Utility Communication Market Size, Share & Industry Analysis, By Utility Type (Electric, Gas, Water & Wastewater, and Others), By Component (Hardware, Software, and Services), By Application (Advanced Metering Infrastructure (AMI), Grid Monitoring & Automation, Outage Management & Restoration, Demand Response & Load Management, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

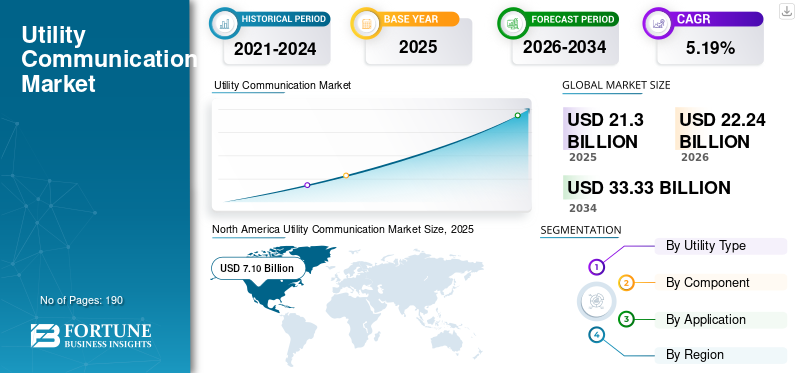

The global utility communication market size was valued at USD 21.30 billion in 2025. The market is projected to grow from USD 22.24 billion in 2026 to USD 33.33 billion by 2034, exhibiting a CAGR of 5.19% during the forecast period. North America dominated the global market with a market share of 33.33% in 2025.

The market is primarily driven by the global modernization of utility infrastructure and the rapid shift toward digital, automated, and data-driven operations. Utilities are increasingly deploying smart meters, sensors, and intelligent field devices, significantly expanding the need for reliable, secure, and real-time communication networks. Globally, hundreds of millions of smart meters are already installed, and annual installations continue to grow at a high single-digit rate, directly leading to increased demand for communication hardware, software, and managed services. Real time communication enables utilities to exchange data instantly for rapid decision-making, fault detection, and system control.

At the same time, utilities are investing heavily in distribution automation and grid monitoring to improve reliability; communication-enabled automation can reduce outage duration by 30–50% through faster fault detection and restoration. The growing integration of renewable energy sources, electric vehicles, and distributed energy resources further increases network complexity, requiring low-latency and high-bandwidth communication systems. High speed, secure communication systems that enable real-time data exchange, monitoring, and control across utility networks for reliable and efficient operations.

- For instance, in March 2025, Itron, Schneider Electric, and Microsoft announced a strategic expansion of their collaboration to deliver a Grid Edge Intelligence solution designed to give utilities better real-time visibility and control of the electric distribution grid. This joint initiative integrates each company’s strengths to address key communication and operational challenges facing modern grids.

Siemens is a global technology leader that provides communication infrastructure and solutions for utility networks, particularly in the electric power sector. Its offerings are designed to support secure, high-speed, and reliable communications across transmission, distribution, and field devices, which are essential for modern grid operations. Fiber optic communication is widely used in utility networks to provide high-speed, low-latency, and interference-free data transmission for grid monitoring, protection, and control applications. A high-speed communication system enables real time monitoring, data exchange, and control of utility networks to ensure reliable and efficient operations.

Download Free sample to learn more about this report.

UTILITY COMMUNICATION MARKET TRENDS

Widespread Adoption of Smart Metering & Two-Way Communications are Key Market Trends

The utility communication landscape is rapidly evolving as grids become more intelligent, decentralized, and data-driven. One major trend is the widespread adoption of smart metering and two-way communications, with well over one billion smart meters installed globally, driving continuous demand for reliable communication networks. Another trend is the migration from legacy narrowband systems to broadband IP-based networks and private wireless (LTE/5G), enabling higher bandwidth, lower latency, and better support for real-time grid operations.

Utilities are increasingly deploying edge computing and distributed intelligence to reduce latency and support local decision-making at substations and grid edges. The integration of distributed energy resources (DERs) such as rooftop solar and storage has increased the complexity of communication requirements, necessitating scalable and secure protocols. Cybersecurity and resilience have become top priorities, with utilities investing in encrypted and redundant communication paths to protect critical infrastructure.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Modernization of Utility Infrastructure to Drive Market Size

The utility communication market growth is being driven by the rapid modernization of utility infrastructure as aging grids are upgraded to support reliability, efficiency, and digital operations. A major driver is the expansion of smart metering and advanced metering infrastructure (AMI), with hundreds of millions of smart meters already deployed globally and annual installations continuing to rise, increasing the need for two-way, secure communication networks.

In addition, the growth of grid automation and real-time monitoring, as utilities deploy sensors, intelligent electronic devices, and automated switches to reduce outage duration; communication-enabled automation has been shown to cut restoration times by 30–50%. The increasing penetration of renewable energy sources, electric vehicles, and distributed energy resources is further driving demand for low-latency, high-bandwidth communication to manage bi-directional power flows. Distribution systems enable utilities to communicate and coordinate across substations, feeders, and end-user connections, supporting efficient monitoring, protection, and control of the power distribution network.

MARKET RESTRAINTS

High Upfront Capital Investment to Restrain Market Growth

The growth of the market is constrained by several structural and operational challenges faced by utilities. A major restraint is the high upfront capital investment required to deploy and upgrade communication infrastructure, including fiber networks, private wireless systems, and secure networking equipment, which can strain utility budgets operating under regulated tariff structures.

Long planning and approval cycles further slow deployment, as utility investments often require regulatory clearance and multi-year cost recovery, delaying large-scale communication upgrades. In addition, the complexity of integrating new communication technologies with legacy systems, as many utilities continue to operate older SCADA, PLC, and proprietary networks that are not easily compatible with modern IP-based architectures.

MARKET OPPORTUNITIES

Expansion of Private Wireless Networks is Driving Growth Opportunities

The market presents significant growth opportunities as utilities transition toward more intelligent, resilient, and digital operating models. One of the largest opportunities lies in the expansion of private wireless networks, including private LTE and emerging 5G deployments, which enable utilities to gain greater control, security, and reliability compared to public utilities.

The continued rollout of advanced metering and grid-edge intelligence offers opportunities to monetize communication upgrades through enhanced data analytics, real-time visibility, and localized control. Water and wastewater utilities, which are at an earlier stage of digitalization than electric utilities, represent a strong growth opportunity as smart metering and leak detection deployments accelerate to reduce non-revenue water losses that can exceed 30% in some regions. Energy efficient utility communication systems reduce power consumption while ensuring reliable data transmission for continuous monitoring and optimized grid operations.

MARKET CHALLENGES

Scalability & Network Performance Present Significant Challenges for Market Growth

One of the primary challenges faced by utility communication industry is the integration of diverse communication technologies across large, geographically dispersed utility assets, as utilities often operate a mix of legacy systems and modern IP-based networks. Ensuring seamless interoperability while maintaining reliability adds technical and operational complexity.

In addition, maintaining cybersecurity across expanding communication footprints, as the growing number of connected devices increases potential attack surfaces and requires continuous monitoring, updates, and compliance with critical infrastructure security standards. Scalability and network performance also pose challenges, as utilities must handle rising data volumes from smart meters, sensors, and automation devices while maintaining low latency for real-time control applications.

Segmentation Analysis

By Utility Type

Electric is Dominant as Power Grids are Most Communication-Intensive Utility Infrastructure

Based on the segmentation of utility type, the market is classified into electric, gas, waste & wastewater, and others.

In 2025, the electric segment dominated the market share. Electricity networks require real-time, two-way communication for generation, transmission, distribution, and consumption monitoring. Globally, electric utilities account for around 45–50% of total utility communication spending, driven by large-scale deployment of smart grids, SCADA systems, and Advanced Metering Infrastructure(AMI). Over 1.3 billion smart electricity meters have been installed worldwide, compared with far lower adoption in water and gas. Grid reliability standards (often >99.9% uptime) and rising investments in grid digitalization estimated at USD 300+ billion globally by 2030, further reinforce electric utilities’ market dominance.

The water & wastewater segment is experiencing the highest growth and is expected to grow at a CAGR of 6.16%.

To know how our report can help streamline your business, Speak to Analyst

By Component

Hardware is Dominant Due to Physical Infrastructure is Crucial for Building & Operating Reliable Utility Networks

On the basis of the segmentation of component, the market is classified into hardware, software, and services.

In 2025, the hardware segment dominated the global market. Utilities require large-scale deployment of smart meters, sensors, routers, switches, communication modules, and data concentrators across transmission and distribution networks. Hardware accounts for about 55–60% of total utility communication spending, as utilities prioritize long asset lifecycles and grid resilience. Globally, over 1.3 billion smart meters and millions of field devices are already installed, with continued growth driven by smart grid expansion.

The software components segment is expected to grow at a CAGR of 6.57%.

By Application

AMI Dominated Market as it Enables Continuous, Two-Way Communication Between Utilities and End Users

On the basis of the segmentation of application, the market is classified into advanced metering infrastructure (AMI), grid monitoring & automation, outage management & restoration, demand response & load management, and others.

In 2025, the advanced metering infrastructure (AMI) segment dominated the global market. AMI supports real-time meter reading, outage detection, demand response, and remote connect-disconnect, making it critical for operational efficiency. AMI accounts for around 40–45% of utility communication deployments, driven by large-scale smart meter rollouts. Globally, more than 1.3 billion smart meters are installed, with electricity meters representing over 70% of these deployments.

The grid monitoring & automation segment is expected to grow at a CAGR of 6.26%.

Utility Communication Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Utility Communication Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant utility communication market share in 2025, valued at USD 7.10 billion, and also took the leading share in 2026 with USD 7.37 billion.

Utility communication growth in North America is driven by large-scale grid modernization and mandated reliability upgrades across the U.S. and Canada. More than 70% of U.S. transmission lines are over 25 years old, pushing utilities to invest in digital communication for monitoring and automation. North America has deployed over 130 million smart meters, enabling real-time data exchange and outage management.

U.S. Utility Communication Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 6.12 billion in 2025, accounting for roughly 28.72% of the global market size.

Europe

Europe is projected to record a growth rate of 5.46% in the coming years, which is the second highest among all regions, and reach a valuation of USD 6.06 billion by 2025. Utility communication growth in Europe is driven by regulatory mandates for smart metering, grid decarbonization, and cross-border power system integration. The EU has installed over 220 million smart meters, covering nearly 75% of electricity consumers, requiring robust two-way communication networks. Renewable energy accounted for around 44% of EU electricity generation in 2024, increasing the need for real-time grid monitoring and control. Aging infrastructure is another key driver, with more than 40% of European power grids over 30 years old, accelerating digital upgrades.

Germany Utility Communication Market

The Germany market in 2025 is estimated to be around USD 1.46 billion and is estimated at around USD 1.54 billion in 2026, representing roughly 6.84% of the global utility communication revenues.

Asia Pacific

Asia Pacific is estimated to reach USD 5.84 billion in 2025 and secure the position of the third-largest region in the market. In the region, India and China are both estimated to reach USD 2.24 billion and USD 1.17 billion, respectively, in 2025.

In the Asia Pacific region, utility communication growth is closely tied to smart metering rollouts that include clear deployment timelines. East Asian countries completed their first-generation smart electricity meter rollouts early in the 2020s, with China and Japan finishing nationwide deployments by around 2023 and South Korea targeting completion by end of 2025. The total installed base in Asia Pacific was about 857 million smart meters in 2024 and is projected to reach nearly 1.3 billion by 2030, with the milestone of 1 billion expected around 2027. This ongoing expansion underpins robust utility communication networks supporting two-way data flows between meters and grid operators.

Japan Utility Communication Market

The Japan market in 2025 is estimated at around USD 0.87 billion, accounting for roughly 4.06% of global utility communication revenues.

Japan completed its nationwide smart electricity meter deployment between 2014 and 2024, installing over 80 million smart meters, which now form the core of the country’s utility communication and smart grid infrastructure.

China Utility Communication Market

China’s market is projected to be significant globally, with 2025 revenues estimated at around USD 2.24 billion, representing roughly 10.53% of the global utility communication.

India Utility Communication Market

The India market in 2025 is estimated at around USD 1.17 billion, accounting for roughly 5.49% of global revenues.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 1.51 billion in 2025.

Latin America’s utility communication growth is driven by smart metering programs deployed mainly between 2016 and 2024, with countries such as Brazil and Mexico installing over 30 million smart meters to improve grid reliability, reduce losses, and support digital utility operations.

Brazil Utility Communication Market

Brazil's market is projected to be around USD 0.74 billion in 2025, representing roughly 3.45% of the global market.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market is set to reach a valuation of USD 0.79 billion in 2025.

Utility communication in the Middle East & Africa has expanded mainly between 2017 and 2024, driven by large-scale smart metering and grid digitalization programs, with over 40 million smart meters deployed across the UAE, Saudi Arabia, South Africa, and Egypt.

GCC Utility Communication Market

The GCC market is projected to be around USD 0.38 billion in 2025, representing roughly 1.77% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors Actively Expanding Market Share Via Partnerships, Business Expansion, and Technological Advancements

The global market holds a fragmented market structure, constituting prominent players such as Siemens, Schneider Electric, and Itron, Inc., among others. Companies operating in the utility communication are adopting targeted growth strategies focused on strengthening technical capability, expanding manufacturing presence, and improving access to high-demand sectors.

- For instance, in August 2024, Siemens topped a major EMS (Energy Management System) competitive ranking, highlighting its strong digital connectivity, AI adoption, and extensive data integration capabilities, with Schneider Electric and Honeywell also recognized, showing ongoing competition in digital communication and grid monitoring technologies.

Other key players in the global market include Huawei Technologies, Ericsson, Open Systems International, and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period. Real time data communication enables utilities to continuously monitor, control, and respond instantly to grid conditions, improving reliability, efficiency, and outage management.

LIST OF KEY UTILITY COMMUNICATION COMPANIES PROFILED

- Siemens (Germany)

- Schneider Electric (France)

- Itron, Inc. (U.S.)

- Huawei Technologies (China)

- Ericsson (Sweden)

- Open Systems International (OSI) (U.S.)

- RAD Data Communications (Israel)

- XetaWave (U.S.)

- Honeywell (U.S.)

- TE Connectivity (Ireland)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Schneider Electric announced the availability of its One Digital Grid Platform, positioning it as a unified, AI-enabled software foundation for utility grid modernization. The release emphasizes modular tools that connect planning, operations, and asset management, aimed at improving resilience and lowering energy costs without forcing “rip-and-replace” infrastructure upgrades. Schneider also highlighted the platform’s role in helping utilities handle rising electricity demand and grid constraints.

- October 2025: RAD announced an enhanced security suite for its SecFlow IoT gateway, targeting private LTE/5G utility networks. The update focuses on “identity-first” protection, designed to add encryption, policy enforcement, and compliance controls while maintaining high uptime for critical infrastructure. RAD positioned SecFlow as a security anchor for next-generation utility communications, where field devices and OT networks increasingly rely on cellular/private wireless backhaul.

- March 2025: Honeywell and Verizon Business announced that Honeywell smart meters will include Verizon 5G connectivity, enabling remote access to data on energy usage, grid conditions, and equipment performance. Honeywell highlighted that meter data can feed utility management platforms (including Honeywell’s own) to improve operational visibility and enable near real-time demand insights. This reflects how cellular connectivity is increasingly used to strengthen utility communication reliability and speed.

- March 2025: Ahead of DISTRIBUTECH 2025, Siemens highlighted grid transformation technologies including digital substation approaches that combine protection, control, and secure communication networks. The messaging emphasized resilience and cybersecurity as utilities expand automation and real-time monitoring. Even when framed as “grid modernization,” the communications layer is central, connecting substations, field devices, and control centers with reliable, standards-aligned networking that supports protection and automation use cases.

- February 2025: Ericsson and the Lower Colorado River Authority (LCRA) signed a multi-year agreement to deploy a private LTE network across parts of 68 Texas counties. Ericsson described the project as supporting grid modernization with reliable, low-latency communications, including a 5G-ready core, RAN, network management, and security management capabilities. The initiative highlights the growing trend of utilities adopting utility-controlled wireless networks for operations and resilience.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.19% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Utility Type, Component, Application, and Region |

|

By Utility Type |

· Electric · Gas · Water & Wastewater · Others |

|

By Component |

· Hardware · Software · Services |

|

By Application |

· Advanced Metering Infrastructure (AMI) · Grid Monitoring & Automation · Outage Management & Restoration · Demand Response & Load Management · Others |

|

By Region |

· North America (By Utility Type, Component, Application, and Country) o U.S. o Canada · Europe (By Utility Type, Component, Application, and Country) o U.K. o Germany o France o Spain o Italy o Rest of Europe · Asia Pacific (By Utility Type, Component, Application, and Country) o China o India o Japan o Australia o South Korea o Rest of Asia Pacific · Latin America (By Utility Type, Component, Application, and Country) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Utility Type, Component, Application, and Country) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 21.30 billion in 2025 and is projected to reach USD 33.33 billion by 2034.

In 2025, the market value stood at USD 7.10 billion.

The market is expected to exhibit a CAGR of 5.19% during the forecast period.

The electric segment led the market by utility type.

Utility communications growth is driven by smart meter and grid automation deployment, rising grid-edge connectivity needs, integration of renewables and EVs, expansion of private LTE/5G networks, and increasing requirements for reliability, real-time visibility, and cybersecurity.

Siemens, Schneider Electric, and Itron, Inc., among others are some of the prominent players in the market.

North America dominated the market in 2025.

Utility communication adoption is expected to be favored by utility grid modernization initiatives, increasing smart metering and automation, growing integration of renewables and EVs, demand for real-time monitoring, and stricter reliability and cybersecurity requirements.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us