Tangential Flow Filtration Market Size, Share & Industry Analysis By Product Type (Instruments [Single-use and Reusable] and Accessories), By Technology (Ultrafiltration, Microfiltration, Nanofiltration, and Others), By Application (Final Product Processing [API Filtration, Protein Purification, Vaccine & Antibody Processing, and Others], Raw Material Filtration [Media & Buffer Filtration, Prefiltration, and Others], Cell Separation, and Others), By End User (Pharmaceutical & Biotechnology Companies, Contract Development & Manufacturing Organizations (CDMOs)), & Regional Forecast, 2026-2034

Tangential Flow Filtration Market Overview

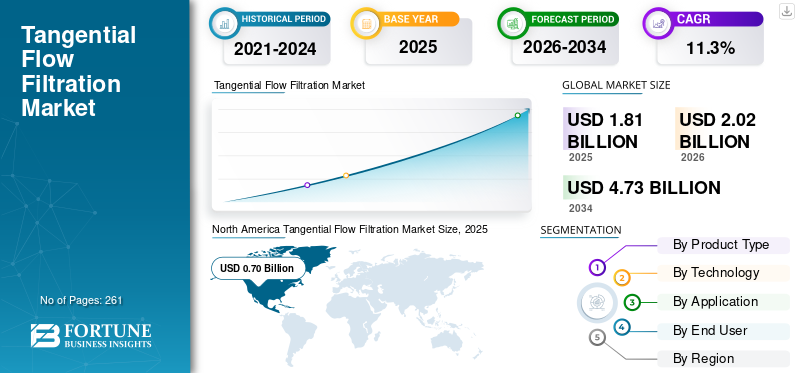

The tangential flow filtration market size was valued at USD 1.81 billion in 2025 and is projected to grow from USD 2.02 billion in 2026 to USD 4.73 billion by 2032, exhibiting a CAGR of 11.3% during the forecast period. North America dominated the tangential flow filtration market with a market share of 38.67% in 2025.

Tangential flow filtration is a specialized technique in the field of bioprocessing and purification, enabling the separation, concentration, and purification of particles and biomolecules in solution. The increasing biologics, biosimilars, vaccines, and cell & gene therapy manufacturing, increasing adoption of tangential flow filtration in downstream processing, and the growing healthcare spending are resulting in growing demand for these devices in the market.

- For instance, according to the 2024 data published by Science Direct, about 13 novel cell and gene therapies received approval by the U.S. FDA, China's NMPA, the E.U. EMA, and Japan's PMDA.

Furthermore, the rising incorporation of technological advancements in these devices among the major players, such as Danaher Corporation and Sartorius AG, among others, is further contributing to the demand for these devices in the market.

Download Free sample to learn more about this report.

Tangential Flow Filtration Market Key Takeaways

- 2025 Market Size: USD 1.81 billion

- 2026 Market Size: USD 2.02 billion

- 2032 Forecast Market Size: USD 4.73 billion

- CAGR: 11.3% from 2025-2032

- North America dominated the tangential flow filtration market with a 38.67% share in 2025.

- The ultrafiltration segment held the largest share of 55.3% in 2025.

- The instruments segment is projected to grow at a CAGR of 11.5% during the forecast period.

North America

North America reached USD 0.70 billion in 2025 and maintained its position as the leading regional market.

Europe

Europe is projected to reach USD 0.54 billion in 2026, supported by strong biopharmaceutical manufacturing activities.

Asia Pacific

Asia Pacific is estimated to reach USD 0.54 billion in 2026, making it the third-largest regional market.

U.S.

The market is estimated at USD 0.69 billion in 2026, accounting for approximately 34.2% of global revenues.

Japan

The market is estimated at USD 0.12 billion in 2026, representing around 5.9% of global revenues.

Read More

Tangential Flow Filtration Market Trends

Shift toward Single-Use TFF Devices is Emerging Market Trend

The market is witnessing a preferential shift from reusable stainless-steel TFF technology toward single use technologies, especially in biosimilars, biologics, vaccines, and advanced therapy manufacturing. Single use tangential flow systems require reduced cleaning, sterilization, and validation, further lowering cross-contamination risk and enabling faster batch changeovers in multi-product facilities.

Additionally, there is an increasing demand for these devices in CDMOs, cell and gene therapies, clinical-scale manufacturing, and biomanufacturing facilities focusing on multiple products or smaller batch sizes. The companies are prioritizing closed processing, faster setup, and operational flexibility, further fueling the adoption rate of these devices in the market.

- In April 2023, Sartorius AG highlighted that its single-use TFF flow kits provide faster turnaround, reduced cleaning validation, and minimized bioburden risk and product carryover in multi-product settings.

Other Prominent Trends

- Automation and digital integration in filtration

- Development of high-efficiency membranes

- Increasing outsourcing of bioprocessing

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Increasing Biologics, Vaccines, Biosimilars, and Cell & Gene Therapy Manufacturing Fuels Market Growth

There is a growing development of biosimilars, biologics, vaccines, and advanced therapies among the pharmaceutical and biotechnology companies. TFF is mainly used in bioprocessing for concentration, diafiltration, buffer exchange, and purification of advanced biomolecules, such as recombinant proteins, monoclonal antibodies, viral vectors, and nucleic acid-based therapies.

- For instance, according to 2023 data published by the National Center for Biotechnology Information (NCBI), about 55 new drugs were approved by the Food and Drug Administration in 2023.

This, along with the expansion of biotech research and rising demand for purification technologies, is further augmenting the adoption rate of such devices in the market. Therefore, the factors above, along with the rising focus of key companies on introducing R&D activities to launch novel systems, are expected to boost the tangential flow filtration market growth.

Market Restraints

High Upfront Cost of Automated TFF Systems and Membranes to Hamper Market Growth

The high cost associated with automated tangential flow filtration systems and recurring membrane expenses is hampering the adoption, especially among small pharmaceutical companies, academic labs, early-stage biosimilar developers, and companies in developing countries. Furthermore, automated TFF devices require membrane filters, pressure sensors, pumps, software, holders, scales, and other accessories, which increases the initial capital expenditure. Additionally, TFF membranes and cassettes are product-contact devices that require frequent replacement and single-use disposal, adding to the financial burden.

- For instance, according to the data published by the RTP Scientific Supply, the cost of the KrosFlo kR2i TFF System ( Repligen) with Pump, Scale, Pressure Valve & Controller is USD 14,500.0

Market Opportunities

Expansion of Contract Development and Manufacturing Organization (CDMO) is a Potential Market Opportunity

There is a rapid expansion of healthcare facilities in developing countries, including China, Mexico, and others. The growing research and development activities, rising outsourcing among the companies, growing number of Contract Development And Manufacturing Organizations (CDMO) are consequently increasing the adoption of tangential flow filtration in these settings. TFF systems are mainly used in CDMO settings for diafiltration, concentration, buffer exchange, and purification of recombinant proteins, monoclonal antibodies, viral vectors, and other biologics. The CDMOs' facilities are also investing in new biologics capacity, single-use manufacturing facilities, and multi-product facilities, resulting in growing demand for automated and single-use TFF systems globally.

- In January 2025, Samsung Biologics, a global contract development and manufacturing organization (CDMO), opened Bio Campus II and launched Antibody-Drug Conjugate (ADC) services.

Market Challenges

Infrastructure Gaps in Developing Countries to Limit Market Growth

There is a growing demand for biopharmaceutical manufacturing, biologics development, and vaccine production among the patient population. However, challenges with skilled workforce availability, healthcare funding, cold-chain systems, advanced manufacturing facilities, regulatory compliance requirements, and access to high-cost biologics are limiting the adoption of these devices in emerging countries. These challenges are hampering the local demand for sophisticated filtration technologies, including automated and single-use TFF systems.

Moreover, a limited number of pharmaceutical and biotechnology companies, lack of healthcare spending among others, are some of the vital factors, resulting in limited adoption of novel devices, especially in emerging nations, such as China, Brazil, and others.

- For instance, according to 2025 statistics published by the International Trade Administration (ITA), the healthcare spending is USD 135.0 billion in Brazil.

Other Prominent Challenges

- Membrane fouling and maintenance issues

- Complex process optimization

SEGMENTATION ANALYSIS

By Product Type

Increasing Prevalence of Catheter Based Infections Led to the Accessories Segment Dominance

Based on the product type, the market is classified into instruments and accessories. Instruments are further classified into single use and reusable.

To know how our report can help streamline your business, Speak to Analyst

The accessories segment held the largest revenue share in 2025. This growth is due to increasing prevalence of catheter based infection among patients, resulting in a rising demand for accessories worldwide. This, coupled with the growing focus of key companies on launching novel accessories, is further anticipated to contribute to the the segment growth.

- For instance, according to a 2024 study published by PLOS, the prevalence of CAUTI was 8.7% in the study population, which comprised a total of 377 patients.

The instruments segment is expected to grow at a CAGR of 11.5% over the forecast period.

By Technology

Increasing Approval of Biologics and Biosimilars Led to the Dominance of the Ultrafiltration Segment

Based on technology, the market is segmented into ultrafiltration, microfiltration, nanofiltration, and others.

The ultrafiltration segment dominated the global market in 2025 with a share of 55.3%. The growth is due to the increasing approval for biologics and biosimilars, resulting in a growing demand for novel devices with ultrafiltration technology, thereby supporting the adoption rate of these devices in the market.

- For instance, as of April 2026, the U.S. FDA has approved more than 80 biosimilars, reflecting the increasing manufacturing base for biologics that commonly require ultrafiltration and other techniques during downstream processing.

The nanofiltration segment is set to flourish with a growth rate of 12.7% across the forecast period.

By Application

Increasing Demand in Downstream Processing Led to Dominance of Final Product Processing Segment

Based on application, the market is segmented into final product processing, raw material filtration, cell separation, and others. Final product processing is further divided into API filtration, protein purification, vaccine & antibody processing, and others. Additionally, raw material filtration is classified into media & buffer filtration, prefiltration, and others.

The final product processing segment dominated the global market in 2025 with a share of 51.2%. The growth is due to the growing adoption of TFF in diafiltration, concentration, buffer exchange, and purification of final biologic drug substances and intermediates.

- For instance, according to 2024 data published by the Food and Drug Administration (FDA), the U.S. FDA’s CBER approved multiple biological license applications, including cell therapy products, vaccines, allergenic products, and other biologics, contributing to the demand for downstream/final processing technologies.

The segment of cell separation is set to flourish with a growth rate of 12.4% across the forecast period.

By End-user

Increasing Number of Pharmaceutical & Biotechnology Companies Led to Segmental Dominance

Based on end user, the market is bifurcated into pharmaceutical & biotechnology companies, contract development and manufacturing organizations (CDMOs), and others.

The pharmaceutical & biotechnology companies segment dominated the market in 2025. The increasing growing R&D activities, rising approval for biosimilars and biologics, growing number of pharmaceutical & biotechnology companies, among others, are some of the crucial factors supporting the growth the segment in the market. Furthermore, the segment is set to hold an 59.3% share in 2026.

- For instance, according to 2026 statistics published by Cross River Therapy, it was reported that there are about 5,000 pharmaceutical companies in the U.S.

Contract development and manufacturing organizations (CDMOs) segment are projected to grow at a 11.9% CAGR during the forecast period.

Tangential Flow Filtration Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Tangential Flow Filtration Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 0.63 billion, and also took the leading share in 2025 with USD 0.70 billion. The growing approval for biologics, increasing healthcare spending, and advanced healthcare infrastructure, among others, are some of the factors contributing to the regional growth.

- For instance, according to 2024 statistics published by the Centers for Medicare & Medicaid Services (CMS), the healthcare spending is around USD 15,474 per person in the U.S.

U.S. Tangential Flow Filtration Market

Based on North America’s strong contribution, the U.S. market can be analytically approximated at around USD 0.69 billion in 2026, accounting for roughly 34.2% of global sales.

Europe

Europe is projected to record a growth rate of 10.0% in the coming years, which is the second highest among all regions, and reach a valuation of USD 0.54 billion by 2026. The growing outsourcing of manufacturing services and increasing CDMOs are likely to support the market growth.

U.K. Tangential Flow Filtration Market

The U.K. market in 2026 is estimated at around USD 0.10 billion, representing roughly 4.7% of global revenues.

Germany Tangential Flow Filtration Market

Germany’s market is projected to reach approximately USD 0.13 billion in 2026, equivalent to around 6.2% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 0.54 billion in 2026 and secure the position of the third-largest region in the market. The fast growth in R&D activities and increasing healthcare expenditure are likely to support the growth of the market.

Japan Tangential Flow Filtration Market

The Japan market in 2026 is estimated at around USD 0.12 billion, accounting for roughly 5.9% of global revenues. Japan has historically reported a growing approval for biologics, biosimilars, and vaccines, resulting in rising demand for innovative devices.

China Tangential Flow Filtration Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.17 billion, representing roughly 8.4% of global sales.

India Tangential Flow Filtration Market

The India market size in 2026 is estimated at around USD 0.09 billion, accounting for roughly 4.2% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.09 billion in 2026. The growth is due to the gradual growth tied to public healthcare investment in the region. The Middle East & Africa are also expected to grow due to rising acquisitions and mergers among other companies to strengthen their presence in the market. In the Middle East & Africa, the GCC is set to reach a value of USD 0.03 billion in 2026.

South Africa Tangential Flow Filtration Market

The South Africa market is projected to reach around USD 0.02 billion in 2026, representing roughly 0.8% of global revenues.

Competitive Landscape

Key Industry Players

Increasing Number of Device Launches to Enhance Market Competition

A robust and diversified product portfolio, along with a significant focus on inorganic growth strategies globally, is one of the key factors contributing to the dominance of key companies in the market. Danaher Corporation and Sartorius AG are major companies in the market. Moreover, the growing focus of key companies on novel device launches is likely to strengthen their presence, further contributing to substantial tangential flow filtration market share.

- For instance, in September 2024, Sartorius AG launched Vivaflow SU, setting a new standard for laboratory-dedicated tangential flow filtration. Designed for enhanced ease of use and flexibility, Vivaflow SU ensures more efficient and sustainable ultrafiltration and diafiltration processes for feed volumes ranging from 100 to 1,000 mL.

Other key players, including Merck KGaA and others, are also growing in the market, primarily due to their growing focus on acquisitions and collaborations among other players to strengthen their presence in the market.

List of Key Tangential Flow Filtration Companies Profiled

- Danaher Corporation (U.S.)

- Sartorius AG (Germany)

- Merck KGaA (Germany)

- Repligen Corporation (U.S.)

- PARKER HANNIFIN CORP (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Asahi Kasei Corporation (Japan)

- Cobetter (China)

- Yocell Biotechnology (Qingdao) Co., LTD. (China)

- GEA Group Aktiengesellschaft (Germany)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Repligen Corporation, a life sciences company focused on bioprocessing technology, participated in the J.P. Morgan 2026 Healthcare Conference. This helped the company to increase its presence.

- July 2025: Repligen Corporation, a life sciences company focused on bioprocessing technology, partnered with Novasign to develop and integrate Novasign’s machine learning and modeling workflow into Repligen filtration systems.

- June 2025: PARKER HANNIFIN CORP attended a webinar 10 Ways to be More Agile in Your TFF Processing to help biopharmaceutical manufacturers transform tangential flow filtration.

- November 2023: Repligen Corporation, a life sciences company focused on bioprocessing technology leadership, launched TangenX SC, the industry’s holder-free, self-contained Tangential Flow Filtration (TFF) device.

- April 2023: Repligen Corporation acquired FlexBiosys Inc. The acquisition is another step in building out Repligen’s Fluid Management franchise, adding a full range of single-use bioprocessing bags and assemblies to our product offering.

- November 2022: Alfa Laval launched the MultiSystem to help manufacturers optimise processes and enhance flexibility in production lines.

- November 2021: Donaldson Company, Inc., a provider of innovative filtration products and solutions, acquired Solaris Biotechnology Srl., a manufacturer of bioprocessing equipment, including bioreactors, fermenters and tangential flow filtration systems with an aim to increase its brand presence.

REPORT COVERAGE

The report provides a detailed tangential flow filtration market analysis and focuses on key aspects such as leading companies and market segmentation, including product type, technology, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Technology, Application, End User, and Region |

| By Product Type |

|

| By Technology |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1.81 billion in 2025 and is projected to reach USD 4.73 billion by 2034.

In 2025, the North America market value stood at USD 0.70 billion.

Growing at a CAGR of 11.3%, the market will exhibit steady growth over the forecast period (2026-2034).

By product type, the accessories segment is the leading segment in this market.

The introduction of novel tangential flow filtration is one of the major factors driving the market's growth.

Danaher Corporation and Sartorius AG are the major players in the global market.

North America dominated the market share.

The growing approval for biologics and biosimilars drive the adoption of these products.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us