Vaccine Storage and Packaging Market Size, Share & Industry Analysis, By Material (Plastic, Glass, Paper & Paperboard, and Others), By Product Type (Vaccine Storage and Vaccine Packaging), By End-use Industry (Pharma and Biotech Companies, Diagnostic Centres, Clinical Research Organization, and Other Healthcare Facilities), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

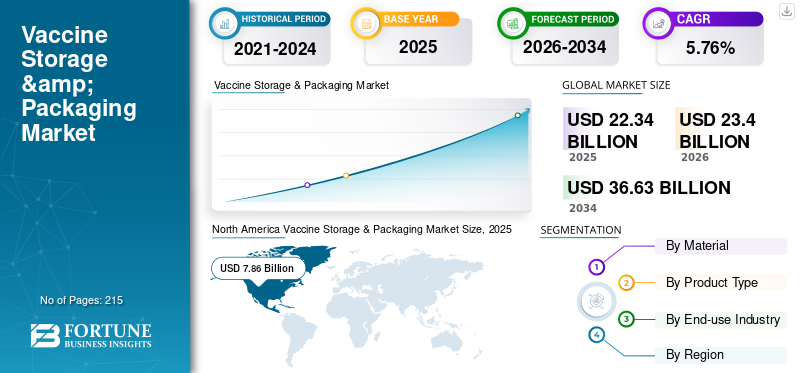

The global vaccine storage & packaging market size was valued at USD 22.34 billion in 2025 and is projected to be worth USD 23.4 billion in 2026 and reach USD 36.63 billion by 2034, exhibiting a CAGR of 5.76% during the forecast period. North America dominated the Vaccine Storage and Packaging Market with a market share of 35.19% in 2025.

The vaccine storage & packaging market refers to an industry focused on the materials, equipment, and systems used for the proper storage, handling, and transportation of vaccines. This market plays a critical role in ensuring that vaccines maintain their efficacy, safety, and stability throughout the supply chain, from production to administration. The growing demand for vaccines across the world will drive the market growth.

Gerresheimer and SCHOTT Pharma AG & Co. KGaA are the leading vaccine storage & packaging product manufacturers, accounting for the largest global market share.

Download Free sample to learn more about this report.

Vaccine Storage and Packaging Market KEY TAKEWAYS

- 2025 Market Size: USD 22.34 Billion

- 2026 Market Size: USD 23.40 Billion

- 2034 Forecast Market Size: USD 36.63 Billion

- CAGR: 5.76% from 2026–2034

- North America dominated the vaccine storage & packaging market with a 35.19% share in 2025.

- The vaccine packaging segment is projected to account for 73.84% of the market in 2026.

- The pharma & biotech companies segment is expected to hold a 42.90% market share in 2026.

North America

North America accounted for USD 7.86 billion in 2025 and is projected to reach USD 8.25 billion in 2026.

Europe

Europe generated USD 6.23 billion in 2025 and is expected to reach USD 6.50 billion in 2026.

Asia Pacific

Asia Pacific reached USD 4.68 billion in 2025 and is projected to grow to USD 4.96 billion in 2026.

U.S.

The market was valued at USD 6.84 billion in 2025 and is projected to reach USD 7.19 billion in 2026.

Japan

The market was valued at USD 0.84 billion in 2025 and is projected to reach USD 0.88 billion in 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Global Vaccination Campaigns and Increased Demand for Vaccines to Enhance Market Growth

The rising number of global vaccination initiatives, particularly those launched in response to the COVID-19 pandemic, has significantly increased the demand for vaccine storage and packaging solutions. International organizations like the World Health Organization (WHO) and governments across the world have prioritized mass vaccination programs, driving the demand for reliable storage and packaging solutions. The expansion of these programs and the need for booster doses for diseases, such as COVID-19, flu, and others have led to the growth in the production and distribution of advanced vaccine storage and packaging systems.

As of August 2024, 13.53 billion COVID-19 vaccine doses were administered globally, with 70.6% of the global population having received at least one dose. While 4.19 million vaccines were then being administered daily, only 22.3% of people in low-income countries had received at least their first vaccine by September 2022, according to official reports from national health agencies.

Technological Advancements in Cold Chain Logistics to Drive Market Expansion

Vaccine storage often requires strict temperature control, particularly for mRNA-based vaccines, which need ultra-cold storage conditions. Technological advancements in cold chain logistics, such as the development of smart containers, IoT-enabled monitoring systems, and more efficient refrigerants have enhanced the ability of medical professionals to transport vaccines across global supply chains safely. These innovations improve the transparency and accountability of temperature-sensitive shipments, minimizing risks of spoilage.

MARKET RESTRAINTS

High Costs of Cold Chain Infrastructure and Vaccine Shelf Life and Sensitivity to Impede Market Development

One of the biggest challenges in the vaccine storage and packaging market growth is the cost associated with maintaining a reliable cold chain infrastructure, particularly for vaccines that require ultra-low temperatures. The development and maintenance of cold chain systems, including specialized refrigeration units, temperature-controlled transport, and monitoring equipment, require substantial capital investment. The operational costs of maintaining these systems, especially in remote or developing regions with limited access to stable electricity, are also high.

Many vaccines, particularly those that rely on biological or genetic materials (like mRNA vaccines), are highly sensitive to environmental conditions and have short shelf lives. This requires highly specialized storage conditions to maintain efficacy of these vaccines. Once the vaccines are produced, they must be administered within a limited time frame, particularly those that are stored in multi-dose vials after being opened.

MARKET OPPORTUNITIES

Expansion of Cold Chain Infrastructure in Developing Countries Will Bring New Market Opportunities

Many developing nations still lack adequate cold chain infrastructure for storing and distributing vaccines, particularly those requiring ultra-cold temperatures. Investments in building and expanding cold chain facilities in these regions present a major opportunity for growth. Governments, non-governmental organizations, and international bodies are working to improve vaccine accessibility, which is driving the demand for portable and cost-effective storage solutions tailored for harsh environments and remote locations.

MARKET CHALLENGES

Vaccine Wastage Due to Inadequate Packaging Solutions to Affect the Market Growth

Vaccine wastage can occur when packaging solutions are not suited to the specific requirements of the vaccine or the distribution environment. For example, multi-dose vials may lead to wastage if they are not used entirely within a specified timeframe after being opened. Moreover, poorly designed packaging can expose vaccines to contamination, temperature fluctuations, or physical damage, all of which can degrade the vaccine’s efficacy.

Download Free sample to learn more about this report.

MARKET TRENDS

Shift Toward Prefilled Syringes and Single-dose Packaging to Emerge as Key Trend

There is an increasing trend of prefilled syringes and single-dose packaging, which offer several benefits over traditional multi-dose vials. These options reduce the risk of contamination, improve dosing accuracy, and simplify administration, making them ideal for large-scale vaccination campaigns. Single-dose packaging is particularly advantageous in mass immunization programs and in low-resource settings where vaccine wastage is a concern.

IMPACT OF COVID-19

The COVID-19 pandemic had a profound impact on the vaccine storage & packaging market, accelerating its growth, driving innovation, and revealing both vulnerabilities and opportunities in the global healthcare logistics. The unprecedented global demand for COVID-19 vaccines, especially mRNA-based vaccines (e.g., Pfizer-BioNTech and Moderna), which require ultra-cold storage, led to a surge in the demand for a cold chain infrastructure. Many countries, particularly those in developing regions, had insufficient cold storage capacity, driving urgent investments in refrigeration units, portable coolers, and ultra-low temperature freezers.

SEGMENTATION ANALYSIS

By Material

Plastic Dominates Market Growth Due to Its Lightweight Nature and Better Durability Than Glass

Based on material, the market is segmented into plastic, glass, paper & paperboard, and others.

The plastic segment is projected to dominate the market, accounting for a 43.07% share in 2026. Plastic is significantly lighter than glass, making it easier and cheaper to transport in large quantities. Its durability also means that plastic packaging is less prone to breakage, especially during handling and distribution, reducing the risk of contamination or vaccine loss. The segment is expected to dominate the market share of 43.07% in 2025.

Glass is the second-dominating segment. This segment is anticipated to exhibit a CAGR of 6.17% during the forecast period. Although plastic leads in terms of volume and versatility, glass remains a crucial material, especially for vaccines that require packaging materials with long-term stability or high chemical resistance. Glass is particularly valued for its inert and non-reactive nature, making it essential for certain types of vaccines and medical products.

By Product Type

Vaccine Packaging Gains Traction Due to Their Ability to Maintain Vaccine Integrity

Based on product type, the market is segmented into vaccine storage and vaccine packaging.

The vaccine packaging segment is expected to lead the market by product type, contributing 73.84% of the total market share in 2026. Vaccine packaging is essential for protecting the integrity of vaccines. It must provide a sterile environment, maintain the required temperature, and protect against light and moisture. Advanced packaging solutions, such as prefilled syringes and multi-dose vials ensure that vaccines are delivered effectively and safely to end users. The segment is expected to dominate the market share of 73.7% in 2025.

Vaccine storage is the second-dominating segment. This segment is anticipated to exhibit a CAGR of 4.8% during the forecast period. While vaccine packaging is the leading segment, vaccine storage plays a complementary role. Effective storage solutions, such as refrigeration and freezing systems are essential for meeting the conditions required by the packaging. For instance, the effectiveness of a well-designed packaging solution can be undermined if proper storage conditions are not maintained.

By End-use

Growing Production of Vaccines Increases Product Use in Pharmaceutical and Biotech Companies

Based on end-use industry, the market is segmented into pharma and biotech companies, diagnostic centers, clinical research organizations, and other healthcare facilities.

The pharma & biotech companies end-use industry segment dominated the global vaccine storage & packaging market with a market share of 42.90% in 2026. These companies are the primary developers of vaccines and responsible for researching, developing, and manufacturing vaccine formulations. These companies invest heavily in research and development to create effective vaccines for various diseases, including emerging infectious ailments.

Diagnostic centers are the second-dominating segment. While pharmaceutical and biotech companies lead in vaccine production, diagnostic centers play a crucial role in the administration and distribution of vaccines. They are responsible for conducting tests and screenings related to vaccine-preventable diseases, and they often serve as vaccination sites.

To know how our report can help streamline your business, Speak to Analyst

VACCINE STORAGE and PACKAGING MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Vaccine Storage & Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

Well-Established Pharmaceutical Industry Drives North America Market Growth

North America, particularly the U.S. and Canada, is a dominant region in the global vaccine storage & packaging market share. Regulatory agencies, such as the FDA impose stringent guidelines that necessitate the use of high-quality storage and packaging solutions, ensuring that the vaccines remain effective throughout the supply chain. The U.S. market is projected to reach USD 7.19 billion by 2026. In 2025, North America held 35.19% of the global market share, reaching a valuation of USD 7.86 billion, and is projected to grow to USD 8.25 billion in 2026.

The U.S. stands out as a leader in the global vaccine storage & packaging market, driven by its robust pharmaceutical sector and advanced research capabilities. The U.S. market size is expected to hit USD 6.84 billion in 2025. The country has a well-established cold chain infrastructure that is critical for the distribution of temperature-sensitive vaccines, including those developed for the COVID-19 virus.

- North America witnessed a growth from USD 7.86 Billion in 2025 to USD 8.25 Billion in 2026.

Europe

Cross-Border Vaccine Distribution Enhances Europe’s Market Growth

Europe is another significant market for vaccine storage & packaging, driven by a strong regulatory framework and a well-established healthcare system. Europe is anticipated to account for the second-highest market size of USD 6.23 billion in 2025, exhibiting the second-fastest growing CAGR of 4.91% during the forecast period. The European Medicines Agency (EMA) oversees vaccine approvals and mandates compliance with stringent packaging and storage standards. Countries, such as Germany, France, and the U.K. have made substantial investments in cold chain logistics and packaging technologies, particularly in response to the COVID-19 pandemic. The market in Europe reached USD 6.23 billion in 2025, representing 27.88% of total market revenue, and is projected to reach USD 6.5 billion in 2026.

The UK market is projected to reach USD 0.75 billion by 2026, while the Germany market is projected to reach USD 1.45 billion by 2026.

Asia Pacific

Rising Pharmaceutical Initiatives to Support Market Growth in Asia Pacific

Asia Pacific is experiencing rapid growth in the global vaccine storage & packaging market, fueled by increasing vaccine production capacities and rising healthcare investments. The region is likely to be the third-largest market with a value of USD 4.68 billion in 2025. The Japan market is projected to reach USD 0.88 billion by 2026, the China market is projected to reach USD 1.75 billion by 2026, and the India market is projected to reach USD 1.23 billion by 2026. Asia Pacific contributed approximately USD 4.68 billion to the global market in 2025, accounting for 20.97% share, and is expected to reach USD 4.96 billion in 2026.

On the other hand, the market in India is likely to hit USD 1.16 billion and Japan is expected to hit USD 0.84 billion in 2025.

Latin America

Strong Immunization Initiatives Supported by International Organizations Will Encourage Steady Growth in Latin America

In Latin America, the vaccine storage & packaging market is gradually expanding, driven by rising healthcare expenditures and increased vaccine access initiatives. The region is expected to hit USD 2.30 billion as the fourth-largest market in 2025. Countries, such as Brazil and Mexico are investing in improving their cold chain logistics to ensure efficient vaccine distribution. However, the region faces challenges, such as economic disparities and limited infrastructure in rural areas, which can hinder effective vaccine storage and distribution. In 2025, Latin America generated USD 2.3 billion, contributing 10.28% to global market revenue, and is projected to grow to USD 2.39 billion in 2026.

Middle East & Africa

Growing Adoption of Temperature-Controlled Storage Systems in Middle East to Drive Market Growth

The Middle East & Africa presents a mixed landscape for vaccine storage and packaging. While some countries are investing in strengthening their healthcare infrastructure and cold chain logistics, challenges, such as political instability, economic constraints, and limited access to technology can hinder the regional market’s progress. Saudi Arabia is expected to hit USD 0.53 billion in 2025. However, initiatives by organizations like the World Health Organization (WHO) and funding from international partners are helping improve vaccine distribution capabilities of these regions. The Middle East & Africa region captured 5.68% of the global market in 2025, generating USD 1.27 billion in revenue, and is projected to reach USD 1.31 billion in 2026.

FUTURE OUTLOOK

The increased focus on global health, especially after the COVID-19 pandemic, has spurred higher demand for vaccines, including routine immunizations and newer vaccines for emerging diseases. To cater to this demand, these vaccines require sophisticated packaging and storage solutions to ensure that they remain effective and safe during distribution.

The market is seeing innovations in packaging materials that offer improved temperature control, reduced waste, and enhanced protection against contamination. This includes the development of active and passive temperature-controlled packaging solutions and integration of smart packaging with real-time monitoring systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Participants to Witness Significant Growth Opportunities With New Product Launches

The global vaccine storage & packaging market is highly fragmented and competitive. A few significant players are dominating the market by offering innovative packaging solutions in the packaging industry. These major companies are constantly focusing on expanding their customer base across regions by innovating their existing range of products. The report also highlights the key developments by the manufacturers.

Major players in the industry include Gerresheimer, SCHOTT Pharma AG & Co. KGaA, Sealed Air Corporation, DHL, Stevanato, B Medical Systems, and others. Various companies offering vaccine storage packages are also analyzed in the report.

List of the Key Companies Profiled in the Report:

- Gerresheimer (Germany)

- SCHOTT Pharma AG & Co. KGaA (Germany)

- Sealed Air Corporation (U.S.)

- DHL (Germany)

- Stevanato (Italy)

- B Medical Systems (Luxembourg)

- Nipro (Japan)

- Csafe (U.S.)

- Arctiko (U.K.)

- The Cool Ice Box Company Ltd. (U.K.)

- Haier Biomedical (China)

- Cole-Parmer Instrument Company, LLC (U.S.)

- Origin Pharma Packaging (U.K.)

- DWK Life Sciences (Germany)

- Vestfrost Solutions (Denmark)

KEY INDUSTRY DEVELOPMENTS:

- October 2024 – Nipro PharmaPackaging announced the launch of its innovative D2F (Direct-to-Fill) glass vials. These vials, featuring Stevanato Group’s advanced EZ-fill technology, offer a high-quality Ready-To-Use (RTU) solution designed to meet the rigorous standards and increasing requirements of the pharmaceutical industry.

- July 2024 – CSafe announced the launch of a new reusable pallet shipper – the Silverpod MAX RE – with a host of updated features. The new and improved product will help pharmaceutical customers around the world save on disposal costs, meet their sustainability targets, and improve logistical transparency during the shipping journey.

- January 2024 – SCHOTT Pharma introduced glass vials optimized for deep-cold storage of drugs. These life-saving drugs, such as gene therapy and mRNA medications, must be frozen and transported at temperatures down to -80°C.

- August 2023 – ARCTIKO announced the launch of 22 all-new models, including 15 new pharmaceutical refrigerators and 7 new biomedical freezers. Each new model was carefully designed from the ground up to offer superior features and reliability needed for pharmaceutical and biomedical applications.

- January 2021 – Cole-Parmer announced the acquisition of ZeptoMetrix Corporation. ZeptoMetrix is a life sciences developer and manufacturer of quality control standards and verification panels used in molecular diagnostic testing for infectious diseases.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The report provides a detailed market analysis. The market overview also focuses on key aspects, such as top players, competitive landscape, product/service types, market segments, Porter’s five forces analysis, and leading segments of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the abovementioned factors, it encompasses several factors that have contributed to the market’s intelligence and growth in recent years.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

CAGR of 5.76% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material

|

|

By Product Type

|

|

|

By End-use Industry

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global vaccine storage and packaging market was valued at USD 20.49 billion in 2024 and is projected to reach USD 36.63 billion by 2034, growing at a CAGR of 5.76% during the forecast period.

The market is projected to record a CAGR of 5.76% during the forecast period.

The market size of North America was valued at USD 7.86 billion in 2025.

Plastic is the most widely used material due to its affordability and versatility. Glass is preferred for sensitive vaccines because it offers better chemical resistance and product stability.

The vaccine packaging segment currently leads in revenue, while ultra-low temperature storage solutions and prefilled syringe formats are rapidly gaining popularity due to their role in simplifying logistics and reducing contamination risk.

Major end users include pharmaceutical and biotechnology companies, diagnostic centers, clinical research organizations, hospitals, and government health agencies, which rely heavily on reliable vaccine storage and packaging systems.

North America holds the largest market share, driven by advanced healthcare infrastructure and regulatory compliance. Asia Pacific is the fastest-growing region, propelled by increased vaccine manufacturing and immunization initiatives in countries like India and China.

Key drivers include the global rise in immunization programs, growing adoption of mRNA and temperature-sensitive vaccines, and innovations in cold-chain management. Major challenges include high installation and maintenance costs and limited cold-chain infrastructure in developing regions.

Notable trends include the rise of smart cold-chain systems with IoT-enabled monitoring, solar-powered vaccine refrigerators, prefilled syringes, eco-friendly packaging, and single-dose units to reduce vaccine wastage and improve accessibility.

- 2021-2034

- 2025

- 2021-2024

- 215

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us