Transmission Repair Market Size, Share & Industry Analysis, By Components (Gaskets and Seals, Transmission Filters, O-Rings, Axles, Flywheels, Gears, Clutch Plates, Pressure Plates, and Others), By Repair Type (Transmission General Repair and Transmission Overhaul), By Vehicle Type (Two-Wheelers, Passenger Vehicle, Light Commercial Vehicle, and Heavy Commercial Vehicle), By Distribution Channel (Independent Repair Workshops and OEM Workshops) and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

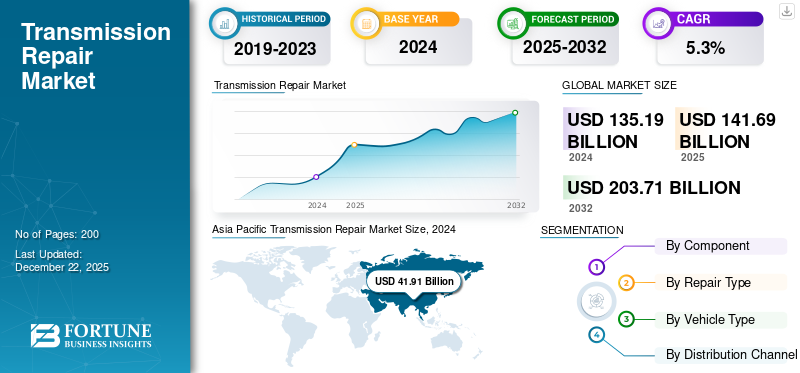

The global Transmission Repair Market size was valued at USD 141.69 billion in 2025. The market is projected to grow from USD 148.81 billion in 2026 to USD 224.58 billion by 2034, exhibiting a CAGR of 5.28% during the forecast period. Asia Pacific dominated the transmission repair market with a market share of 31.23% in 2025.

The transmission repair market is a specialized segment of the automotive repair industry focused on detecting, servicing, and rebuilding vehicle transmissions, which are critical components responsible for transferring power from the engine to the wheels. As vehicles become more advanced with complex transmission systems including manual, automatic, continuously variable (CVT), and dual-clutch transmissions the demand for skilled technicians and specialized repair services continues to grow.

Factors such as increasing vehicle lifespan, rising consumer preference for cost-effective repairs over replacements, and the growing number of vehicles on the road contribute to market expansion. Additionally, the rise of electric and hybrid vehicles is introducing new challenges and opportunities, as these models often incorporate unique transmission technologies. The market is highly competitive, with independent repair shops, franchised service centers, and dealerships competing for customer trust through expertise, warranties, and advanced diagnostic tools. As automotive technology evolves, the transmission repair industry must adapt through continuous training and investment in equipment to meet changing demands.

Schaeffler Group, Continental, and ZF are recognized as leading players in the transmission repair market due to their strong expertise in drivetrain technologies and extensive aftermarket service networks. Schaeffler excels in precision components, Continental in advanced electronics and diagnostics, while ZF dominates with genuine parts, remanufactured units, and global service support.

The COVID-19 pandemic significantly impacted the transmission repair services, causing disruptions in supply chains, labor shortages, and reduced consumer demand due to economic uncertainty. Many independent repair shops faced financial strain, with some forced to close permanently. However, as restrictions eased and economic activity resumed, pent-up demand and an increase in used car sales driven by new vehicle shortages helped the market recover.

Download Free sample to learn more about this report.

Transmission Repair Market Trends

Digitalization & Automation in Repair Shops are Re-Shaping Market

The transmission repair services are experiencing a major shift as digitalization and automation revolutionize traditional practices. Repair shops are increasingly adopting cutting-edge technologies to improve precision, productivity, and customer satisfaction. Traditionally reliant on manual expertise and mechanical knowledge, the auto repair sector is now embracing a wave of innovation. Advanced diagnostic equipment, AI-driven solutions, and digital service platforms are redefining vehicle maintenance, repair processes, and problem detection. This technological evolution is not just optimizing repair quality and speed but also elevating the entire service experience. With modern vehicles becoming more sophisticated and interconnected, repair businesses must evolve to remain competitive in today's tech-driven landscape.

Customer interactions are also being transformed by digital tools. Many repair shops now offer mobile applications and online systems that enable clients to book services, monitor repair progress, and view cost estimates easily. Some businesses even provide visual updates through photos or videos, fostering transparency and building trust. These digital solutions enhance communication between technicians and vehicle owners, minimizing errors and strengthening customer relationships. In today's fast-paced world, where convenience and openness are top priorities, these tech-enabled engagement methods are reshaping the way repair services connect with their clients. All these factors are anticipated to boost the market growth.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Average Age of Vehicles Drives the Growth of Market

The increasing average age of vehicles and average vehicle miles traveled is a key driver for the transmission repair market growth, as older vehicles are more prone to less fuel efficiency and mechanical failures and require more frequent maintenance. As transmissions accumulate mileage, components such as clutches, gears, and seals wear out, leading to a higher demand for repairs, rebuilds, and replacements. Additionally, many consumers prefer cost-effective transmission repairs over purchasing new vehicles, especially in a challenging economic climate. This trend benefits both independent repair shops and dealership service centers, as they see sustained demand for transmission diagnostics, fluid services, and part replacements. Furthermore, the growing complexity of modern transmissions, including CVTs and dual-clutch systems, as well-maintained older vehicles eventually need professional servicing, ensure steady market growth despite the rise of electric vehicles. As long as aging ICE vehicles remain on the road, the transmission repair services will continue to expand.

MARKET RESTRAINTS

Shortage of Skilled Technicians Hinders Market Growth

The automotive industry is facing critical workforce challenges such as an escalating shortage of qualified technicians. As vehicles become more technologically advanced and expert mechanics retire, service centers and dealerships are finding it increasingly difficult to recruit competent personnel. This widening skills gap, compounded by the growing technical complexity of modern repairs, is creating significant operational challenges. The industry's inability to attract and train new talent is hindering workforce replenishment, presenting a serious constraint on market expansion. Resolving this talent pipeline issue has become imperative for sustaining industry growth and meeting service demands. These workforce challenges are expected to significantly limit market development in the coming years.

MARKET OPPORTUNITES

Growing Demand for Hybrid and Electric Vehicles offers Lucrative Market Opportunities

The rapid adoption of preventive periodic maintenance services of hybrid and electric vehicles is creating new business opportunities for repair shops, particularly in EV drivetrain maintenance and specialized services for gearboxes and reduction units. The growing availability of remanufactured and refurbished transmissions also offers a more affordable solution for cost-sensitive customers. According to projections by IEA, the global EV fleet (excluding two- and three-wheelers) is set to expand dramatically from around 30 million in 2022 to approximately 240 million by 2030 under the Stated Policies Scenario (STEPS), reflecting a compound annual growth rate of roughly 30%. By 2030, EVs would account for more than 10% of the total road vehicle fleet in this scenario, with annual sales exceeding 20 million in 2025 and 40 million in 2030 making up 20% and 30% of total vehicle sales, respectively. Under the more ambitious Announced Pledges Scenario (APS), which factors in stricter government commitments, the global EV fleet could reach nearly 250 million by 2030 about 5% higher than STEPS projections. With an annual growth rate approaching 35%, EVs would represent one in seven vehicles on the road by 2030, with sales hitting 45 million that year and capturing over 35% of the market.

This accelerating shift toward electrification is expected to create fresh demand for transmission-related services, presenting opportunities for the industry.

Segmentation Analysis

By Component

Transmission Filters Dominate the Market Due to Frequent Wear and Tear

By Component, the market is segmented into Gaskets and Seals, Transmission Filters, O-Rings, Axles, Flywheels, Gears, Clutch Plates, Pressure Plates, and Others.

Transmission filters have emerged as a dominant component in transmission repair due to their critical role in maintaining system health and their frequent replacement needs, will account for 21.57% market share in 2026. As the first line of defense against contaminants, transmission filters prevent abrasive metal particles, sludge, and debris from circulating through the transmission, which can cause accelerated wear and failure. This recurring demand is further driven by the rising awareness about the importance of clean transmission fluid among vehicle owners, to prolong the lifespan of complex modern transmissions, including CVTs and dual-clutch systems.

The clutch plate component is poised for robust growth in the market, driven by increasing vehicle longevity, rising manual transmission maintenance in emerging economies, and performance-driven demand in enthusiast segments. As a wear-and-tear part, clutch plates require periodic replacement typically every 40,000 to 100,000 miles creating steady demand across passenger and commercial vehicles. In developing markets such as India, Brazil, and Southeast Asia, manual transmissions still dominate, sustaining high-volume clutch repair needs. Meanwhile, in mature markets, the growing popularity of performance and off-road vehicles (with heavy-duty clutch systems) and the trend of restoring classic cars further fuels the demand.

Moreover, other segments such as gaskets and seals, o-rings, axles, flywheels, gears, pressure plates, and others are also showing significant growth owing to their significance in the entire transmission system.

By Repair Type

Transmission General Repair Segment Dominates Market Owing to Increasing Need for Normal Service of Vehicles

By Repair Type, the market is segmented into transmission general repair and transmission overhaul.

In 2026, the transmission general repair segment is projected to lead the market with a 67.07% share. Unlike full transmission replacements or complex overhauls, general repairs such as fluid changes, filter replacements, solenoid repairs, and minor leak fixes are routine yet critical to preventing major failures. With the average age of vehicles rising globally, these preventative and corrective maintenance services are in higher demand to extend transmission lifespan and avoid costly breakdowns. Additionally, modern transmissions, particularly CVTs and dual-clutch systems, are more sensitive to fluid degradation and require frequent servicing, further boosting the need for general repairs. Repair shops benefit from this segment’s high volume and repeat customer base, as vehicle owners prioritize affordable maintenance over expensive replacements. As awareness grows about the importance of proactive transmission care, coupled with the increasing complexity of transmission systems, the general repair segment will continue to propel the overall market’s growth.

The transmission overhaul segment is projected to experience substantial growth, driven by the increasing adoption of modern transmissions, which are complex, and the rising cost of new replacements. As vehicles age and accumulate higher mileage, wear-and-tear on critical components such as gears, clutches, torque converters, and seals often necessitates a complete teardown and rebuild rather than minor repairs. This is significant for high-performance vehicles, heavy-duty trucks, and high quality luxury cars, where replacing the entire transmission is prohibitively expensive compared to a professionally overhauled unit.

By Vehicle Type

Passenger Vehicle Segment Dominates the Market Owing to Increasing Fleet Size

By vehicle type, the market is segmented into two-wheelers, passenger vehicles, light commercial vehicles, and heavy commercial vehicles.

The passenger vehicle segment is anticipated to hold a dominant market share of 32.85% in 2026, fueled by the rapid expansion of the global car fleet and rising vehicle longevity. With over 1.4 billion passenger cars on roads worldwide, a growing sheer volume of vehicles annually, ensures sustained demand for transmission maintenance and repairs. Urbanization, ride-hailing services, and the growing middle class in emerging economies are further accelerating passenger vehicle adoption, thus leading to higher repair needs. Additionally, modern transmissions such as CVTs, dual-clutch, and automated manuals are more prone to software-related issues than traditional units, requiring specialized servicing. With passenger vehicles accounting for the largest share of aftermarket repairs, this segment will remain the backbone of the transmission repair industry’s growth.

The light commercial vehicle (LCV) segment is expected to exhibit significant growth in the market, driven by the expanding e-commerce sector, last-mile delivery demand, and urban logistics. With the rise of online shopping and just-in-time supply chains, fleets of delivery vans and small trucks are accumulating higher mileage at an accelerated pace, leading to faster transmission wear-and-tear. As global trade and logistics networks expand, the LCV segment will remain a key growth driver for the market, particularly in emerging economies where small commercial vehicles dominate urban freight transport.

The two-wheelers and heavy commercial vehicle segments are also anticipated to show robust growth owing to the continuously increasing fleet size and modern transmission systems in the vehicles.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel

OEM Workshops to Dominate the Market Owing to Reliability of Service Offered

By Distribution Channel, the market is segmented into Independent Repair workshops and OEM Workshops.

The OEM workshops segment is positioned to dominate the transmission repair industry over the forecast period, leveraging brand trust, access to proprietary technology, and certified parts that appeal to vehicle owners seeking high-quality repairs, will account for 60.98% market share in 2026. Additionally, the rise of connected car technology enables OEMs to proactively notify customers of transmission issues, directing them to authorized service networks. While independent shops compete on price, OEM workshops attract consumers prioritizing long-term reliability, especially for high-end or under-warranty vehicles.

The independent repair workshops are also anticipated to grow significantly, fueled by cost competitiveness, flexibility, and expanding technical capabilities. While OEM workshops dominate for newer or warranty-covered vehicles, independent shops attract a broad customer base, particularly owners of older cars, out-of-warranty vehicles, and budget conscious consumers, by offering repairs at 30–50% lower costs than dealerships. With the global vehicle Parc aging and economic pressures pushing owners to extend car lifespans, independent repairers are well-positioned to capture growing demand, especially in emerging markets where OEM networks are less.

TRANSMISSION REPAIR MARKET REGIONAL OUTLOOK

Geographically, the market is segmented into Asia Pacific, North America, Europe and Rest of the World.

Asia Pacific

Asia Pacific Transmission Repair Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific to Dominate the Market Due to Growing Automotive Industry

The market in Asia Pacific reached USD 44.24 billion in 2025, representing 31.23% of total market revenue, and is projected to reach USD 46.79 billion in 2026. The Asia Pacific region is poised to dominate the transmission repair industry over the forecast period. Rapid urbanization, increasing vehicle ownership, and a growing automotive industry drives the demand for transmission repair services across countries. Additionally, the presence of a large number of aging vehicles, particularly in developing nations, further fuels market growth. As of November 30, 2024, India had approximately 385.1 million registered motor vehicles, according to Vahan 4.0 data maintained by the Ministry of Road Transport and Highways (MoRTH). This figure includes all types of motor vehicles. Governments in the region are also investing in better transportation infrastructure, which increases vehicle movement and the need for maintenance and repairs. With these factors combined, the Asia Pacific region is expected to lead the global transmission repair industry in the coming years. The Japan market is projected to reach USD 7.74 billion by 2026, the China market is projected to reach USD 12.54 billion by 2026, and the India market is projected to reach USD 10.03 billion by 2026.

Europe

In 2025, Europe held 25.65% of the global market, reaching a valuation of USD 36.34 billion, and is projected to grow to USD 38.23 billion in 2026. Europe is expected to be the fastest-growing region in the transmission repair market due to several factors. The region has a high concentration of aging vehicles, particularly in countries such as Germany, France, and the U.K., where consumers tend to keep cars longer, increasing the need for transmission maintenance and repairs. Additionally, stringent government regulations on vehicle emissions and safety standards encourage regular servicing, further driving demand for transmission repair services. The UK market is projected to reach USD 7.32 billion by 2026, while the Germany market is projected to reach USD 9.34 billion by 2026.

North America and Rest of the World

The North America market was valued at USD 28.65 billion in 2025, capturing 20.22% of global revenue, and is estimated to reach USD 29.98 billion in 2026. In 2025, Rest of the World generated USD 32.46 billion, contributing 22.90% to global market revenue, and is projected to grow to USD 33.81 billion in 2026. North America and the Rest of the World are also expected to witness significant growth. In North America, especially in the U.S., preference for larger vehicles, such as trucks and SUVs, which often face higher transmission wear, boosts the market growth. Meanwhile, in Rest of the World (RoW), including Latin America, and the Middle East & Africa, the market growth is fueled by rising vehicle ownership, improving economic conditions, and expanding automotive fleets in commercial sectors. Countries such as Brazil, Mexico, and South Africa are noticing increased demand for transmission repairs due to aging vehicle populations and harsh driving conditions that accelerate wear, boosting the market growth. The U.S. market is projected to reach USD 12.63 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

The transmission repair market is characterized by a highly fragmented structure, with different players dominating a significant share of the industry. This fragmentation stems from several factors, including low barriers to entry for independent repair shops, regional variations in vehicle demographics, and diverse service offerings across providers. According to the research, Schaeffler Group has emerged as the global leader in transmission repair, leveraging its strong expertise in automotive components, innovative solutions, and extensive service network. As a leading manufacturer of bearings, clutch systems, and precision components for transmissions, Schaeffler has built a reputation for high-quality repair kits, remanufactured transmissions, and diagnostic tools that cater to both manual and advanced automatic transmissions, including dual-clutch and hybrid systems.

LIST OF KEY TRANSMISSION REPAIR COMPANIES PROFILED

- Schaeffler Group (Germany)

- Borgwarner (U.S.)

- ZF Friedrichshafen AG (Germany)

- Continental AG (Germany)

- Allison Transmission

- Mister Transmission (Canada)

- AAMCO Transmissions (U.S.)

- Lee Myles Autocare & Transmission (U.S.)

- Cottman Transmission and Total Auto Care (U.S.)

- Firestone Complete Auto Care (U.S.)

- Recro Ltd (Latvia)

KEY INDUSTRY DEVELOPMENTS

- January 2025, Stellantis N.V. announced that it has acquired the remaining minority stake in its joint venture with Belgian transmission specialist Punch Powertrain, taking full ownership of the partnership established in 2018.

- March 2025 – ZF India, a leading automotive technology provider, has signed a strategic partnership agreement with a prominent Indian commercial vehicle manufacturer to supply several thousand manual and automatic transmissions for heavy-duty trucks.

- January 2024, Allison Transmission, a global leader in commercial duty automatic transmissions, has entered into a strategic partnership with SANY, one of the world's largest heavy equipment manufacturers. Under the agreement, Allison will supply its rugged Off Road Series (ORS) and Wide Body Dump Series (WBD) transmissions for integration across SANY's mining vehicle portfolio.

- June 2024, Schaeffler India, a leading motion technology company, has introduced its advanced Planetary Gear System (PGS), manufactured at its Hosur facility. The innovative solution is tailored for Dedicated Hybrid Transmission (DHT) vehicles, catering to the growing demand for hybrid mobility in the Indian market. This development reinforces Schaeffler's commitment to sustainable and efficient automotive technologies.

- September 2024, Global technology leader ZF and Chinese commercial vehicle giant Foton Motor have signed a Letter of Intent (LOI) to expand their strategic cooperation. The agreement paves the way for their existing joint venture to introduce ZF's latest hybrid transmission systems for commercial vehicles in China.

REPORT COVERAGE

The global transmission repair research report provides detailed market analysis and focuses on key aspects such as leading companies, vehicle types, design, and technology. Besides this, the report offers insights into the latest market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.28% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

By Repair Type

By Vehicle Type

By Distribution Channel

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the market was valued at USD 141.69 billion in 2025 and is projected to reach USD 224.58 billion by 2034.

The market is expected to register a CAGR of 5.28% during the forecast period of 2026-2034.

The increasing global vehicle fleet is driving the market growth.

Asia Pacific led the market in 2025.

China led the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us