Thin Film Drugs Market Size, Share & Industry Analysis, By Drug Type (Oral Thin Film Drugs and Transdermal Thin Film Drugs), By Disease Indication (Schizophrenia, Migraine, Opioid Dependence, and Others), By Distribution Channel (Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

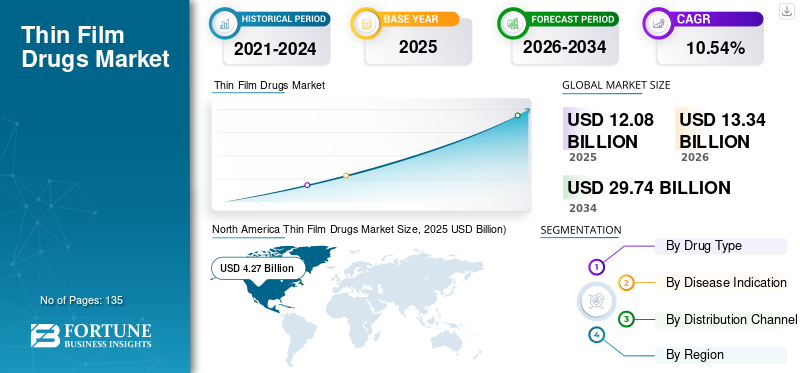

The global thin film drugs market size was USD 12.08 billion in 2025 and is projected to grow from USD 13.34 billion in 2026 to USD 29.74 billion in 2034 at a CAGR of 10.54% during the 2026-2034 period. North America dominated the thin film drugs market with a market share of 35.36% in 2025.

Thin-film drug delivery is an upcoming form of drug administration that is an advanced alternative to traditional forms such as capsules, tablets, and liquids. This emerging drug delivery system is currently being researched by pharmaceutical companies around the globe as a novel form of drug administration tool. Pharmaceutical and pharmacological properties of the drug have to be extensively researched to develop the formulation of a thin film. This kind of drug delivery has proved beneficial in individuals who have trouble swallowing tablets and experience nausea or vomiting. The upcoming drug delivery method is gaining traction due to its fast dissolving nature and increasing patent life cycle of existing products. Additionally, the currently dissolving dental buccal film drugs are also gaining popularity in the industry.

The COVID-19 pandemic negatively impacted the thin film drugs market. The sudden outbreak of COVID-19 in various countries across the world significantly impacted research and development initiatives. The increased focus on developing medicines and vaccines against COVID-19 led to this disruption in R&D activities. However, the growth of sales of the thin-film drug remained unchanged during the pandemic. Companies such as Zim Laboratories experienced a slight dip in sales revenue in the first two quarters of 2020. However, the company's revenue was regained and showed significant improvement in the next half of 2020. Furthermore, the manufacturing capabilities of the companies increased in 2022 with the ease of the COVID guidelines and an increase in the prescriptions for the thin films. Thus, the market is expected to grow during the forecast period.

Download Free sample to learn more about this report.

Global Thin Film Drugs Market Overview

Market Size:

- 2025 Value: USD 12.08 billion

- 2026 Value: USD 13.34 billion

- 2034 Forecast Value: USD 29.74 billion, with a CAGR of 10.54% from 2026–2034

Market Share:

- North America dominated the thin film drugs market with a share of 35.36% in 2025 due to high awareness, large patient base for neurological conditions, and strong adoption of novel delivery systems.

- By disease indication, schizophrenia segment is projected to generate USD 6.55 billion in revenue by 2025.

- By distribution channel, hospital pharmacy segment is expected to hold a 45.25% share in 2026.

Key Country Highlights:

- Japan: Thin film drugs market expected to reach USD 905.9 million by 2025

- China: Projected to witness a strong CAGR of 11.50% during the forecast period

- Europe: Anticipated to grow at a CAGR of 10.7% during the forecast period

Thin Film Drugs Market Trends

Focus on Mergers, Acquisitions, and Collaborations by Key Players is a Vital Trend

The thin film drugs market has a significant growth potential in the forthcoming years owing to the increasing adoption of the drug type. Key players recognize this market potential, and they are actively engaging in the expansion of research and development to gain more share. For instance, in September 2019, XPhyto Therapeutics (now Bionxt Solutions) closed the acquisition of Vektor Pharma TF GmbH. With this acquisition, XPhyto now owns all the developmental drugs, such as thin-film therapeutics, particularly transdermal patches developed by Vektor Pharma.

In addition to this, in February 2019, EsoCap AG collaborated with Therapy-Systeme AG for the industrial development of thin film drug technologies for upper gastrointestinal tract diseases. Such partnerships by prominent companies tend to boost the growth of the market during the forecast period.

Download Free sample to learn more about this report.

Thin Film Drugs Market Growth Factors

Increasing Research and Development in Thin Film Drugs to Augment Market Growth

The global market is driven by various factors. However, the predominant aspect that is estimated to drive the market is the advancements in this novel drug delivery. Various companies around the globe are focusing on investment in this emerging form of drug delivery owing to a rise in popularity. Key startup companies are particularly focusing on thin-film drug delivery routes for cannabis-based drugs.

For instance, XPhyto Pharma is currently developing 13 drugs utilizing the thin film drug delivery method. As of February 2021, all of its products are currently in Phase II clinical trials in European countries. At present, the generic form of Rivastigmine is being evaluated by XPhyto Pharma in Phase 2 clinical trial to treat Alzheimer’s. Another factor anticipated to influence the market's growth is adopting thin-film drug delivery methods to extend the patent of key molecules by major players in the market.

Additionally, the rise in the regulatory approvals for thin film drugs for various disease indications is propelling the growth of the market.

- For instance, in April 2023, the U.S. Food and Drug Administration approved the new drug application for rizatriptan benzoate oral thin film formulation under the brand name Rizafilm to be used for the treatment of migraine.

Rising Geriatric Population to Propel the Market Growth

The rising adoption of thin-film therapeutics among the older population of the world is increasing owing to the ease of administration of such therapeutics. As a result, key players are also focusing on these drug delivery methods for diseases such as Parkinson’s and Alzheimer’s predominant in the geriatric population. Hence, an increase in the geriatric population worldwide could tremendously benefit the market's growth in the upcoming years. According to the World Population Prospects, one in six people will be over 65 in 2050 compared to one in 11 in 2019.

Additionally, the rising incidence of neurological conditions such as Parkinson’s disease is propelling the adoption of thin film drugs.

- For instance, according to the Parkinson's Foundation, in 2022, nearly 90,000 people are diagnosed with Parkinson’s disease in the U.S. annually, and the incidence of disease increases in people aged 65 and older.

RESTRAINING FACTORS

Limited Penetration and Research in Emerging Countries to Hamper Growth

The market is currently dominated by regions populated with developed countries such as the U.S., Germany, and Japan. Due to the high cost associated with thin-film drug development, there is currently limited adoption and research in drug delivery in evolving economic countries such as China, India, and Brazil. The development of thin-film therapeutics requires higher investment and funding, which seems to be lacking in companies operating in developing countries, such as Brazil, India, and China.

Thin Film Drugs Market Segmentation Analysis

By Drug Type Analysis

Oral Thin Film Drugs Segment Held the Highest Market Share in 2023

Based on drug type, the market is categorized into oral thin film (OTF) drugs and transdermal film drugs.

The global oral thin film therapeutics segment led the market accounting for 55.62% market share in 2026. This is attributed to the higher revenue sales generated by these drugs in the market by key players. The segment is also anticipated to witness considerable growth during 2024-2032 owing to the increasing number of pipeline products under development that will be launched in the market in the upcoming years. Innovations in buccal cavity oral thin films drugs are also estimated to boost the thin film drugs market growth.

Furthermore, the increase in research and development initiatives for new product launches by key market players in the oral thin film category is expected to boost the segmental growth over the forecast period.

- For instance, in July 2023, the National Institute of Singapore’s Department of Pharmacy researchers developed easy-to-use oral films that will provide painless, efficient, and discreet drug delivery.

To know how our report can help streamline your business, Speak to Analyst

The transdermal thin film drugs segment generated a lower share in 2023. However, upcoming therapies focusing on transdermal thin film delivery is projected to bolster the demand for the product in the near future. Transdermal thin film delivery development, especially in the domain of pain management, is estimated to benefit the drug type significantly in the upcoming years.

By Disease Indication Analysis

Schizophrenia Segment to Garner Maximum Share during the Forecast Period

Based on the disease indication, the market is segmented into schizophrenia, migraine, opioid dependence, and others.

The market was predominantly dominated by the schizophrenia and migraine segments in 2026. The growth of the segment is augmented due to the increasing prevalence of schizophrenia and increasing adoption of the drug delivery is highly adopted in patients suffering from schizophrenia. Owing to underlying factors such as the difficulty in swallowing tablets and liquids, fast absorption of the drug into the mucosal membrane, and ease of administration. By disease indication, the schizophrenia segment is projected to generate USD 6.55 billion in revenue by 2025. The schizophrenia segment dominated the market accounting for 54.21% market share in 2026.

- For instance, in January 2022, according to the data published by the World Health Organization (WHO), 24.0 million people globally are impacted with schizophrenia, or 1 out of 300 individuals in every country.

The drug delivery type is also popular among patients suffering from migraine attributed to its effectiveness and quick action to relieve pain.

By Distribution Channel Analysis

Retail Pharmacy Segment Dominated the Market in 2023

Based on the categorization of distribution channels, the market of thin film drugs was segregated into retail pharmacies, hospital pharmacies, and others. In 2026, By distribution channel, the hospital pharmacy segment is projected to lead the market with a 45.25% share.

The retail pharmacy segment dominated portion in the global thin film drugs market share in 2023. The factors influencing the dominance of this segment were the higher availability of drug products through retail channels. The majority of products under the thin film drug delivery model are generic molecules and are hence widely available in the retail pharmacy. However, the increasing adoption of online pharmacy and mail order pharmacy is expected to drive the growth of the others segment in the market.

REGIONAL INSIGHTS

North America

North America Thin Film Drugs Market Size, 2025 USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America region captured 35.36% of the global market in 2025, generating USD 4.27 billion in revenue, and is expected to reach USD 4.7 billion in 2026. The growth is attributable to the adoption of thin-film drugs in the region. Additionally, the increasing prevalence of schizophrenia in developed countries such as the U.S. is estimated to augment the market growth in the region in the upcoming years. According to various published sources, 1 in every 10,000 individuals in the U.S. is diagnosed with schizophrenia. This is attributed to the higher awareness and larger diagnosis rate of the disease indication in the country. Combined with this, a similar trend in the rise of neurological disorders such as Parkinson’s disease and Alzheimer’s is witnessed in the United States of America. The U.S. market is projected to reach USD 4.45 billion by 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 3.22 billion in 2025, accounting for 26.62% share, and is expected to reach USD 3.56 billion in 2026. The growth of the market in Europe is influenced by various factors such as the increasing prevalence of Parkinson’s disease. Additionally, the larger research and development activities on thin-film drugs are estimated to propel the market growth in countries of the European region. Combined with this, the higher government funding for innovative drug delivery models is anticipated to drive the market in the upcoming years positively. Europe is anticipated to grow at a CAGR of 10.7% during the forecast period. The UK market is projected to reach USD 0.47 billion by 2026, while the Germany market is projected to reach USD 0.73 billion by 2026.

Asia-Pacific

In 2025, Asia Pacific generated USD 2.64 billion, contributing 21.88% to global market revenue, and is expected to reach USD 2.95 billion in 2026. Meanwhile, Asia-Pacific market is projected to witness stable growth during the forecast period. Factors such as the presence of a larger geriatric patient pool and growing healthcare spending and infrastructure supplement the growth of the market in this region. The increasing awareness of thin-film therapeutics is anticipated to drive the market during the forecast period. The Japan market is projected to reach USD 1.01 billion by 2026, the China market is projected to reach USD 0.67 billion by 2026, and the India market is projected to reach USD 0.33 billion by 2026.

- The thin film drugs market in Japan is expected to reach USD 905.9 million by 2025.

- China is projected to witness a strong CAGR of 11.50% during the forecast period.

Middle East & Africa and Latin America

Middle East & Africa recorded a market size of USD 0.72 billion in 2025, capturing 5.97% of the global market share, and is expected to reach USD 0.79 billion in 2026. The Latin America market generated USD 1.23 billion in 2025, representing 10.17% of the global market landscape, and is expected to reach USD 1.34 billion in 2026. The countries of Latin America and the Middle East & Africa are continually engaging in augmenting the access to treatment options to their citizens. Moreover, substantial developments in the public and private healthcare sectors are likely to increase the growth of the market in these regions.

List of Key Companies in Thin Film Drugs Market

The Market is Semi Consolidated with Only Five Major Players

The global market shows moderate competition, with key companies such as Pfizer, Inc., Novartis AG, Aquestive Therapeutics, AbbVie Inc., and ZIM Laboratories Limited leading the market. A strong pipeline of molecules, mergers, acquisitions, and innovative product launches are chief strategies adopted by these key market players to gain higher customer reach. Other players involved in the market are Sumitomo Dainippon Pharma Co.Ltd., IntelGenx Corp, Wolters Kluwer, and Bionxt Solutions, among others.

LIST OF KEY COMPANIES PROFILED:

- Pfizer, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- ZIM Laboratories Limited (India)

- Novartis AG (Switzerland)

- Aquestive Therapeutics (U.S)

- Sumitomo Dainippon Pharma Co. Ltd. (Japan)

- IntelGenx Corp (Canada)

- Bionxt Solutions (Canada)

KEY INDUSTRY DEVELOPMENTS:

- September 2023: DifGen Pharmaceuticals LLC launched Suboxone (Buprenorphine/ Naloxone) oral sublingual/ buccal film in the US market.

- June 2021: Shilpa Medicare Ltd. launched paracetamol oral thin film under the brand name Molshil. The first of its kind with pediatric dose.

- June 2020: Zim Laboratories received the U.S. patent from the United States Patent and Trademark Office for its oral thin film formulation.

- September 2020: XPhyto Pharma (now Bionxt Solutions) announced the advancement of an oral disintegrating drug development program in the human bioavailability study. The company announced the results are expected by the end of the first quarter of 2021.

REPORT COVERAGE

The market research report provides qualitative and quantitative insights on the industry and detailed analysis with market size and growth rate for all possible market segments. Along with this, it provides an elaborative analysis of the market dynamics and competitive landscape. Various key market insights provided in the report are the number of key industry developments, key industry trends, pipeline analysis, regulatory scenario, and analysis of COVID-19 on the global market, among others.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.54% from 2026 to 2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Drug Type

|

|

By Disease Indication

|

|

|

By Distribution Channel

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 13.34 billion in 2026 and is projected to reach USD 29.74 billion by 2034.

In 2025, the North American market value stood at USD 4.27 billion.

The market will exhibit a significant CAGR of 10.54% during the forecast period (2026-2034).

The oral segment dominated the global market in 2026.

The increasing research and development in thin-film drugs is projected to drive the growth of the market.

Pfizer, Inc., Novartis AG, Aquestive Therapeutics, Allergan plc., and ZIM Laboratories Limited are the major players in the global market.

North America dominated the market in terms of share in 2026.

New product launches are expected to drive the adoption of thin-film therapeutics.

- 2021-2034

- 2025

- 2021-2024

- 135

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us