Sustainable Pharmaceutical Packaging Market Size, Share & Industry Analysis, By Material (Plastic, Glass, Paper & Paperboard, Metal, and Others), By Product Type (Bottles, Vials & Ampoules, Blister Packs, Caps & Closures, Syringes & Cartridges, Boxes & Cartons, Bags & Pouches, and Others), By End-User (Pharmaceutical Companies, Retail Pharmacies, Contract Packaging Companies, Institutional Pharmacies, and Others), and Regional Forecast, 2026-2034

Sustainable Pharmaceutical Packaging Market Size & Industry Overview

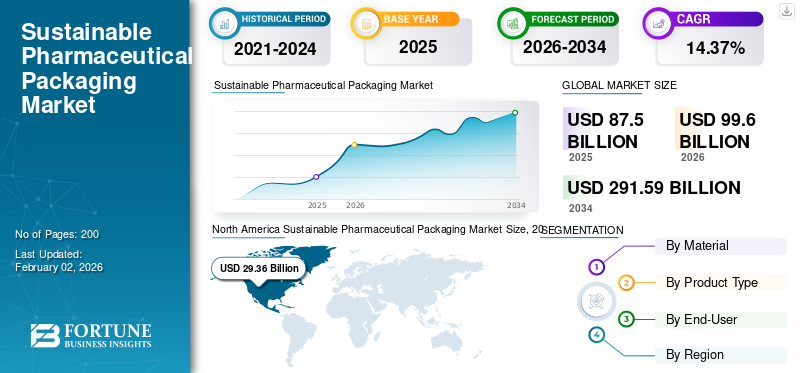

The global sustainable pharmaceutical packaging market size was valued at USD 87.50 billion in 2025 and is projected to grow from USD 99.60 billion in 2026 to USD 291.59 billion by 2034, exhibiting a CAGR of 14.37% during the forecast period. North America dominated the sustainable pharmaceutical packaging market with a market share of 33.56% in 2025.

Sustainable pharmaceutical packaging involves packaging solutions that reduce environmental and societal impact throughout their lifecycle, from sourcing raw materials to their disposal. This approach utilizes materials that can be recycled, are biodegradable, or derived from renewable resources, aiming to decrease material waste, and employs principles of a circular economy, such as reusable packaging systems.

The market includes major players such as, Gerresheimer AG, Origin Pharma Packaging, and Stoelzle Glass Group. These companies hold a leading position owing to their robust product portfolio and introduction of new sustainable packaging.

Download Free sample to learn more about this report.

Sustainable Pharmaceutical Packaging Market Key Takeaways

- 2025 Market Size: USD 87.50 billion

- 2026 Market Size: USD 99.60 billion

- 2034 Forecast Market Size: USD 291.59 billion

- CAGR: 14.37% from 2026–2034

- North America dominated the sustainable pharmaceutical packaging market with a 33.56% share in 2025.

- The plastic material segment is projected to account for 43.93% of the global market share in 2026.

- The glass material segment is expected to grow at a CAGR of 14.32% during the forecast period.

North America

North America generated USD 29.36 billion in 2025 and is projected to reach USD 33.49 billion in 2026.

Asia Pacific

Asia Pacific accounted for 26.40% of global revenue in 2025 and is expected to reach USD 26.5 billion in 2026.

Europe

Europe represented 20.57% of the global market in 2025 and is projected to reach USD 20.44 billion in 2026.

U.S.

The sustainable pharmaceutical packaging market is projected to reach USD 26.29 billion by 2026.

Japan

The sustainable pharmaceutical packaging market is estimated to reach USD 5.05 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Stringent Regulatory Frameworks are Driving Market Growth

Governments and regulatory agencies across the globe are implementing stringent regulations on packaging waste, recyclability, and carbon emissions. In the European Union, policies such as the Green Deal and Packaging Waste Regulations are compelling pharmaceutical companies to utilize recyclable and biodegradable materials. Similarly, India and China are prohibiting specific single-use plastics, which directly impacts packaging decisions. These regulatory demands are hastening the transition toward sustainable options and serve as one of the most significant catalysts for market acceptance.

MARKET RESTRAINTS

High Material and Production Costs Hampers Market Growth

One of the main factors hampering the sustainable pharmaceutical packaging market growth is the increased expense of sustainable materials when compared to traditional plastics and foils. Bio-based polymers, compostable films, and recyclable options typically necessitate exorbitant raw materials and specialized processing techniques. For pharmaceutical companies facing stringent cost pressures, particularly in the generics sector, these extra expenses can hinder widespread adoption. Although economies of scale may ultimately reduce costs, the price gap continues to be an obstacle for broad implementation in the short term.

MARKET OPPORTUNITIES

Innovation in Cold Chain and Specialty Packaging Creates Lucrative Opportunities

The expansion of biologics, cell and gene therapies, and vaccines present opportunities for eco-friendly cold chain packaging solutions. Advances in phase-change materials, reusable insulated shippers, and recyclable temperature-controlled containers are becoming increasingly sought after. This specialized yet rapidly growing sector signifies one of the most profitable opportunities within the sustainable pharmaceutical packaging industry.

MARKET CHALLENGES

Compatibility with Drug Safety and Stability Challenges Market Growth

Pharmaceutical packaging is required to maintain stability, sterility, and effectiveness of sensitive medications, particularly biologics and injectables. Numerous sustainable materials still face challenges in satisfying strict barrier property standards for protection against moisture, oxygen, and light. For instance, compostable films may deteriorate under specific storage conditions or may not possess the durability necessary for high-barrier applications such as blister packs. This lack of compatibility with drug safety regulations leads pharmaceutical companies to be cautious about substituting proven conventional packaging with innovative sustainable alternatives.

SUSTAINABLE PHARMACEUTICAL PACKAGING MARKET TRENDS

Utilization of Smart, Bio-Based, and Compostable Solutions Emerges as a Market Trend

Digitalization is converging with sustainability, resulting in packaging solutions that utilize fewer materials and incorporate smart features such as QR codes, RFID tags, and digital leaflets in place of printed inserts. This minimizes paper consumption while enhancing patient engagement and traceability, illustrating a wider trend in the pharmaceutical industry toward digital health ecosystems. The use of bio-based plastics (PLA, PHA, starch blends) and compostable films in pharmaceutical packaging is steadily increasing. These alternatives lessen dependence on fossil fuels and are becoming more prevalent in sachets, pouches, and secondary packaging cartons. Although they are presently expensive, increased production and supportive policies are making bio-based options affordable.

Download Free sample to learn more about this report.

Sustainable Pharmaceutical Packaging Market Segmentation Analysis

By Material

Remarkable Benefits Offered by the Plastic Material Propels Segment Growth

In terms of material, the market is categorized into plastic, glass, paper & paperboard, metal, and others.

The plastic material segment is projected to dominate the sustainable pharmaceutical packaging market, accounting for 43.93% of the global market share in 2026. Sustainable packaging in the pharmaceutical sector employs recyclable, biodegradable, or bio-based plastic materials to minimize environmental effects by decreasing waste, lowering carbon emissions, and reducing resource usage. Major advantages for the pharmaceutical industry consist of an enhanced corporate reputation, adherence to regulations, financial savings, improved supply chain effectiveness due to lighter packaging, and satisfying increasing consumer preferences for environmentally friendly products.

The glass material segment is expected to grow at a CAGR of 14.32% over the forecast period.

By Product Type

Bottles Segment Leads Owing to their High Usage in Pharmaceutical Sector

In terms of product type, the market is categorized into bottles, vials & ampoules, blister packs, caps & closures, syringes & cartridges, boxes & cartons, bags & pouches, and others.

The bottles segment is expected to lead the market, contributing 30.12% globally in 2026. Sustainable pharmaceutical packaging, such as bottles, is expanding quickly due to regulations, consumer preferences for sustainable alternatives, and the pharmaceutical sector's commitment to minimizing its environmental impact. Bottles are among the most adaptable packaging options in the pharmaceutical sector and are commonly utilized for solid dosage forms (tablets and capsules), liquid formulations (syrups and suspensions), and powdered medications. Their capacity to hold various drug types, volumes, and dosage specifications makes them a preferred option for manufacturers. This adaptability guarantees that bottles continue to be a leading packaging choice, even as new alternatives such as blister packs or prefilled syringes gain popularity.

Moreover, innovation in materials such as plant-based PLA (Polylactic Acid) and a greater application of Post-Consumer Resin (PCR) are driving the demand for bottles, along with a move toward lighter designs and the embrace of "reduce, reuse, recycle" strategies.

- Notable instances include Bayer's implementation of environmentally-conscious PET blister packaging and Innovative Bottles Inc.'s employment of PLA vials, both of which contribute to lowering carbon emissions and conserving resources.

The vials and ampoules product type segment is expected to grow at a CAGR of 14.84% over the forecast period.

By End-User

Pharmaceutical Companies’ Increased Adoption of Sustainable Packaging Bolsters its Growth

Based on end-user, the market is segmented into pharmaceutical companies, retail pharmacies, contract packaging companies, institutional pharmacies, and others.

The pharmaceutical companies end-user segment will remain the largest category, accounting for 37.51% of the global market share in 2026.

Pharmaceutical companies are progressively embracing sustainable packaging in response to stringent environmental regulations. In the European Union, the Packaging and Packaging Waste Directive states that packaging be recyclable and plastic use be minimized, while the U.S. FDA is incorporating sustainability considerations into its packaging assessments. Similarly, India and China have started prohibiting non-recyclable plastics. These regulations are compelling pharmaceutical companies to rethink their packaging designs (blisters, bottles, cartons) in favor of recyclable, bio-based, or compostable options, thereby accelerating their adoption throughout the sector.

To know how our report can help streamline your business, Speak to Analyst

In addition, the retail pharmacies segment is projected to grow at a CAGR of 14.63% during the study period.

Sustainable Pharmaceutical Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America Sustainable Pharmaceutical Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America contributed 33.56% to the global market in 2025, with a valuation of USD 29.36 billion, and is projected to reach USD 33.49 billion in 2026. In North America, especially in the U.S. and Canada, the primary catalyst for sustainable pharmaceutical packaging is the ESG commitments made by major pharmaceutical companies. Industry leaders such as Pfizer, Johnson & Johnson, and Moderna are facing significant pressure from both investors and consumers to showcase their climate responsibility. Regulations, including the waste management guidelines set by the U.S. Environmental Protection Agency (EPA) and various state-level plastic reduction laws (in California), further encourage this transition. The U.S. market is projected to reach USD 26.29 billion by 2026.

Additionally, healthcare providers and retail pharmacy chains such as CVS and Walgreens are advocating for eco-friendly packaging, generating demand throughout the supply chain. There is a higher level of patient awareness regarding sustainability compared to many other areas, making it an important factor for reputation as well.

In 2025, the U.S. market is estimated to reach USD 20.14 billion.

Asia Pacific

Asia Pacific and Europe, are estimated to attain notable growth over the projected timeframe. The Asia Pacific market was valued at USD 23.1 billion in 2025, capturing 26.40% of global revenue, and is estimated to reach USD 26.5 billion in 2026. During the forecast period, Asia Pacific sustainable pharmaceutical packaging market is projected to record a growth rate of 15.16%, which is the second highest amongst all the regions, and touch the valuation of USD 23.10 billion in 2025. In the region, the rise of eco-friendly pharmaceutical packaging is fueled by significant growth in pharmaceutical manufacturing and government initiatives aimed at sustainability. India and China, which are among the biggest producers of generic medications, are advocating for a reduction in single-use plastics in accordance with their national environmental policies.

Japan

The Japan market is estimated to reach USD 5.05 billion by 2026, the China market is projected to reach USD 8.69 billion by 2026, and the India market is estimated to reach USD 7.04 billion by 2026.

Europe

Europe accounted for USD 18 billion in 2025, representing 20.57% of the global market share, and is projected to reach USD 20.44 billion in 2026. In Europe, the sustainable pharmaceutical packaging market share will witness exponential growth. Strict regulatory standards largely influence the market. The EU Green Deal, along with the Packaging and Packaging Waste Directive (PPWD), requires that packaging be recyclable, lighter, and use less plastic, compelling pharmaceutical companies to rethink their packaging designs. Germany, France, and the U.K. have national sustainability objectives, driving faster change.

The UK market is estimated to reach USD 3.78 billion by 2026 and the Germany market is projected to reach USD 4.48 billion by 2026.

Middle East & Africa and Latin America

Over the years, the growth in the Middle East & Africa and Latin America is set to be moderate. The market in Middle East & Africa reached USD 7.29 billion in 2025, representing 8.33% of total market revenue, and is projected to reach USD 8.16 billion in 2026. In 2025, the Latin America market stood at USD 9.74 billion, representing 11.14% of global demand, and is projected to grow to USD 11.01 billion in 2026 as multinational pharmaceutical firms are implementing their sustainability pledges to their operations in Latin America, which speeds up implementation even when local regulations are not rigorously enforced. Increased urbanization and the expanding middle-class appetite for over-the-counter medications also present prospects for the growth of sustainable packaging solutions.

In the Middle East & Africa, South Africa is set to attain the value of USD 2.08 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Companies Maintain their Leading Position with Novel Product Offering and Strong R&D

The global sustainable pharmaceutical packaging market holds a mix of several small and mid-size companies and showcases a semi-consolidated structure. Some of these companies operate globally and implement strategies including, collaborations, partnerships, and product innovation to expand geographic reach. Gerresheimer AG, Origin Pharma Packaging, and Stoelzle Glass Group are some of the leading firms aiming to reducing plastic waste. These firms focus on cementing their market position by introducing sustainable pharmaceutical packaging products, strong distribution networks, and partnerships. Moreover, Nipro Corporation, SGD Pharma, and SCHOTT are gaining popularity by making investments in R&D and joining forces with pharmaceutical companies.

LIST OF KEY SUSTAINABLE PHARMACEUTICAL PACKAGING COMPANIES PROFILED

- Gerresheimer AG (Germany)

- Origin Pharma Packaging (U.K.)

- Stoelzle Glass Group (Austria)

- Nipro Corporation (Japan)

- SGD Pharma (France)

- SCHOTT (Germany)

- OLIVER (U.S.)

- Amcor plc (Switzerland)

- West Pharmaceutical Services, Inc. (U.S.)

- Corning Incorporated (U.S.)

- CCL Healthcare (Canada)

- Sonoco Products Company (U.S.)

- Bormioli Pharma S.p.A (Italy)

- LOG (Israel)

- Cosmo Films (India)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Aptar Pharma revealed a breakthrough in eco-friendly pharmaceutical packaging, as its Freepod nasal spray pump is now manufactured using mass balance bio-based resins. This pump, utilized in Haleon's Otrivin brand offerings, is noted to be the first Aptar delivery system globally to be commercialized with these materials, according to the companies.

- August 2025: With PharmaGuard, a recyclable blister packaging solution made from PP, SÜDPACK Medica has initiated a significant advancement toward sustainability in the pharmaceutical sector. However, this is only the beginning. The film manufacturer is already working on the forthcoming iterations of its innovative packaging systems that merge sustainability with outstanding quality and dependability.

- October 2024: Bayer introduced a groundbreaking polyethylene terephthalate (PET) blister packaging for its well-known Aleve brand in the healthcare sector. Developed in collaboration with packaging expert Liveo Research, this cutting-edge solution decreases the carbon footprint of the packaging by 38%. It represents a significant advancement in environmental responsibility by removing polyvinyl chloride (PVC) from the equation.

- February 2024: Gerresheimer, a forward-thinking provider of systems and solutions and a worldwide collaborator for the pharmaceutical, biotechnology, and cosmetics sectors, is excited to reveal that its eco-friendly packaging solution, which features the Gx Amsterdam glass jar paired with a bio-based forewood closure, has been chosen for the introduction of a groundbreaking cosmetic product by the German start-up 4peoplewhocare.

- October 2023: Stoelzle Pharma, a leading global manufacturer of high-quality primary glass packaging, declared the launch of its new PharmaCos Line. The PharmaCos line features a wide variety of glass jars, offered in sizes from 5 ml to 500 ml, all in amber with a screw neck design. PharmaCos distinguishes itself by concentrating on the Nutra- and Cosmeceutical industries, where sustainability holds great significance.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2024 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.37% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Product Type, End-User, and Region |

|

By Material |

|

|

By Product Type |

|

|

By End-User |

|

|

By Geography |

North America (By Material, Product Type, End-User, and Country)

Europe (By Material, Product Type, End-User, and Country/Sub-region)

Asia Pacific (By Material, Product Type, End-User, and Country/Sub-region)

Latin America (By Material, Product Type, End-User, and Country/Sub-region)

Middle East & Africa (By Material, Product Type, End-User, and Country/Sub-region)

|

Frequently Asked Questions

The global sustainable pharmaceutical packaging market size is projected to grow from USD 99.60 billion in 2026 to USD 291.59 billion by 2034, exhibiting a CAGR of 14.37% during the forecast period.

In 2025, the market value of North America stood at USD 29.36 billion.

The market is expected to exhibit a CAGR of 14.37% during the forecast period of 2026-2034.

The bottles segment led the market by product type.

The key factors driving the market growth are the stringent regulatory frameworks.

Gerresheimer AG, Origin Pharma Packaging, Stoelzle Glass Group, Nipro Corporation, SGD Pharma, and SCHOTT are some of the prominent players in the market.

North America dominated the market in 2024.

An increase in demand from the pharmaceutical sector is one of the factors that is expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us