Concrete Formwork Market Size, Share & Industry Analysis, By Material Type (Timber & Plywood, Aluminum, Steel, and Others), By End Use (Residential, Commercial, Industrial, and Infrastructure), and Regional Forecast, 2026-2034

Concrete Formwork Market Size and Future Outlook

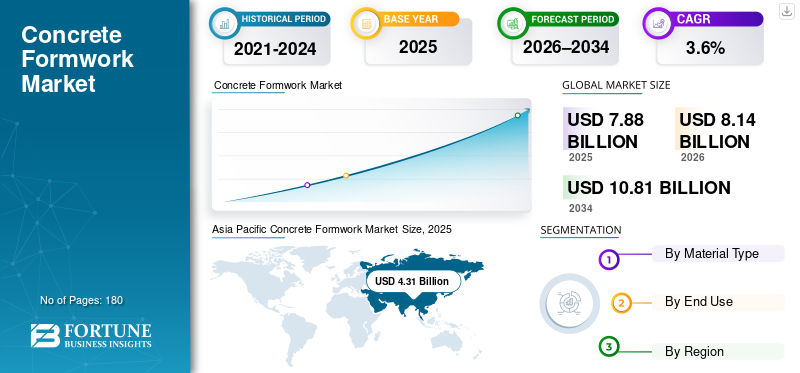

The global concrete formwork market size was valued at USD 7.88 billion in 2025. The market is projected to grow from USD 8.14 billion in 2026 to USD 10.81 billion by 2034, exhibiting a CAGR of 3.6% during the forecast period. Asia Pacific dominated the concrete formwork market with a market share of 54.7% in 2025.

Concrete formwork systems are critical construction frameworks used to mold, support, and stabilize concrete structures during curing. They directly influence structural accuracy, surface finish quality, construction speed, labor efficiency, and overall project economics. Formwork solutions are widely applied across residential and commercial buildings, industrial facilities, and large-scale infrastructure projects such as bridges, tunnels, metros, and highways. As construction activity increasingly shifts toward high-rise, repetitive, and time-sensitive projects, demand continues to move from conventional site-built formwork toward engineered, reusable, and modular systems.

Steady urbanization, infrastructure modernization programs, and growing emphasis on construction productivity, worker safety, and lifecycle cost optimization drive the market. While growth remains moderate, formwork demand is structurally resilient due to its indispensable role in reinforced concrete construction.

The global concrete formwork market is shaped by manufacturers with strong expertise in construction engineering, material durability, and modular system design, supported by rental-based distribution models and on-site technical services. Leading companies such as PERI Group, Doka Group, ULMA Construction, MEVA, and RMD Kwikform maintain strong market positions through comprehensive product portfolios spanning timber, aluminum, and steel formwork systems. These players benefit from global project experience, close collaboration with EPC contractors, and the ability to deliver customized solutions for high-rise buildings and infrastructure megaprojects.

Download Free sample to learn more about this report.

CONCRETE FORMWORK MARKET TRENDS

Rising Shift toward Modular, Reusable, and High-Cycle Formwork Systems is a Key Market Trend

Construction contractors are increasingly adopting engineered advanced formwork systems that enable faster assembly, improved dimensional accuracy, and multiple reuse cycles across projects. Aluminum and steel systems are gaining traction due to their durability, consistent performance, and suitability for repetitive high-rise and infrastructure construction. At the same time, improved plywood treatments are extending the lifespan of timber-based formwork, maintaining its relevance in cost-sensitive residential applications. This shift aligns with broader construction industry priorities focused on reducing labor dependency, shortening construction cycles, minimizing material waste, and improving job-site safety, especially in urban and large-scale developments.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Urban Construction and Infrastructure Investment Sustains Formwork Demand

Steady growth in urbanization, population-driven residential projects, and government-led infrastructure investment programs is strengthening demand for concrete formwork systems across both developed and emerging economies. Residential housing developments, commercial buildings, transportation infrastructure, and public utilities rely heavily on reinforced concrete construction, making formwork an essential input throughout the project lifecycle. As cities expand vertically and infrastructure projects become more complex, contractors increasingly prioritize formwork systems that support high load capacities, faster turnaround times, and consistent concrete finishes. Aforementioned factors are set to drive the global concrete formwork market growth during the forecast period.

- According to the National Institute of Securities Markets (NISM), India's urban infrastructure needs an investment of USD 840 billion by 2036 to create a conducive environment for market growth.

MARKET RESTRAINTS

High Initial System Costs and Rental Dependence Limit Wider Adoption

Advanced aluminum and steel formwork systems require a higher upfront capital investment than traditional timber-based solutions. While these systems offer superior durability and reuse efficiency, cost sensitivity among small contractors and low-rise residential builders continues to limit penetration in price-driven markets. Additionally, the market’s heavy reliance on rental-based business models can constrain supplier margins and limit adoption in regions with underdeveloped rental infrastructure. Logistics complexity, system availability, and project-specific customization requirements can further restrict deployment, particularly in fragmented construction markets.

MARKET OPPORTUNITIES

Infrastructure Megaprojects and High-Rise Construction Create Long-Term Growth Potential

Large-scale infrastructure developments, including metro rail networks, highways, bridges, and urban transit systems, present significant growth opportunities for advanced concrete formwork solutions. These projects demand high structural precision, fast construction cycles, and robust safety performance, favoring engineered steel and aluminum systems. Additionally, rapid growth in high-rise residential and mixed-use developments across Asia Pacific and the Middle East is increasing demand for climbing, self-climbing, and modular formwork systems that reduce crane dependency and labor intensity. Suppliers capable of delivering integrated engineering support and customized solutions are well-positioned to capture these high-value opportunities.

- For instance, GCC countries are investing nearly USD 1 trillion in transformative, large-scale megaprojects, primarily driven by Saudi Arabia's Vision 2030 and the UAE's urban master plans to diversify economies.

Segmentation Analysis

By Material Type

Timber & Plywood Led Market Share Due to Cost-Effectiveness and Broad Residential Use

Based on material type, the market is segmented into timber & plywood, aluminum, steel, and others.

The timber & plywood segment accounted for the largest global concrete formwork market share in 2025, driven by its widespread use in residential construction and small-to-medium commercial projects. Timber formwork remains preferred due to its low initial cost, ease of handling, adaptability to varied shapes, and availability across regions. Improved plywood treatments and coatings have enhanced durability, allowing moderate reuse while maintaining cost advantages.

Aluminum formwork is the fastest-growing material segment, registering a CAGR of 3.9% during 2026–2034, driven by its lightweight properties, high reuse cycles, and suitability for repetitive high-rise construction. Aluminum systems enable faster assembly, reduced labor requirements, and improved surface finishes, making them increasingly attractive for mass housing and urban development projects.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Residential Construction Dominated as Urban Housing Demand Accelerates

By end use, the market is segmented into residential, commercial, industrial, and infrastructure.

The residential segment accounted for the largest share in 2025, supported by continuous demand for housing driven by urban population growth and government-backed affordable housing initiatives. Residential construction relies heavily on formwork solutions for slabs, walls, columns, and foundations, with both timber and aluminum systems widely deployed depending on project scale and budget.

The commercial segment is expected to grow at a CAGR of 3.5% over the forecast period, driven by the steady development of office, retail, hospital, and educational facilities. Meanwhile, infrastructure construction, growing at a 3.3% CAGR, remains a critical demand driver due to ongoing investments in transportation and public works.

The industrial sector is a major driver of demand for advanced concrete formwork systems, primarily due to the need for high-speed, high-strength, and repeatable construction in projects such as factories, warehouses, and power plants. As industrial construction shifts toward faster, cost-effective methods, demand is rising for engineered, modular, and reusable systems over traditional, labor-intensive timber methods.

Concrete Formwork Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America and the Middle East & Africa.

Asia Pacific

Asia Pacific Concrete Formwork Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global concrete formwork market in 2025, reaching USD 4.31 billion, and is expected to maintain its leadership in 2026 with USD 4.45 billion. The region’s dominance is driven by large-scale residential construction, infrastructure expansion, and rapid urbanization across China, India, and Southeast Asia. High-volume housing developments and infrastructure megaprojects continue to support strong demand for modular and reusable formwork systems.

China Concrete Formwork Market

China is expected to reach USD 2.44 billion in 2026, representing around 30% of global demand, supported by extensive urban housing projects and infrastructure modernization.

India Concrete Formwork Market

India is expected to reach USD 0.72 billion in 2026, driven by residential expansion, metro rail development, and government-led infrastructure initiatives.

North America

North America reached USD 1.42 billion in 2025, supported by stable residential demand, commercial renovation activity, and infrastructure rehabilitation. The U.S. remains the dominant market due to large-scale construction projects and the adoption of engineered formwork systems. Government initiatives to address aging transportation networks, bridges, tunnels, and metro rail projects are driving demand for durable, large-scale formwork solutions.

U.S. Concrete Formwork Market

The U.S. market is expected to reach USD 1.29 billion in 2026, accounting for roughly 16% of global revenues.

Europe

Europe reached USD 1.28 billion in 2025 and is expected to rise at a CAGR of 3.0% over the forecast period. Demand is supported by commercial construction, infrastructure upgrades, and strict safety and quality standards that favor engineered formwork systems. Moreover, increasing focus on eco-friendly, reusable, and durable formwork solutions is driving market adoption.

Germany Concrete Formwork Market

Germany is expected to reach USD 0.28 billion in 2026, representing around 4% of global demand, supported by industrial and infrastructure construction.

U.K. Concrete Formwork Market

The U.K. market in 2026 is expected to reach USD 0.20 billion, accounting for roughly ~2% of global revenues. Increased demand for rapid, high-quality construction is driving the adoption of efficient, reusable aluminum, steel, and modular systems.

Latin America

Latin America reached USD 0.47 billion in 2025, supported by residential and commercial construction growth. In Latin America, significant government-backed projects in transportation and urban development, particularly in Brazil, are fueling demand for robust, high-performance formwork.

Brazil Concrete Formwork Market

The Brazil market in 2026 is expected to reach USD 0.23 billion, accounting for roughly ~3% of global revenues. In Brazil, product demand is driven by massive infrastructure investments in roads, airports, and sanitation, and the "Minha Casa Minha Vida" affordable housing program.

Middle East & Africa

The Middle East & Africa market was valued at USD 0.38 billion in 2025, driven by infrastructure development and urban expansion projects, particularly in Gulf countries. Other factors, such as the surge in large-scale, complex infrastructure developments, roads, bridges, tunnels, and airports, require specialized, high-load formwork systems. Especially, Saudi Arabia’s Vision 2030 and infrastructure developments in the UAE are major demand drivers.

COMPETITIVE LANDSCAPE

Key Industry Players

Engineering Capability and Project Support Define Competitive Strength

The concrete formwork market is defined by companies that combine robust system engineering, durable materials, and on-site technical expertise. Competitive positioning depends on the ability to deliver safe, reusable, and adaptable formwork solutions across diverse construction environments. Key players include PERI Group, Doka Group, ULMA Construction, MEVA, RMD Kwikform, Alsina Formwork, and Acrow Group. These companies offer comprehensive system portfolios supported by rental services, engineering design, and logistics capabilities. Continuous innovation in lightweight systems, climbing formwork, and digital project planning tools strengthens their market leadership. Firms that integrate material innovation with application-driven engineering and contractor collaboration continue to dominate as construction projects grow in scale and complexity.

LIST OF KEY CONCRETE FORMWORK COMPANIES PROFILED

- Alsina (Spain)

- Aluma Systems (Canada)

- Doka (Austria)

- Kumkang Kind (South Korea)

- MEVA (Germany)

- PASCHAL (India)

- PERI (Germany)

- Suzhou TECON Construction Technology Co., Ltd (China)

- ULMA Construction (Spain)

- USA-FORM, INC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: PERI Group expanded its modular formwork and climbing system portfolio to support large-scale infrastructure and high-rise construction projects. The development focuses on faster assembly cycles, enhanced load-bearing performance, and improved safety features, strengthening PERI’s positioning in complex urban and infrastructure construction environments.

- September 2025: Doka Group introduced advanced digital planning and formwork optimization solutions integrated with its wall and slab systems. These tools enhance project planning accuracy, reduce material usage, and improve on-site productivity, reinforcing Doka’s role as a technology-driven formwork solutions provider.

- July 2025: ULMA Construction expanded its aluminum formwork system offerings aimed at mass housing and repetitive residential construction projects. The expansion targets improved reuse cycles, lightweight handling, and faster turnaround times, supporting growing demand from large residential developments in the Asia Pacific and Latin America.

- May 2025: RMD Kwikform strengthened its rental fleet and engineering support capabilities for infrastructure projects, focusing on bridge, tunnel, and transportation applications. The initiative enhances the company’s ability to support long-duration and technically demanding projects across Europe and the Middle East.

- October 2024: MEVA Formwork Systems launched upgraded wall and column formwork solutions designed to improve concrete surface finish and reduce labor intensity. The development supports contractors seeking higher-quality finishes and greater efficiency in commercial and industrial construction projects.

- August 2024: Alsina Formwork expanded its presence in emerging construction markets by increasing system availability and local engineering support. This move aims to capture demand from fast-growing residential and infrastructure projects, where the adoption of reusable modular formwork is accelerating.

REPORT COVERAGE

The global concrete formwork market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.6%from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material Type, End Use, and Region |

|

By Material Type |

Timber & Plywood Aluminum Steel Others |

|

By End Use |

Residential Commercial Industrial Infrastructure |

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 7.88 billion in 2025 and is projected to reach USD 10.81 billion by 2034.

In 2025, the market value stood at USD 4.31 billion.

Recording a CAGR of 3.6%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The residential end use segment led the market in 2025.

Expanding urban construction and infrastructure investment is expected to drive market growth.

PERI Group, Doka Group, ULMA Construction, MEVA, and RMD Kwikform are some of the prominent players in the market.

Asia Pacific held the highest market share in 2025.

The rising shift toward modular, reusable, and high-cycle formwork systems will accelerate production consumption.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us