Tungsten Market Size, Share & Industry Analysis, By Product (Carbide, Mill Products (Sheet, Rods, Plates), Alloys, and Others), By End-Use Industry (Automotive, Construction, Mining, Aerospace and Defense, and Others), and Regional Forecast, 2026-2034

Tungsten Market Size and Future Outlook

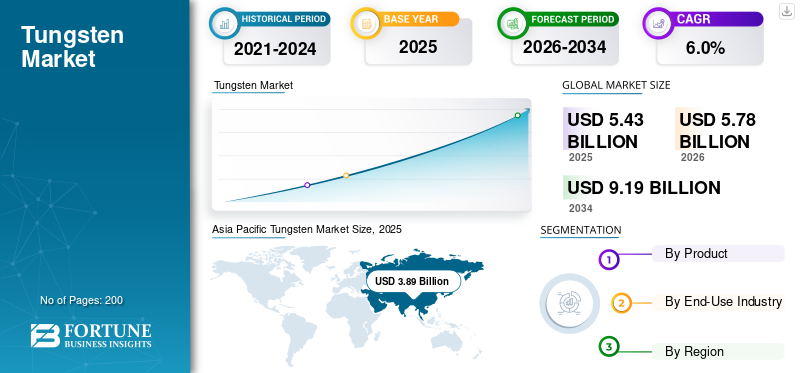

The global tungsten market size was valued at USD 5.43 billion in 2025. The market is projected to grow from USD 5.78 billion in 2026 to USD 9.19 billion by 2034, exhibiting a CAGR of 6.0% during the forecast period. Asia Pacific dominated the tungsten market with a market share of 71.64% in 2025.

The market is progressing steadily as industries increasingly demand durable, high-performance materials for arduous operations. The growing demand for wear-resistant tools, high-temperature components, and precision manufacturing solutions is driving wider adoption across the mining, construction, automotive, aerospace, and industrial equipment sectors. Tungsten-based materials offer exceptional hardness and thermal stability, enabling manufacturers to improve tool life, operational efficiency, and equipment reliability. Expansion in infrastructure development, metal fabrication, and advanced engineering activities is further driving market growth.

Key companies such as Masan High-Tech Materials Corporation, H.C. Starck Tungsten GmbH, Global Tungsten & Powders, Wolfram Bergbau und Hütten AG, and Kennametal Inc. are reinforcing their presence in the market by advancing product development, enhancing processing and manufacturing capabilities, and strengthening their global supply chains.

Download Free sample to learn more about this report.

Tungsten Market Key Takeaways

- 2025 Market Size: USD 5.43 billion

- 2026 Market Size: USD 5.78 billion

- 2034 Forecast Market Size: USD 9.19 billion

- CAGR: 6.0% from 2026–2034

- Asia Pacific dominated the tungsten market with a 71.64% share in 2025.

- The Carbide segment accounted for the largest market share in 2025.

- The Mining segment accounted for the largest market share in 2025.

North America

North America market valued at USD 0.50 billion in 2025.

Asia Pacific

Asia Pacific held 71.64% share in 2025, valued at USD 3.89 billion.

Europe

Europe market valued at USD 0.82 billion in 2025.

U.S.

Market valued at USD 0.44 billion in 2025.

Germany

Market reached a valuation of USD 0.20 billion in 2025.

Read More

TUNGSTEN MARKET TRENDS

Increasing Demand for High-Performance Wear-Resistant Tools

A prominent trend in the market is the rising demand for high-performance wear-resistant tools across the industrial sector. Industries such as mining, construction, automotive, and metalworking increasingly rely on tungsten-based materials to improve durability, precision, and operational efficiency in demanding environments. Tungsten carbide tools are widely used in drilling, cutting, and machining applications as they maintain hardness and stability even under extreme heat and pressure. As manufacturing activity expands and infrastructure projects increase worldwide, companies are adopting tungsten components to extend equipment life and reduce maintenance costs.

- According to the International Tungsten Industry Association (ITIA), approximately 60–65% of tungsten consumed globally is used in cemented carbides, which are widely used in cutting tools, drilling equipment, and wear-resistant industrial components across mining, construction, and metalworking.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expanding Mining Activities and Demand for Wear-Resistant Tools to Drive Market Growth

The tungsten market growth is strongly driven by expanding product demand in the mining industry, where equipment is exposed to extreme abrasion, pressure, and temperature. Tungsten carbide is widely used in drilling bits, cutting tools, and rock-crushing equipment as it offers exceptional hardness and durability compared to conventional materials. As the global demand for minerals, metals, and energy resources continues to rise, mining operations are expanding and requiring more reliable and long-lasting tooling solutions. Tungsten components help extend equipment life, improve operational efficiency, and reduce maintenance downtime in heavy extraction environments.

- According to the U.S. Geological Survey (USGS), about 60% of the tungsten consumed globally is used in cemented carbides, which are widely utilized in cutting tools, drilling equipment, and wear-resistant components for the mining, construction, and metalworking industries. This highlights the strong dependence of mining and heavy industrial activities on the product.

MARKET RESTRAINTS

Supply Concentration and Raw Material Dependence to Restrain Market Expansion

The market faces challenges related to the high concentration of production and dependence on limited raw material sources. A significant share of the global product supply is concentrated in a few countries, creating supply risks and price volatility for downstream industries. This dependence makes manufacturers vulnerable to export controls, trade restrictions, and fluctuations in mining output. In addition, developing new mines requires substantial capital investment, strict environmental compliance, and long project development timelines, which can limit rapid supply expansion.

- According to the U.S. Geological Survey (USGS), China accounted for about 82% of global tungsten mine production in 2025, highlighting the high concentration of supply in a single country and the potential for supply disruptions and price volatility for downstream industries.

MARKET OPPORTUNITIES

Expansion of Advanced Manufacturing and Precision Engineering to Create New Growth Opportunities

The market presents strong growth opportunities as advanced manufacturing and precision engineering activities continue to expand worldwide. Industries such as aerospace, automotive, electronics, and industrial machinery increasingly require materials that can perform reliably under extreme temperatures, pressure, and mechanical stress. Tungsten-based materials are gaining attention for their exceptional hardness, thermal stability, and durability in demanding production environments. Their use in high-precision cutting tools, wear-resistant components, and specialized alloys supports improved manufacturing efficiency and product quality.

- According to the International Tungsten Industry Association (ITIA), about two-thirds of the global tungsten is used in carbide products, particularly for cutting tools, mining equipment, and wear-resistant components used across manufacturing and heavy industries.

MARKET CHALLENGES

Recycling Complexity and Processing Costs to Create Challenges for Market Expansion

The market faces challenges related to the complex processing and recycling requirements of the products. Tungsten products, such as carbides and high-performance alloys, are extremely hard and chemically stable, making their recovery and reprocessing technically demanding. Specialized equipment, high-temperature processing, and advanced metallurgical techniques are often required to extract usable product from scrap materials. These processes can increase operational costs for manufacturers and recyclers compared to many other industrial metals.

- According to Seather Technology, tungsten has the highest melting point of all metals at about 3,422 °C (6,192 °F). This extremely high temperature stability makes the product difficult to process and recycle, requiring specialized high-temperature equipment and advanced metallurgical techniques, thereby increasing manufacturing and recovery costs for products.

Segmentation Analysis

By Product

Extensive Use in Industrial Cutting and Drilling Applications to Support the Dominance of the Carbide Segment

Based on product, the market is segmented into carbide, mill products (sheet, rods, plates), alloys, and others.

The carbide segment holds the largest tungsten market share due to its extensive use in industrial cutting, drilling, and wear-resistant applications across multiple sectors. Carbide products are widely used in mining, construction, metalworking, and manufacturing industries due to their exceptional hardness, durability, and resistance to extreme temperatures and abrasion. These properties allow carbide tools to maintain performance under demanding operating conditions, making them essential for drilling equipment, machining tools, and heavy industrial components. As global mining activities, infrastructure development, and precision manufacturing continue to expand, the demand for tungsten carbide tools and components remains strong.

- According to Kennametal, conventional tungsten carbide powders are used in hard metal-cutting tools, mining and road construction tools, dies, and wear parts, showing the strong dependence of mining operations on carbide products for drilling, excavation, and high-wear applications.

The mill products (sheet, rods, plates) segment is expected to grow at a CAGR of 5.4% over the forecast period.

By End-Use Industry

High Consumption of Wear-Resistant Tools in Extraction Work Supports the Growth of the Segment

In terms of end-use industry, the market is categorized into automotive, construction, mining, aerospace and defense, and others.

To know how our report can help streamline your business, Speak to Analyst

The mining segment holds the largest market share, driven by the extensive use of the product in drilling, cutting, excavation, and rock-crushing applications. Tungsten carbide is widely used in mining tools and wear parts as it offers exceptional hardness, corrosion resistance, and durability under harsh operating conditions. Mining equipment is exposed to continuous impact, pressure, and friction, making the product an essential material for improving tool life and reducing maintenance needs. The high demand for minerals, metals, and energy resources continues to support large-scale exploration and extraction activities worldwide.

The construction segment is expected to grow at a CAGR of 6.2% over the forecast period.

Tungsten Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Asia Pacific

Asia Pacific Tungsten Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant position in the market in 2025 with a value of USD 3.89 billion, and is expected to maintain its leading role in 2026, reaching USD 4.15 billion. The region’s leadership is supported by its strong presence in the metal’s mining, refining, powder processing, carbide production, and downstream tool manufacturing. High demand from mining, construction, automotive, electronics, and industrial machinery sectors contributes significantly to regional consumption. The region also benefits from its well-established manufacturing ecosystem and the large-scale use of carbide products in cutting, drilling, and wear-resistant applications.

China Tungsten Market

Based on Asia Pacific’s strong contribution and China’s position as the leading producer and consumer of the metal, the China market was valued at USD 2.93 billion in 2025, accounting for approximately 75.3% of regional revenues. The country’s extensive resource base, large carbide and tool manufacturing sector, and strong industrial demand from mining, construction, automotive, and machinery industries support both domestic consumption and export-oriented production.

To know how our report can help streamline your business, Speak to Analyst

North America

North America represents a mature yet steadily developing regional market, projected to reach a valuation of USD 0.50 billion in 2025. Demand is supported by the region’s strong base in mining equipment, metalworking, aerospace, defense, automotive manufacturing, and industrial machinery. The market benefits from the widespread use of carbide products in cutting tools, drilling equipment, and wear-resistant components, as well as growing interest in secure supply chains for critical materials.

U.S. Tungsten Market

The U.S. market reached a valuation of USD 0.44 billion in 2025, accounting for approximately 88.2% of regional revenues. Demand is driven by extensive product use in metal cutting, drilling, construction tools, aerospace components, and defense-related applications. The country also benefits from a strong industrial base, high demand for durable, wear-resistant materials, and an increasing focus on securing critical mineral supplies.

Europe

Europe is expected to maintain stable growth and reached a valuation of USD 0.82 billion in 2025. The region’s progress is supported by its strong industrial base in metalworking, automotive production, the aerospace sector, industrial machinery, and advanced engineering. Europe benefits from well-established capabilities in product processing, powder metallurgy, and carbide tool manufacturing, which support demand across precision cutting, drilling, and wear-resistant applications.

Germany Tungsten Market

The Germany market reached a valuation of USD 0.20 billion in 2025, accounting for approximately 24.4% of regional demand. Growth is driven by the country’s strong automotive, machinery, metalworking, and industrial equipment sectors, where the product is widely used in cutting tools, wear parts, and precision manufacturing applications. Advanced engineering capabilities, a large industrial production base, and strong demand for durable high-performance materials continue to support market expansion.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa are projected to experience steady market growth during the forecast period. The Latin America market reached a valuation of USD 0.16 billion in 2025, supported by expanding mining activities, rising infrastructure development, and increasing use of wear-resistant tools and industrial equipment. The Middle East & Africa market was valued at USD 0.05 billion in 2025, driven by growing mining operations, industrial maintenance needs, and gradual expansion in construction and energy-related applications. The increasing demand for durable drilling tools, cutting equipment, and high-performance industrial materials continues to support product consumption across both regions.

Brazil Tungsten Market

The Brazilian market was valued at USD 0.08 billion in 2025, accounting for approximately 52.5% of Latin America revenues. Demand is supported by strong mining activity, expanding infrastructure projects, and a well-established industrial base that uses the product in cutting tools, drilling equipment, and wear-resistant components. Growth in metalworking, construction equipment demand, and broader industrial development continues to support product utilization across mining and manufacturing end-use industries.

COMPETITIVE LANDSCAPE

Key Industry Players

High Capital Intensity and Integrated Processing Capabilities Shape Competition in the Market

The market remains moderately consolidated, as large-scale tungsten production requires access to reliable raw material sources, advanced processing capabilities, and consistent product quality across powders, carbides, alloys, and fabricated components. Investment in mining assets, refining, and powder metallurgy infrastructure, technical application support, regulatory compliance, and global supply networks creates significant barriers for new entrants.

Leading companies such as Masan High-Tech Materials Corporation, H.C. Starck Tungsten GmbH, Global Tungsten & Powders, Wolfram Bergbau und Hütten AG, and Kennametal Inc. are expanding processing capacity. They are also strengthening product development, improving application-specific performance, and reinforcing global distribution and customer support capabilities to maintain their positions in the market.

LIST OF KEY TUNGSTEN COMPANIES PROFILED

- Masan High-Tech Materials Corporation (Vietnam)

- C. Starck Tungsten GmbH (Germany)

- Global Tungsten & Powders (U.S.)

- Wolfram Bergbau und Hütten AG (Austria)

- Kennametal Inc (U.S.)

- Sumitomo Electric Industries, Ltd. (Japan)

- Japan New Metals Co., Ltd. (Japan)

- Umicore (Belgium)

- Buffalo Tungsten Inc. (U.S.)

- Elmet Technologies (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Sumitomo Electric Industries, Ltd. launched new coated carbide grades AC9115T/AC9125T for titanium alloy turning, using a tungsten-carbide-based composition to improve wear resistance and tool life.

- January 2025: Sumitomo Electric Industries, Ltd. launched the new coated carbide grade ACS1000 and expanded related cutter and drill lineups for stainless steel and exotic alloy milling.

- September 2024: Elmet Technologies entered a strategic collaboration and long-term offtake agreement with EQ Resources to strengthen tungsten concentrate supply for the metal’s downstream manufacturing.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size and forecast for all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also includes a detailed competitive landscape, including the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.0% from 2026-2034 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Segmentation | By Product, End-Use Industry, and Region |

| By Product |

|

| By End-Use Industry |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 5.43 billion in 2025 and is projected to reach USD 9.19 billion by 2034.

The market is slated to exhibit steady growth at a CAGR of 6.0% during the forecast period of 2026-2034.

The mining end-use industry segment leads the market.

Asia Pacific held the highest market share in 2025.

The expanding demand for wear-resistant tools and high-performance materials across mining, construction, and industrial manufacturing is a key factor driving the market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us