms, and operational implementation services for energy and industrial clients. The initiative specifically supports enterprise-scale net-zero transformation and ESG execution programs.

- March 2025: Ernst & Young (EY) launched enhancements to its EY Climate Risk and Resilience platform, enabling clients to conduct scenario-based climate risk assessments aligned with evolving regulatory disclosure frameworks. The update supports ESG reporting, transition planning, and climate-related financial risk analysis for large enterprises.

- October 2024: PricewaterhouseCoopers (PwC) formally expanded its CSRD (Corporate Sustainability Reporting Directive) advisory and assurance services across Europe, supporting clients with end-to-end implementation of EU sustainability disclosure requirements, including data readiness, governance design, and independent assurance.

- August 2024: KPMG announced the launch of an Industrial Decarbonization & Supply Chain Sustainability Center of Excellence, focused on advising manufacturing and industrial clients on Scope 1–3 emissions reduction, ESG performance optimization, and regulatory compliance across global value chains.

- May 2024: Deloitte introduced a unified Global Sustainability Transformation Framework, combining ESG strategy, regulatory reporting, climate analytics, and operational implementation services into a single delivery model to support large enterprises executing multi-year sustainability programs.

REPORT COVERAGE

The global sustainable consulting market analysis includes a comprehensive study of market size & forecast across all key segments included in the report. It provides insights into market trends, drivers, restraints, opportunities, and challenges expected to influence market growth over the forecast period. The report also covers technological advancements in digital identity and verification platforms, compliance considerations, and key strategic developments, including partnerships and M&A activity, alongside regional insights and competitive landscape analysis. Additionally, it includes regional insights and competitive landscape analysis, highlighting the market positioning and strategic initiatives of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.5% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service Type, End-User Industry, and Region |

| By Service Type |

|

| By End-User Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 11.79 billion in 2025 and is projected to reach USD 27.21 billion by 2034.

In 2025, the market value in North America stood at USD 4.25 billion.

The market is expected to exhibit a CAGR of 9.5% during the forecast period of 2026-2034.

By end-user industry, the manufacturing & industrial segment leads the market.

Regulatory pressure and investor scrutiny are driving the market growth.

Accenture plc, Deloitte Touche Tohmatsu Limited, Ernst & Young Global Limited, PricewaterhouseCoopers International Limited, KPMG International Limited, and McKinsey & Company are among the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 100

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us