Tandem Solar Cell Market Size, Share & Industry Analysis, By Type (Perovskite-Silicon Tandem, III-V on Silicon Tandem, CIGS/Perovskite Tandem, and Others), By Cell Architecture (2-Terminal (2T) and 4-Terminal (4T)), By Module (Rigid and Flexible/Lightweight), By Application (Residential, Commercial, Utility, and Others), Regional Forecast, 2026-2034

Tandem Solar Cell Market Size and Future Outlook

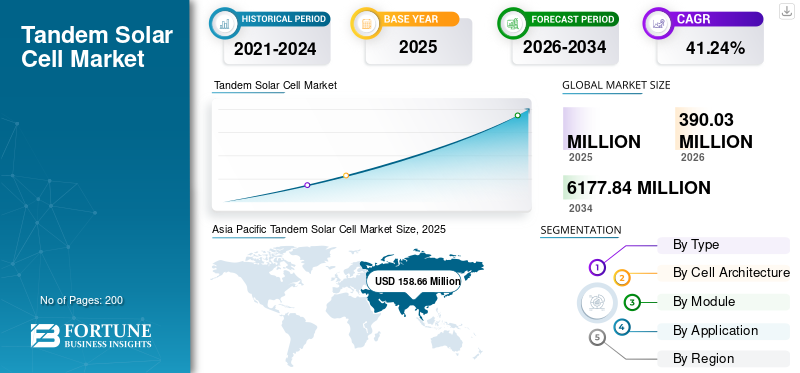

The global tandem solar cell market size is projected to grow from $390.03 million in 2026 to $6,177.84 million by 2034, exhibiting a CAGR of 41.24%Tandem solar cells are advanced solar panel technologies that use multiple layers to increase energy conversion efficiency beyond conventional designs. Typically, a high-bandgap material, such as perovskite materials, is layered on top of a conventional silicon cell, enabling more efficient utilization of solar energy compared to single-junction cells. This architecture significantly improves power conversion efficiency, with laboratory results already exceeding 30%, surpassing the theoretical limits of traditional silicon-based modules.

Tandem cells are gaining attention due to their compatibility with existing silicon manufacturing infrastructure and their potential to reduce the levelized cost of electricity (LCOE) over time. A key driver for the product adoption is the growing demand for higher energy output per unit area, particularly in utility-scale and space-constrained installations. As land availability becomes a critical constraint and solar deployment accelerates globally, higher-efficiency modules offer a practical solution to maximize energy generation without expanding the footprint. This efficiency advantage makes tandem technology increasingly attractive for next-generation solar projects.

- For instance, in May 2023, Oxford PV announced the commercial production of its perovskite-silicon tandem solar modules at its Brandenburg facility in Germany. The company reported that its tandem cells achieved efficiencies exceeding conventional silicon modules, marking a key step toward large-scale commercialization. This milestone demonstrated the viability of integrating perovskite silicon tandem solar cells layer into existing manufacturing processes for next-generation solar technologies.

Some of the leading companies operating in the tandem solar cell industry include Oxford PV, LONGi Green Energy Technology Co., Ltd., Trina Solar Co., Ltd., JinkoSolar Holding Co., Ltd., and others. Oxford PV is a leading solar technology company focused on developing and commercializing perovskite-silicon tandem solar cells to achieve higher efficiencies than conventional PV modules. The company is known for pioneering the integration of perovskite materials into existing silicon manufacturing processes, with early commercial production underway in Germany.

Download Free sample to learn more about this report.

Tandem Solar Cell Market Key Takeaways

- 2026 Market Size: USD 390.03 million

- 2034 Forecast Market Size: USD 6,177.84 million

- CAGR: 41.24% from 2026–2034

- Asia Pacific dominated the market with a value of USD 158.66 million in 2025.

- The flexible/lightweight segment is projected to grow at the fastest CAGR of 43.03% during the forecast period.

- The III-V on silicon tandem segment is anticipated to expand at a CAGR of 40.70% over the study period.

North America

The market reached USD 39.45 million in 2025 and is projected to reach USD 55.97 million in 2026.

Asia Pacific

The market reached USD 158.66 million in 2025, driven by strong manufacturing expansion and photovoltaic production capabilities.

Europe

The market reached USD 49.69 million in 2025 and is projected to grow at a 41.29% CAGR during the forecast period.

U.S.

The market reached USD 35.37 million in 2025.

Japan

The market reached USD 19.69 million in 2025.

Read More

TANDEM SOLAR CELL MARKET TRENDS

Scaling of Tandem Solar Cells into Mainstream Manufacturing Ecosystems is the Key Market Trend

A key trend in the market is the gradual integration of tandem architectures into established photovoltaic manufacturing ecosystems. Rather than building entirely new production systems, manufacturers are adapting existing fabrication lines to accommodate additional layers and advanced deposition techniques. This shift is enabling faster industrial adoption while minimizing capital expenditure barriers. Equipment suppliers and material developers are aligning their innovations to support high-throughput tandem production, improving uniformity, yield, and long-term reliability.

Furthermore, collaborations between research institutions and manufacturers are accelerating the transfer of lab-scale breakthroughs into scalable processes. This trend reflects a broader transition from experimental development toward industrial maturity, where process optimization, supply chain readiness, and manufacturing standardization are becoming central to competitiveness in the tandem solar cell landscape.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Investment and Policy Support for Next-Generation Solar Technologies to Drive Market Growth

A major driver for tandem solar cells is the growing global investment and policy support aimed at accelerating next-generation photovoltaic technologies. Governments and public institutions are actively funding research, pilot manufacturing, and early commercialization to diversify solar technology pathways. For instance, in September 2023, the U.S. Department of Energy (DOE) announced additional funding under its Solar Energy Technologies Office to advance perovskite and tandem PV durability and scalability.

Similarly, the European Commission, through its Horizon Europe program (2022–2024), has supported multiple projects focused on scaling tandem solar technologies. In Asia, China’s national energy strategy, 2023, emphasized high-efficiency solar innovation, encouraging leading manufacturers to invest in tandem production lines. These coordinated efforts are reducing technological risks, improving bankability, and accelerating the transition from pilot to commercial deployment.

MARKET RESTRAINTS

Material Stability and Long-Term Durability Challenges to Hamper Market Demand

A key restraint for tandem solar cells is the challenge of ensuring long-term material stability and durability under real-world operating conditions. Unlike conventional silicon modules, tandem cells, especially those using perovskite layers, are more sensitive to environmental factors such as moisture, heat, and ultraviolet exposure. For instance, the National Renewable Energy Laboratory (NREL) highlighted in June 2023 that maintaining performance over 20-25 years remains a critical hurdle for perovskite-based tandem devices.

These durability concerns impact investor confidence and slow large-scale adoption, particularly in utility projects where long-term reliability is essential. Until advancements in material engineering and protective technologies are fully commercialized, concerns around lifespan and performance consistency act as a restraint on product adoption.

MARKET OPPORTUNITIES

Growing Role of Advanced PV Technologies in Urban Energy Systems to Present Excellent Market Opportunities

A significant opportunity for tandem solar cells lies in their expanding applicability across emerging and specialized solar markets that require higher performance and design flexibility. As solar deployment extends beyond traditional ground-mounted systems, there is increasing demand for technologies that can operate efficiently under diverse conditions, such as partial shading, high temperatures, and limited installation space.

For instance, initiatives led by the International Energy Agency (IEA) in 2023 highlighted the growing role of advanced PV technologies in urban energy systems and distributed generation. Additionally, sectors such as building-integrated photovoltaics (BIPV), agrivoltaics, and mobility applications are creating new avenues where lightweight and high-efficiency tandem modules can offer distinct advantages.

MARKET CHALLENGES

Scaling Manufacturing Processes While Maintaining Yield and Cost Efficiency Presents Challenges for Market Growth

A major challenge for tandem solar cells is scaling manufacturing processes from pilot lines to high-volume production while maintaining consistent yield and cost efficiency. The integration of multiple semiconductor layers introduces additional complexity in deposition, alignment, and defect control compared to conventional single-junction modules.

For instance, in 2023, the International Technology Roadmap for Photovoltaics (ITRPV) highlighted that uniform large-area coating and process reproducibility remain critical hurdles for tandem technologies. Minor variations during fabrication can significantly impact performance and module reliability, leading to yield losses. Additionally, the need for new materials, specialized equipment, and process optimization increases production complexity, thereby hindering the tandem solar cell market growth.

Segmentation Analysis

By Type

Perovskite-Silicon Tandem Segment Dominates as it is Compatible with Existing Silicon Manufacturing Infrastructure

Based on type, the market is classified into Perovskite-Silicon Tandem, III-V on Silicon Tandem, CIGS/Perovskite tandem, and others. Perovskite-silicon tandem solar cells dominate primarily due to their ability to integrate seamlessly with the well-established global silicon photovoltaic manufacturing ecosystem. This compatibility allows manufacturers to upgrade existing production lines rather than invest in entirely new facilities, reducing capital expenditure and accelerating commercialization. Additionally, the combination leverages the maturity, reliability, and large-scale availability of silicon with the high absorption efficiency of perovskite materials.

The III-V on silicon tandem segment is experiencing the highest growth and is expected to grow at a CAGR of 40.70% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Cell Architecture

2-Terminal (2T) Segment Dominates Due to their Simpler Architecture

Based on cell architecture, the market is classified into 2-Terminal (2T) and 4-Terminal (4T).

2-Terminal (2T) capture the major tandem solar cell market share primarily due to their simpler architecture and better compatibility with large-scale manufacturing processes. In this design, the sub-cells are electrically connected in series within a single structure, allowing the device to operate using standard module configurations and inverters. This reduces system complexity compared to 4-terminal designs, which require separate electrical connections and additional components. Furthermore, 2T architectures enable easier integration into existing silicon production lines, supporting faster commercialization and cost efficiency.

The 4-Terminal (4T) segment is expected to grow at a CAGR of 39.45% during the forecast period.

By Module

Rigid Segment Dominates Due to Its Properties

On the basis of the module, the market is classified into rigid and flexible/lightweight.

Rigid modules dominate the tandem solar cell market due to their strong alignment with existing solar deployment infrastructure and proven long-term reliability. Most global solar installations, particularly in utility-scale and commercial projects, are designed for glass-based rigid modules, making integration of tandem technology more straightforward without requiring major system redesign. These modules offer superior mechanical strength, environmental resistance, and longer operational lifetimes, which are critical for large-scale energy generation projects.

The flexible/lightweight segment is expected to grow at a CAGR of 43.03% during the forecast period.

By Application

Utility Segment Dominated the Market Due to its Ability to Leverage the high efficiency of Tandem Technology at Scale

On the basis of application, the market is classified into residential, commercial, utility, and others. The utility segment dominates the market due to its ability to leverage the high efficiency of tandem technology at scale. Large solar parks require maximum energy generation per unit area, making high-efficiency modules more economically attractive. Tandem solar cells help improve overall project output, which directly enhances revenue generation for utility developers. Additionally, utility-scale projects have greater financial capacity to adopt emerging technologies compared to residential or small commercial users.

The commercial batteries segment is expected to grow at a CAGR of 40.81%.

Tandem Solar Cell Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Asia Pacific Tandem Solar Cell Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the third-highest share in 2025, valued at USD 39.45 million, and also maintained its significant share in 2026 with USD 55.97 million. The growth of the market in the region is driven by a strong innovation ecosystem supported by government funding and policy incentives. The region benefits from advanced research infrastructure, with institutions such as national laboratories and universities actively working on next-generation photovoltaic technologies. In addition, policy frameworks such as clean energy tax credits and funding programs are encouraging the development and commercialization of high-efficiency solar solutions.

U.S. Tandem Solar Cell Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 35.37 million in 2025, accounting for roughly 13.15% of the global market sales.

Europe

Europe is projected to record a growth rate of 41.29% in the coming years, which is the second-highest among all regions, reaching a valuation of USD 49.69 million in 2025. Europe is a key region driving the advancement of the product due to its strong research foundation and early-stage commercialization efforts. The region hosts leading research institutes and collaborative innovation platforms that focus on improving the efficiency, scalability, and stability of tandem technologies. The region hosts leading research institutes and collaborative innovation platforms that focus on improving the efficiency, scalability, and stability of tandem technologies.

Germany Tandem Solar Cell Market

Germany’s market in 2025 stood around USD 14.70 million 2025 and is estimated at around USD 21.59 million by 2026, representing roughly 5.47% of the global revenues.

Asia Pacific

Asia Pacific reached USD 158.66 million in 2025, securing the largest share of the market. In the region, India reached USD 12.29 million in 2025. The region is emerging as the primary manufacturing and scale-up hub for the product, driven by China’s rapid transition from pilot lines to industrial production. Leading manufacturers are integrating tandem architectures into existing high-volume silicon fabs, enabling faster commercialization. Japan and South Korea continue to contribute through advanced material research, while India is positioning itself as a future high-demand adoption market supported by domestic manufacturing initiatives.

Japan Tandem Solar Cell Market

The Japanese market in 2025 stood at around USD 19.69 million, accounting for roughly 7.32% of global revenues. Japan is advancing tandem solar cells through strong perovskite research led by institutions and companies such as Panasonic and the University of Tokyo. The country is also focusing on lightweight and flexible tandem modules suited for urban and building-integrated applications.

China Tandem Solar Cell Market

China’s market is projected to be significant worldwide, with 2025 revenues standing at around USD 99.48 million, representing roughly 37.00% of the global sales.

Australia Tandem Solar Cell Market

The Australian market in 2025 stood at around USD 4.86 million, accounting for roughly 1.81% of global revenues.

Latin America

Latin America is expected to witness moderate growth in this market during the study

period. The Latin American market reached a valuation of USD 13.46 million in 2025.

The region is emerging as a high-potential deployment market for tandem solar cells, driven by strong utility-scale solar expansion in countries such as Brazil and Chile. Adoption is expected to accelerate as costs decline, with the region primarily relying on imported high-efficiency modules.

Brazil Tandem Solar Cell Market

Brazil's market stood around USD 7.27 million in 2025, representing roughly 2.70% of global revenues.

Middle East & Africa

The Middle East & Africa region is expected to witness significant growth in this market during the forecast period. The Middle East & Africa market reached a valuation of USD 7.64 million in 2025. The region is witnessing growing interest in tandem solar cells due to large-scale solar projects and high irradiance conditions, particularly in GCC countries. Adoption is expected to rise post-2030 as the region seeks higher efficiency technologies for mega utility-scale installations.

GCC Tandem Solar Cell Market

The GCC market stood at around USD 3.77 million in 2025, representing roughly 1.40% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Major players are Focusing on Collaborations to Increase their Global Market Share

The global tandem solar cell market holds a consolidated market structure, constituting prominent players such as Oxford PV, LONGi Green Energy Technology Co., Ltd., Trina Solar Co., Ltd., and others. Companies operating in the industry are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in November 2023, LONGi announced a breakthrough in perovskite-silicon tandem solar cell efficiency, achieving over 33% in laboratory conditions in collaboration with research institutions. The company also highlighted its roadmap to scale tandem technology through pilot production lines in China. This development reflects LONGi’s strategic focus on integrating tandem architectures into its existing high-volume silicon manufacturing ecosystem to accelerate commercialization.

Other key players in the global market include Hanwha Qcells, First Solar, Inc., CubicPV, and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY TANDEM SOLAR CELL COMPANIES PROFILED

- Oxford PV (U.K.)

- LONGi Green Energy Technology Co., Ltd. (China)

- Trina Solar Co., Ltd. (China)

- JinkoSolar Holding Co., Ltd. (China)

- Hanwha Qcells (South Korea)

- First Solar, Inc. (U.S.)

- CubicPV (U.S.)

- Meyer Burger Technology AG (Switzerland)

- Panasonic Corporation (Japan)

- Tandem PV, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2024: CubicPV announced plans to scale its perovskite-silicon tandem solar technology, supported by investments aimed at establishing pilot manufacturing capabilities in the U.S. The company is focusing on combining high-efficiency tandem cells with advanced silicon wafer technologies. This initiative is expected to accelerate the transition from laboratory-scale innovation to early-stage commercial production.

- December 2023: JinkoSolar announced its progress in developing tandem solar cell technology, focusing on enhancing efficiency and durability through advanced material engineering. The company reported ongoing research into perovskite-based tandem structures as part of its long-term innovation strategy. JinkoSolar is leveraging its global manufacturing expertise to explore the future integration of tandem cells into next-generation photovoltaic modules.

- October 2023: Trina Solar revealed advancements in its tandem solar cell program, achieving high-efficiency perovskite–silicon cells exceeding 30% in lab tests. The company emphasized ongoing pilot-scale production and collaboration with academic partners to improve stability and scalability. Trina is actively working to align tandem technology with its module manufacturing platforms, aiming for gradual integration into commercial product lines.

- September 2023: Hanwha Qcells expanded its research into tandem solar technologies, focusing on perovskite–silicon integration to achieve higher efficiencies. The company highlighted investments in R&D facilities in South Korea and Germany to advance next-generation PV technologies. This initiative aligns with its strategy to develop high-performance modules and maintain competitiveness in the evolving solar market.

- August 2023: First Solar announced research initiatives exploring tandem solar cell architectures, particularly integrating perovskite layers with its thin-film technology platforms. The company emphasized its focus on improving efficiency while maintaining long-term durability. These efforts are part of First Solar’s broader strategy to expand beyond conventional thin-film modules into next-generation photovoltaic technologies.

REPORT COVERAGE

The global tandem solar cell market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 41.24% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Type, Cell Architecture, Module, Application, and Region |

| By Type |

|

| By Cell Architecture |

|

| By Module |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 268.89 million in 2025 and is projected to reach USD 6,177.84 million by 2034.

In 2025, the market value stood at USD 158.66 million.

The market is expected to exhibit a CAGR of 41.24% during the forecast period.

The utility segment leads the market by application.

Increasing investment and policy support for next-generation solar technologies are the key factors driving the market.

Oxford PV, LONGi Green Energy Technology Co., Ltd., and Trina Solar Co., Ltd. are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us